North America Topical Drug Delivery Market

Market Size in USD Billion

USD

54.23 Billion

USD

91.80 Billion

2024

2032

USD

54.23 Billion

USD

91.80 Billion

2024

2032

| 2025 - 2032 | |

| USD 54.23 Billion | |

| USD 91.80 Billion | |

| % | |

|

North America Topical Drug Delivery Market Size

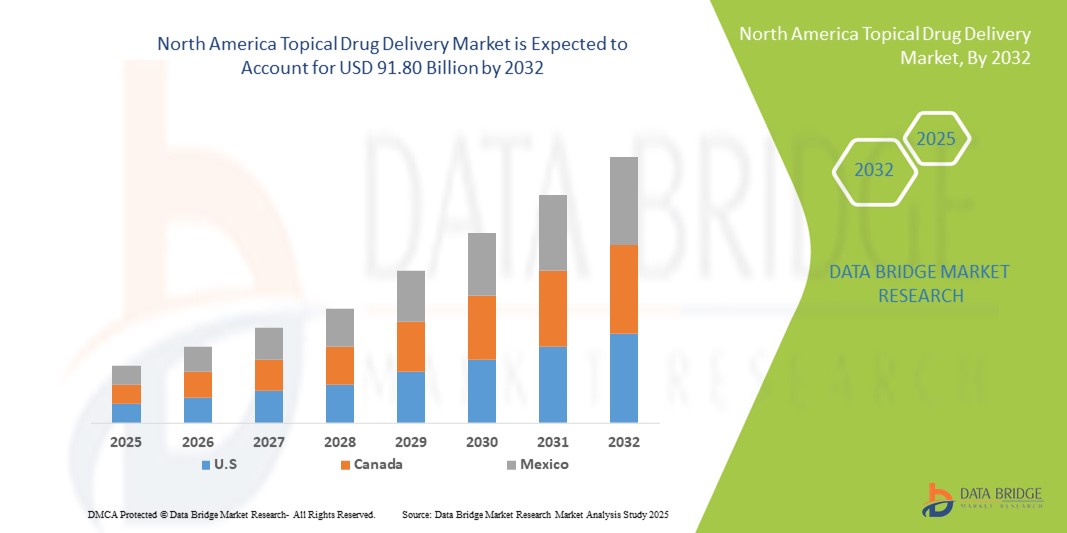

- The North America topical drug delivery market size was valued at USD 54.23 billion in 2024 and is expected to reach USD 91.80 billion by 2032, at a CAGR of 6.8% during the forecast period

- This growth is primarily driven by the increasing prevalence of skin disorders, rising demand for non-invasive treatment options, and advancements in drug delivery technologies.

- In addition, the growing preference for self-administration, particularly for chronic skin conditions and pain management, is contributing to the market's expansion

North America Topical Drug Delivery Market Analysis

- Topical drug delivery systems, enabling localized administration of therapeutic agents through the skin, are increasingly vital in both dermatology and pain management due to their non-invasive nature, targeted action, and reduced systemic side effects

- The rising demand for topical drug delivery is primarily fueled by the growing prevalence of skin disorders, chronic pain conditions, and patient preference for self-administration over oral or injectable therapies

- U.S. dominated the North America topical drug delivery market with the largest revenue share of 85.3% in 2024, characterized by advanced pharmaceutical research infrastructure, high healthcare expenditure, and widespread adoption of innovative drug delivery technologies, with substantial growth in transdermal patches and gels driven by advancements in second-generation transdermal delivery systems

- Canada is expected to be the fastest-growing country in the North America topical drug delivery market during the forecast period due to rising healthcare awareness, increasing prevalence of dermatological conditions, and growing adoption of non-invasive therapeutic options

- The iontophoresis segment dominated the North America topical drug delivery market with a market share of 28.9% in 2024, driven by its ability to enhance drug penetration non-invasively and improve therapeutic outcomes

Report Scope and North America Topical Drug Delivery Market Segmentation

|

Attributes |

North America Topical Drug Delivery Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

North America Topical Drug Delivery Market Trends

Rising Adoption of Advanced Non-Invasive Delivery Techniques

- A significant and accelerating trend in the North America topical drug delivery market is the increasing use of advanced non-invasive techniques such as iontophoresis, sonophoresis, and microneedle-assisted systems, which improve drug penetration and patient compliance

- For instance, iontophoresis patches are being used to deliver anti-inflammatory agents effectively for localized pain management, allowing precise dosage and reducing systemic side effects

- Integration of nanotechnology and sustained-release formulations in topical products enables controlled drug release, enhances therapeutic efficacy, and provides prolonged action, increasing patient convenience

- These advancements facilitate personalized therapy for chronic dermatological and pain-related conditions, making topical delivery a preferred alternative to oral or injectable routes

- This trend towards more efficient, patient-friendly, and technologically enhanced topical therapies is reshaping expectations for home healthcare and outpatient treatment, driving innovation among pharmaceutical companies

- The demand for topical drug delivery systems incorporating advanced penetration techniques and controlled-release mechanisms is growing rapidly across both hospital and home healthcare settings as patients prioritize convenience, safety, and therapeutic effectiveness

North America Topical Drug Delivery Market Dynamics

Driver

Growing Need Due to Rising Chronic Skin and Pain Conditions

- The increasing prevalence of dermatological disorders, chronic pain, and age-related conditions is a significant driver for the heightened demand for topical drug delivery systems

- For instance, a rise in eczema, psoriasis, and localized musculoskeletal pain cases is prompting healthcare providers to adopt non-invasive and targeted treatment options

- Topical delivery systems offer localized therapy, reduced systemic side effects, and improved patient adherence compared to oral or injectable formulations, providing a compelling treatment alternative

- Furthermore, increasing awareness of patient-friendly therapies and the preference for self-administration at home are making topical drug delivery a vital part of treatment protocols in hospitals and specialty centers

- The convenience of precise dosing, ease of application, and integration with home healthcare devices are key factors propelling the adoption of topical drug delivery in North America, while healthcare providers continue to encourage its use for chronic and dermatological conditions

Restraint/Challenge

Skin Irritation Issues and Regulatory Compliance Hurdle

- Concerns regarding skin irritation, allergic reactions, and local adverse effects pose a significant challenge to wider adoption of topical drug delivery products

- For instance, some patients experience erythema or dermatitis due to prolonged use of transdermal patches or certain chemical formulations, limiting product acceptance

- Addressing these safety concerns through biocompatible materials, hypoallergenic formulations, and rigorous clinical testing is crucial for building patient and provider trust

- Furthermore, compliance with regulatory standards such as FDA guidelines for topical drug delivery devices and formulations adds complexity to product development and market entry

- The relatively high cost of advanced delivery systems compared to conventional topical creams or gels can also restrict adoption, especially among price-sensitive patients, necessitating a balance between innovation, safety, and affordability

- Overcoming these challenges through improved product safety, patient education, and cost-effective solutions will be vital for sustained growth in the North America topical drug delivery market

North America Topical Drug Delivery Market Scope

The market is segmented on the basis of product type, delivery techniques, therapeutic type, generation, mode of purchase, indication, route of administration, end user, and distribution channel.

- By Product Type

On the basis of product type, the North America topical drug delivery market is segmented into drug delivery formulations and drug delivery devices. The drug delivery formulations segment dominated the market with the largest market revenue share of 61.5% in 2024, driven by the widespread use of creams, gels, and transdermal patches for dermatological and pain management applications. Formulations are preferred for their convenience, ease of application, and compatibility with a wide range of therapeutic agents. Patients and healthcare providers often favor formulations for home-based treatment and outpatient care due to their non-invasive nature. In addition, formulations offer flexibility in dosing, sustained release, and targeted therapy, enhancing patient compliance. Pharmaceutical companies continue to innovate in formulation technology to improve absorption, minimize side effects, and increase efficacy. The broad availability of prescription and OTC topical formulations further strengthens the segment’s dominance.

The drug delivery devices segment is expected to witness the fastest growth from 2025 to 2032, fueled by rising adoption of advanced delivery systems such as microneedle patches, iontophoresis devices, and wearable transdermal systems. Devices enhance the precision of drug administration, improve therapeutic outcomes, and support long-term chronic treatment plans. They are increasingly integrated with smart healthcare technologies and monitoring systems, allowing clinicians and patients to track therapy adherence. The growing trend toward personalized medicine and non-invasive delivery further drives demand. In addition, regulatory approvals for innovative devices in the U.S. and Canada are accelerating market expansion. Healthcare providers and hospitals are investing in devices for targeted delivery and improved patient convenience, boosting market penetration.

- By Delivery Technique

On the basis of delivery technique, the North America topical drug delivery market is segmented into iontophoresis, sonophoresis, laser ablation, radio frequency ablation, magnetophoresis, electroporation, and others. The iontophoresis segment dominated the market with a share of 28.9% in 2024, driven by its ability to non-invasively enhance drug penetration into targeted skin layers. Iontophoresis is widely applied for anti-inflammatory drugs and analgesics, providing localized therapy with reduced systemic exposure. Patients benefit from faster onset of action and fewer side effects compared to oral administration. Healthcare providers often prefer iontophoresis for controlled delivery and outpatient use. Advances in device design and wearable patches are increasing convenience and treatment adherence. The integration of iontophoresis with smart monitoring systems allows dose tracking and improves therapeutic outcomes, sustaining strong market demand.

The sonophoresis segment is expected to witness the fastest growth from 2025 to 2032, due to increasing research in ultrasound-assisted transdermal delivery, which enhances permeability of large molecules and vaccines. Sonophoresis is being explored for non-invasive delivery of hormones, analgesics, and dermatological therapeutics. Its application in hospital and home healthcare settings is expanding as patients seek faster and pain-free treatment options. Technological advancements and reduced device costs are further driving adoption. Growing awareness among dermatologists and pain management specialists about its efficacy is expected to support rapid uptake.

- By Type

On the basis of type, the North America topical drug delivery market is segmented into cleansing agents, protective agents, moisturizing agents, drying agents, anti-itch agents, anti-inflammatory agents, anti-infective agents, keratolytics, and others. The anti-inflammatory agents segment dominated the market with a share of 33.2% in 2024, driven by the high prevalence of chronic skin inflammation, musculoskeletal pain, and post-operative conditions in North America. Anti-inflammatory topical products are preferred for localized relief, minimizing systemic side effects associated with oral medications. They are commonly used in dermatology, physiotherapy, and home healthcare settings. The availability of prescription and OTC formulations increases accessibility and patient compliance. Pharmaceutical companies continue to develop advanced anti-inflammatory formulations with improved absorption and sustained-release properties. The growing awareness among patients and clinicians about the benefits of targeted therapy sustains the segment’s market leadership.

The moisturizing agents segment is expected to witness the fastest growth from 2025 to 2032, fueled by rising demand for cosmetic dermatology products and preventive skin care. Increased awareness about skin hydration, combined with the prevalence of eczema and dry skin conditions, is driving adoption. Integration of moisturizers with other therapeutic agents for combination therapy is boosting usage. E-commerce and retail channels are enhancing accessibility, while technological innovations in formulation improve stability and efficacy. Growth is also supported by the aging population seeking skin care solutions for sensitive and aging skin.

- By Generation

On the basis of generation, the North America topical drug delivery market is segmented into first generation transdermal delivery systems, second generation transdermal delivery systems, and third generation transdermal delivery systems. The second generation transdermal delivery systems segment dominated the market with a share of 42.1% in 2024, driven by improved drug permeation, enhanced control over release rates, and broader compatibility with various drugs. Second-generation systems such as iontophoresis and sonophoresis-based patches provide effective localized therapy, reduce systemic side effects, and enhance patient adherence. Healthcare providers prefer these systems for chronic conditions requiring sustained dosing. Pharmaceutical companies continue to invest in second-generation systems due to their balance of efficacy, safety, and manufacturability. Their proven clinical success, combined with cost-effectiveness compared to third-generation systems, sustains strong demand.

The third generation transdermal delivery systems segment is expected to witness the fastest growth from 2025 to 2032, fueled by innovations in microneedle arrays, nanocarrier-assisted delivery, and laser-enhanced transdermal techniques. These systems allow delivery of larger molecules, including proteins and vaccines, previously unsuitable for topical administration. Growing research in advanced formulations and increasing adoption in specialty hospitals and home healthcare settings are driving rapid uptake. Patients benefit from minimal invasiveness and precise dosing, encouraging market expansion. Regulatory approvals for next-generation systems are further accelerating growth. Clinical trials demonstrating safety and efficacy contribute to high adoption rates.

- By Mode of Purchase

On the basis of mode of purchase, the North America topical drug delivery market is segmented into prescription and over-the-counter (OTC). The prescription segment dominated the market with a share of 58.7% in 2024, driven by the prevalence of dermatological disorders, chronic pain, and other therapeutic indications requiring professional supervision. Prescription products offer higher efficacy and safety monitoring, which is crucial for drugs such as anti-inflammatory agents, keratolytics, and hormone-based topical formulations. Hospitals, specialty centers, and clinicians often recommend prescription topical therapies for better treatment outcomes. The requirement for regulatory approval ensures quality and consistency, further supporting the prescription segment. Patients and caregivers also prefer professional guidance for dosage, duration, and combination therapies, reinforcing the segment’s dominance.

The OTC segment is expected to witness the fastest growth from 2025 to 2032, due to rising self-medication trends, increasing awareness of preventive dermatology, and easier access through retail and online pharmacies. OTC topical products, such as moisturizers, anti-itch creams, and protective agents, are increasingly used for minor skin conditions and home-based care. Digital marketing and e-commerce channels are enhancing visibility and accessibility. Growing consumer preference for convenient, non-prescription therapies supports segment expansion. Companies are innovating OTC formulations to improve efficacy, safety, and aesthetic appeal.

- By Indication

On the basis of indication, the North America topical drug delivery market is segmented into dermatological disorders, ophthalmic disorders, pain management, neurosurgical disorders, hormonal therapy, smoking cessation, and others. The dermatological disorders segment dominated the market with a share of 44.3% in 2024, driven by the high incidence of acne, eczema, psoriasis, and other skin conditions in North America. Topical formulations provide localized therapy with fewer systemic side effects compared to oral medications. Hospitals, dermatology clinics, and home healthcare settings widely adopt these treatments. Pharmaceutical innovation in anti-inflammatory, anti-infective, and moisturizing topical products further strengthens this segment. Patient preference for non-invasive, easy-to-apply treatments supports sustained demand. Continuous R&D to enhance efficacy and patient compliance contributes to dominance.

The pain management segment is expected to witness the fastest growth from 2025 to 2032, fueled by increasing cases of chronic musculoskeletal pain, arthritis, and post-operative discomfort. Topical analgesics, gels, and patches provide localized relief and reduce dependency on oral painkillers. Adoption in hospitals, specialty centers, and home healthcare is increasing. Integration with advanced delivery techniques such as iontophoresis accelerates growth. Awareness campaigns promoting safer alternatives to systemic pain management support segment expansion. Technological improvements in formulation and patient-friendly application methods further drive adoption.

- By Route of Administration

On the basis of route of administration, the North America topical drug delivery market is segmented into dermal, ophthalmic, rectal, vaginal, nasal, and others. The dermal segment dominated the market with a share of 67.8% in 2024, due to the high demand for localized treatment of skin conditions and pain management. Dermal administration allows precise targeting, minimizes systemic absorption, and enhances patient convenience. Healthcare providers and home care patients prefer dermal delivery for its ease of use, non-invasive nature, and compatibility with advanced patches and gels. Continuous innovations in penetration enhancers, iontophoresis, and sustained-release systems further strengthen this segment. Prescription and OTC dermal products dominate hospitals, pharmacies, and home healthcare markets. Ongoing research for enhanced dermal absorption supports sustained growth.

The ophthalmic segment is expected to witness the fastest growth from 2025 to 2032, driven by increasing prevalence of eye disorders, rising geriatric population, and innovations in non-invasive ocular drug delivery systems. Drops, gels, and inserts are becoming preferred options for localized treatment, improving therapeutic outcomes. Regulatory approvals and clinical validations boost market confidence. Expansion in hospitals, specialty centers, and home healthcare supports adoption. Technological advancements in formulations improve drug retention and efficacy. Digital health platforms promoting compliance accelerate growth.

- By End User

On the basis of end user, the North America topical drug delivery market is segmented into hospitals, specialty centers, home healthcare, and others. The hospitals segment dominated the market with a share of 49.2% in 2024, due to high adoption of topical therapies for dermatological, pain management, and post-operative care. Hospitals provide professional supervision, ensuring proper usage, efficacy, and safety of topical drug delivery systems. They also support advanced delivery techniques such as iontophoresis and microneedle patches. High patient footfall and integration with pharmacy services reinforce hospital dominance. Hospitals continue to adopt innovative products to improve treatment outcomes and patient satisfaction. Research collaborations between hospitals and pharmaceutical companies enhance adoption of next-generation topical therapies.

The home healthcare segment is expected to witness the fastest growth from 2025 to 2032, fueled by rising preference for self-administered therapies, chronic care management, and telehealth integration. Patients increasingly rely on home-based topical therapies for convenience, cost savings, and continuous care. Growth is supported by wearable and smart delivery devices. Educational initiatives and patient awareness programs accelerate adoption. Integration with remote monitoring and digital health platforms improves compliance and safety. Expansion of home healthcare services in North America is boosting market penetration.

- By Distribution Channel

On the basis of distribution channel, the North America topical drug delivery market is segmented into hospital pharmacy, retail pharmacy, online pharmacy, and others. The retail pharmacy segment dominated the market with a share of 52.5% in 2024, driven by easy accessibility of prescription and OTC topical products. Retail pharmacies provide both professional guidance and immediate availability, making them the preferred choice for patients. They also offer loyalty programs, promotional discounts, and counseling services, enhancing customer engagement. The presence of multiple branded and generic topical products in retail outlets further strengthens this segment. Strong distribution networks and partnerships with pharmaceutical companies reinforce retail pharmacy dominance. Ongoing expansion of retail chains in urban and semi-urban areas supports continued growth.

The online pharmacy segment is expected to witness the fastest growth from 2025 to 2032, fueled by rising e-commerce penetration, increasing preference for home delivery, and digital health adoption. Online pharmacies offer convenience, subscription services, and a wider product range, attracting tech-savvy consumers. Ease of access during pandemic and post-pandemic periods has accelerated adoption. Digital platforms also provide teleconsultation and home delivery integration. Growing consumer trust and promotional strategies by pharma companies boost market expansion.

North America Topical Drug Delivery Market Regional Analysis

- U.S. dominated the North America topical drug delivery market with the largest revenue share of 85.3% in 2024, characterized by advanced pharmaceutical research infrastructure, high healthcare expenditure, and widespread adoption of innovative drug delivery technologies, with substantial growth in transdermal patches and gels driven by advancements in second-generation transdermal delivery systems

- Patients and healthcare providers in the region prioritize convenience, targeted therapy, and reduced systemic side effects, making topical drug delivery systems increasingly preferred over oral or injectable formulations

- This widespread adoption is further supported by advanced healthcare infrastructure, strong pharmaceutical research and development capabilities, high healthcare expenditure, and growing awareness of home healthcare solutions, establishing topical drug delivery as a favored treatment option across hospitals, specialty centers, and home healthcare settings

U.S. North America Topical Drug Delivery Market Insight

The U.S. topical drug delivery market captured the largest revenue share in 2024 within North America, fueled by the high prevalence of dermatological disorders, chronic pain conditions, and growing adoption of advanced non-invasive delivery techniques such as iontophoresis and sonophoresis. Patients and healthcare providers are increasingly prioritizing targeted, localized therapy to reduce systemic side effects and improve treatment adherence. The growing preference for home-based therapies, combined with integration of digital health monitoring and wearable drug delivery devices, further propels the market. Moreover, the presence of strong pharmaceutical R&D infrastructure, high healthcare expenditure, and regulatory support for innovative delivery systems significantly contributes to market expansion.

Canada Topical Drug Delivery Market Insight

The Canada topical drug delivery market is anticipated to grow at a substantial CAGR throughout the forecast period, primarily driven by increasing awareness of skin health, chronic pain management, and preventive care therapies. Rising urbanization and higher disposable incomes are fostering adoption of advanced topical formulations and delivery devices. Canadian patients are also drawn to the convenience, safety, and patient-friendly features offered by non-invasive drug delivery solutions. The region is experiencing growth across hospitals, specialty centers, and home healthcare applications, with both prescription and OTC topical products being increasingly adopted. Government initiatives promoting patient education and telehealth integration further support market expansion.

Mexico Topical Drug Delivery Market Insight

The Mexico topical drug delivery market is expected to expand at a noteworthy CAGR during the forecast period, driven by the growing prevalence of dermatological and musculoskeletal disorders and the rising demand for convenient, home-based treatment solutions. Increasing healthcare awareness and adoption of modern drug delivery techniques are encouraging patients and providers to prefer localized therapies over systemic medications. The availability of affordable topical products and rising penetration of retail and online pharmacies are stimulating market growth. Mexico’s growing healthcare infrastructure and partnerships with multinational pharmaceutical companies are enhancing accessibility and adoption of advanced topical formulations. The trend toward non-invasive, patient-friendly therapies is expected to continue driving market expansion.

North America Topical Drug Delivery Market Share

The North America topical drug delivery industry is primarily led by well-established companies, including:

- 3M (U.S.)

- AbbVie Inc. (U.S.)

- Cipla (India)

- Galderma S.A. (Switzerland)

- Hisamitsu Pharmaceutical Co., Inc. (Japan)

- Johnson & Johnson and its affiliates (U.S.)

- Merck & Co., Inc. (U.S.)

- Novartis AG (Switzerland)

- Piramal Pharma Solutions (India)

- Teva Pharmaceuticals (Israel)

- Bausch Health Companies Inc. (Canada)

- Lupin (India)

- Amgen Inc. (U.S.)

- Sandoz Inc. (U.S.

- Dr. Reddy's Laboratories Ltd. (India)

- Sun Pharmaceutical Industries Ltd. (India)

- Zydus Cadila (India)

- Boehringer Ingelheim Pharmaceuticals, Inc. (Germany)

- Sanofi (France)

What are the Recent Developments in North America Topical Drug Delivery Market?

- In November 2024, Endo, Inc. announced that its subsidiary, Paladin Pharma Inc., entered into a definitive agreement with MC2 Therapeutics to commercialize Wynzora Cream in Canada. If approved by Health Canada, this collaboration will offer Canadian patients a new treatment option for plaque psoriasis, leveraging Paladin's experience in dermatology and MC2's innovative formulation

- In May 2024, Taiwan-based Formosa Pharmaceuticals ("Formosa", 6838.TWO) announced that the company has entered into an exclusive licensing agreement with Tabuk Pharmaceuticals Manufacturing Company ("Tabuk"), for exclusive rights to the commercialization of clobetasol propionate ophthalmic suspension, 0.05% (APP13007), a patented innovative medicine for the treatment of inflammation and pain following ocular surgery

- In March 2024, Formosa Pharmaceuticals announced that the U.S. FDA approved APP13007, a clobetasol propionate ophthalmic suspension (0.05%), for treating inflammation and pain following ocular surgery. This approval marks a significant advancement in post-operative care for patients undergoing eye surgeries

- In August 2023, The U.S. FDA issued a public warning regarding compounded topical finasteride products marketed for hair loss treatment. The agency highlighted that no FDA-approved topical formulations exist and documented 32 adverse event reports associated with these unapproved products between 2019 and 2024

- In February 2021, Almirall, a global biopharmaceutical company, entered into a licensing, collaboration, and commercialization agreement with MC2 Therapeutics to grant Almirall exclusive European rights to commercialize Wynzora Cream (calcipotriene and betamethasone dipropionate) for the treatment of plaque psoriasis. Under the agreement, MC2 Therapeutics is responsible for manufacturing and supply, while Almirall focuses on commercialization in Europe

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.