North America Spinal Cord Injury Treatment Market

Market Size in USD Billion

USD

2.76 Billion

USD

4.10 Billion

2024

2032

USD

2.76 Billion

USD

4.10 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.76 Billion | |

| USD 4.10 Billion | |

| % | |

|

North America Spinal Cord Injury Treatment Market Analysis

According to an article published by International Journal of Health Policy and Management in may 2021, Partnership approaches are becoming increasingly popular within the spinal cord injury (SCI) health research field, creating opportunities to explore and learn from the successes of SCI research partnership champions. The growing collaboration and expanding partnerships in the North America spinal cord injury treatment market are pivotal in driving innovation, advancing research, and improving patient care. By combining expertise from diverse sectors, these collaborations foster the development of novel therapies, enhance rehabilitation techniques, and improve medical devices.

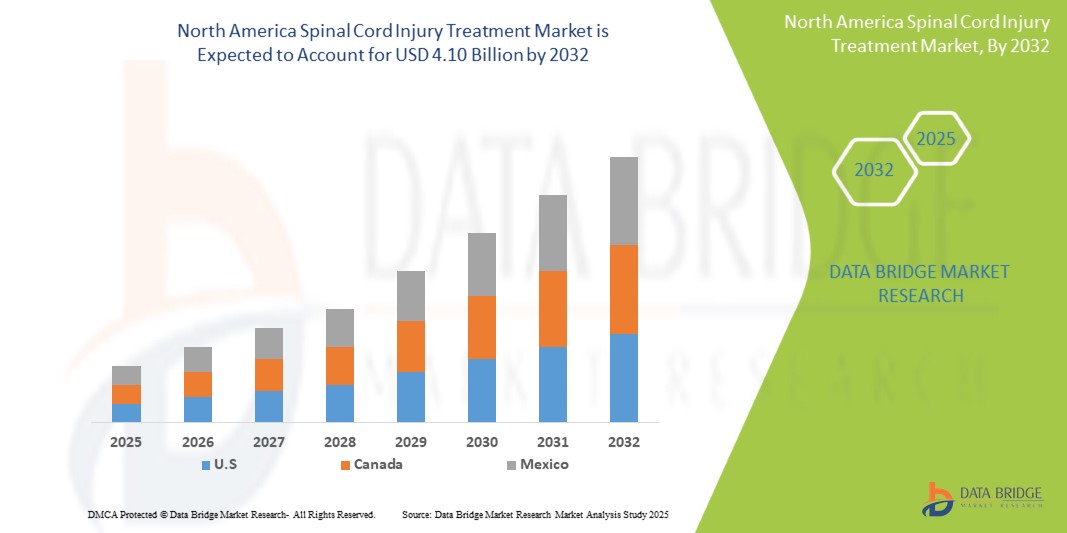

North America Spinal Cord Injury Treatment Market Size

North America spinal cord injury treatment market is expected to reach USD 4.10 billion by 2032 from USD 2.76 billion in 2024, growing at a CAGR of 5.1% in the forecast period of 2025 to 2032. In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework.

North America Spinal Cord Injury Treatment Market Trends

“Growing Collaboration and Expanding Partnerships”

In the evolving field of spinal cord injury (SCI) research, a notable trend is the increasing collaboration among academic institutions, research organizations, pharmaceutical companies, and medical device manufacturers. These alliances facilitate the sharing of expertise, resources, and funding to tackle SCI’s inherent challenges—such as limited regenerative capacity and the complexities of treatment. By uniting diverse strengths, these partnerships are accelerating the development of innovative therapies, including stem cell treatments, neuroprosthetics, and gene therapies. Moreover, industry stakeholders are joining forces to enhance rehabilitation programs, refine mobility aids, and improve diagnostic tools. An emerging trend is the collective sharing of clinical data, which deepens our understanding of SCI’s pathophysiology and helps tailor personalized treatment strategies. In addition, collaborations between North America healthcare providers and policy-makers are driving reforms that improve access to cutting-edge treatments and ensure their affordability. Overall, these collaborative trends not only raise the standard of care but also propel the worldwide effort to cure spinal cord injuries, ultimately transforming the lives of those affected.

Report Scope and North America Spinal Cord Injury Treatment Market Segmentation

|

Attributes |

North America Spinal Cord Injury Treatment Market Insights |

|

Segments Covered |

|

|

Region Covered |

U.S., Canada, Mexico, Germany, U.K., France, Russia, Italy, Spain, Turkey, Poland, Netherlands, Switzerland, Norway, Austria, Ireland, Rest of Europe, China, Japan, India, Australia, South Korea, Singapore, Thailand, Philippines, Malaysia, Indonesia, Vietnam, Taiwan, Rest of Asia-Pacific, Brazil, Argentina, Chile, Peru, Rest of South America, Saudi Arabia, U.A.E., South Africa, Egypt, Kuwait, Israel, and Rest of Middle East and Africa |

|

Key Market Players |

Novartis AG (Switzerland), Pfizer Inc. (U.S.), Medtronic (Ireland), Zimmer Biomet (U.S.), Abbott (U.S.), Amneal Pharmaceuticals LLC (U.S.), Sanofi (France), Axonis Therapeutics (U.S.), Zydus Group (India), Lineage Cell Therapeutics, Inc. (U.S.), Sun Pharmaceutical Industries Ltd. (India), Camber Pharmaceuticals, Inc. (U.S.), Dr. Reddy’s Laboratories Ltd. (India), Teva Pharmaceuticals U.S., Inc. (Israel), Niksan Pharmaceuticals (India), Covis Pharma GmbH (Switzerland), Indian Spinal Injuries Centre (India), Jubilant Cadista Pharmaceuticals Inc. (U.S.), Johnson & Johnson (U.S.), Nervgen Pharma Corp (Canada), Advacare Pharma (U.S.), Boston Scientific (U.S.), Vasudha Pharma (India), Enomark (India), Glenmark Pharmaceuticals U.S. Inc. (U.S.), Inova Pharmaceuticals (Australia), Globus Medical (U.S.), Zimvie Inc. (U.S.), and Bioaxone (Canada) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

North America Spinal Cord Injury Treatment Market Definition

Spinal cord treatment involves various medical approaches to manage injuries, diseases, or disorders affecting the spinal cord. Depending on the severity and condition, treatment may include medications like pain relievers, anti-inflammatory drugs, or muscle relaxants to reduce symptoms. Surgical interventions such as decompression or spinal fusion may be necessary for stabilization and repair. Physical therapy helps restore mobility and strengthen muscles, while rehabilitation therapy supports daily activities and independence. Assistive devices like wheelchairs and braces aid movement, and emerging treatments like stem cell therapy offer potential regenerative benefits. Psychological support and alternative therapies, including acupuncture and hydrotherapy, can also enhance recovery. A multidisciplinary approach and early intervention are crucial for better outcomes..

Global Spinal Cord Injury Treatment Market Dynamics

Drivers

Growing Collaboration and Expanding Partnerships

As SCI research continues to evolve, collaboration among academic institutions, research organizations, pharmaceutical companies, and medical device manufacturers has become increasingly vital. These partnerships enable the pooling of expertise, resources, and funding to overcome the significant challenges associated with spinal cord injuries, including limited regeneration potential and the complexity of treatment. Through collaborative efforts, the development of innovative therapies, such as stem cell treatments, neuroprosthetics, and gene therapies, has been accelerated. In addition, industry players are collaborating to create more effective rehabilitation programs, improve medical devices like mobility aids, and establish better diagnostic tools. Expanding partnerships also provide a platform for sharing clinical data, which is essential for enhancing understanding of SCI's pathophysiology and optimizing personalized treatment strategies. Moreover, collaborations between global healthcare providers and policy-makers help drive healthcare reforms, improve access to cutting-edge treatments, and ensure the affordability of SCI therapies. Ultimately, these growing partnerships not only improve the quality of care but also contribute to the global effort to find a cure for spinal cord injuries, driving innovation and improving the lives of those affected by SCI worldwide.

For instance,

- In May 2021, according to an article published by International Journal of Health Policy and Management, Partnership approaches are becoming increasingly popular within the spinal cord injury (SCI) health research field, creating opportunities to explore and learn from the successes of SCI research partnership champions

- In May 2023, according to an article published in the TechTarget Network, the Reeve Foundation and University of Alberta partnership aimed to facilitate open data sharing in spinal cord injury research to promote value, shared knowledge, and data transparency. The University of Alberta and the Reeve Foundation have launched a joint three-year project to facilitate open data sharing through the Open Data Commons for Spinal Cord Injury (ODC-SCI)

The growing collaboration and expanding partnerships in the global spinal cord injury treatment market are pivotal in driving innovation, advancing research, and improving patient care. By combining expertise from diverse sectors, these collaborations foster the development of novel therapies, enhance rehabilitation techniques, and improve medical devices. As a result, SCI patients benefit from more effective, personalized treatments and better outcomes. With continued investment in partnerships, the market is poised to make significant strides in both the treatment and potential cure for spinal cord injuries, ultimately improving the quality of life for millions of individuals worldwide.

Technological Advancements In Treatment Methods

Innovations such as stem cell therapy, neuroprosthetics, and advanced neurostimulation techniques are significantly improving recovery prospects for SCI patients. The development of robotic exoskeletons and artificial intelligence for personalized treatment plans enhances rehabilitation outcomes. In addition, breakthroughs in biomaterials for spinal cord regeneration and gene editing technologies, like CRISPR, offer new hope for restoring lost functions. These cutting-edge treatments are not only boosting the effectiveness of therapies but also expanding the market as more patients seek advanced solutions to improve quality of life.

For instance,

- In October 2023, according to an article published by NCBI, technological advancements in SCI treatment, such as the development of flexible biomaterials like hydrogels, address challenges in tissue repair. These materials support spinal cord regeneration by adapting to lesion shapes, preventing fibrosis, and promoting axonal growth

- In July 2021, according to an article published by NCBI, technological advancements in SCI treatment, such as Epidural Electrical Stimulation (EES), have shown promising results in both preclinical and clinical studies. EES enhances sensory and motor functions following spinal cord injury, highlighting its potential to improve recovery outcomes. This innovation underscores the growing role of electrical stimulation in SCI rehabilitation

Technological advancements are transforming the landscape of spinal cord injury treatment, offering new hope for patients and significantly improving recovery outcomes. Innovations in stem cell therapy, neuroprosthetics, neurostimulation, and personalized treatment powered by artificial intelligence are enhancing rehabilitation prospects. Breakthroughs in biomaterials and gene editing further push the boundaries of spinal cord regeneration, restoring lost functions and improving quality of life. As these cutting-edge treatments continue to evolve, the SCI treatment market is set to grow, providing more advanced and effective solutions to those in need.

Opportunities

Rising Geriatric Population

As people age, they often experience a decline in bone density, muscle strength, and balance, making them more susceptible to falls—a leading cause of SCI in this demographic. This demographic shift translates to a growing patient base requiring specialized treatment and rehabilitation services. The demand is not only for immediate care following an injury but also for long-term management of SCI-related complications, such as pain, spasticity, and pressure ulcers, which often require ongoing medical attention.

For instance,

- In January 2024, according to an article published by the Population Reference Bureau, the number of Americans ages 65 and older is projected to increase from 58 million in 2022 to 82 million by 2050 (a 47% increase), and the 65-and-older age group’s share of the total population is projected to rise from 17% to 23%. The growing elderly population, prone to spine injuries, will drive demand and expand the spine injury treatment market.

- In October 2019, according to an article published by National Library of Medicine, the levels of functional disability, as well as functional difficulties, activities of daily living, and physical capacity, were identified in 60% of the studies. This review indicated a high prevalence of LBP in elderly individuals and functional disability.

Moreover, the geriatric population often presents unique challenges in SCI treatment, necessitating tailored approaches and innovative solutions. Older individuals may have pre-existing conditions that complicate treatment plans and require specialized care strategies. This situation drives the need for research and development in age-specific therapies and assistive devices. Additionally, the focus extends beyond merely addressing the physical aspects of SCI to encompass mental health support, social integration, and enhanced quality of life for elderly patients. Therefore, the rising geriatric population acts as a catalyst for the growth and diversification of the SCI treatment market, compelling stakeholders to innovate and provide comprehensive care solutions tailored to the needs of older adults.

Rising Incidence of Traumatic Injuries

Traumatic injuries, such as those from motor vehicle accidents, falls, sports injuries, and violence, presents a significant opportunity for the global Spinal Cord Injury (SCI) treatment market. As the frequency of these incidents increases, so does the number of individuals suffering from spinal cord injuries, thereby expanding the potential patient base for treatment. This trend is particularly notable among younger populations, who are often more prone to engaging in high-risk activities. The consequent demand for effective and advanced treatment options, including emergency care, surgical interventions, rehabilitation services, and assistive technologies, drives growth in the SCI treatment market. Manufacturers of medical devices, pharmaceutical companies, and healthcare providers can capitalize on this trend by developing and marketing innovative treatments and services tailored to the needs of traumatic SCI patients.

For instance,

- In June 2022, according to an article published by the National Library of Medicine, the incidence and burden of SCI has increased over the last 30 years. Males and the elderly were affected to a greater degree than females and younger individuals. falls and road injuries were the leading causes of the most of the SCIs.

- In April 2024, according to an article published by the World Health Organization, globally, over 15 million people are living with spinal cord injury (SCI). Most SCI cases are due to trauma, including falls, road traffic injuries or violence.

The rising incidence of traumatic injuries fuels significant expansion in the global SCI treatment market, creating opportunities across various healthcare sectors. Focusing on innovative and effective solutions tailored to the specific needs of this patient population will be crucial. The ongoing development and provision of advanced treatments are paramount in meeting the growing demand and improving outcomes for individuals affected by spinal cord injuries.

Incorporation of Artificial Intelligence and Big Data Analytics

By leveraging AI-powered algorithms and vast amounts of patient data, researchers can identify patterns and correlations that were previously unknown, leading to the development of more effective treatment strategies and personalized care plans. AI can assist in predicting treatment outcomes, optimizing rehabilitation plans, and streamlining patient care processes. Additionally, the use of machine learning algorithms can help in identifying high-risk patients, enabling proactive interventions and reducing the likelihood of complications. This data-driven approach can also facilitate the development of more accurate diagnostic tools and predictive models, ultimately improving the quality of care for SCI patients.

For instance,

In April 2023, according to an article published by the National Library of Medicine, in acute spinal cord injury care, generative AI can analyze vital signs, lab results, and other patient data to predict the likelihood of pressure sores, urinary tract infections, or other complications. This can help clinicians intervene early, which can improve patient outcomes and reduce healthcare costs

In April 2023, according to an article published by the European Journal of Radiology, Early AI applications in spine have demonstrated remarkable utility in the assessment of the focal lesions. For example, some algorithms have been able to detect early compressive myelopathy changes and demyelinating lesions in the spinal cord, which are otherwise occult on normally appearing MR images

By leveraging AI-driven insights, manufacturers can design and engineer more effective and adaptive assistive technologies that cater to the unique needs of individual patients. Furthermore, the use of telemedicine and remote monitoring platforms can enhance patient engagement and compliance, while AI-powered chatbots and virtual assistants can provide 24/7 support and guidance to patients. By embracing AI and Big Data Analytics, stakeholders in the SCI treatment market can revolutionize patient care, enhance the efficiency of healthcare services, and drive growth in the industry. This convergence of technology and healthcare can lead to the creation of more effective treatment modalities, improved patient outcomes, and a more personalized approach to SCI care.

Restraints/Challenges

Potential Risks, Side Effects, and Complications of Spinal Cord Treatments

Some of the current treatment options for spinal cord injuries, including surgical interventions and drug therapies, carry a range of potential side effects, complications, and long-term risks. Surgical procedures, while essential for certain injuries, can sometimes result in infection, bleeding, or damage to surrounding tissues, which may further impair the patient's condition. In addition, there is always the possibility of neurological complications, such as paralysis or loss of motor functions, as a result of the surgery. For drug therapies, side effects such as nausea, dizziness, and dependency on pain medications can complicate the recovery process. In more severe cases, medications used to manage pain or inflammation can lead to long-term issues such as organ damage or immunosuppression. These risks can discourage many patients from pursuing these treatment options, especially if they are concerned about potential worsening of their health or the development of new complications. As a result, some patients may choose to avoid or delay these treatments, opting for alternative therapies or non-conventional approaches that may not have undergone extensive clinical testing. This reluctance to pursue traditional treatment methods can ultimately impact a patient's recovery journey, potentially delaying improvements or diminishing overall treatment efficacy. Moreover, for patients facing the lifelong consequences of SCI, the burden of ongoing treatment risks and complications can add to both the physical and emotional toll, making the decision to proceed with treatment even more challenging.

For Instance

- In December 2024, according to an article published by NCBI, Chronic or oncologic SCI may present with symptoms like persistent back pain, constitutional signs (weight loss, fever, anorexia), and progressive sensorimotor weakness. As the lesion grows, motor deficits, including loss of grasp and mobility, may emerge. Risk factors include smoking, prior cancer treatment, tuberculosis exposure, recent surgery, and immunosuppression.

- In January 2025, according to an article published by NCBI, Spinal cord injuries (SCI) can lead to various complications, including pneumonia, circulatory problems, muscle stiffness, autonomic dysreflexia, pressure sores, neurogenic pain, bladder and bowel issues, sexual dysfunction, and depression. Patients require careful monitoring, preventive measures, and specialized treatments, such as medications, physical therapy, and emotional support to manage these challenges.

While surgical and pharmaceutical treatments are essential for spinal cord injury recovery, they come with significant risks, including infections, neurological complications, and long-term side effects. These potential drawbacks often discourage patients from pursuing or fully committing to these treatments, fearing further harm or a reduced quality of life. As a result, patients may turn to alternative therapies, which may not always be as effective. This underscores the need for safer, more effective treatment options and emphasizes the importance of providing comprehensive care that balances potential risks with the likelihood of recovery to better support SCI patients.

Limited Understanding Related to Spinal Cord Injury Treatments

The limited understanding of the complex pathophysiology of Spinal Cord Injury (SCI) significantly hinders the development of effective treatments and poses a substantial challenge to the global SCI treatment market. SCI involves a cascade of events at the molecular and cellular levels, leading to neuronal damage, inflammation, and the formation of glial scars, all of which contribute to functional deficits. A lack of complete understanding of these intricate processes makes it difficult to identify precise therapeutic targets and design interventions that can effectively promote neural regeneration and functional recovery. As a result, many current treatments focus on managing symptoms and preventing complications rather than addressing the underlying causes of SCI.

For instance,

- In October 2020, according to an article published in the National Library of Medicine, heterogeneous factors such as complex characteristics, abundant inconsistencies and complex pathophysiologic consequences post-SCI are the major reasons for poor understanding and failure of SCI treatment

- In February 2023, according to an article published by the Oxford University Press, the pathophysiology of SCI is complicated and multifaceted, and thus individual treatments acting on a specific aspect or process are inadequate to elicit neuronal regeneration and functional recovery after SCI

This knowledge gap also hampers the development of personalized treatment strategies. SCI is not a uniform condition, and individual patients exhibit varying degrees of injury severity, neurological impairment, and functional limitations. Without a thorough understanding of the specific mechanisms driving each patient's injury, it becomes challenging to tailor treatment plans to their individual needs. This can lead to suboptimal treatment outcomes and reduced patient satisfaction. Furthermore, the limited understanding of SCI impedes the development of accurate diagnostic tools and biomarkers, making it difficult to monitor treatment efficacy and predict long-term outcomes. Overcoming this challenge requires significant investment in basic and translational research to unravel the complexities of SCI and pave the way for more effective and targeted therapies.

North America Spinal Cord Injury Treatment Market Scope

The market is segmented on the basis of type, injury type, level of injury, gender, end user, and distribution channel. The growth amongst these segments will help you analyze meagre growth segments in the industries and provide the users with a valuable market overview and market insights to help them make strategic decisions for identifying core market applications.

Type

- Non-Operative Management

- Therapy

- Rehabilitation Therapy

- Physical

- Occupational Or Speech Therapy

- Intrathecal Baclofen Therapy (Ibt)

- Rehabilitation Therapy

- Medication

- Anticonvulsants

- Corticosteroids

- Methylprednisolone

- Dexamethasone

- Antidepressants

- Ssris (Selective Serotonin Reuptake Inhibitors)

- Snris (Serotonin And Norepinephrine Reuptake Inhibitors)

- Tricyclic Drugs

- Anxiety Medications

- Antispasmodics And Muscle Relaxants

- Benzodiazepines

- Alpha-2 Agonists

- Other Gaba Agonists

- Others

- Nsaids

- Ibuprofen

- Naproxen

- Others

- Narcotic Analgesics

- Antibiotics

- Β-Lactams (Penicillins, Cephalosporins)

- Macrolides (Azithromycin, Erythromycin)

- Minocycline (Tetracycline Class)

- Dapsone

- Others (Fluoroquinolones, Aminoglycosides, Etc.)

- Therapy

- By Drug Type

- Generic

- Branded

- Medrol

- Lioresal

- Lyrica

- Neurontin

- Zanaflex

- Gralise

- Horizant

- Rilutek

- By Route Of Administration

- Oral

- Tablets

- Capsules

- Parenteral

- Transdermal Patches

- Operative Management

- Decompression Surgery

- Discectomy Or Microdiscectomy

- Laminectomy

- Posterior Microdiscectomy/ Microdecompression

- Foraminectomy

- Reconstructive Spinal Surgery

- Posterior Cervical Laminectomy

- Laminotomy

- Disc Replacement

- Artificial Cervical Disc Implantation

- Artificial Disc Surgery/ Spinal Arthroplasty

- Disc And Facet Joint Removal

- Anterior Cervical Discectomy

- Spinal Fusion

- Lumbar Spinal Fusion

- Cervical Spinal Fusion

- Sextant Fusion

- Medial Facetectomy

- Remove Two Facet Joint

- Remove One Facet Joint

- Others

- Decompression Surgery

Injury Type

- Complete Spinal Cord Injuries

- Partial Spinal Cord Injuries

Level Of Injury

- Cervical Spinal Cord Injuries

- Complete Spinal Cord Injuries

- Partial Spinal Cord Injuries

- Thoracic Spinal Cord Injuries

- Complete Spinal Cord Injuries

- Partial Spinal Cord Injuries

- Lumbar Spinal Cord Injuries

- Complete Spinal Cord Injuries

- Partial Spinal Cord Injuries

- Sacral Spinal Cord Injuries

- Complete Spinal Cord Injuries

- Partial Spinal Cord Injuries

Gender

- Male

- Adult

- Geriatic

- Children

- Female

- Adult

- Geriatic

- Children

End User

- Hospitals

- Trauma Centers

- Speciality Clinics

- Clinics

- Ambulatory And Research Centers

- Others

Distribution Channel

- Hospital Pharmacy

- Retail Pharmacy

- Online Pharmacy

North America Spinal Cord Injury Treatment Market Regional Analysis

The market is analyzed and market size insights and trends are provided by country, type, injury type, level of injury, gender, end user, and distribution channel as referenced above.

The countries covered in the spinal cord injury treatment market are U.S., Canada, and Mexico.

U.S. is expected to dominate the North America spinal cord injury treatment market due to its substantial investments in healthcare infrastructure, advanced medical research, and supportive government policies. In addition, its large population coupled with a growing demand for innovative spinal cord treatments reinforces its market leadership.

U.S. is expected to witness the highest CAGR in the spinal cord injury treatment market. This growth is driven by aggressive healthcare investments, robust government support for innovation, and rapid advancements in treatment technologies. In addition, the expanding patient base and rising demand for cutting-edge therapies contribute significantly to this accelerated growth.

The country section of the report also provides individual market impacting factors and changes in regulation in the market domestically that impacts the current and future trends of the market. Data points like down-stream and upstream value chain analysis, technical trends and porter's five forces analysis, case studies are some of the pointers used to forecast the market scenario for individual countries. Also, the presence and availability of North America brands and their challenges faced due to large or scarce competition from local and domestic brands, impact of domestic tariffs and trade routes are considered while providing forecast analysis of the country data.

North America Spinal Cord Injury Treatment Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, North America presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

North America Spinal Cord Injury Treatment Market Leaders Operating in the Market Are:

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- Medtronic (Ireland)

- Zimmer Biomet (U.S.)

- Abbott (U.S.)

- Amneal Pharmaceuticals LLC (U.S.)

- Sanofi (France)

- Axonis Therapeutics (U.S.)

- Zydus Group (India)

- Lineage Cell Therapeutics, Inc. (U.S.)

- Sun Pharmaceutical Industries Ltd. (India)

- Camber Pharmaceuticals, Inc. (U.S.)

- Dr. Reddy’s Laboratories Ltd. (India)

- Teva Pharmaceuticals U.S., Inc. (Israel)

- Niksan Pharmaceuticals (India)

- Covis Pharma GmbH (Switzerland)

- Indian Spinal Injuries Centre (India)

- Jubilant Cadista Pharmaceuticals Inc. (U.S.)

- Johnson & Johnson (U.S.)

- Nervgen Pharma Corp (Canada)

- Advacare Pharma (U.S.)

- Boston Scientific (U.S.)

- Vasudha Pharma (India)

- Enomark (India)

- Glenmark Pharmaceuticals U.S. Inc. (U.S.)

- Inova Pharmaceuticals (Australia)

- Globus Medical (U.S.)

- Zimvie Inc. (U.S.)

- Bioaxone (Canada)

Latest Developments North America Spinal Cord Injury Treatment Market

- In May 2023, Abbott announced that FDA has approved its spinal cord stimulation (SCS) devices for the treatment of chronic back pain in people who have not had or are not eligible to receive back surgery, known as non-surgical back pain.

- In January 2025, Abbott announced new four-year data showing the long-term and sustained relief that its proprietary BurstDR spinal cord stimulation (SCS) technology provides people with chronic pain, particularly pain in the back and legs. The data, which reinforces the high level of satisfaction people have with the treatment, represents outcomes from the four-year mark of a multi-year follow-up study and is being shared at the North American Neuromodulation (NANS) 2025 Annual Meeting, held in Orlando, Fla

- In August 2024 , Zimmer Biomet has signed an agreement to acquire OrthoGrid Systems, expanding its hip portfolio with OrthoGrid’s AI-driven Hip AI surgical guidance platform. The acquisition includes AI-powered fluoroscopy-based systems, enhancing surgical accuracy and efficiency

- In December 2020 , Camber Pharmaceuticals launched Baclofen Tablets, a generic version of Lioresal. Baclofen is used to treat muscle pain, spasms, and stiffness in conditions like multiple sclerosis and spinal cord injury. Available in 10 mg and 20 mg strengths, it provides relief by relaxing muscles and easing discomfort for patients with these conditions

- In December 2020 , Globus Medical announced that it has been awarded with a group purchasing agreement with Premier, a leading group purchasing organizations in the U.S. This agreement done by the company has increased its credibility in the market leading to increased revenue in future

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF THE NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET

1.4 LIMITATIONS

1.5 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 CURRENCY AND PRICING

2.5 DBMR TRIPOD DATA VALIDATION MODEL

2.6 MULTIVARIATE MODELLING

2.7 TYPE LIFELINE CURVE

2.8 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.9 DBMR MARKET POSITION GRID

2.1 MARKET END USER COVERAGE GRID

2.11 VENDOR SHARE ANALYSIS

2.12 SECONDARY SOURCES

2.13 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 PESTAL ANALYSIS

4.2 PORTERS FIVE FORCES ANALYSIS

5 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: REGULATIONS

5.1 ONGOING COMPLIANCE AND UPDATES:

6 MARKET OVERVIEW

6.1 DRIVERS

6.1.1 GROWING COLLABORATION AND EXPANDING PARTNERSHIPS

6.1.2 TECHNOLOGICAL ADVANCEMENTS IN TREATMENT METHODS

6.1.3 INCREASING HEALTHCARE EXPENDITURE

6.1.4 ENHANCED REHABILITATION TECHNIQUES

6.2 RESTRAINTS

6.2.1 POTENTIAL RISKS, SIDE EFFECTS, AND COMPLICATIONS OF SPINAL CORD TREATMENTS

6.2.2 REGULATORY BARRIERS LIMIT MARKET GROWTH BY DELAYING TREATMENT APPROVALS AND ACCESSIBILITY

6.3 OPPORTUNITIES

6.3.1 RISING GERIATRIC POPULATION

6.3.2 RISING INCIDENCE OF TRAUMATIC INJURIES

6.3.3 INCORPORATION OF ARTIFICIAL INTELLIGENCE AND BIG DATA ANALYTICS

6.4 CHALLENGES

6.4.1 LIMITED UNDERSTANDING RELATED TO SPINAL CORD INJURY TREATMENTS

6.4.2 HIGH COSTS ASSOCIATED WITH THE TREATMENTS

7 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET, BY TYPE

7.1 OVERVIEW

7.2 NON-OPERATIVE MANAGEMENT

7.2.1 THERAPY

7.2.1.1 Rehabilitation Therapy

7.2.1.1.1 PHYSICAL

7.2.1.1.2 OCCUPATIONAL OR SPEECH THERAPY

7.2.1.2 INTRATHECAL BACLOFEN THERAPY (IBT)

7.2.2 MEDICATION

7.2.2.1 ANTICONVULSANTS

7.2.2.1.1 Pregabalin

7.2.2.1.2 Gabapentin

7.2.2.1.3 Others

7.2.2.2 CORTICOSTEROIDS

7.2.2.2.1 Methylprednisolone

7.2.2.2.2 Dexamethasone

7.2.2.3 ANTIDEPRESSANTS

7.2.2.3.1 SSRIs (Selective Serotonin Reuptake Inhibitors)

7.2.2.3.2 SNRIs (Serotonin and Norepinephrine Reuptake Inhibitors)

7.2.2.3.3 Tricyclic Drugs

7.2.2.3.4 Anxiety Medications

7.2.2.4 ANTISPASMODICS AND MUSCLE RELAXANTS

7.2.2.4.1 Benzodiazepines

7.2.2.4.2 Alpha-2 Agonists

7.2.2.4.3 Other GABA Agonists

7.2.2.4.4 Others

7.2.2.5 NSAIDS

7.2.2.5.1 Ibuprofen

7.2.2.5.2 Naproxen

7.2.2.5.3 Others

7.2.2.6 NARCOTIC ANALGESICS

7.2.2.7 ANTIBIOTICS

7.2.2.7.1 β-Lactams (Penicillins, Cephalosporins)

7.2.2.7.2 Macrolides (Azithromycin, Erythromycin)

7.2.2.7.3 Minocycline (Tetracycline Type)

7.2.2.7.4 Dapsone

7.2.2.7.5 Others (Fluoroquinolones, Aminoglycosides, etc.)

7.2.2.8 Medrol

7.2.2.9 Lioresal

7.2.2.10 Lyrica

7.2.2.11 Neurontin

7.2.2.12 Zanaflex

7.2.2.13 Gralise

7.2.2.14 Rilutek

7.3 OPERATIVE MANAGEMENT

7.3.1 DECOMPRESSION SURGERY

7.3.1.1 Discectomy Or Microdiscectomy

7.3.1.2 Laminectomy

7.3.1.3 Posterior Microdiscectomy/ Microdecompression

7.3.1.4 Foraminectomy

7.3.1.5 Reconstructive Spinal Surgery

7.3.1.6 Posterior Cervical Laminectomy

7.3.1.7 Laminotomy

7.3.2 DISC REPLACEMENT

7.3.2.1 Artificial Cervical Disc Implantation

7.3.2.2 Artificial Disc Surgery/ Spinal Arthroplasty

7.3.3 DISC AND FACET JOINT REMOVAL

7.3.3.1 Anterior Cervical Discectomy

7.3.3.2 Spinal Fusion

7.3.3.2.1 Lumbar Spinal Fusion

7.3.3.2.2 Cervical Spinal Fusion

7.3.3.2.3 Sextant Fusion

7.3.3.3 Medial Facetectomy

7.3.3.3.1 REMOVE TWO FACET JOINT

7.3.3.3.2 REMOVE ONE FACET JOINT

8 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET, BY LEVEL OF INJURY

8.1 OVERVIEW

8.2 CERVICAL SPINAL CORD INJURIES

8.2.1 COMPLETE SPINAL CORD INJURIES

8.2.2 PARTIAL SPINAL CORD INJURIES

8.3 THORACIC SPINAL CORD INJURIES

8.3.1 COMPLETE SPINAL CORD INJURIES

8.3.2 PARTIAL SPINAL CORD INJURIES

8.4 LUMBAR SPINAL CORD INJURIES

8.4.1 COMPLETE SPINAL CORD INJURIES

8.4.2 PARTIAL SPINAL CORD INJURIES

8.5 SACRAL SPINAL CORD INJURIES

8.5.1 COMPLETE SPINAL CORD INJURIES

8.5.2 PARTIAL SPINAL CORD INJURIES

9 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET, BY INJURY TYPE

9.1 OVERVIEW

9.2 COMPLETE SPINAL CORD INJURIES

9.3 PARTIAL SPINAL CORD INJURIES

10 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET, BY GENDER

10.1 OVERVIEW

10.2 MALE

10.2.1 ADULT

10.2.2 GERIATIC

10.2.3 CHILDREN

10.3 FEMALE

10.3.1 ADULT

10.3.2 GERIATIC

10.3.3 CHILDREN

11 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET, BY END USER

11.1 OVERVIEW

11.2 HOSPITALS

11.3 TRAUMA CENTERS

11.4 SPECIALTY CLINICS

11.5 CLINICS

11.6 AMBULATORY AND RESEARCH CENTERS

11.7 OTHERS

12 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET, BY REGION

12.1 NORTH AMERICA

12.1.1 U.S.

12.1.2 CANADA

12.1.3 MEXICO

13 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: COMPANY LANDSCAPE

13.1 COMPANY SHARE ANALYSIS: GLOBAL

14 SWOT ANALYSIS

15 COMPANY PROFILE

15.1 PFIZER INC.

15.1.1 COMPANY SHARE ANALYSIS

15.1.2 REVENUE ANALYSIS

15.1.3 COMPANY SHARE ANALYSIS

15.1.4 PRODUCT PORTFOLIO

15.1.5 RECENT DEVELOPMENT

15.2 ABBOTT

15.2.1 COMPANY SNAPSHOT

15.2.2 REVENUE ANALYSIS

15.2.3 COMPANY SHARE ANALYSIS

15.2.4 PRODUCT PORTFOLIO

15.2.5 RECENT DEVELOPMENT

15.3 MEDTRONIC

15.3.1 COMPANY SNAPSHOT

15.3.2 REVENUE ANALYSIS

15.3.3 COMPANY SHARE ANALYSIS

15.3.4 PRODUCT PORTFOLIO

15.3.5 RECENT DEVELOPMENT

15.4 NOVARTIS AG

15.4.1 COMPANY SNAPSHOT

15.4.2 REVENUE ANALYSIS

15.4.3 COMPANY SHARE ANALYSIS

15.4.4 PRODUCT PORTFOLIO

15.4.5 RECENT DEVELOPMENT

15.5 ZIMMER BIOMET

15.5.1 COMPANY SNAPSHOT

15.5.2 REVENUE ANALYSIS

15.5.3 COMPANY SHARE ANALYSIS

15.5.4 PRODUCT PORTFOLIO

15.5.5 RECENT DEVELOPMENT

15.6 AMNEAL PHARMACEUTICALS LLC

15.6.1 COMPANY SNAPSHOT

15.6.2 REVENUE ANALYSIS

15.6.3 PRODUCT PORTFOLIO

15.6.4 RECENT DEVELOPMENT

15.7 AXONIS THERAPEUTICS

15.7.1 COMPANY SNAPSHOT

15.7.2 PRODUCT PORTFOLIO

15.7.3 RECENT DEVELOPMENT

15.8 ADVACARE PHARMA

15.8.1 COMPANY SNAPSHOT

15.8.2 PRODUCT PORTFOLIO

15.8.3 RECENT DEVELOPMENT

15.9 BIOAXONE BIOSCIENCES

15.9.1 COMPANY SNAPSHOT

15.9.2 PRODUCT PORTFOLIO

15.9.3 RECENT DEVELOPMENT

15.1 BOSTON SCIENTIFIC CORPORATION

15.10.1 COMPANY SNAPSHOT

15.10.2 REVENUE ANALYSIS

15.10.3 PRODUCT PORTFOLIO

15.10.4 RECENT DEVELOPMENT

15.11 COVIS PHARMA GMBH.

15.11.1 COMPANY SNAPSHOT

15.11.2 PRODUCT PORTFOLIO

15.11.3 RECENT DEVELOPMENT

15.12 CAMBER PHARMACEUTICALS, INC

15.12.1 COMPANY SNAPSHOT

15.12.2 PRODUCT PORTFOLIO

15.12.3 RECENT DEVELOPMENT

15.13 DR. REDDY’S LABORATORIES LTD

15.13.1 COMPANY SNAPSHOT

15.13.2 REVENUE ANALYSIS

15.13.3 PRODUCT PORTFOLIO

15.13.4 RECENT DEVELOPMENT

15.14 ENOMARK PHARMA

15.14.1 COMPANY SNAPSHOT

15.14.2 PRODUCT PORTFOLIO

15.14.3 RECENT DEVELOPMENT

15.15 GLENMARK PHARMACEUTICALS INC.,

15.15.1 COMPANY SNAPSHOT

15.15.2 REVENUE ANALYSIS

15.15.3 PRODUCT PORTFOLIO

15.15.4 RECENT DEVELOPMENT

15.16 GLOBUS MEDICAL

15.16.1 COMPANY SNAPSHOT

15.16.2 REVENUE ANALYSIS

15.16.3 PRODUCT PORTFOLIO

15.16.4 RECENT DEVELOPMENTS/NEWS

15.17 INOVA PHARMACEUTICALS

15.17.1 COMPANY SNAPSHOT

15.17.2 PRODUCT PORTFOLIO

15.17.3 RECENT DEVELOPMENT

15.18 INDIAN SPINAL INJURIES CENTRE

15.18.1 COMPANY SNAPSHOT

15.18.2 PRODUCT PORTFOLIO

15.18.3 RECENT DEVELOPMENT

15.19 JUBILANT CADISTA PHARMACEUTICALS INC.

15.19.1 COMPANY SNAPSHOT

15.19.2 PRODUCT PORTFOLIO

15.19.3 RECENT DEVELOPMENT

15.2 JOHNSON & JOHNSON SERVICES, INC

15.20.1 COMPANY SNAPSHOT

15.20.2 REVENUE ANALYSIS

15.20.3 PRODUCT PORTFOLIO

15.20.4 RECENT DEVELOPMENTS

15.21 LINEAGE CELL THERAPEUTICS, INC.

15.21.1 COMPANY SNAPSHOT

15.21.2 ANNUAL REVENUE

15.21.3 PRODUCT PORTFOLIO

15.21.4 RECENT DEVELOPMENT

15.22 NERVGEN PHARMA CORP.

15.22.1 COMPANY SNAPSHOT

15.22.2 REVENUE ANALYSIS

15.22.3 PRODUCT PIPELINE PORTFOLIO

15.22.4 RECENT DEVELOPMENT

15.23 NIKSAN PHARMACEUTICAL

15.23.1 COMPANY SNAPSHOT

15.23.2 PRODUCT PORTFOLIO

15.23.3 RECENT DEVELOPMENT

15.24 SUN PHARMACEUTICAL INDUSTRIES LTD.

15.24.1 COMPANY SNAPSHOT

15.24.2 REVENUE ANALYSIS

15.24.3 PRODUCT PORTFOLIO

15.24.4 RECENT DEVELOPMENT

15.25 SANOFI

15.25.1 COMPANY SNAPSHOT

15.25.2 REVENUE ANALYSIS

15.25.3 PRODUCT PORTFOLIO

15.25.4 RECENT DEVELOPMENT

15.26 TEVA PHARMACEUTICALS USA, INC.

15.26.1 COMPANY SNAPSHOT

15.26.2 REVENUE ANALYSIS

15.26.3 PRODUCT PORTFOLIO

15.26.4 RECENT DEVELOPMENT

15.27 VASUDHA PHARMA

15.27.1 COMPANY SNAPSHOT

15.27.2 PRODUCT PORTFOLIO

15.27.3 RECENT DEVELOPMENT

15.28 ZIMVIE INC.

15.28.1 COMPANY SNAPSHOT

15.28.2 REVENUE ANALYSIS

15.28.3 PRODUCT PORTFOLIO

15.28.4 RECENT NEWS

15.29 ZYDUS GROUP

15.29.1 COMPANY SNAPSHOT

15.29.2 REVENUE ANALYSIS

15.29.3 PRODUCT PORTFOLIO

15.29.4 RECENT DEVELOPMENT

16 QUESTIONNAIRE

17 RELATED REPORTS

List of Table

TABLE 1 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 2 NORTH AMERICA NON-OPERATIVE MANAGEMENT IN SPINAL CORD INJURY TREATMENT MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 3 NORTH AMERICA NON-OPERATIVE MANAGEMENT IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 4 NORTH AMERICA THERAPY IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 5 NORTH AMERICA REHABILITATION THERAPY IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 6 NORTH AMERICA MEDICATION IN SPINAL CORD INJURY TREATMENT IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 7 NORTH AMERICA ANTICONVULSANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 8 NORTH AMERICA ANTICONVULSANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (THOUSAND UNITS)

TABLE 9 NORTH AMERICA ANTICONVULSANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD/UNITS)

TABLE 10 NORTH AMERICA CORTICOSTEROIDS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 11 NORTH AMERICA CORTICOSTEROIDS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (THOUSAND UNITS)

TABLE 12 NORTH AMERICA CORTICOSTEROIDS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD/UNITS)

TABLE 13 NORTH AMERICA ANTIDEPRESSANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 14 NORTH AMERICA ANTIDEPRESSANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (THOUSAND UNITS)

TABLE 15 NORTH AMERICA ANTIDEPRESSANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD/UNITS)

TABLE 16 NORTH AMERICA ANTISPASMODICS AND MUSCLE RELAXANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE 2018-2032 (USD THOUSAND)

TABLE 17 NORTH AMERICA ANTISPASMODICS AND MUSCLE RELAXANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (THOUSAND UNITS)

TABLE 18 NORTH AMERICA ANTISPASMODICS AND MUSCLE RELAXANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD/UNITS)

TABLE 19 NORTH AMERICA NSAIDS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 20 NORTH AMERICA NSAIDS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (THOUSAND UNITS)

TABLE 21 NORTH AMERICA NSAIDS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD/UNITS)

TABLE 22 NORTH AMERICA ANTIBIOTICS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 23 NORTH AMERICA ANTIBIOTICS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (THOUSAND UNITS)

TABLE 24 NORTH AMERICA ANTIBIOTICS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD/UNITS)

TABLE 25 NORTH AMERICA MEDICATION IN SPINAL CORD INJURY TREATMENT MARKET, BY DRUG TYPE, 2018-2032 (USD THOUSAND)

TABLE 26 NORTH AMERICA BRANDED IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 27 NORTH AMERICA MEDICATION IN SPINAL CORD INJURY TREATMENT MARKET, BY ROUTE OF ADMINISTRATION, 2018-2032 (USD THOUSAND)

TABLE 28 NORTH AMERICA ORAL IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 29 NORTH AMERICA OPERATIVE MANAGEMENT IN SPINAL CORD INJURY TREATMENT MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 30 NORTH AMERICA OPERATIVE MANAGEMENT IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 31 NORTH AMERICA DECOMPRESSION SURGERY IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 32 NORTH AMERICA DISC REPLACEMENT IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 33 NORTH AMERICA DISC AND FACET JOINT REMOVAL IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 34 NORTH AMERICA SPINAL FUSION IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 35 NORTH AMERICA MEDIAL FACETECTOMY IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE 2018-2032 (USD THOUSAND)

TABLE 36 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET, BY LEVEL OF INJURY, 2018-2032 (USD THOUSAND)

TABLE 37 NORTH AMERICA CERVICAL SPINAL CORD INJURIES IN SPINAL CORD INJURY TREATMENT MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 38 NORTH AMERICA CERVICAL SPINAL CORD INJURIES IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 39 NORTH AMERICA THORACIC SPINAL CORD INJURIES IN SPINAL CORD INJURY TREATMENT MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 40 NORTH AMERICA THORACIC SPINAL CORD INJURIES IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 41 NORTH AMERICA LUMBAR SPINAL CORD INJURIES IN SPINAL CORD INJURY TREATMENT MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 42 NORTH AMERICA LUMBAR SPINAL CORD INJURIES IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 43 NORTH AMERICA SACRAL SPINAL CORD INJURIES IN SPINAL CORD INJURY TREATMENT MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 44 NORTH AMERICA SACRAL SPINAL CORD INJURIES IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 45 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET, BY INJURY TYPE, 2018-2032 (USD THOUSAND)

TABLE 46 NORTH AMERICA COMPLETE SPINAL CORD INJURIES IN SPINAL CORD INJURY TREATMENT MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 47 NORTH AMERICA PARTIAL SPINAL CORD INJURIES IN SPINAL CORD INJURY TREATMENT MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 48 NORTH AMERICA SPINAL CORD INJURY TREA TMENT MARKET, BY GENDER, 2018-2032 (USD THOUSAND)

TABLE 49 NORTH AMERICA MALE IN SPINAL CORD INJURY TREATMENT MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 50 NORTH AMERICA MALE IN SPINAL CORD INJURY TREATMENT MARKET, BY AGE GROUP, 2018-2032 (USD THOUSAND)

TABLE 51 NORTH AMERICA FEMALE IN SPINAL CORD INJURY TREATMENT MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 52 NORTH AMERICA FEMALE IN SPINAL CORD INJURY TREATMENT MARKET, BY AGE GROUP, 2018-2032 (USD THOUSAND)

TABLE 53 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET, BY END USER, 2018-2032 (USD THOUSAND)

TABLE 54 NORTH AMERICA HOSPITALS IN SPINAL CORD INJURY TREATMENT MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 55 NORTH AMERICA TRAUMA CENTERS IN SPINAL CORD INJURY TREATMENT MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 56 NORTH AMERICA SPECIALITY CLINICS IN SPINAL CORD INJURY TREATMENT MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 57 NORTH AMERICA CLINICS IN SPINAL CORD INJURY TREATMENT MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 58 NORTH AMERICA AMBULATORY AND RESEARCH CENTERS IN SPINAL CORD INJURY TREATMENT MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 59 NORTH AMERICA OTHERS IN SPINAL CORD INJURY TREATMENT MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 60 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET, BY COUNTRY, 2018-2032 (USD THOUSAND)

TABLE 61 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 62 NORTH AMERICA NON-OPERATIVE MANAGEMENT IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 63 NORTH AMERICA THERAPY IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 64 NORTH AMERICA REHABILITATION THERAPY IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 65 NORTH AMERICA MEDICATION IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 66 NORTH AMERICA ANTICONVULSANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 67 NORTH AMERICA ANTICONVULSANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (THOUSAND UNITS)

TABLE 68 NORTH AMERICA ANTICONVULSANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD/UNITS)

TABLE 69 NORTH AMERICA CORTICOSTEROIDS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 70 NORTH AMERICA CORTICOSTEROIDS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (THOUSAND UNITS)

TABLE 71 NORTH AMERICA CORTICOSTEROIDS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD/UNITS)

TABLE 72 NORTH AMERICA ANTIDEPRESSANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 73 NORTH AMERICA ANTIDEPRESSANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (THOUSAND UNITS)

TABLE 74 NORTH AMERICA ANTIDEPRESSANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD/UNITS)

TABLE 75 NORTH AMERICA ANTISPASMODICS AND MUSCLE RELAXANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 76 NORTH AMERICA ANTISPASMODICS AND MUSCLE RELAXANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (THOUSAND UNITS)

TABLE 77 NORTH AMERICA ANTISPASMODICS AND MUSCLE RELAXANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD/UNITS)

TABLE 78 NORTH AMERICA NSAIDS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 79 NORTH AMERICA NSAIDS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (THOUSAND UNITS)

TABLE 80 NORTH AMERICA NSAIDS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD/UNITS)

TABLE 81 NORTH AMERICA ANTIBIOTICS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 82 NORTH AMERICA ANTIBIOTICS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (THOUSAND UNITS)

TABLE 83 NORTH AMERICA ANTIBIOTICS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD/UNITS)

TABLE 84 NORTH AMERICA OPERATIVE MANAGEMENT IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 85 NORTH AMERICA DECOMPRESSION SURGERY IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 86 NORTH AMERICA DISC REPLACEMENT IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 87 NORTH AMERICA DISC AND FACET JOINT REMOVAL IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 88 NORTH AMERICA SPINAL FUSION IN ANTERIOR CERVICAL DISCECTOMY IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 89 NORTH AMERICA MEDIAL FACETECTOMY IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 90 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET, BY INJURY TYPE, 2018-2032 (USD THOUSAND)

TABLE 91 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET, BY LEVEL OF INJURY, 2018-2032 (USD THOUSAND)

TABLE 92 NORTH AMERICA CERVICAL SPINAL CORD INJURIES IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 93 NORTH AMERICA THORACIC SPINAL CORD INJURIES IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 94 NORTH AMERICA LUMBAR SPINAL CORD INJURIES IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 95 NORTH AMERICA SACRAL SPINAL CORD INJURIES IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 96 NORTH AMERICA MEDICATION IN SPINAL CORD INJURY TREATMENT MARKET, BY DRUG TYPE, 2018-2032 (USD THOUSAND)

TABLE 97 NORTH AMERICA BRANDED IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 98 NORTH AMERICA MEDICATION IN SPINAL CORD INJURY TREATMENT MARKET, BY ROUTE OF ADMINISTRATION, 2018-2032 (USD THOUSAND)

TABLE 99 NORTH AMERICA ORAL IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 100 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET, BY GENDER, 2018-2032 (USD THOUSAND)

TABLE 101 NORTH AMERICA MALE IN SPINAL CORD INJURY TREATMENT MARKET, BY AGE GROUP, 2018-2032 (USD THOUSAND)

TABLE 102 NORTH AMERICA FEMALE IN SPINAL CORD INJURY TREATMENT MARKET, BY AGE GROUP, 2018-2032 (USD THOUSAND)

TABLE 103 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET, BY END USER, 2018-2032 (USD THOUSAND)

TABLE 104 NORTH AMERICA MEDICATION IN SPINAL CORD INJURY TREATMENT MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (USD THOUSAND)

TABLE 105 U.S. SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 106 U.S. NON-OPERATIVE MANAGEMENT IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 107 U.S. THERAPY IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 108 U.S. REHABILITATION THERAPY IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 109 U.S. MEDICATION IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 110 U.S. ANTICONVULSANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 111 U.S. ANTICONVULSANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (THOUSAND UNITS)

TABLE 112 U.S. ANTICONVULSANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD/UNITS)

TABLE 113 U.S. CORTICOSTEROIDS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 114 U.S. CORTICOSTEROIDS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (THOUSAND UNITS)

TABLE 115 U.S. CORTICOSTEROIDS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD/UNITS)

TABLE 116 U.S. ANTIDEPRESSANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 117 U.S. ANTIDEPRESSANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (THOUSAND UNITS)

TABLE 118 U.S. ANTIDEPRESSANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD/UNITS)

TABLE 119 U.S. ANTISPASMODICS AND MUSCLE RELAXANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 120 U.S. ANTISPASMODICS AND MUSCLE RELAXANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (THOUSAND UNITS)

TABLE 121 U.S. ANTISPASMODICS AND MUSCLE RELAXANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD/UNITS)

TABLE 122 U.S. NSAIDS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 123 U.S. NSAIDS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (THOUSAND UNITS)

TABLE 124 U.S. NSAIDS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD/UNITS)

TABLE 125 U.S. ANTIBIOTICS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 126 U.S. ANTIBIOTICS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (THOUSAND UNITS)

TABLE 127 U.S. ANTIBIOTICS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD/UNITS)

TABLE 128 U.S. OPERATIVE MANAGEMENT IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 129 U.S. DECOMPRESSION SURGERY IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 130 U.S. DISC REPLACEMENT IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 131 U.S. DISC AND FACET JOINT REMOVAL IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 132 U.S. SPINAL FUSION IN ANTERIOR CERVICAL DISCECTOMY IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 133 U.S. MEDIAL FACETECTOMY IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 134 U.S. SPINAL CORD INJURY TREATMENT MARKET, BY INJURY TYPE, 2018-2032 (USD THOUSAND)

TABLE 135 U.S. SPINAL CORD INJURY TREATMENT MARKET, BY LEVEL OF INJURY, 2018-2032 (USD THOUSAND)

TABLE 136 U.S. CERVICAL SPINAL CORD INJURIES IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 137 U.S. THORACIC SPINAL CORD INJURIES IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 138 U.S. LUMBAR SPINAL CORD INJURIES IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 139 U.S. SACRAL SPINAL CORD INJURIES IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 140 U.S. MEDICATION IN SPINAL CORD INJURY TREATMENT MARKET, BY DRUG TYPE, 2018-2032 (USD THOUSAND)

TABLE 141 U.S. BRANDED IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 142 U.S. MEDICATION IN SPINAL CORD INJURY TREATMENT MARKET, BY ROUTE OF ADMINISTRATION, 2018-2032 (USD THOUSAND)

TABLE 143 U.S. ORAL IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 144 U.S. SPINAL CORD INJURY TREATMENT MARKET, BY GENDER, 2018-2032 (USD THOUSAND)

TABLE 145 U.S. MALE IN SPINAL CORD INJURY TREATMENT MARKET, BY AGE GROUP, 2018-2032 (USD THOUSAND)

TABLE 146 U.S. FEMALE IN SPINAL CORD INJURY TREATMENT MARKET, BY AGE GROUP, 2018-2032 (USD THOUSAND)

TABLE 147 U.S. SPINAL CORD INJURY TREATMENT MARKET, BY END USER, 2018-2032 (USD THOUSAND)

TABLE 148 U.S. MEDICATION IN SPINAL CORD INJURY TREATMENT MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (USD THOUSAND)

TABLE 149 CANADA SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 150 CANADA NON-OPERATIVE MANAGEMENT IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 151 CANADA THERAPY IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 152 CANADA REHABILITATION THERAPY IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 153 CANADA MEDICATION IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 154 CANADA ANTICONVULSANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 155 CANADA ANTICONVULSANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (THOUSAND UNITS)

TABLE 156 CANADA ANTICONVULSANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD/UNITS)

TABLE 157 CANADA CORTICOSTEROIDS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 158 CANADA CORTICOSTEROIDS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (THOUSAND UNITS)

TABLE 159 CANADA CORTICOSTEROIDS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD/UNITS)

TABLE 160 CANADA ANTIDEPRESSANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 161 CANADA ANTIDEPRESSANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (THOUSAND UNITS)

TABLE 162 CANADA ANTIDEPRESSANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD/UNITS)

TABLE 163 CANADA ANTISPASMODICS AND MUSCLE RELAXANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 164 CANADA ANTISPASMODICS AND MUSCLE RELAXANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (THOUSAND UNITS)

TABLE 165 CANADA ANTISPASMODICS AND MUSCLE RELAXANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD/UNITS)

TABLE 166 CANADA NSAIDS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 167 CANADA NSAIDS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (THOUSAND UNITS)

TABLE 168 CANADA NSAIDS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD/UNITS)

TABLE 169 CANADA ANTIBIOTICS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 170 CANADA ANTIBIOTICS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (THOUSAND UNITS)

TABLE 171 CANADA ANTIBIOTICS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD/UNITS)

TABLE 172 CANADA OPERATIVE MANAGEMENT IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 173 CANADA DECOMPRESSION SURGERY IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 174 CANADA DISC REPLACEMENT IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 175 CANADA DISC AND FACET JOINT REMOVAL IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 176 CANADA SPINAL FUSION IN ANTERIOR CERVICAL DISCECTOMY IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 177 CANADA MEDIAL FACETECTOMY IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 178 CANADA SPINAL CORD INJURY TREATMENT MARKET, BY INJURY TYPE, 2018-2032 (USD THOUSAND)

TABLE 179 CANADA SPINAL CORD INJURY TREATMENT MARKET, BY LEVEL OF INJURY, 2018-2032 (USD THOUSAND)

TABLE 180 CANADA CERVICAL SPINAL CORD INJURIES IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 181 CANADA THORACIC SPINAL CORD INJURIES IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 182 CANADA LUMBAR SPINAL CORD INJURIES IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 183 CANADA SACRAL SPINAL CORD INJURIES IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 184 CANADA MEDICATION IN SPINAL CORD INJURY TREATMENT MARKET, BY DRUG TYPE, 2018-2032 (USD THOUSAND)

TABLE 185 CANADA BRANDED IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 186 CANADA MEDICATION IN SPINAL CORD INJURY TREATMENT MARKET, BY ROUTE OF ADMINISTRATION, 2018-2032 (USD THOUSAND)

TABLE 187 CANADA ORAL IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 188 CANADA SPINAL CORD INJURY TREATMENT MARKET, BY GENDER, 2018-2032 (USD THOUSAND)

TABLE 189 CANADA MALE IN SPINAL CORD INJURY TREATMENT MARKET, BY AGE GROUP, 2018-2032 (USD THOUSAND)

TABLE 190 CANADA FEMALE IN SPINAL CORD INJURY TREATMENT MARKET, BY AGE GROUP, 2018-2032 (USD THOUSAND)

TABLE 191 CANADA SPINAL CORD INJURY TREATMENT MARKET, BY END USER, 2018-2032 (USD THOUSAND)

TABLE 192 CANADA MEDICATION IN SPINAL CORD INJURY TREATMENT MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (USD THOUSAND)

TABLE 193 MEXICO SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 194 MEXICO NON-OPERATIVE MANAGEMENT IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 195 MEXICO THERAPY IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 196 MEXICO REHABILITATION THERAPY IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 197 MEXICO MEDICATION IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 198 MEXICO ANTICONVULSANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 199 MEXICO ANTICONVULSANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (THOUSAND UNITS)

TABLE 200 MEXICO ANTICONVULSANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD/UNITS)

TABLE 201 MEXICO CORTICOSTEROIDS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 202 MEXICO CORTICOSTEROIDS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (THOUSAND UNITS)

TABLE 203 MEXICO CORTICOSTEROIDS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD/UNITS)

TABLE 204 MEXICO ANTIDEPRESSANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 205 MEXICO ANTIDEPRESSANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (THOUSAND UNITS)

TABLE 206 MEXICO ANTIDEPRESSANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD/UNITS)

TABLE 207 MEXICO ANTISPASMODICS AND MUSCLE RELAXANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 208 MEXICO ANTISPASMODICS AND MUSCLE RELAXANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (THOUSAND UNITS)

TABLE 209 MEXICO ANTISPASMODICS AND MUSCLE RELAXANTS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD/UNITS)

TABLE 210 MEXICO NSAIDS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 211 MEXICO NSAIDS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (THOUSAND UNITS)

TABLE 212 MEXICO NSAIDS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD/UNITS)

TABLE 213 MEXICO ANTIBIOTICS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 214 MEXICO ANTIBIOTICS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (THOUSAND UNITS)

TABLE 215 MEXICO ANTIBIOTICS IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD/UNITS)

TABLE 216 MEXICO OPERATIVE MANAGEMENT IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 217 MEXICO DECOMPRESSION SURGERY IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 218 MEXICO DISC REPLACEMENT IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 219 MEXICO DISC AND FACET JOINT REMOVAL IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 220 MEXICO SPINAL FUSION IN ANTERIOR CERVICAL DISCECTOMY IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 221 MEXICO MEDIAL FACETECTOMY IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 222 MEXICO SPINAL CORD INJURY TREATMENT MARKET, BY INJURY TYPE, 2018-2032 (USD THOUSAND)

TABLE 223 MEXICO SPINAL CORD INJURY TREATMENT MARKET, BY LEVEL OF INJURY, 2018-2032 (USD THOUSAND)

TABLE 224 MEXICO CERVICAL SPINAL CORD INJURIES IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 225 MEXICO THORACIC SPINAL CORD INJURIES IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 226 MEXICO LUMBAR SPINAL CORD INJURIES IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 227 MEXICO SACRAL SPINAL CORD INJURIES IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 228 MEXICO MEDICATION IN SPINAL CORD INJURY TREATMENT MARKET, BY DRUG TYPE, 2018-2032 (USD THOUSAND)

TABLE 229 MEXICO BRANDED IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 230 MEXICO MEDICATION IN SPINAL CORD INJURY TREATMENT MARKET, BY ROUTE OF ADMINISTRATION, 2018-2032 (USD THOUSAND)

TABLE 231 MEXICO ORAL IN SPINAL CORD INJURY TREATMENT MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 232 MEXICO SPINAL CORD INJURY TREATMENT MARKET, BY GENDER, 2018-2032 (USD THOUSAND)

TABLE 233 MEXICO MALE IN SPINAL CORD INJURY TREATMENT MARKET, BY AGE GROUP, 2018-2032 (USD THOUSAND)

TABLE 234 MEXICO FEMALE IN SPINAL CORD INJURY TREATMENT MARKET, BY AGE GROUP, 2018-2032 (USD THOUSAND)

TABLE 235 MEXICO SPINAL CORD INJURY TREATMENT MARKET, BY END USER, 2018-2032 (USD THOUSAND)

TABLE 236 MEXICO MEDICATION IN SPINAL CORD INJURY TREATMENT MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (USD THOUSAND)

List of Figure

FIGURE 1 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: SEGMENTATION

FIGURE 2 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: DATA TRIANGULATION

FIGURE 3 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: DROC ANALYSIS

FIGURE 4 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: NORTH AMERICA VS REGIONAL MARKET ANALYSIS

FIGURE 5 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 7 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: DBMR MARKET POSITION GRID

FIGURE 8 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: MARKET END USER COVERAGE GRID

FIGURE 9 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: VENDOR SHARE ANALYSIS

FIGURE 10 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: SEGMENTATION

FIGURE 11 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET EXECUTIVE SUMMARY

FIGURE 12 STRATEGIC DECISIONS

FIGURE 13 TWO SEGMENTS COMPRISE THE NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET, BY TYPE

FIGURE 14 GROWING COLLABORATION AND EXPANDING PARTNERSHIPS IS EXPECTED TO DRIVE THE NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET GROWTH IN THE FORECAST PERIOD OF 2025 TO 2032

FIGURE 15 NON-OPERATIVE MANAGEMENT SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE NORTH AMERICA SPINAL CORD INJURY TREATMENT IN THE FORECAST PERIOD OF 2025 & 2032

FIGURE 16 MARKET OVERVIEW

FIGURE 17 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: BY TYPE, 2024

FIGURE 18 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: BY TYPE, 2025-2032 (USD THOUSAND)

FIGURE 19 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: BY TYPE, CAGR (2025-2032)

FIGURE 20 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: BY TYPE, LIFELINE CURVE

FIGURE 21 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: BY LEVEL OF INJURY, 2024

FIGURE 22 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: BY LEVEL OF INJURY, 2025-2032 (USD THOUSAND)

FIGURE 23 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: BY LEVEL OF INJURY, CAGR (2025-2032)

FIGURE 24 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: BY LEVEL OF INJURY, LIFELINE CURVE

FIGURE 25 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: BY INJURY TYPE, 2024

FIGURE 26 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: BY INJURY TYPE, 2025-2032 (USD THOUSAND)

FIGURE 27 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: BY INJURY TYPE, CAGR (2025-2032)

FIGURE 28 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: BY INJURY TYPE, LIFELINE CURVE

FIGURE 29 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: BY GENDER, 2024

FIGURE 30 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: BY GENDER, 2025-2032 (USD THOUSAND)

FIGURE 31 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: BY GENDER, CAGR (2025-2032)

FIGURE 32 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: BY GENDER, LIFELINE CURVE

FIGURE 33 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: BY END USER, 2024

FIGURE 34 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: BY END USER, 2025-2032 (USD THOUSAND)

FIGURE 35 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: BY END USER, CAGR (2025-2032)

FIGURE 36 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: BY END USER, LIFELINE CURVE

FIGURE 37 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: SNAPSHOT (2024)

FIGURE 38 NORTH AMERICA SPINAL CORD INJURY TREATMENT MARKET: COMPANY SHARE 2024 (%)

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.