North America Surgical Imaging Market

Market Size in USD Billion

USD

5.30 Billion

USD

7.67 Billion

2025

2033

USD

5.30 Billion

USD

7.67 Billion

2025

2033

| 2026 - 2033 | |

| USD 5.30 Billion | |

| USD 7.67 Billion | |

| % | |

|

North America Surgical Imaging Market Size

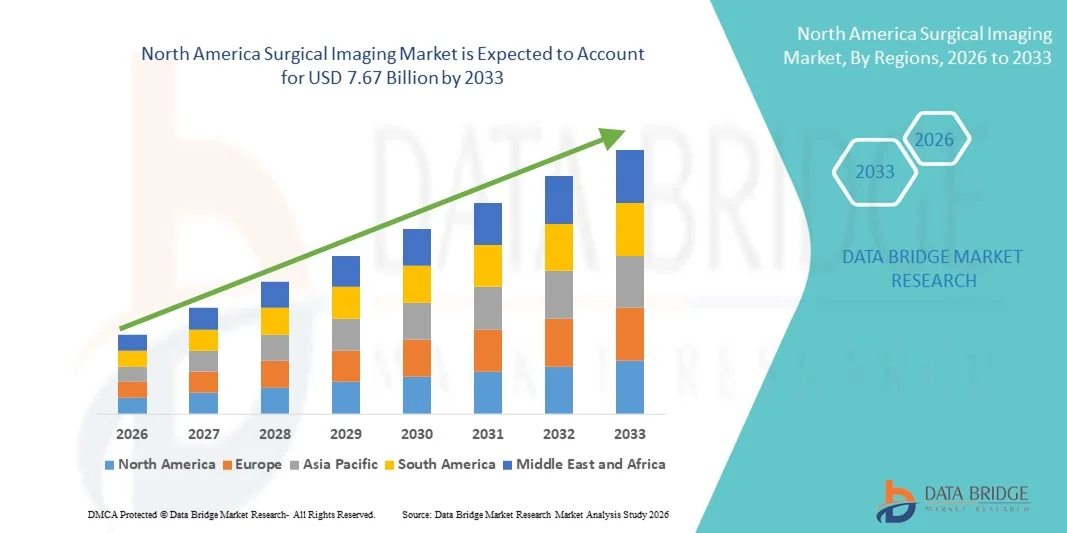

- The North America Surgical Imaging market size was valued at USD 5.30 billion in 2025 and is expected to reach USD 7.67 billion by 2033, at a CAGR of 4.73% during the forecast period

- The market growth is largely fueled by the increasing adoption of advanced imaging technologies and technological innovations in surgical procedures, leading to improved precision, reduced operation times, and better patient outcomes

- Furthermore, rising demand for minimally invasive surgeries, growing investments in modern healthcare infrastructure, and the need for real-time intraoperative imaging are accelerating the uptake of Surgical Imaging solutions, thereby significantly boosting the industry's growth

North America Surgical Imaging Market Analysis

- Surgical imaging systems, providing real-time visualization and intraoperative guidance during surgical procedures, are increasingly essential for improving precision, reducing operation times, and enhancing patient outcomes in both hospitals and specialty surgical centers

- The escalating demand for surgical imaging is primarily fueled by the rising adoption of minimally invasive procedures, increasing healthcare infrastructure investments, and growing preference for advanced imaging solutions that enable safer, more efficient surgeries

- U.S. dominated the Surgical Imaging market with the largest revenue share of 39.80% in 2025, driven by high adoption of advanced imaging technologies, well-established healthcare infrastructure, and a strong presence of key market players, with the U.S. accounting for a significant portion of regional revenue due to widespread use of intraoperative MRI, CT, and fluoroscopy systems

- Canada is expected to be the fastest-growing country in the Surgical Imaging market during the forecast period, expanding at a CAGR of 8.7% from 2026 to 2033, supported by increasing investments in hospital modernization, growing adoption of minimally invasive surgeries, and favorable government healthcare initiatives

- The image intensifier C-arms segment dominated the largest market revenue share of 46.3% in 2025, owing to their long-standing presence in hospitals and established reliability for intraoperative imaging

Report Scope and Surgical Imaging Market Segmentation

|

Attributes |

Surgical Imaging Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

North America Surgical Imaging Market Trends

Enhanced Convenience Through Advanced Surgical Imaging Systems

- A significant and accelerating trend in the North America Surgical Imaging market is the increasing adoption of high-resolution imaging technologies, real-time intraoperative visualization, and integrated imaging platforms

- These innovations are enhancing surgical precision, reducing operation time, and improving patient outcomes across multiple specialties including neurosurgery, orthopedics, and cardiovascular surgery

- For instance, hospitals such as the Mayo Clinic and Cleveland Clinic have implemented intraoperative CT and MRI systems, enabling surgeons to visualize anatomy in real time and make more accurate decisions during complex procedures

- Modern imaging systems now allow seamless integration of multiple imaging modalities—such as MRI, CT, and fluoroscopy—into a single surgical workflow, improving accuracy and efficiency in operating rooms

- The trend towards multi-modality imaging and digital integration is reshaping surgical expectations, leading to wider adoption of advanced imaging platforms across both public and private healthcare institutions

- Consequently, companies like Siemens Healthineers and GE Healthcare are developing next-generation surgical imaging solutions that combine high-definition visualization, advanced software analytics, and ergonomic designs tailored for operating rooms

- The demand for advanced surgical imaging systems is growing rapidly across hospitals, specialty surgical centers, and research institutes, as healthcare providers increasingly prioritize patient safety, operational efficiency, and clinical accuracy

North America Surgical Imaging Market Dynamics

Driver

Rising Demand for Precision Surgery and Minimally Invasive Procedures

- The growing preference for minimally invasive and image-guided surgeries, coupled with increasing surgical volumes and complex procedures, is a major driver of market growth

- For instance, in 2025, Johns Hopkins Hospital integrated high-definition laparoscopic imaging and 3D navigation systems in its surgical suites, improving outcomes in oncology and cardiovascular surgeries

- Hospitals and surgical centers are investing in advanced imaging systems to reduce intraoperative errors, shorten procedure times, and enhance postoperative recovery

- Rising adoption of digital and robotic-assisted surgeries, coupled with healthcare providers’ focus on precision and efficiency, continues to propel the Surgical Imaging market forward

- Expanding surgical infrastructure, government funding for hospital modernization, and increasing awareness of advanced imaging benefits among clinicians are further boosting market growth

Restraint/Challenge

High Capital Investment and Operational Complexity

- High initial investment costs for advanced imaging equipment, along with operational and maintenance expenses, can pose challenges for hospitals and smaller surgical centers, limiting adoption in certain regions

- For instance, the cost of installing a hybrid operating room equipped with intraoperative CT and angiography systems at a medium-sized hospital in Canada exceeded $5 million, making it difficult for smaller facilities to adopt these technologies

- In addition, the complexity of operating and integrating multiple imaging modalities requires skilled technicians and surgeons trained in advanced workflows, which can slow implementation

- Limited reimbursement policies for certain high-end imaging procedures in developing regions can also hinder adoption, particularly for expensive or highly specialized systems

- Overcoming these challenges through cost-effective system designs, comprehensive training programs, and government or private funding initiatives will be essential to ensure wider adoption and sustained growth of surgical imaging technologies

North America Surgical Imaging Market Scope

The market is segmented on the basis of technology, application, product, modality, and end user.

- By Technology

On the basis of technology, the market is segmented into image intensifier C-arms and flat panel detector C-arms. The image intensifier C-arms segment dominated the largest market revenue share of 46.3% in 2025, owing to their long-standing presence in hospitals and established reliability for intraoperative imaging. These systems provide high-resolution fluoroscopy suitable for orthopedic, trauma, and cardiovascular surgeries. Physician familiarity and ease of integration with existing surgical suites enhance adoption. The segment benefits from cost-effectiveness relative to newer technologies. Compatibility with multi-specialty surgical workflows strengthens demand. Training programs for surgeons improve clinical confidence. Strong reimbursement policies support hospital procurement. Maintenance simplicity and availability of refurbished units boost adoption. Expanding orthopedic and trauma surgery volumes sustain utilization. Regulatory approvals facilitate deployment. Integration with surgical navigation tools expands clinical applications. Ongoing digital enhancements improve image quality. The segment remains preferred in both private and public hospitals.

The flat panel detector C-arms segment is expected to witness the fastest CAGR of 12.9% from 2026 to 2033, driven by superior imaging resolution and lower radiation exposure. Rising adoption in minimally invasive procedures fuels growth. Hospitals increasingly invest in flat panel systems for precision-guided surgeries. Integration with 3D imaging and navigation supports complex interventions. Technological improvements in detector sensitivity enhance clinical accuracy. Expansion of specialty surgical centers accelerates adoption. Favorable reimbursement policies for high-tech imaging drive purchases. Increasing awareness among surgeons regarding advanced imaging benefits adoption. Mobile flat panel units provide flexibility in ORs. Continuous R&D in software and imaging algorithms improves performance. Surgeons prefer flat panel systems for real-time visualization. Patient demand for minimally invasive procedures supports growth. Partnerships between hospitals and manufacturers facilitate faster deployment.

- By Application

On the basis of application, the market is segmented into orthopedic and trauma surgeries, neurosurgeries, cardiovascular surgeries, gastrointestinal surgeries, and other applications. The orthopedic and trauma surgeries segment dominated the largest market revenue share of 42.7% in 2025, owing to the high prevalence of fractures, joint replacements, and musculoskeletal disorders in North America. Hospitals widely use C-arms for intraoperative imaging during fracture fixation and spinal procedures. High surgical volumes in orthopedic departments sustain adoption. Reimbursement coverage supports acquisition. Surgeons prefer real-time imaging for complex interventions. Expanding outpatient orthopedic centers increase market penetration. Technological upgrades in C-arms enhance precision. Training programs improve clinician proficiency. Integration with navigation tools strengthens outcomes. Multi-specialty hospitals benefit from flexible imaging applications. Demand is further driven by an aging population and sports injuries. Portable C-arms enhance point-of-care usability.

The neurosurgeries segment is expected to witness the fastest CAGR of 13.5% from 2026 to 2033, driven by increasing demand for minimally invasive brain and spinal surgeries. High-resolution imaging provides precise visualization of neural structures. Specialty neurosurgical centers are expanding, fueling adoption. Integration with navigation and intraoperative MRI enhances surgical accuracy. Technological advancements reduce complication rates. Training programs increase adoption among neurosurgeons. Government reimbursement for advanced procedures supports growth. Patient preference for minimally invasive techniques accelerates uptake. Hospitals invest in cutting-edge imaging to improve outcomes. Compatibility with flat panel and mobile systems enhances flexibility. Increased prevalence of neurological disorders supports demand. Collaboration between manufacturers and academic institutions facilitates innovation.

- By Product

On the basis of product, the market is segmented into mobile C-arms, mini C-arms, endoscopy, laparoscopy, angiography, surgical navigation systems, and others. The mobile C-arms segment dominated the largest market revenue share of 44.1% in 2025, due to portability, ease of use, and integration with multiple surgical procedures. Hospitals benefit from flexible deployment across operating rooms. Cost-effectiveness compared to fixed systems strengthens adoption. Multi-specialty applicability increases market penetration. Maintenance and service support are widely available. Expansion of ambulatory surgical centers drives adoption. High procedural volumes in orthopedic, trauma, and cardiovascular surgeries sustain demand. User-friendly interfaces improve workflow efficiency. Regulatory approvals support acquisition. Refurbished mobile units expand access in smaller hospitals. Integration with navigation tools enhances precision. Technological upgrades improve imaging quality. Hospitals continue to favor mobile units for flexibility.

The surgical navigation systems segment is expected to witness the fastest CAGR of 13.2% from 2026 to 2033, driven by increasing preference for precision-guided surgeries. Adoption is accelerated by complex orthopedic, neurosurgical, and cardiovascular procedures. Integration with intraoperative imaging enhances accuracy. Favorable reimbursement policies support purchases. Surgeon training and familiarity improve adoption. Expansion of specialty centers encourages uptake. Collaborations between manufacturers and hospitals facilitate deployment. Technological advancements enhance software usability. Patient demand for safer, minimally invasive procedures promotes usage. Hospitals invest in navigation systems for improved outcomes. Integration with robotic-assisted surgeries supports market growth. Continuous software and hardware upgrades enhance functionality. Increasing awareness of clinical benefits drives adoption.

- By Modality

On the basis of modality, the market is segmented into MRI, X-ray, computed tomography, optical, nuclear imaging, and ultrasound. The X-ray segment dominated the largest market revenue share of 45.6% in 2025, due to its cost-effectiveness, wide availability, and intraoperative versatility. Hospitals widely use X-ray C-arms for orthopedic, trauma, and cardiovascular procedures. Compatibility with mobile and fixed systems enhances adoption. Strong reimbursement and regulatory approvals support penetration. High patient volumes drive demand. Training programs improve proficiency. Technological upgrades enhance resolution and reduce radiation. Integration with surgical workflows ensures efficiency. Refurbished units increase accessibility. Expansion of surgical departments sustains growth. Reliable imaging reinforces clinician preference. Hospitals continually invest in X-ray C-arms to support high procedural loads.

The MRI segment is expected to witness the fastest CAGR of 12.8% from 2026 to 2033, driven by growing adoption in neurosurgical and cardiovascular interventions. MRI-compatible imaging systems enable detailed soft tissue visualization. Expansion of specialized hospitals accelerates deployment. Integration with navigation and planning tools improves precision. Minimally invasive procedure preference fuels growth. Government funding and reimbursement encourage acquisition. Technological advancements enhance image clarity and operational efficiency. Surgeon awareness supports adoption. Collaboration with vendors facilitates OR deployment. Advanced MRI reduces complications, promoting use. Training programs ensure effective operation. Rising demand for accurate intraoperative imaging drives growth.

- By End User

On the basis of end user, the market is segmented into hospitals, clinics, and others. The hospitals segment dominated the largest market revenue share of 48.2% in 2025, due to high surgical volumes and established infrastructure. Hospitals deploy multiple imaging modalities for orthopedic, cardiovascular, and neurosurgeries. Purchasing power allows acquisition of high-end C-arms. Multi-specialty surgical centers enhance utilization. Reimbursement policies support procurement. Availability of trained staff ensures effective operation. Continuous upgrades improve clinical outcomes. Trauma and orthopedic unit expansion sustains demand. Integration with navigation systems enhances accuracy. Research and clinical trials promote adoption. Partnerships with manufacturers support access to innovations. High patient throughput justifies multiple installations.

Ambulatory surgical centers are expected to witness the fastest CAGR of 13.7% from 2026 to 2033, driven by rising outpatient and minimally invasive procedures. Mobile and compact imaging solutions suit limited OR space. Increasing day-care orthopedic, cardiovascular, and neurosurgical procedures boost adoption. Favorable reimbursement supports procurement. Integration with portable C-arms improves procedural efficiency. Staff training enhances imaging competency. Expansion of ambulatory networks drives equipment deployment. Patient preference for faster recovery and shorter stays fuels demand. Technological advancements reduce footprint and improve usability. Manufacturer partnerships enable timely upgrades. Awareness of advanced imaging benefits promotes adoption. Growing procedure volumes sustain continuous market expansion.

North America Surgical Imaging Market Regional Analysis

- North America dominated the surgical imaging market with the largest revenue share of 41.5% in 2025, driven by advanced healthcare infrastructure, increasing adoption of minimally invasive surgical procedures, and a strong presence of leading medical device manufacturers. Hospitals and surgical centers are increasingly investing in high-resolution imaging systems, intraoperative navigation tools, and integrated imaging platforms to improve surgical outcomes

- For instance, leading hospitals in the U.S., such as the Mayo Clinic and Cleveland Clinic, have implemented advanced intraoperative CT and MRI systems to enhance precision in neurosurgery and cardiovascular procedures

- The region’s growth is further supported by high R&D investments, regulatory support for innovative imaging technologies, and a well-established reimbursement framework, facilitating rapid adoption of cutting-edge surgical imaging solutions

U.S. Surgical Imaging Market Insight

The U.S. surgical imaging market captured the largest share of the North American Surgical Imaging market in 2025, accounting for 39.8% of total revenue. Growth is fueled by advanced surgical infrastructure, increasing adoption of robotic-assisted surgeries, and high penetration of minimally invasive procedures. Hospitals are prioritizing the integration of multimodal imaging systems to enhance surgical precision and reduce procedural risks. Strong healthcare spending, supportive reimbursement policies, and a high rate of clinical adoption of advanced imaging technologies are driving sustained growth in the U.S. market.

Canada Surgical Imaging Market Insight

Canada surgical imaging market is expected to be one of the fastest-growing markets in North America, expanding at a CAGR of 8.7% from 2026 to 2033, driven by increasing hospital modernization projects, growing awareness of advanced surgical imaging techniques, and government initiatives supporting precision medicine. Rising healthcare expenditure, integration of imaging systems in public hospitals, and investments in minimally invasive surgical infrastructure are expected to accelerate market growth in Canada.

North America Surgical Imaging Market Share

The Surgical Imaging industry is primarily led by well-established companies, including:

- Siemens Healthineers (Germany)

- GE Healthcare (U.S.)

- Philips Healthcare (Netherlands)

- Cannon Medical Systems (Japan)

- Ziehm Imaging (Germany)

- Hologic (U.S.)

- Shimadzu Corporation (Japan)

- Planmed (Finland)

- OrthoScan (U.S.)

- Medtronic (Ireland)

- Brainlab (Germany)

- Invivo (U.S.)

- KV Technologies (France)

- Stryker (U.S.)

- DePuy Synthes (Switzerland)

- Samsung Medison (South Korea)

- Braun (Germany)

- Fujifilm Holdings (Japan)

- Toshiba Medical Systems (Japan)

- Carestream Health (U.S.)

Latest Developments in North America Surgical Imaging Market

- In March 2023, Philips announced the launch of its Zenition 10 mobile C‑arm surgical imaging system, designed to deliver high‑quality fluoroscopic imaging and enhanced ergonomics for a wide range of surgical specialties, including orthopedics, trauma, and spine procedures. This launch expanded the company’s mobile imaging portfolio with a system aimed at improving intraoperative visualization and workflow efficiency

- In March 2024, Siemens Healthineers received FDA clearance for its CIARTIC Move mobile C‑arm platform, a next‑generation imaging system featuring autonomous driving functionality. The technology aims to streamline intraoperative imaging workflows by automating certain functions, improving consistency of image capture, and reducing operation times across orthopedic, trauma, and spine surgical procedures

- In April 2024, Karl Storz SE & Co. KG introduced its IMAGE1 S 4U 3D visualization platform, featuring native 3D imaging for endoscopic procedures. Designed to enhance image quality and depth perception during minimally invasive surgeries, the system supports improved procedural precision and surgeon ergonomics

- In May 2024, Intuitive Surgical announced the integration of advanced 3D imaging capabilities into its da Vinci robotic surgical platform, enhancing depth perception and tissue differentiation for surgeons performing complex robotic‑assisted procedures, particularly in urology, gynecology, and general surgery

- In June 2024, Brainlab AG received FDA approval for its Mixed Reality surgical navigation system, enabling surgeons to interact with 3D anatomical models using gesture controls and holographic visualization during operations — a significant step toward augmented reality‑enhanced image‑guided surgery

- In July 2025, X‑EIZO Corporation launched the CuratOR SC431 surgical field camera system, featuring 4K 60p image capture and advanced image stabilization for superior intraoperative visualization integrated with surgical monitors and recorders, enabling clearer imaging for surgeon teams during complex procedures

- In May 2025, **GE HealthCare Technologies introduced CleaRecon DL, an AI‑based 3D reconstruction technology for cone‑beam CT (CBCT) imaging, which enhances image quality and detail during interventional procedures, supporting more precise surgical navigation and decision‑making

- In May 2025, Philips partnered with Polarean to integrate advanced hyperpolarized Xenon MRI imaging (XENOVIEW) into Philips’ 3.0 T MRI platforms, positioning the technology to enhance functional imaging in surgical planning, particularly for lung and thoracic procedures

- In April 2025, **Canon Medical Systems Corporation launched an integrated hybrid imaging‑and‑navigation platform combining 3D C‑arm and fluoroscopy modules tailored to minimally invasive procedures, offering surgeons unified imaging support that enhances procedural accuracy and reduces operative times

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.