Us Specialty Coffee Caf Market

Market Size in USD Million

USD

56.79 Million

USD

110.87 Million

2025

2033

USD

56.79 Million

USD

110.87 Million

2025

2033

| 2026 - 2033 | |

| USD 56.79 Million | |

| USD 110.87 Million | |

| % | |

|

U.S. Specialty Coffee Café Market Size

- The U.S. Specialty Coffee Café Market size was valued at USD 56.79 Million in 2025 and is expected to reach USD 110.87 Million by 2033, at a CAGR of 8.8% during the forecast period

- The market is witnessing consistent expansion as consumer preference continues to shift toward premium, artisally crafted, and experience-driven coffee consumption. Increasing demand for high-quality beans, unique brewing techniques, and differentiated café environments is contributing to sustained growth across urban and suburban regions.

- Specialty coffee cafés, offering single-origin varieties, ethically sourced beans, innovative flavor profiles, and customized beverage experiences, are positioned to deliver superior taste, freshness, and brand engagement. Market growth is being supported by evolving consumer lifestyles, rising disposable incomes, growing café culture, expansion of premium retail formats, and heightened awareness regarding sustainability and responsible sourcing practices.

U.S. Specialty Coffee Café Market Analysis

- A specialty coffee café refers to a retail establishment primarily focused on serving premium-grade coffee prepared using high-quality beans and advanced brewing techniques. These cafés typically emphasize single-origin sourcing, artisanal roasting, and skilled extraction methods.

- Specialty cafés are specifically positioned to deliver enhanced sensory experiences, superior taste profiles, personalized beverage customization, and ethically sourced offerings, along with an inviting ambiance that supports community engagement and lifestyle-driven consumption.

- Technological advancements in coffee roasting equipment, precision brewing systems, digital ordering platforms, customer relationship management tools, and supply chain traceability solutions have improved product consistency, flavor optimization, operational efficiency, and overall customer experience, enabling cafés to offer differentiated menus, reduce waste, and enhance brand loyalty.

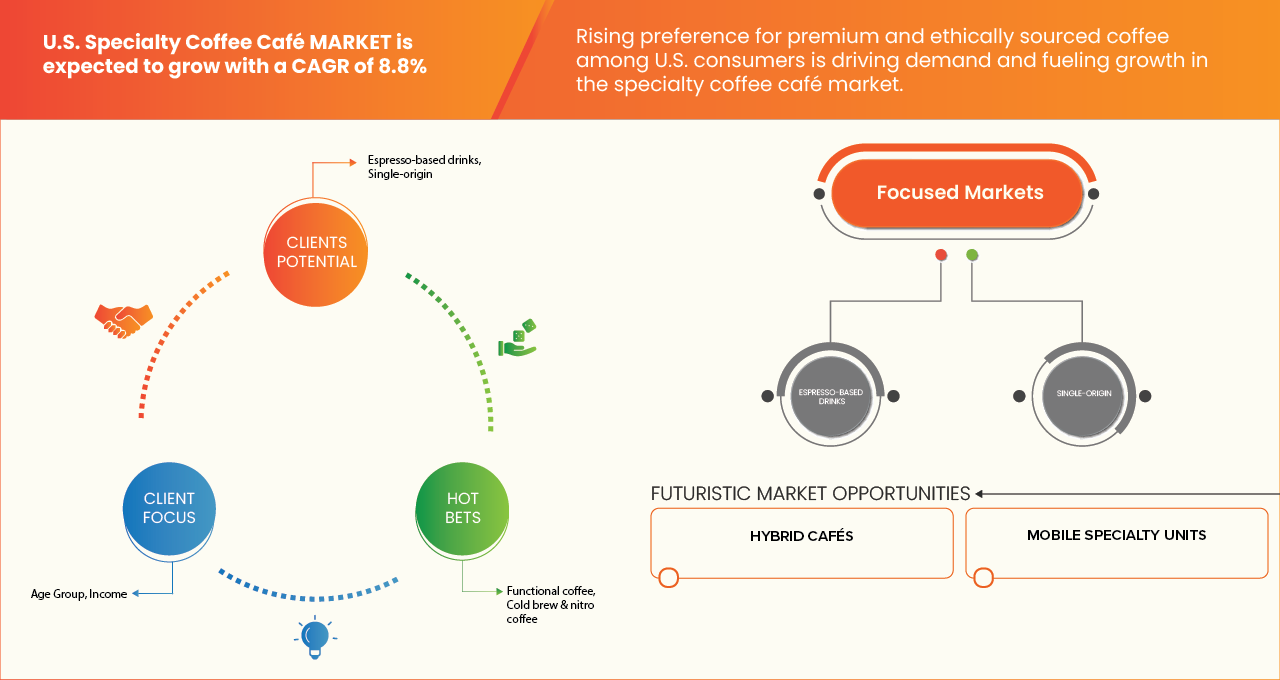

- The Espresso-based drinks segment dominated the largest market revenue share of 37.79% in 2026, driven by increasing consumer demand for traceability, distinctive flavor notes, ethically sourced beans, and high-quality brewing standards that elevate the overall specialty coffee experience.

Report Scope and U.S. Specialty Coffee Café Market Segmentation

|

Attributes |

Middle East and Africa Nickel Alloy Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

U.S. Specialty Coffee Café Market Trends

“Rising Adoption of Specialty and Premium Coffee Experiences in the U.S. Market”

- The rapid growth of the specialty coffee segment is creating significant opportunities in the U.S. Specialty Coffee Café Market. Increasing consumer preference for high-quality, artisanal coffee, supported by rising disposable incomes, urban café culture, and lifestyle-driven consumption, is accelerating café expansion across the country. Specialty coffee sales in the region have surged in recent years, reflecting a shift toward premium, experience-oriented beverage consumption.

- Specialty cafés play a critical role in delivering unique coffee experiences through expertly brewed beverages, ethically sourced beans, and customized drink options. High-quality coffee, including single-origin, espresso-based, cold brew, and functional blends, enables richer flavor profiles, enhanced freshness, and differentiated offerings, making them increasingly preferred by consumers.

- Additionally, specialty cafés focus on quality infrastructure, such as advanced brewing equipment, precision roasting, and efficient service models, where consistency, taste, and customer satisfaction are essential.

- Beyond beverages, the broader adoption of specialty cafés in hybrid formats, takeaway, and mobile units supports convenience, community engagement, and brand differentiation.

- Therefore, as café operators continue to expand locations, diversify offerings, and elevate the consumer experience, the demand for premium and specialty coffee is expected to grow steadily, positioning the segment as a key trend area for the U.S. Specialty Coffee Café Market.

U.S. Specialty Coffee Café Market Dynamics

Driver

“Rising Preference for Premium and Ethically Sourced Coffee Among U.S. Consumers”

- Rising consumer demand for high-quality and ethically sourced coffee is a key driver of the U.S. Specialty Coffee Café Market, particularly among urban and millennial demographics. Coffee enthusiasts are increasingly prioritizing premium beans and sustainable sourcing practices while seeking superior flavor and unique café experiences.

- Specialty coffee offerings provide an optimal combination of exceptional taste, freshness, and traceability, making them well-suited for consumers seeking quality beverages with ethical and environmental credentials.

- These coffees are widely served in single-origin, espresso-based, cold brew, and functional coffee formats where distinctive flavor profiles and sustainable sourcing directly influence consumer choice and loyalty.

- In addition, the emphasis on consistent quality, artisanal preparation, and responsible sourcing enhances customer satisfaction and brand trust, encouraging repeat visits and premium spending. As awareness of ethical coffee sourcing rises and consumers focus on taste and sustainability, cafés are expanding their specialty offerings to meet evolving preferences.

- This continued shift toward premium, ethically sourced, and experience-driven coffee consumption is expected to sustain strong demand for specialty cafés, supporting long-term market growth.

Restraint/Challenge

“Intensifying Competition from Premium Offerings by Large Coffee Chains”

- Increasing competition from established large coffee chains offering premium beverages is emerging as a key challenge for the U.S. Specialty Coffee Café Market. These chains leverage brand recognition, expansive retail networks, and marketing budgets to attract consumers seeking high-quality coffee experiences.

- Competitive pressure from large players has intensified scrutiny on independent specialty cafés, requiring them to differentiate through unique offerings, ethical sourcing, and superior customer experiences.

- Additionally, large chains benefit from economies of scale, advanced supply chain management, and consistent product quality, making it difficult for smaller cafés to compete on price and convenience.

- As consumer awareness of premium and ethically sourced options grows, specialty cafés face growing expectations to match or exceed the offerings of major chains, including innovative beverages, loyalty programs, and café ambiance.

- Rising market saturation and aggressive expansion of large players also create challenges for location selection, foot traffic, and customer retention for independent operators.

- Furthermore, maintaining high-quality beans, sustainable sourcing, and artisanal preparation in the face of competitive pricing pressures increases operational costs, potentially limiting profitability and slowing market expansion. Collectively, these competitive, operational, and market pressures may influence growth trajectories for smaller specialty cafés.

U.S. Specialty Coffee Café Market Scope

The US Specialty Coffee Café Market is categorized into five key segments intoproduct type, café size, service format, demographics, and sales channel.

By Product Type

On the basis of product type, the US Specialty Coffee Café market is segmented into espresso-based drinks, single-origin coffees, cold brew & nitro coffee, functional coffee, and others.

The Espresso-based drinks segment dominated the largest market revenue share of 37.81% in 2025, driven by its exceptional flavor consistency, wide consumer appeal, and versatility in premium café offerings, making it indispensable for specialty cafés focusing on high-quality, artisanal beverage experiences.

The Functional coffee segment is anticipated to witness the fastest CAGR of 9.1% from 2026 to 2033, fueled by escalating demand for health-oriented and performance-enhancing coffee beverages, particularly among urban consumers, fitness enthusiasts, and wellness-focused demographics, where fortified blends and functional ingredients excel in delivering added benefits.

By Café Size

On the basis of café size, the US Specialty Coffee Café market is segmented into small, medium, and large cafés.

The Medium segment held the largest market revenue share of 54.92% in 2025, driven by its versatility in catering to diverse consumer preferences, offering the perfect balance of portion size, flavor intensity, and beverage experience in specialty cafés across urban and suburban areas.

The Small segment is expected to witness the fastest CAGR of 9.1% from 2026 to 2033, driven by surging demand for convenient, on-the-go coffee options, takeaway-focused consumption, and portability that aligns with busy lifestyles and compact café formats.

By Service Format

On the basis of service format, the US Specialty Coffee Café market is segmented into traditional sit-in cafés, takeaway, hybrid cafés, mobile specialty units, and others.

The Traditional Sit-In Cafés segment dominated the market with a revenue share of 48.03% in 2025, fueled by escalating consumer preference for immersive café experiences, premium beverage offerings, and social ambiance where patrons seek comfortable seating, personalized service, and high-quality specialty coffee.

The Hybrid Cafés segment is anticipated to witness the fastest CAGR of 8.7% from 2026 to 2033, driven by the burgeoning demand for flexible café formats combining takeaway, delivery, and sit-in options, catering to busy urban lifestyles and diverse consumer preferences.

By Demographic

On the basis of demographic, the US Specialty Coffee Café market is segmented into age group, income, and occupation.

The Age Group segment dominated the market with a revenue share of 44.68% in 2025, driven by surging preference for specialty coffee among key age demographics, particularly millennials and Gen Z consumers who seek premium, ethically sourced beverages and immersive café experiences.

The Income segment is expected to witness the fastest CAGR of 8.8% from 2026 to 2033, fueled by rising demand from higher-income consumers for artisanal, functional, and ethically sourced coffee options that offer superior quality, customized flavors, and lifestyle-oriented experiences.

By Sales Channel

On the basis of sales channel, the US Specialty Coffee Café market is segmented into on-premise and retail & at-home channels.

The On-Premise segment dominated the market with a revenue share of 58.34% in 2025, driven by surging consumer preference for enjoying specialty coffee within café settings that offer premium ambiance, personalized service, and immersive beverage experiences.

The Retail & At-Home Channels segment is expected to witness the fastest CAGR of 9.1% from 2026 to 2033, fueled by rising demand for convenient, ready-to-brew, and packaged specialty coffee products that allow consumers to enjoy high-quality, artisanal beverages in their homes or on the go.

U.S. Specialty Coffee Café Market Players

The U.S. Specialty Coffee Café Market is primarily led by well-established companies, including:

- The Coffee Movement (U.S.)

- Peregrine Espresso (U.S.)

- Houndstooth Coffee (U.S.)

- Caffe Driade (U.S.)

- Public Espresso (U.S.)

- Bloc 11 Café (U.S.)

- Black Dog Coffeehouse (U.S.)

- Phin Coffee House (U.S.)

- Abraço (U.S.)

- Devil's Food Bakery (U.S.)

- Q Specialty Coffee (U.S.)

- Cafe Grumpy (U.S.)

Latest Developments in the Middle East and Africa Nickel Alloy Market

- In August 2024, Company launched its Small Batch Roasted Instant Coffee, offering a convenient way for consumers to prepare café quality coffee drinks at home by simply adding hot or cold water. The product featured several signature blends from the brand’s roasted coffee line, expanding its retail offerings beyond whole beans and café beverages. This enabled the company to enter the at home ready-to-drink coffee segment.

- In June 2023, Caffè Driade has announced that it is now a Certified Living Wage Employer, reaffirming its commitment to ethical employment practices and fair compensation for its workforce. By voluntarily adopting living wage standards, the company ensures that all employees receive pay that reflects the real cost of living, fostering greater financial security and wellbeing. This milestone aligns with Caffè Driade’s values of social responsibility, respect for its team and community engagement, while setting a positive example for fair labour practices within the specialty coffee industry.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF US SPECIALTY COFFEE CAFÉ MARKET

1.4 LIMITATIONS

1.5 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 CURRENCY AND PRICING

2.5 DBMR TRIPOD DATA VALIDATION MODEL

2.6 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.7 MULTIVARIATE MODELLING

2.8 DBMR MARKET POSITION GRID

2.9 VENDOR SHARE ANALYSIS

2.1 MARKET END-USER COVERAGE GRID

2.11 SECONDARY SOURCES

2.12 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 PORTER’S FIVE FORCES

4.1.1 THREAT OF NEW ENTRANTS

4.1.2 BARGAINING POWER OF SUPPLIERS

4.1.3 BARGAINING POWER OF BUYERS

4.1.4 THREAT OF SUBSTITUTES

4.1.5 COMPETITIVE RIVALRY

4.2 CONSUMER BUYING BEHAVIOUR

4.2.1 OVERVIEW:

4.2.2 CONSUMER PROFILE AND SEGMENTATION

4.2.3 PSYCHOGRAPHIC CHARACTERISTICS:

4.2.4 KEY DRIVERS OF CONSUMER BUYING BEHAVIOUR

4.2.5 PRODUCT QUALITY AND SENSORY EXPERIENCE

4.2.6 PRICE SENSITIVITY AND PERCEIVED VALUE

4.2.7 ETHICAL SOURCING AND SUSTAINABILITY

4.2.8 BRAND IMAGE AND DIGITAL INFLUENCE

4.2.9 BRAND REPUTATION

4.2.10 ROLE OF DIGITAL MEDIA AND REVIEWS

4.2.11 CONSUMER PURCHASE DECISION PROCESS

4.2.12 CONSUMPTION PATTERNS

4.2.13 CAFE AS A “THIRD PLACE”

4.2.14 CHALLENGES INFLUENCING BUYING BEHAVIOUR

4.2.15 CONCLUSION

4.3 VENDOR SELECTION CRITERIA

4.4 TARIFFS & IMPACT ON THE MARKET

4.4.1 CURRENT TARIFF RATE

4.4.2 OVERVIEW

4.4.3 HARMONIZED TARIFF SCHEDULE (HTS) – COFFEE CLASSIFICATIONS AND RATES

4.4.4 COFFEE PREPARATIONS & EXTRACTS

4.4.5 RECENT TRADE POLICY DEVELOPMENTS

4.4.5.1 2025 TARIFF ACTIONS AND EXEMPTIONS:

4.4.5.2 NON-TARIFF IMPORT COSTS:

4.4.6 OUTLOOK: LOCAL PRODUCTION V/S IMPORT RELIANCE

4.4.7 VENDOR SELECTION CRITERIA DYNAMICS

4.4.8 IMPACT ON SUPPLY CHAIN

4.4.9 RAW MATERIAL PROCUREMENT

4.4.10 MANUFACTURING AND PRODUCTION

4.4.11 LOGISTICS AND DISTRIBUTION

4.4.12 PRICE PITCHING AND POSITION OF MARKET

4.4.13 INDUSTRY PARTICIPANTS: PROACTIVE MOVES

4.4.14 SUPPLY CHAIN OPTIMIZATION

4.4.15 JOINT VENTURE ESTABLISHMENTS

4.4.16 IMPACT ON PRICES

4.4.17 REGULATORY INCLINATION

4.4.18 GEOPOLITICAL SITUATION

4.4.19 TRADE PARTNERSHIPS BETWEEN THE COUNTRIES

4.4.19.1 FREE TRADE AGREEMENTS

4.4.19.2 ALLIANCES ESTABLISHMENTS

4.4.20 STATUS ACCREDITATION (INCLUDING MFTN)

4.4.21 DOMESTIC COURSE OF CORRECTION

4.4.21.1 INCENTIVE SCHEMES TO BOOST PRODUCTION OUTPUTS

4.4.21.2 ESTABLISHMENT OF SEZS/INDUSTRIAL PARKS

4.5 CLIMATE CHANGE SCENARIO

4.5.1 ENVIRONMENTAL CONCERNS

4.5.2 INDUSTRY RESPONSE

4.5.3 GOVERNMENT’S ROLE

4.5.4 ANALYST RECOMMENDATIONS

4.6 INDUSTRY ECO-SYSTEM ANALYSIS

4.6.1 PROMINENT COMPANIES

4.6.2 SMALL & MEDIUM SIZE COMPANIES

4.6.3 END USERS

4.7 VALUE CHAIN ANALYSIS

4.7.1 RAW MATERIAL PROCUREMENT

4.7.2 MANUFACTURING & PROCESSING

4.7.3 PACKAGING & STORAGE

4.7.4 DISTRIBUTION & LOGISTICS

4.7.5 END-USE INDUSTRIES

4.8 BRAND OUTLOOK – US SPECIALTY COFFEE CAFÉ MARKET

4.8.1 INTRODUCTION

4.8.2 BRAND POSITIONING

4.8.3 BRAND IDENTITY AND DIFFERENTIATION

4.8.4 BRAND AWARENESS & PERCEPTION

4.8.5 BRAND LOYALTY & CUSTOMER RETENTION

4.8.6 BRAND MESSAGING AND COMMUNICATION

4.8.7 BRAND VISUAL IDENTITY

4.8.8 BRAND EQUITY ASSESSMENT

4.8.9 BRAND CHALLENGES & OPPORTUNITIES

4.8.10 COMPETITIVE BRAND LANDSCAPE

4.8.11 BRAND EXPANSION & FUTURE STRATEGY

4.8.12 CONCLUSION

4.9 INNOVATION TRACKER AND STRATEGIC ANALYSIS

4.9.1 INTRODUCTION

4.9.2 MAJOR DEALS AND STRATEGIC ALLIANCES ANALYSIS

4.9.3 JOINT VENTURES

4.9.4 MERGERS AND ACQUISITIONS

4.9.5 LICENSING AND PARTNERSHIPS

4.9.6 TECHNOLOGY COLLABORATIONS

4.9.7 STRATEGIC DIVESTMENTS

4.9.8 NUMBER OF PRODUCTS IN DEVELOPMENT

4.9.9 STAGE OF DEVELOPMENT

4.9.10 TIMELINES AND MILESTONES

4.9.11 INNOVATION STRATEGIES AND METHODOLOGIES

4.9.12 RISK ASSESSMENT AND MITIGATION

4.9.13 FUTURE OUTLOOK

4.9.14 CONCLUSION

4.1 RAW MATERIAL COVERAGE

4.10.1 INTRODUCTION

4.10.2 COFFEE BEANS – THE CORE RAW MATERIAL

4.10.2.1 ORIGIN AND SOURCING

4.10.2.2 ROAST PROFILES AND CUSTOMIZATION

4.10.2.3 SPECIALTY AND RARE VARIETALS

4.10.2.4 FRESHNESS AND STORAGE PRACTICES

4.10.2.5 INTEGRATION WITH MENU INNOVATION

4.10.3 DAIRY AND MILK ALTERNATIVES – ENHANCING FLAVOR AND TEXTURE

4.10.3.1 TRADITIONAL DAIRY SOURCING

4.10.3.2 MILK ALTERNATIVES AND DIETARY INCLUSIVITY

4.10.3.3 FRESHNESS AND HANDLING PRACTICES

4.10.3.4 SPECIALTY INGREDIENTS AND FLAVOR ENHANCERS

4.10.3.5 SUSTAINABILITY AND ETHICAL CONSIDERATIONS

4.10.3.6 INTEGRATION WITH COFFEE BEVERAGE INNOVATION

4.10.4 SYRUPS, SWEETENERS, AND FLAVOR ENHANCERS – ELEVATING TASTE PROFILES

4.10.4.1 ARTISANAL AND NATURAL SYRUPS

4.10.4.2 SEASONAL AND LIMITED-EDITION FLAVORS

4.10.4.3 ALTERNATIVE SWEETENERS FOR DIETARY NEEDS

4.10.4.4 SPICES AND FLAVOR ENHANCERS

4.10.4.5 FRESHNESS AND STORAGE MANAGEMENT

4.10.4.6 INTEGRATION WITH MENU INNOVATION

4.10.4.7 ETHICAL AND SUSTAINABLE SOURCING

4.10.5 PACKAGING, CONSUMABLES, AND ANCILLARY MATERIALS – SUPPORTING THE CUSTOMER EXPERIENCE

4.10.5.1 ECO-FRIENDLY AND FUNCTIONAL PACKAGING

4.10.5.2 CONSUMABLES FOR IN-CAFÉ USE

4.10.5.3 PACKAGING FOR RETAIL AND TAKEAWAY

4.10.5.4 ANCILLARY INGREDIENTS AND TOPPINGS

4.10.5.5 INVENTORY AND STORAGE MANAGEMENT

4.10.5.6 SUSTAINABILITY AND CUSTOMER PERCEPTION

4.10.5.7 INTEGRATION WITH OVERALL CAFÉ EXPERIENCE

4.10.6 WATER QUALITY AND BREWING ESSENTIALS – ENSURING CONSISTENT FLAVOR AND EXTRACTION

4.10.6.1 IMPORTANCE OF WATER QUALITY IN SPECIALTY COFFEE

4.10.6.2 FILTRATION AND PURIFICATION SYSTEMS

4.10.6.3 WATER TEMPERATURE AND BREWING CONTROL

4.10.6.4 INTEGRATION WITH EQUIPMENT AND RAW MATERIALS

4.10.6.5 COLD BREW AND SPECIALTY WATER APPLICATIONS

4.10.6.6 SUSTAINABILITY AND RESOURCE MANAGEMENT

4.10.6.7 ENHANCING CUSTOMER EXPERIENCE THROUGH WATER QUALITY

4.10.7 CONCLUSION

4.11 SUPPLY CHAIN ANALYSIS – US SPECIALTY COFFEE CAFÉ MARKET

4.11.1 INTRODUCTION

4.11.2 RAW MATERIAL SOURCING & PROCUREMENT:

4.11.3 PROCESSING & PRODUCT MANUFACTURING (PRODUCTION)

4.11.4 SUPPLY CHAIN & DISTRIBUTION LOGISTICS (TRANSPORTATION)

4.11.5 RETAIL & COMMERCIAL BUYER CHANNELS (DISTRIBUTION & SALES)

4.11.6 CONCLUSION

4.12 TECHNOLOGICAL ADVANCEMENTS– US SPECIALTY COFFEE CAFÉ MARKET

4.12.1 INTRODUCTION

4.12.2 DIGITAL ORDERING & MOBILE APPS

4.12.3 CONTACTLESS AND MOBILE PAYMENTS

4.12.4 IOT AND SMART EQUIPMENT IN CAFÉ OPERATIONS

4.12.5 CUSTOMER DATA ANALYTICS FOR PERSONALIZATION

4.12.6 AUTOMATED AND SEMI‑AUTOMATED COFFEE MACHINES

4.12.7 SOCIAL MEDIA & DIGITAL MARKETING TECHNOLOGIES

4.12.8 CONCLUSION

4.13 PRICING ANALYSIS

5 REGULATION COVERAGE– U.S. SPECIALTY COFFEE CAFÉ MARKET

5.1 INTRODUCTION

5.2 PRODUCT CODES

5.3 CERTIFIED STANDARDS

5.4 SAFETY STANDARDS

5.4.1 MATERIAL HANDLING & STORAGE

5.4.2 TRANSPORT & PRECAUTIONS

5.4.3 HAZARD IDENTIFICATION

5.5 CONCLUSION

6 MARKET OVERVIEW

6.1 DRIVERS

6.1.1 RISING PREFERENCE FOR PREMIUM AND ETHICALLY SOURCED COFFEE AMONG U.S. CONSUMERS.

6.1.2 EXPANSION OF CAFÉ CULTURE AS SOCIAL AND WORKSPACES IN METROPOLITAN AREAS.

6.1.3 MENU INNOVATION FOCUSED ON CRAFT BEVERAGES AND CUSTOMIZATION

6.1.4 STRONG PRESENCE OF INDEPENDENT AND REGIONAL SPECIALTY CAFÉ BRANDS

6.2 RESTRAINTS

6.2.1 HIGH OPERATING COSTS ACROSS PRIME URBAN LOCATIONS.

6.2.2 PRICE SENSITIVITY OUTSIDE PREMIUM URBAN CONSUMER SEGMENTS

6.3 OPPORTUNITIES

6.3.1 GROWTH OF READY-TO-DRINK AND TAKE-AWAY SPECIALTY COFFEE FORMATS

6.3.2 INCREASING ADOPTION OF TECHNOLOGY-ENABLED ORDERING AND LOYALTY PLATFORMS

6.3.3 RISING DEMAND FOR SUSTAINABILITY-FOCUSED CAFÉ OPERATIONS

6.4 CHALLENGES

6.4.1 INTENSIFYING COMPETITION FROM PREMIUM OFFERINGS BY LARGE COFFEE CHAINS

6.4.2 DEPENDENCE ON SKILLED BARISTAS AND WORKFORCE RETENTION ISSUES

7 U.S. SPECIALTY COFFEE CAFÉ MARKET, BY PRODUCT TYPE

7.1 OVERVIEW

7.2 U.S. SPECIALTY COFFEE CAFÉ MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

7.2.1 ESPRESSO-BASED DRINKS

7.2.2 SINGLE-ORIGIN

7.2.3 COLD BREW & NITRO COFFEE

7.2.4 FUNCTIONAL COFFEE

7.2.5 OTHERS

7.3 U.S. SPECIALTY COFFEE CAFÉ MARKET, BY PRODUCT TYPE, 2018-2033 (THOUSAND UNITS)

7.3.1 ESPRESSO-BASED DRINKS

7.3.2 SINGLE-ORIGIN

7.3.3 COLD BREW & NITRO COFFEE

7.3.4 FUNCTIONAL COFFEE

7.3.5 OTHERS

7.4 ESPRESSO-BASED DRINKS IN U.S. SPECIALTY COFFEE CAFÉ MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

7.4.1 LATTES

7.4.2 CAPPUCCINOS

7.4.3 MACCHIATOS

7.5 ESPRESSO-BASED DRINKS IN U.S. SPECIALTY COFFEE CAFÉ MARKET, BY PRODUCT TYPE, 2018-2033 (THOUSAND UNITS)

7.5.1 LATTES

7.5.2 CAPPUCCINOS

7.5.3 MACCHIATOS

8 U.S. SPECIALTY COFFEE CAFÉ MARKET, BY CAFÉ SIZE

8.1 OVERVIEW

8.2 U.S. SPECIALTY COFFEE CAFÉ MARKET, BY CAFÉ SIZE, 2018-2033 (USD THOUSAND)

8.2.1 MEDIUM

8.2.2 SMALL

8.2.3 LARGE

9 U.S. SPECIALTY COFFEE CAFÉ MARKET, BY SERVICE FORMAT

9.1 OVERVIEW

9.2 U.S. SPECIALTY COFFEE CAFÉ MARKET, BY SERVICE FORMAT, 2018-2033 (USD THOUSAND)

9.2.1 TRADITIONAL SIT-IN CAFÉS

9.2.2 TAKEAWAY

9.2.3 HYBRID CAFÉS

9.2.4 MOBILE SPECIALTY UNITS

9.2.5 OTHERS

10 U.S. SPECIALTY COFFEE CAFÉ MARKET, BY DEMOGRAPHIC

10.1 OVERVIEW

10.2 U.S. SPECIALTY COFFEE CAFÉ MARKET, BY DEMOGRAPHIC, 2018-2033 (USD THOUSAND)

10.2.1 AGE GROUP

10.2.2 INCOME

10.2.3 OCCUPATION

10.3 AGE GROUP IN U.S. SPECIALTY COFFEE CAFÉ MARKET, BY DEMOGRAPHIC, 2018-2033 (USD THOUSAND)

10.3.1 GEN Z (18–24)

10.3.2 MILLENNIALS (25–40)

10.3.3 GEN X (41–56)

10.3.4 BOOMERS (57+)

10.4 INCOME IN U.S. SPECIALTY COFFEE CAFÉ MARKET, BY DEMOGRAPHIC, 2018-2033 (USD THOUSAND)

10.4.1 HIGH INCOME

10.4.2 MEDIUM INCOME

10.4.3 BUDGET ORIENTED

10.5 INCOME IN U.S. SPECIALTY COFFEE CAFÉ MARKET, BY DEMOGRAPHIC, 2018-2033 (USD THOUSAND)

10.5.1 STUDENTS

10.5.2 PROFESSIONALS

10.5.3 REMOTE WORKERS

10.5.4 OTHERS

11 U.S. SPECIALTY COFFEE CAFÉ MARKET, BY SALES CHANNEL

11.1 OVERVIEW

11.2 U.S. SPECIALTY COFFEE CAFÉ MARKET, BY SALES CHANNEL, 2018-2033 (USD THOUSAND)

11.2.1 ON-PREMISE

11.2.2 RETAIL & AT-HOME CHANNELS

12 US SPECIALTY COFFEE CAFÉ MARKET: COMPANY LANDSCAPE

12.1 COMPANY SHARE ANALYSIS: US

13 COMPANY PROFILES

13.1 THE COFFEE MOVEMENT

13.1.1 COMPANY SNAPSHOT

13.1.2 PRODUCT PORTFOLIO

13.1.3 RECENT DEVELOPMENT

13.2 PEREGRINE ESPRESSO

13.2.1 COMPANY SNAPSHOT

13.2.2 PRODUCT PORTFOLIO

13.2.3 RECENT DEVELOPMENT

13.3 HOUNDSTOOTH COFFEE

13.3.1 COMPANY SNAPSHOT

13.3.2 PRODUCT PORTFOLIO

13.3.3 RECENT DEVELOPMENT

13.4 CAFFE DRIADE

13.4.1 COMPANY SNAPSHOT

13.4.2 PRODUCT PORTFOLIO

13.4.3 RECENT DEVELOPMENT

13.5 PUBLIC ESPRESSO

13.5.1 COMPANY SNAPSHOT

13.5.2 PRODUCT PORTFOLIO

13.5.3 RECENT DEVELOPMENT

13.6 ABRACO

13.6.1 COMPANY SNAPSHOT

13.6.2 PRODUCT PORTFOLIO

13.6.3 RECENT DEVELOPMENT

13.7 BLACKDOG COFFEEHOUSE

13.7.1 COMPANY SNAPSHOT

13.7.2 PRODUCT PORTFOLIO

13.7.3 RECENT DEVELOPMENT

13.8 BLOC CAFE

13.8.1 COMPANY SNAPSHOT

13.8.2 PRODUCT PORTFOLIO

13.8.3 RECENT DEVELOPMENT

13.9 CAFÉ GRUMPY

13.9.1 COMPANY SNAPSHOT

13.9.2 PRODUCT PORTFOLIO

13.9.3 RECENT DEVELOPMENT

13.1 DEVIL’S FOOD BAKERY

13.10.1 COMPANY SNAPSHOT

13.10.2 PRODUCT PORTFOLIO

13.10.3 RECENT DEVELOPMENT

13.11 PHIN COFFEE HOUSE

13.11.1 COMPANY SNAPSHOT

13.11.2 PRODUCT PORTFOLIO

13.11.3 RECENT DEVELOPMENT

13.12 Q SPECIALTY COFFEE

13.12.1 COMPANY SNAPSHOT

13.12.2 PRODUCT PORTFOLIO

13.12.3 RECENT DEVELOPMENT

14 QUESTIONNAIRE

15 RELATED REPORTS

List of Table

TABLE 1 DEMOGRAPHIC CHARACTERISTICS OF U.S. SPECIALTY COFFEE CONSUMERS

TABLE 2 PRICE SENSITIVITY BY COFFEE CONSUMER TYPE

TABLE 3 INFLUENCE OF INFORMATION SOURCES ON PURCHASE DECISIONS

TABLE 4 SPECIALTY COFFEE CONSUMPTION BEHAVIOUR

TABLE 5 VENDOR SELECTION CRITERIA FOR A SPECIALTY COFFEE CAFÉ IN THE UNITED STATES

TABLE 6 COFFEE BEANS (GREEN AND ROASTED)

TABLE 7 U.S. TARIFF RATES FOR COFFEE PREPARATIONS AND EXTRACTS

TABLE 8 NON-TARIFF IMPORT COSTS FOR COFFEE IMPORTS INTO THE U.S.

TABLE 9 IMPACT OF TARIFFS ON VENDOR SELECTION CRITERIA DYNAMICS:

TABLE 10 ANALYST RECOMMENDATIONS FOR CLIMATE CHANGE MITIGATION IN THE U.S. SPECIALTY COFFEE MARKET

TABLE 11 BRAND COMPARATIVE ANALYSIS – US SPECIALTY COFFEE CAFÉS

TABLE 12 KEY RAW MATERIALS DRIVING QUALITY AND INNOVATION IN U.S. SPECIALTY COFFEE CAFÉS

TABLE 13 SUPPLY CHAIN STAGES OF U.S. SPECIALTY COFFEE CAFÉS – INDEPENDENT & SMALL-SCALE OPERATORS

TABLE 14 U.S. SPECIALTY COFFEE CAFÉ MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 15 U.S. SPECIALTY COFFEE CAFÉ MARKET, BY PRODUCT TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 16 ESPRESSO-BASED DRINKS IN U.S. SPECIALTY COFFEE CAFÉ MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 17 ESPRESSO-BASED DRINKS IN U.S. SPECIALTY COFFEE CAFÉ MARKET, BY PRODUCT TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 18 U.S. SPECIALTY COFFEE CAFÉ MARKET, BY CAFÉ SIZE, 2018-2033 (USD THOUSAND)

TABLE 19 U.S. SPECIALTY COFFEE CAFÉ MARKET, BY SERVICE FORMAT, 2018-2033 (USD THOUSAND)

TABLE 20 U.S. SPECIALTY COFFEE CAFÉ MARKET, BY DEMOGRAPHIC, 2018-2033 (USD THOUSAND)

TABLE 21 AGE GROUP IN U.S. SPECIALTY COFFEE CAFÉ MARKET, BY DEMOGRAPHIC, 2018-2033 (USD THOUSAND)

TABLE 22 INCOME IN U.S. SPECIALTY COFFEE CAFÉ MARKET, BY DEMOGRAPHIC, 2018-2033 (USD THOUSAND)

TABLE 23 INCOME IN U.S. SPECIALTY COFFEE CAFÉ MARKET, BY DEMOGRAPHIC, 2018-2033 (USD THOUSAND)

TABLE 24 U.S. SPECIALTY COFFEE CAFÉ MARKET, BY SALES CHANNEL, 2018-2033 (USD THOUSAND)

List of Figure

FIGURE 1 US SPECIALTY COFFEE CAFÉ MARKET: SEGMENTATION

FIGURE 2 US SPECIALTY COFFEE CAFÉ MARKET: DATA TRIANGULATION

FIGURE 3 US SPECIALTY COFFEE CAFÉ MARKET: DROC ANALYSIS

FIGURE 4 US SPECIALTY COFFEE CAFÉ MARKET: COUNTRYWISE MARKET ANALYSIS

FIGURE 5 US SPECIALTY COFFEE CAFÉ MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 US SPECIALTY COFFEE CAFÉ MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 7 US SPECIALTY COFFEE CAFÉ MARKET: MULTIVARIATE MODELLING

FIGURE 8 US SPECIALTY COFFEE CAFÉ MARKET: DBMR MARKET POSITION GRID

FIGURE 9 US SPECIALTY COFFEE CAFÉ MARKET: VENDOR SHARE ANALYSIS

FIGURE 10 US SPECIALTY COFFEE CAFÉ MARKET: MARKET END-USER COVERAGE GRID

FIGURE 11 US SPECIALTY COFFEE CAFÉ MARKET: SEGMENTATION

FIGURE 12 US SPECIALTY COFFEE CAFÉ MARKET: EXECUTIVE SUMMARY

FIGURE 13 US SPECIALTY COFFEE CAFÉ MARKET: STRATEGIC DECISIONS

FIGURE 14 RISING PREFERENCE FOR PREMIUM AND ETHICALLY SOURCED COFFEE AMONG U.S. CONSUMERS EXPECTED TO DRIVE THE GROWTH OF THE US SPECIALTY COFFEE CAFÉ MARKET FROM 2026 TO 2033

FIGURE 15 THE TYPE 2 ENDOSCOPIC HEMOSTASIS SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE US SPECIALTY COFFEE CAFÉ MARKET IN 2026 & 2033

FIGURE 16 TWO SEGMENTS COMPRISE THE DOMINICAN REPUBLIC ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE

FIGURE 17 PORTER’S FIVE FORCES

FIGURE 18 VALUE CHAIN OF US SPECIALTY COFFEE CAFÉ MARKET

FIGURE 19 YEARLY STRATEGIC DEALS AND ALLIANCES BY INDEPENDENT SPECIALTY COFFEE CAFÉS (2019–2024)

FIGURE 20 NO OF DEALS BY TYPE

FIGURE 21 SUPPLY CHAIN ANALYSIS

FIGURE 22 PROPORTION OF INDEPENDENT U.S. SPECIALTY COFFEE CAFÉS ADOPTING KEY TECHNOLOGIES

FIGURE 23 DROC ANALYSIS

FIGURE 24 U.S. SPECIALTY COFFEE CAFÉ MARKE: BY PRODUCT TYPE, 2025

FIGURE 25 U.S. SPECIALTY COFFEE CAFÉ MARKET: BY CAFÉ SIZE, 2025

FIGURE 26 U.S. SPECIALTY COFFEE CAFÉ MARKET: BY SERVICE FORMAT, 2025

FIGURE 27 U.S. SPECIALTY COFFEE CAFÉ MARKET: BY DEMOGRAPHIC, 2025

FIGURE 28 U.S. SPECIALTY COFFEE CAFÉ MARKET: BY SALES CHANNEL, 2025

FIGURE 29 US SPECIALTY COFFEE CAFÉ MARKET: COMPANY SHARE 2025 (%)

Us Specialty Coffee Caf Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Us Specialty Coffee Caf Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Us Specialty Coffee Caf Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.