North America Underactive Bladder Market

Market Size in USD Billion

USD

1.73 Billion

USD

2.61 Billion

2025

2033

USD

1.73 Billion

USD

2.61 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.73 Billion | |

| USD 2.61 Billion | |

| % | |

|

North America Underactive Bladder Market Overview

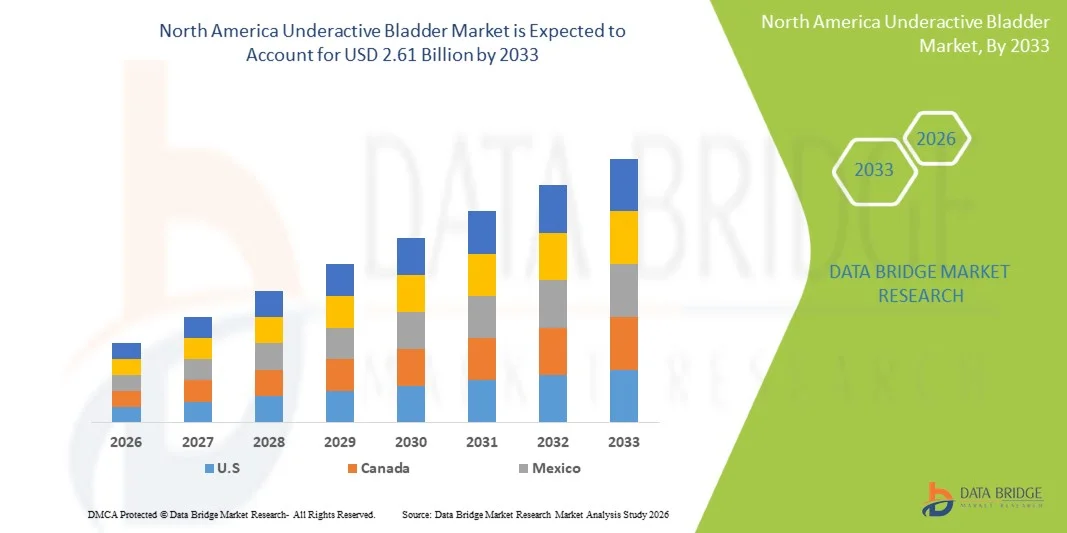

The North America underactive bladder market was valued at USD 1.73 billion in 2025 and is projected to reach USD 2.61 billion by 2033, growing at a CAGR of 5.3% from 2026 to 2033. The market is witnessing steady growth driven by the rising prevalence of neurogenic bladder disorders, increasing geriatric population, and growing awareness regarding urinary dysfunction diagnosis and management across clinical settings.

The increasing burden of diabetes, Parkinson’s disease, spinal cord injuries, and post-surgical urinary complications is significantly contributing to the demand for effective underactive bladder treatment options in North America. Advancements in pharmacotherapy, neuromodulation therapies, and catheter-based management solutions are improving patient outcomes, while increasing adoption of minimally invasive and outpatient treatment approaches is further supporting market expansion across hospitals and specialty urology clinics.

Key Market Trends & Insights

- The United States dominated the North America underactive bladder market with the largest revenue share of 72.6% in 2025, supported by advanced urology care infrastructure, high disease awareness, and strong availability of pharmacotherapy and neuromodulation treatment options.

- The Pharmacotherapy segment led the market with a 46.3% share in 2025, driven by its widespread clinical acceptance as the first-line treatment for bladder dysfunction management.

- Canada is expected to be the fastest-growing region at a CAGR of 6.1% from 2026 to 2033, fueled by improving access to specialized urology care, rising geriatric population, and increasing adoption of minimally invasive and neuromodulation-based therapies.

- Stem Cell and Gene Therapies are the fastest-growing type, projected to register a CAGR of 7.2%, reflecting the surge in research into regenerative medicine for bladder dysfunction.

- The Oral segment dominated the route of administration category with a 62.8% revenue share in 2025, led by strong patient preference for non-invasive and easy-to-use medication forms.

- Neurogenic Underactive Bladder accounted for 58.4% of the market, preferred by rising prevalence of neurological disorders such as Parkinson’s disease, multiple sclerosis, spinal cord injuries, and diabetic neuropathy.

- The Parenteral segment is the fastest-growing route of administration category, with a CAGR of 6.5%, driven by increasing use of injectable neuromodulation-related drugs and advanced biologics.

Market Size & Forecast

- Global Market Value (2025): USD 1.73 Billion

- Expected Market Value (2033): USD 2.61 Billion

- Forecast CAGR (2026–2033): 5.3%

- Leading Country in 2025: United States

- Fastest Growing Country: Canada

Report Scope and North America Underactive Bladder Market Segmentation

|

Attributes |

North America Underactive Bladder Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico |

|

Key Market Players |

· Astellas Pharma Inc. (Japan) · Boston Scientific Corporation (U.S.) · Coloplast Corp (Denmark) · Convatec Group PLC (U.K.) · Cook (U.S.) · Hollister Incorporated (U.S.) · B. Braun SE (Germany) · Medtronic (Ireland) · Teleflex Incorporated (U.S.) · Wellspect HealthCare (Sweden) · Laborie Medical Technologies Corp. (Canada) · Pfizer Inc. (U.S.) · AbbVie Inc. (U.S.) · UroMems (France) · Axonics, Inc. (U.S.) · C. R. Bard, Inc. (U.S.) · Olympus Corporation (Japan) · Fresenius Medical Care AG (Germany) · Cogentix Medical, Inc. (U.S.) · BD (U.S.) |

|

Market Opportunities |

· Growing adoption of sacral neuromodulation and implantable bladder stimulation devices · Increasing clinical research on regenerative medicine and stem cell-based bladder therapies · Expansion of home-based catheterization products and remote urology monitoring solutions |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

North America Underactive Bladder Market Trends

Trend: Growth in Advanced Neuromodulation & Patient-Centric Care

Advanced neuromodulation therapies such as sacral nerve stimulation and tibial nerve stimulation are increasingly being adopted for underactive bladder management, improving bladder contractility and patient quality of life. Urology clinics are integrating minimally invasive procedures with digital monitoring tools to personalize treatment plans and enhance long-term clinical outcomes. Rising preference for outpatient-based care is further supporting the shift from long-term pharmacotherapy toward device-assisted and precision-based bladder dysfunction management, while AI-supported diagnostics improve early detection and treatment optimization. For instance, Medtronic’s sacral neuromodulation systems are widely used in North American urology centers for refractory bladder dysfunction cases.

North America Underactive Bladder Market Dynamics

Key Market Driver: Rising Prevalence of Neurogenic and Age-Related Disorders

The increasing prevalence of neurogenic conditions such as Parkinson’s disease, multiple sclerosis, spinal cord injuries, and diabetic neuropathy is significantly driving demand for underactive bladder treatment solutions. A rapidly aging population across the United States and Canada is further contributing to higher diagnosis rates and treatment uptake in clinical settings. Expanding awareness among physicians and patients regarding bladder dysfunction management is also improving early intervention rates and accelerating market growth. For instance, high geriatric prevalence in the United States is leading to greater utilization of pharmacotherapy and neuromodulation treatments.

Key Restraint/Challenge: High Cost of Advanced Treatment and Device-Based Therapies

A major restraint in the North America underactive bladder market is the high cost associated with neuromodulation devices, long-term pharmacotherapy, and advanced diagnostic procedures. Limited insurance coverage for certain minimally invasive therapies and variability in reimbursement policies across healthcare systems can restrict patient access to advanced treatment options. Additionally, long-term dependency on catheterization and maintenance therapies increases the overall financial burden on patients and healthcare providers. For instance, sacral nerve stimulation implants remain expensive, limiting adoption among cost-sensitive patient groups despite clinical effectiveness.

Key Market Opportunity: Integration of Digital Urology and AI-Enabled Diagnostics

The integration of digital health technologies and AI-enabled diagnostic platforms presents a significant opportunity in the North America underactive bladder market. Remote patient monitoring systems, smart bladder scanners, and predictive analytics tools are improving diagnosis accuracy and enabling proactive treatment strategies. The expansion of tele-urology services is also increasing access to specialized care, particularly in rural and underserved regions. For instance, AI-based urodynamic testing systems are being adopted in specialized urology hospitals to enhance bladder dysfunction assessment and treatment planning.

North America Underactive Bladder Market Scope

The North America underactive bladder market is segmented on the basis of type, route of administration, disease type, and distribution channel.

- By Type

On the basis of type, the North America underactive bladder market is segmented into pharmacotherapy, surgical methods, urethral assist devices, and stem cell and gene therapies. The Pharmacotherapy segment dominated the market with a 46.3% share in 2025, owing to its widespread clinical acceptance as the first-line treatment for bladder dysfunction management. Oral and injectable drug therapies are extensively prescribed across hospitals and specialty urology clinics due to ease of administration and established clinical efficacy. Growing prevalence of neurogenic bladder disorders and age-related urinary dysfunction is further strengthening demand for drug-based treatment options. High availability of branded and generic formulations also supports market dominance. Continuous prescription-based treatment adherence contributes to sustained revenue generation. However, limitations in long-term effectiveness for severe cases slightly constrain growth potential.

The Stem Cell and Gene Therapies segment is projected to register the fastest growth at a CAGR of 7.2% from 2026 to 2033, driven by increasing research into regenerative medicine for bladder dysfunction. These advanced therapies aim to restore bladder contractility at a cellular level, offering potential long-term disease modification rather than symptom management. Rising investment in biotechnology and regenerative urology is accelerating clinical trials in North America. Increasing collaboration between academic institutions and biotech firms is further supporting innovation. Growing unmet clinical need in refractory underactive bladder cases is boosting demand for novel therapies. However, high development costs and regulatory complexity remain key challenges for commercialization.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral, parenteral, and others. The Oral segment dominated the market with a 62.8% share in 2025, driven by strong patient preference for non-invasive and easy-to-use medication forms. Oral pharmacotherapy is widely prescribed as the primary treatment option for managing mild to moderate bladder dysfunction symptoms. High compliance rates and broad availability of oral drugs across hospital and retail pharmacies further support dominance. Physicians prefer oral administration due to ease of dose adjustment and outpatient suitability. The segment also benefits from established reimbursement frameworks across North America. However, limited efficacy in advanced neurogenic cases restricts its standalone effectiveness.

The Parenteral segment is expected to witness the fastest growth at a CAGR of 6.5% from 2026 to 2033, supported by increasing use of injectable neuromodulation-related drugs and advanced biologics. Parenteral therapies are gaining traction in severe and refractory underactive bladder cases requiring rapid and targeted action. Growing adoption of hospital-based treatment protocols is further driving demand. Advancements in drug delivery systems are improving safety and efficacy profiles. Rising clinical focus on personalized medicine is also supporting segment expansion. However, higher procedural complexity and need for clinical supervision limit widespread outpatient use.

- By Disease Type

On the basis of disease type, the market is segmented into neurogenic underactive bladder and non-neurogenic underactive bladder. The Neurogenic Underactive Bladder segment dominated the market with a 58.4% share in 2025, driven by rising prevalence of neurological disorders such as Parkinson’s disease, multiple sclerosis, spinal cord injuries, and diabetic neuropathy. These conditions significantly impair bladder contractility, leading to higher clinical intervention rates. Strong presence of neurology-integrated urology care pathways in North America further supports segment dominance. Increasing geriatric population is also contributing to higher disease burden. Continuous demand for long-term management solutions strengthens market growth. However, complex disease progression requires multi-modal treatment approaches.

The Non-Neurogenic Underactive Bladder segment is projected to register the fastest growth at a CAGR of 6.2% from 2026 to 2033, driven by rising awareness and improved diagnosis of idiopathic bladder dysfunction. Increasing cases related to aging, diabetes, and post-surgical complications are contributing to segment expansion. Advancements in diagnostic imaging and urodynamic testing are improving detection rates. Growing physician awareness is also reducing underdiagnosis of non-neurogenic cases. Expanding outpatient urology services is further supporting treatment adoption. However, variability in symptom presentation continues to pose diagnostic challenges.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and others. The Hospital Pharmacy segment dominated the market with a 51.7% share in 2025, driven by high patient inflow in tertiary care hospitals and specialist-led urology treatment pathways. Most neuromodulation procedures and advanced pharmacological therapies are initiated in hospital settings. Strong availability of prescription-based bladder management drugs supports sustained demand. Hospitals also provide integrated diagnostic and treatment services, improving patient adherence. Increasing hospitalization rates for neurogenic bladder conditions further reinforce dominance. However, limited accessibility in rural regions restricts some patient reach.

The Retail Pharmacy segment is expected to witness the fastest growth at a CAGR of 6.0% from 2026 to 2033, driven by increasing shift toward outpatient care and long-term medication use. Expanding availability of generic drugs and improved prescription fulfillment systems are boosting accessibility. Rising preference for home-based management of chronic bladder conditions supports segment expansion. Growth of pharmacy chains and digital prescription platforms is also enhancing distribution efficiency. Increasing healthcare decentralization is further driving adoption. However, limited availability of advanced therapies in retail settings restricts higher-value revenue contribution.

North America Underactive Bladder Market Regional Analysis

The United States dominated the North America underactive bladder market with the largest revenue share of 72.6% in 2025, supported by advanced urology care infrastructure, high disease awareness, and strong availability of pharmacotherapy and neuromodulation treatment options. The country benefits from a large geriatric population, rising prevalence of neurogenic disorders such as Parkinson’s disease, multiple sclerosis, spinal cord injuries, and diabetic neuropathy, and well-established clinical pathways for bladder dysfunction management. Strong presence of leading pharmaceutical and medical device companies, along with widespread availability of specialist urology clinics, further strengthens market leadership. Increasing utilization of sacral nerve stimulation, advanced diagnostic tools, and outpatient treatment models continues to drive sustained growth, reinforcing the United States as the dominant contributor in the North America underactive bladder market.

U.S. Underactive Bladder Market Insight

The U.S. underactive bladder market is witnessing strong growth due to high disease awareness, advanced urology care infrastructure, and increasing adoption of pharmacotherapy and neuromodulation-based treatment solutions. The country’s large aging population, along with rising prevalence of neurogenic disorders such as Parkinson’s disease, multiple sclerosis, spinal cord injuries, and diabetic neuropathy, is significantly driving demand for effective bladder dysfunction management. In addition, strong presence of leading pharmaceutical companies, medical device manufacturers, and specialized urology clinics is supporting treatment accessibility. Growing use of sacral nerve stimulation, minimally invasive therapies, and advanced diagnostic technologies continues to accelerate market expansion across hospitals and outpatient care centers.

Canada Underactive Bladder Market Insight

The Canada underactive bladder market is experiencing steady growth, supported by improving access to specialized urology care, rising healthcare awareness, and increasing diagnosis rates of bladder dysfunction disorders. Growing geriatric population and higher prevalence of chronic conditions such as diabetes and neurological disorders are contributing to rising treatment demand. Expansion of publicly funded healthcare services and increasing adoption of neuromodulation therapies are further supporting market development. Additionally, growing focus on minimally invasive treatment approaches and improved clinical infrastructure is enhancing patient access to advanced bladder management solutions across the country.

Mexico Underactive Bladder Market Insight

The Mexico underactive bladder market is gradually expanding due to increasing awareness of urinary disorders, improving healthcare infrastructure, and rising burden of diabetes-related neuropathic complications. Limited but growing access to specialized urology care is driving gradual adoption of pharmacotherapy-based treatment approaches. Urban healthcare centers are increasingly integrating diagnostic and treatment services for bladder dysfunction management. However, affordability constraints and uneven healthcare access remain key challenges. Growing government efforts to strengthen healthcare delivery systems and expand specialist availability are expected to support future market growth in Mexico.

North America Underactive Bladder Market Share

The North America underactive bladder industry is primarily led by well-established companies, including:

- Astellas Pharma Inc. (Japan)

- Boston Scientific Corporation (U.S.)

- Coloplast Corp (Denmark)

- Convatec Group PLC (U.K.)

- Cook (U.S.)

- Hollister Incorporated (U.S.)

- Braun SE (Germany)

- Medtronic (Ireland)

- Teleflex Incorporated (U.S.)

- Wellspect HealthCare (Sweden)

- Laborie Medical Technologies Corp. (Canada)

- Pfizer Inc. (U.S.)

- AbbVie Inc. (U.S.)

- UroMems (France)

- Axonics, Inc. (U.S.)

- R. Bard, Inc. (U.S.)

- Olympus Corporation (Japan)

- Fresenius Medical Care AG (Germany)

- Cogentix Medical, Inc. (U.S.)

- BD (U.S.)

Latest Developments in North America Underactive Bladder Market

- In September 2025, Medtronic, a global medical technology leader, received FDA approval for its Altaviva™ implantable tibial neuromodulation system, expanding minimally invasive treatment options for urinary retention and bladder dysfunction in North America. The device is designed to improve nerve signaling through ankle-based stimulation, offering an alternative to traditional sacral neuromodulation and enhancing outpatient care for patients with chronic bladder control disorders. This approval strengthens Medtronic’s position in the urology neuromodulation space and broadens access to advanced therapies for underactive bladder-related conditions

- In June 2025, Neuspera Medical, a U.S.-based medtech company, received FDA approval for its integrated sacral neuromodulation (iSNM) system, designed for patients with urinary urge incontinence and bladder dysfunction disorders. The system introduces a battery-free, miniaturized implant that is activated externally, reducing the need for surgical battery replacements and improving long-term patient comfort. Clinical trial data supporting the approval showed strong responder rates and significant improvement in urinary symptoms, marking a major advancement in minimally invasive neuromodulation therapy in North America

- In January 2023, Axonics (now part of Boston Scientific following a 2024 acquisition agreement), received FDA approval for its fourth-generation Axonics R20 sacral neuromodulation system in the United States, expanding treatment options for urinary retention and bladder dysfunction. The device features a rechargeable implant with a long operational lifespan of up to 20 years and improved MRI compatibility, enhancing long-term disease management for patients with neurogenic and non-neurogenic bladder disorders

- In March 2022, Medtronic announced the first patient implants in its investigational implantable tibial neuromodulation (TNM) therapy program in the United States, marking a key step in expanding minimally invasive nerve stimulation options for bladder dysfunction. The TITAN study evaluates alternative neuromodulation approaches for urinary incontinence and retention, aiming to broaden treatment pathways beyond sacral nerve stimulation. This initiative reflects growing innovation in next-generation urology therapies and increasing demand for alternative device-based solutions in North America

- In February 2022, Medtronic received FDA approval for its InterStim X™ system, a next-generation sacral neuromodulation therapy used for bladder and bowel control disorders. The system offers improved battery life, personalized stimulation settings, and long-term management of urinary retention and neurogenic bladder dysfunction. This development significantly strengthened adoption of implantable neuromodulation therapies across North America and reinforced Medtronic’s leadership in the bladder dysfunction treatment segment

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.