North America Sperm Separation Devices Market

Market Size in USD Million

USD

429.05 Million

USD

1,537.77 Million

2025

2033

USD

429.05 Million

USD

1,537.77 Million

2025

2033

| 2026 - 2033 | |

| USD 429.05 Million | |

| USD 1,537.77 Million | |

| % | |

|

North America Sperm Separation Devices Market Overview

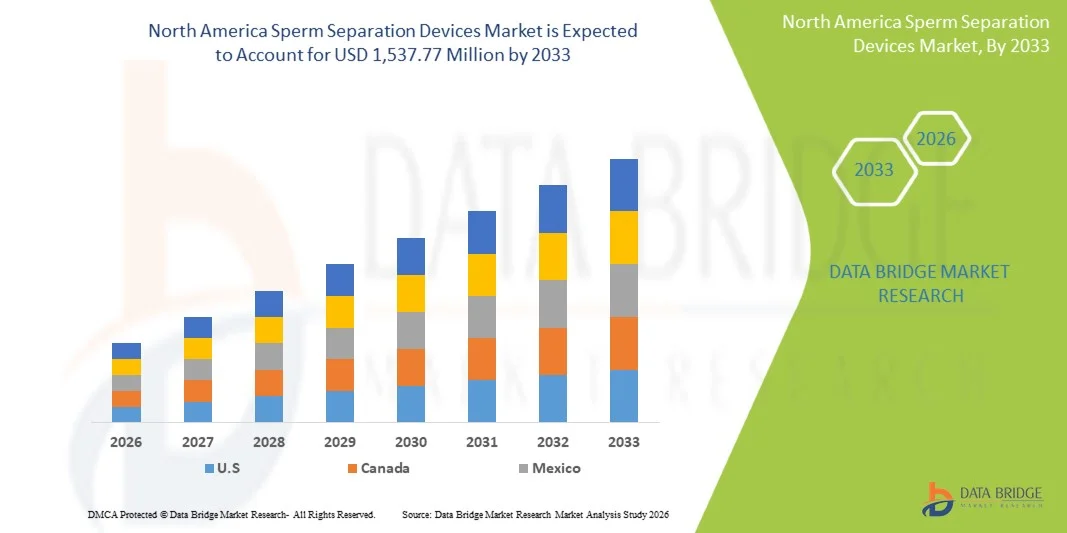

The North America sperm separation devices market was valued at USD 429.05 million in 2025 and is projected to reach USD 1,537.77 million by 2033, growing at a CAGR of 17.30% from 2026 to 2033. The market is witnessing steady expansion driven by increasing infertility cases, rising demand for assisted reproductive technologies (ART), and growing awareness regarding advanced sperm selection techniques in clinical and fertility settings.

The region’s strong healthcare infrastructure, high adoption of in vitro fertilization (IVF) procedures, and continuous technological advancements in microfluidics-based and density gradient sperm separation methods are further accelerating market growth. In addition, favorable reimbursement scenarios, expanding fertility clinic networks, and increasing preference for minimally invasive and high-precision reproductive solutions are supporting the adoption of sperm separation devices across the United States and Canada.

Key Market Trends & Insights

- United States dominated the North America sperm separation devices market with the largest revenue share of 72.46% in 2025, supported by high IVF adoption rates, advanced fertility infrastructure, and strong presence of specialized reproductive health centers.

- The Centrifugation Devices segment led the market with a 46.38% share in 2025, driven by their long-standing clinical use, cost efficiency, and strong adoption in IVF and ICSI laboratories

- Canada is expected to be the fastest-growing country with a CAGR of 7.9% from 2026 to 2033, fueled by increasing infertility treatments, expanding fertility clinic networks, and improving access to assisted reproductive technologies.

- Centrifugation-Free Devices are the fastest-growing devices type, projected to register a CAGR of 8.2%, reflecting the surge in demand for gentler sperm selection methods that preserve sperm DNA integrity.

- The On-Chip Technology segment dominated the technology category with a 42.18% revenue share in 2025, led by its precision, minimal sample handling, and ability to select high-quality sperm under controlled microfluidic environments.

- Fertility accounted for 54.67% of the market, preferred by high IVF and ICSI procedure volumes across North America.

- The Diagnostics segment is the fastest-growing application category, with a CAGR of 7.4%, driven by the increasing use of sperm analysis in infertility diagnosis and male reproductive health assessment.

Market Size & Forecast

- Global Market Value (2025): USD 429.05 Million

- Expected Market Value (2033): USD 1,537.77 Million

- Forecast CAGR (2026–2033): 17.30%

- Leading Country in 2025: United States

- Fastest Growing Country: Canada

Report Scope and North America Sperm Separation Devices Market Segmentation

|

Attributes |

North America Sperm Separation Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico |

|

Key Market Players |

· CooperSurgical, Inc. (U.S.) · Hamilton Thorne Ltd. (U.S.) · Cook (U.S.) · Merck KGaA (U.S.) · Thermo Fisher Scientific Inc. (U.S.) · MilliporeSigma (U.S.) · Irvine Scientific (U.S.) · FUJIFILM Irvine Scientific (U.S.) · Vitrolife Inc. (U.S.) · Genea Biomedx (U.S.) · Microptic S.L. (Spain) · Esco Medical Technologies (U.S.) · Nidacon International AB (Sweden) · Sage Media (U.S.) · IVFtech ApS (U.S.) · Minerva Scientific (U.S.) · ZyMōT Fertility (U.S.) · Hamilton Thorne Research (U.S.) |

|

Market Opportunities |

· Growing adoption of microfluidics-based sperm selection technologies in IVF clinics · Increasing integration of AI-driven semen analysis and automated sperm processing systems · Rising investment in fertility preservation services |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

North America Sperm Separation Devices Market Trends

Trend: Rising Adoption of Advanced Microfluidic Sperm Selection in ART Procedures

Fertility clinics across the United States and Canada are increasingly shifting from conventional centrifugation-based sperm preparation toward advanced microfluidic sperm separation technologies due to their ability to reduce oxidative stress and improve sperm DNA integrity. These systems operate through controlled fluid dynamics on lab-on-chip platforms, enabling the selection of highly mobile and morphologically superior sperm cells without mechanical damage. This transition is being reinforced by rising IVF success expectations, demand for higher embryo quality, and increasing standardization of assisted reproductive workflows across private and hospital-based fertility centers. In addition, integration of AI-driven imaging and automated semen analysis tools is improving decision-making accuracy and laboratory efficiency. This is further supported by the growing adoption of digital fertility labs in major U.S. reproductive networks, with for instance the expansion of automated microfluidic sperm sorting systems in high-volume IVF clinics in California and New York

North America Sperm Separation Devices Market Dynamics

Key Market Driver: Rising Infertility Rates and Expansion of Assisted Reproductive Technology Adoption

The steady increase in infertility prevalence across North America is a major factor driving the demand for sperm separation devices, particularly in IVF and ICSI procedures. Contributing factors include delayed childbearing, lifestyle-related health issues, obesity, stress, and underlying reproductive disorders, all of which are increasing reliance on assisted reproductive technologies. As a result, fertility clinics, hospitals, and specialized reproductive centers are expanding their ART infrastructure and investing in advanced sperm selection systems to improve fertilization success rates. Insurance coverage for fertility treatments in parts of the United States and growing awareness campaigns around reproductive health are also supporting market penetration. Moreover, technological improvements in sperm preparation methods are enabling higher clinical efficiency, reduced procedural variability, and better embryo implantation outcomes

Key Restraint/Challenge: High Cost and Limited Accessibility of Advanced Sperm Separation Technologies

Despite strong clinical demand, the adoption of advanced sperm separation devices remains constrained by high capital investment requirements and ongoing operational costs. Microfluidic systems, AI-integrated sperm analysis platforms, and automated laboratory instruments require significant upfront procurement expenditure along with recurring costs for consumables, maintenance, calibration, and software licensing. In addition, these systems demand highly trained embryologists and laboratory technicians, increasing staffing and training costs for fertility clinics. Smaller clinics and independent reproductive centers often face financial limitations, making it difficult to transition from conventional centrifugation-based methods to advanced technologies. Furthermore, disparities in healthcare infrastructure across rural and semi-urban areas limit access to high-end fertility treatments, creating uneven market penetration.

Key Market Opportunity: Integration of AI-Driven Sperm Analysis and Automated Reproductive Laboratory Systems

The integration of artificial intelligence, machine learning, and automation into sperm separation workflows represents a significant opportunity to enhance precision, scalability, and clinical outcomes in assisted reproductive technologies. AI-enabled systems can analyze sperm motility patterns, morphological characteristics, and DNA fragmentation levels in real time, enabling more accurate sperm selection for IVF procedures. Automation further reduces human intervention, minimizes procedural variability, and improves consistency across high-throughput fertility laboratories. Cloud-based data management platforms are also enabling centralized tracking of reproductive outcomes, supporting continuous optimization of treatment protocols. In addition, the combination of robotics and microfluidics is paving the way for fully automated IVF laboratory environments

North America Sperm Separation Devices Market Scope

The North America sperm separation devices market is segmented on the basis of devices, media, assisted devices, technology, application, end user, and distribution channel.

- By Devices

On the basis of devices, the North America sperm separation devices market is segmented into centrifugation devices and centrifugation-free devices. The Centrifugation Devices segment dominated the market with a 46.38% share in 2025, owing to their long-standing clinical use, cost efficiency, and strong adoption in IVF and ICSI laboratories. These systems are widely preferred due to established protocols, high sperm recovery rates, and compatibility with standard ART workflows. They are extensively used in hospitals and fertility clinics for routine sperm preparation procedures. Continuous improvements in closed-system centrifugation techniques are enhancing safety by reducing oxidative stress and contamination risks. Their affordability and availability across most fertility centers further strengthen their dominance. However, concerns regarding DNA fragmentation during processing remain a limitation.

The Centrifugation-Free Devices segment is projected to register the fastest growth at a CAGR of 8.2% from 2026 to 2033, driven by increasing demand for gentler sperm selection methods that preserve sperm DNA integrity. These devices, including microfluidic systems, eliminate mechanical stress, improving sperm quality outcomes for assisted reproductive procedures. They are gaining strong traction in advanced IVF laboratories focused on improving embryo development rates. Continuous innovation in chip-based sorting technologies is enhancing precision and efficiency. Rising preference for non-invasive and biomimetic sperm selection methods is accelerating adoption. Increasing investments in next-generation fertility technologies are further supporting growth.

- By Media

On the basis of media, the market is segmented into sperm washing media, sperm processing media, sperm freezing media, and other media. The Sperm Washing Media segment dominated the market with a 38.75% share in 2025, driven by its widespread use in routine IVF and ICSI preparation procedures. It is essential for removing seminal plasma, debris, and non-motile sperm to improve fertilization outcomes. High compatibility with centrifugation-based systems makes it the most frequently used consumable in fertility laboratories. Its standardized formulation ensures consistent sperm quality across procedures. Growing IVF cycles in North America are directly supporting demand. Continuous improvements in media formulations are enhancing sperm survival and motility rates.

The Sperm Processing Media segment is expected to witness the fastest growth at a CAGR of 7.6% from 2026 to 2033, driven by increasing demand for specialized media that optimize sperm capacitation and selection. These media are increasingly used in advanced ART procedures requiring high precision sperm preparation. They support improved fertilization efficiency and embryo quality outcomes. Rising adoption of microfluidic and AI-assisted sperm sorting systems is further boosting usage. Continuous R&D in biomimetic media composition is enhancing clinical effectiveness. Expanding IVF procedures and personalized fertility treatments are accelerating market growth.

- By Assisted Devices

On the basis of assisted devices, the market is segmented into imaging systems, incubators, cabinets, and others. The Imaging Systems segment dominated the market with a 34.62% share in 2025, driven by their critical role in sperm analysis, motility assessment, and morphology evaluation. These systems provide high-resolution visualization, enabling precise selection of viable sperm cells. Integration with AI-based analysis tools is improving diagnostic accuracy and workflow efficiency. They are widely used across IVF laboratories and fertility clinics for quality control. Increasing adoption of digital lab environments is further strengthening demand. Continuous technological advancements are enhancing imaging speed and resolution.

The Incubators segment is expected to register the fastest growth at a CAGR of 7.1% from 2026 to 2033, driven by rising demand for controlled and stable environments for sperm preservation and preparation. Modern incubators maintain optimal temperature, humidity, and CO₂ levels to ensure sperm viability. They are increasingly integrated with automated IVF laboratory systems. Growing emphasis on embryo and sperm culture optimization is supporting adoption. Technological advancements in smart incubators with remote monitoring are further accelerating growth. Expansion of fertility clinics and IVF labs is also contributing to demand.

- By Technology

On the basis of technology, the market is segmented into electrophoresis, dielectrophoresis, and on-chip technologies. The On-Chip Technology segment dominated the market with a 42.18% share in 2025, owing to its precision, minimal sample handling, and ability to select high-quality sperm under controlled microfluidic environments. These systems reduce mechanical stress and improve DNA integrity outcomes. They are increasingly used in advanced IVF laboratories and research institutions. Integration with automation and imaging systems enhances efficiency and repeatability. Growing preference for lab-on-chip solutions is strengthening adoption. Continuous innovation in microfluidic design is further supporting dominance.

The Dielectrophoresis segment is expected to witness the fastest growth at a CAGR of 8.0% from 2026 to 2033, driven by its ability to separate sperm based on electrical properties without chemical or mechanical stress. This technology improves sperm selection accuracy and reduces cellular damage. It is gaining traction in research-focused fertility centers and advanced ART labs. Increasing R&D investment in biophysical sperm sorting methods is supporting growth. Rising demand for high-quality sperm selection in IVF procedures is further accelerating adoption. Expanding use in experimental reproductive technologies is strengthening market potential.

- By Application

On the basis of application, the market is segmented into fertility, diagnostics, forensics, and others. The Fertility segment dominated the market with a 54.67% share in 2025, driven by high IVF and ICSI procedure volumes across North America. Sperm separation devices are essential for improving fertilization success rates and embryo quality. Increasing infertility cases and delayed parenthood trends are boosting demand. Fertility clinics heavily rely on these systems for routine ART workflows. Continuous technological improvements are enhancing treatment outcomes. Rising patient awareness of reproductive health is further supporting dominance.

The Diagnostics segment is expected to witness the fastest growth at a CAGR of 7.4% from 2026 to 2033, driven by increasing use of sperm analysis in infertility diagnosis and male reproductive health assessment. Advanced diagnostic tools are improving accuracy in identifying sperm abnormalities. Integration with AI-based imaging systems is enhancing diagnostic efficiency. Growing emphasis on early fertility assessment is supporting demand. Expanding clinical adoption in hospitals and diagnostic laboratories is further accelerating growth. Increasing awareness of male infertility is also contributing significantly.

- By End User

On the basis of end user, the market is segmented into hospitals, clinics, cryobanks, surgical centers, research institutes, fertility centers, IVF laboratories, and others. The Fertility Centers segment dominated the market with a 61.83% share in 2025, driven by high patient inflow, specialized ART services, and advanced reproductive infrastructure. These centers are the primary hubs for IVF and sperm processing procedures. Continuous investment in advanced laboratory technologies is strengthening their dominance. High procedural volumes and specialized expertise further support market leadership. Growing patient preference for dedicated fertility care is boosting demand. Expansion of fertility networks across the United States is further reinforcing this segment.

The IVF Laboratories segment is expected to register the fastest growth at a CAGR of 7.8% from 2026 to 2033, driven by increasing demand for highly controlled and technology-driven reproductive environments. These labs integrate advanced sperm separation systems, AI tools, and automation platforms. Rising IVF cycles and embryo optimization requirements are accelerating adoption. Continuous upgrades in lab infrastructure are enhancing procedural efficiency. Growing collaboration between research institutes and fertility providers is supporting expansion. Increasing focus on improving pregnancy success rates is further driving growth

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, third-party distributors, and others. The Direct Tender segment dominated the market with a 52.14% share in 2025, driven by large procurement contracts from hospitals, fertility centers, and IVF laboratories. Direct purchasing ensures better pricing control, service support, and customized installation. It is widely preferred by large healthcare institutions with high-volume requirements. Strong manufacturer relationships with fertility networks further support this channel. Increasing demand for integrated lab systems is boosting direct procurement. Government and institutional purchases also contribute significantly.

The Third-Party Distributors segment is expected to witness the fastest growth at a CAGR of 6.9% from 2026 to 2033, driven by expanding access to fertility technologies in smaller clinics and emerging healthcare facilities. Distributors help bridge supply chain gaps and provide localized technical support. They play a key role in expanding market penetration across mid-sized fertility centers. Increasing demand for cost-effective procurement solutions is supporting adoption. Growing presence of global medical device distributors is further strengthening this channel. Expanding IVF infrastructure in secondary cities is also accelerating growth.

North America Sperm Separation Devices Market Regional Analysis

United States dominated the North America sperm separation devices market with the largest revenue share of 72.46% in 2025, supported by high IVF adoption rates, advanced fertility infrastructure, and strong presence of specialized reproductive health centers. The country also benefits from rising infertility prevalence, increasing demand for assisted reproductive technologies, and continuous expansion of specialized fertility clinics and IVF laboratories. Growing integration of advanced sperm selection technologies, including microfluidic and AI-assisted systems, is further strengthening clinical outcomes and procedural efficiency. Increasing awareness of male infertility treatment options and supportive reimbursement frameworks in select states continue to reinforce United States leadership in the North America market.

U.S. Sperm Separation Devices Market Insight

The United States dominated the sperm separation devices market and accounted for the largest revenue share of 72.46% in 2025, supported by advanced fertility treatment infrastructure, high IVF adoption rates, and strong presence of leading reproductive healthcare providers. The country also benefits from rising infertility prevalence, increasing demand for assisted reproductive technologies, and continuous expansion of specialized fertility clinics and IVF laboratories. Growing integration of advanced sperm selection technologies, including microfluidic and AI-assisted systems, is further strengthening clinical outcomes and procedural efficiency. Increasing awareness of male infertility treatment options and supportive reimbursement frameworks in select states continue to reinforce United States leadership in the North America market.

Canada Sperm Separation Devices Market Insight

Canada is witnessing steady growth in the sperm separation devices market, driven by increasing infertility rates, expanding access to IVF services, and rising investment in reproductive healthcare infrastructure. Fertility clinics across major provinces are increasingly adopting advanced sperm selection techniques to improve treatment success rates and embryo quality outcomes. The country is also seeing gradual adoption of microfluidic and centrifugation-free technologies, supported by growing awareness of male infertility and improving healthcare accessibility. In addition, collaboration between private fertility providers and research institutions is strengthening clinical adoption and supporting market expansion across Canada.

Mexico Sperm Separation Devices Market Insight

Mexico is emerging as a developing market for sperm separation devices, supported by rising infertility cases, growing medical tourism for fertility treatments, and gradual expansion of IVF clinics in urban regions. The country is increasingly attracting patients from neighboring regions due to comparatively lower treatment costs and improving reproductive healthcare services. Fertility centers are slowly integrating conventional sperm separation techniques, with gradual adoption of advanced microfluidic systems in high-end clinics. However, limited infrastructure and uneven access to advanced technologies remain key challenges. Despite this, rising awareness of assisted reproductive technologies and increasing private healthcare investments are supporting steady market development in Mexico.

North America Sperm Separation Devices Market Share

The North America sperm separation devices industry is primarily led by well-established companies, including:

- CooperSurgical, Inc. (U.S.)

- Hamilton Thorne Ltd. (U.S.)

- Cook (U.S.)

- Merck KGaA (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- MilliporeSigma (U.S.)

- Irvine Scientific (U.S.)

- FUJIFILM Irvine Scientific (U.S.)

- Vitrolife Inc. (U.S.)

- Genea Biomedx (U.S.)

- Microptic S.L. (Spain)

- Esco Medical Technologies (U.S.)

- Nidacon International AB (Sweden)

- Sage Media (U.S.)

- IVFtech ApS (U.S.)

- Minerva Scientific (U.S.)

- ZyMōT Fertility (U.S.)

- Hamilton Thorne Research (U.S.)

Latest Developments in North America Sperm Separation Devices Market

- In June 2024, CooperSurgical, a leading fertility and reproductive health company, completed the acquisition of ZyMōt Fertility, strengthening its portfolio of microfluidic sperm separation devices used in IVF and ICSI procedures across North America. The acquisition integrated ZyMōt’s advanced lab-on-chip technology into CooperSurgical’s assisted reproductive technology (ART) offerings, enabling improved sperm selection with reduced DNA fragmentation and enhanced embryo development outcomes. This move reflects ongoing consolidation in the fertility devices space and growing demand for centrifugation-free sperm preparation solutions in clinical IVF settings

- In March 2024, CooperSurgical expanded the clinical adoption of its ZyMōt™ sperm separation device across IVF laboratories in North America, reflecting increasing use of microfluidic sperm selection technologies in assisted reproductive workflows. The system is designed to isolate highly motile sperm while minimizing oxidative stress and DNA damage, leading to improved embryo quality and higher IVF success potential. Its growing integration across fertility clinics highlights the shift toward standardized, non-invasive sperm preparation methods in modern reproductive medicine

- In January 2024, assisted reproductive technology developers in North America accelerated investments in microfluidic and AI-integrated sperm selection systems aimed at improving IVF outcomes and laboratory efficiency. These advanced systems enable precise sperm sorting, reduce manual handling errors, and support higher consistency in fertility treatments. The trend reflects increasing demand for automated and data-driven reproductive technologies in IVF laboratories and fertility clinics

- In October 2023, researchers at Texas Tech University Health Sciences Center developed a novel one-step sperm collection and selection system designed to improve efficiency in assisted reproductive technology procedures. The innovation simplifies sperm processing while maintaining high sperm viability, supporting better outcomes in IVF and ICSI applications. This development highlights growing academic contributions to next-generation sperm separation technologies and efforts to streamline laboratory workflows

- In May 2022, fertility research groups and assisted reproduction laboratories across North America increasingly adopted AI-based sperm analysis systems to improve sperm quality assessment and selection accuracy. These technologies use machine learning algorithms to evaluate sperm motility and morphology, helping embryologists select higher-quality samples while preserving sperm integrity. The development reflects a broader digital transformation in IVF laboratories and the growing role of AI in reproductive healthcare workflows

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.