The expansion of transmission and distribution infrastructure is a key driver of the station service voltage transformer (SSVT) market, as every new or upgraded substation requires dependable auxiliary power for control, protection, and operation. Rapid urbanization, industrial growth, and increasing renewable energy integration are pushing utilities to invest heavily in grid expansion and modernization worldwide. Large-scale projects—such as India’s multi-billion-dollar transmission expansion, manufacturing investments by major players like Hitachi Energy and Siemens in the U.S., the UK’s SSE £33 billion network upgrade plan, and ongoing distribution strengthening initiatives in Gujarat—are significantly increasing the number of substations. This directly drives the demand for SSVTs, which play a critical role in ensuring stable and independent station service power, making T&D infrastructure growth a sustained long-term catalyst for the global SSVT market.

Access Full Report @ https://www.databridgemarketresearch.com/reports/global-station-service-voltage-transformer-ssvt-market

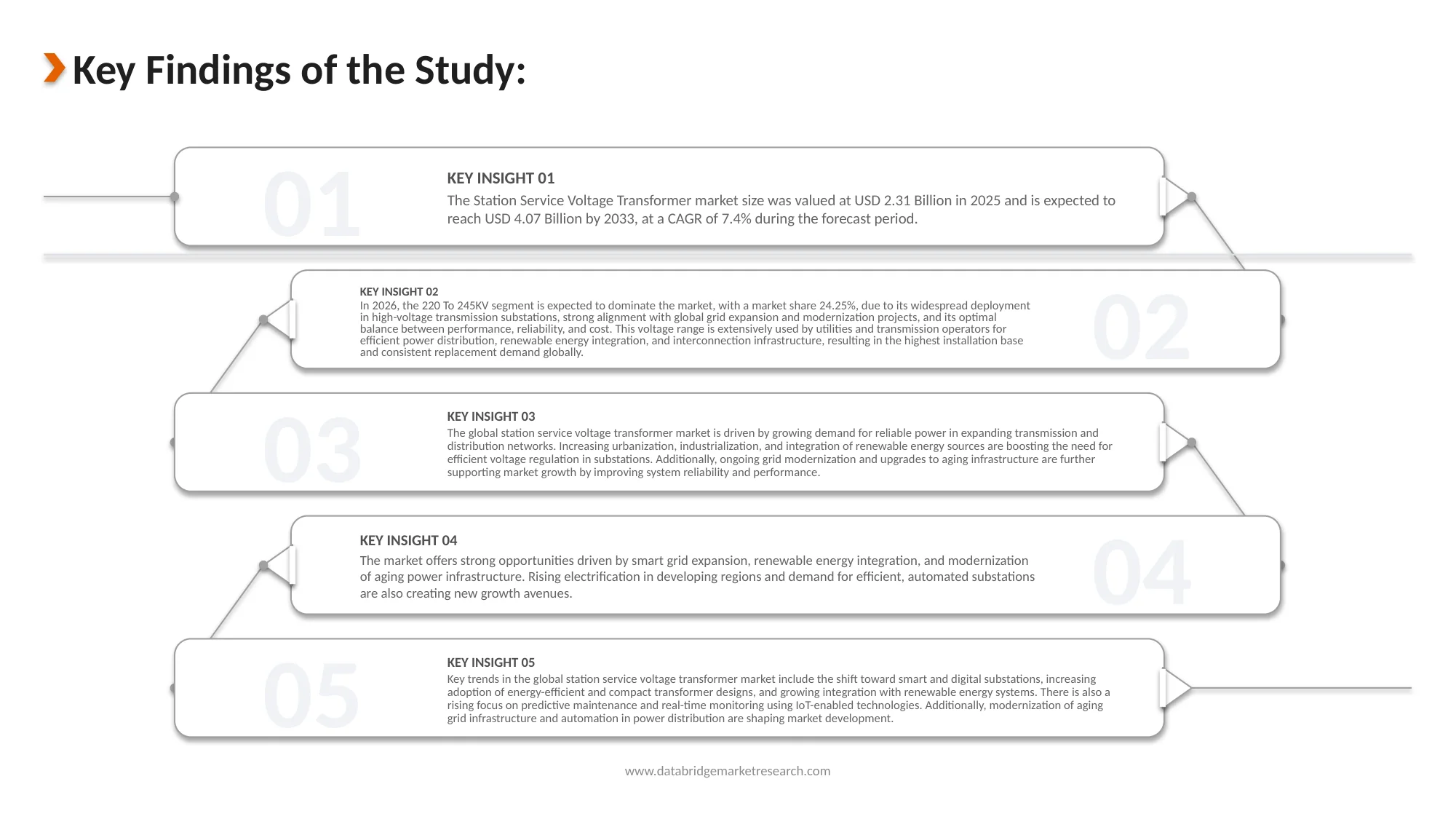

Data Bridge Market Research analyses that the Global Station Service Voltage Transformer (SSVT) Market will grow from USD 2.31 billion in 2025 to USD 4.07 billion by 2033, at a CAGR of 7.4%.

Key Findings of the Study

Increasing Integration of Renewable Energy Sources

The increasing integration of renewable energy sources such as solar and wind is a major driver for the global station service voltage transformer (SSVT) market, as large-scale renewable projects require extensive substation infrastructure for grid connectivity, control, and stability. With renewables often located in remote areas and characterized by intermittent generation, utilities are expanding and upgrading substations to manage variability and ensure reliable power flow. This has heightened the need for dependable auxiliary power systems, where SSVTs play a critical role by providing stable station service power independent of grid fluctuations. Supported by rapid global capacity additions, growing grid connection backlogs, and government-led clean energy initiatives, the expansion of renewable energy continues to drive substation development, thereby significantly boosting demand for SSVTs worldwide.

Report Scope and Market Segmentation

|

Report Metric

|

Details

|

|

Forecast Period

|

2026 to 2033

|

|

Base Year

|

2025

|

|

Historic Years

|

2024 (Customizable from 2018-2023)

|

|

Quantitative Units

|

Revenue in USD Billion

|

|

Segments Covered

|

By voltage level (220 to 245 kV, 132 to 145 kV, 110 to 123 kV, 400 to 420 kV, 66 to 72.5 kV, 275 to 300 kV, 500 to 550 kV, 161 to 170 kV, 150 to 160 kV, 330 to 362 kV), By Power Rating Capacity (Medium Capacity SSVT, High Capacity SSVT, Low Capacity SSVT), By Insulation Type (Oil-Immersed SSVT, Dry-Type SSVT, Gas Insulated SSVT), By Installation Type (Structure Mounted, Pole Mounted), By Phase Configuration (Three Phase SSVT Bank, Single Phase SSVT), By Cooling Technology (Oil Natural, Air Natural), By Output Voltage Type (240 V to 480 V, 110 V to 240 V), By Functional Type (Power Only SSVT, Dual Function SSVT), By Substation Type (Transmission Substations, Collector Substations, Switching Substations), By Application (Substation Auxiliary Power Supply, Industrial Transmission Infrastructure, Renewable Energy Integration, Remote Grid Electrification, Data Center Power Support), By End User (Utilities, Transmission System Operators, Renewable Energy Developers, Industrial Infrastructure Operators, Data Center Operators), By Mounting and Structural Design (Free Standing Units, Compact Integrated Units), By Standards and Compliance (IEC Standard Compliant SSVT, ANSI Standard Compliant SSVT), By Grid Connectivity Type (Direct Line Connected SSVT, Hybrid Grid Connected SSVT), By Digital Integration Level (Conventional SSVT, Smart SSVT, Advanced Digital SSVT), By Country (Japan, China, South Korea, India, Australia, Singapore, Thailand, Malaysia, Indonesia, Philippines, New Zealand, Vietnam, Taiwan, Rest of Asia-Pacific, Germany, France, U.K., Italy, Spain, Russia, Turkey, Belgium, Netherlands, Switzerland, Denmark, Poland, Sweden, Norway, Finland, Rest of Europe, U.S., Canada, Mexico, Argentina, Bolivia, Brazil, Chile, Colombia, Ecuador, Paraguay, Peru, Uruguay, Venezuela, Rest of South America, Saudi Arabia, Israel, United Arab Emirates, Egypt, South Africa, Kuwait, Oman, Qatar, Bahrain and Rest of Middle East and Africa)

|

|

Market Players Covered

|

Hitachi Energy Ltd (Switzerland), Trench Group (Germany), Sieyuan Electric Co., Ltd (China), Arteche (Spain), Guangdong Sihui (China) and Sandian Group (China)

|

|

Data Points Covered in the Report

|

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand.

|

Segment Analysis

Global station service voltage transformer (SSVT) market is categorized into fifteen notable segments which are based on voltage level, power rating capacity, insulation type, installation type, phase configuration, cooling technology, output voltage type, functional type, substation type, application, end user, mounting and structural design, standards and compliance, grid connectivity type, digital integration level.

On the basis of voltage level, global station service voltage transformer (SSVT) market is segmented into 220 to 245 kV, 132 to 145 kV, 110 to 123 kV, 400 to 420 kV, 66 to 72.5 kV, 275 to 300 kV, 500 to 550 kV, 161 to 170 kV, 150 to 160 kV, and 330 to 362 kV.

In 2026, the 220 To 245KV segment is expected to dominate the market

In 2026, the 220 To 245KV segment is expected to dominate the market, with a market share 24.25%, due to its widespread deployment in high-voltage transmission substations, strong alignment with global grid expansion and modernization projects, and its optimal balance between performance, reliability, and cost. This voltage range is extensively used by utilities and transmission operators for efficient power distribution, renewable energy integration, and interconnection infrastructure, resulting in the highest installation base and consistent replacement demand globally.

On the basis of power rating capacity, the global station service voltage transformer (SSVT) market is segmented into medium capacity SSVT, high capacity SSVT, and low capacity SSVT.

In 2026, the medium capacity SSVT segment is expected to dominate the market

In 2026, the medium capacity SSVT segment is expected to dominate the market with a market share 41.96%, due to its broad applicability across transmission and distribution substations, where it meets the majority of auxiliary power requirements without the cost burden of high-capacity systems. This segment offers an optimal balance between load-handling capability, efficiency, and capital expenditure, making it the preferred choice for utilities, renewable energy substations, and industrial infrastructure. Additionally, the high volume of medium-scale grid projects and ongoing substation upgrades globally further drives its dominant share in the SSVT market.

On the basis of insulation type, the global station service voltage transformer (SSVT) market is segmented into oil-immersed SSVT, dry-type SSVT, gas insulated SSVT.

In 2026, the oil-immersed SSVT segment is expected to dominate the market

In 2026, the oil-immersed SSVT segment is expected to dominate the market with a market share 52.59%, due to its superior dielectric strength, efficient heat dissipation, and proven reliability in high-voltage outdoor substation environments. These systems are widely preferred by utilities and transmission operators for their ability to handle higher load conditions and voltage stresses over long operational lifecycles. Additionally, their cost-effectiveness compared to gas-insulated alternatives and established deployment across legacy and new grid infrastructure further support their leading market share globally.

On the basis of installation type, the global station service voltage transformer (SSVT) market is segmented into structure mounted, pole mounted.

In 2026, the structure mounted segment is expected to dominate the market

In 2026, the structure mounted segment is expected to dominate the market with a market share 66.17%, due to its extensive use in high-voltage transmission substations and utility-scale infrastructure, where stable, ground-based installation is critical for handling higher voltage levels and load capacities. Structure-mounted SSVTs offer enhanced mechanical stability, safety, and ease of maintenance, making them the preferred choice for large-scale grid applications. Additionally, the ongoing expansion and modernization of substations globally further drive the demand for structure-mounted installations over pole-mounted alternatives.

On the basis of phase configuration, the global station service voltage transformer (SSVT) market is segmented into three phase SSVT bank, single phase SSVT.

In 2026, the three phase SSVT Bank segment is expected to dominate the market

In 2026, the three phase SSVT Bank segment is expected to dominate the market with a market share 69.61%, due to widespread adoption in transmission and distribution substations, where three-phase power systems are standard. These configurations enable efficient power conversion, balanced load distribution, and improved operational reliability across grid networks. Additionally, three-phase SSVT banks are more suitable for utility-scale and high-capacity applications, making them the preferred choice for modern grid infrastructure and large-scale renewable energy integration projects.

On the basis of cooling technology, the global station service voltage transformer (SSVT) market is segmented into oil natural, air natural.

In 2026, the oil natural segment is expected to dominate the market

In 2026, the oil natural segment is expected to dominate the market with a market share 72.56%, due to its superior cooling efficiency and ability to dissipate heat effectively in high-voltage and high-load operating conditions. Oil natural cooling systems support longer operational life, enhanced thermal stability, and reliable performance under continuous load, making them the preferred choice for utility-scale and transmission substation applications. Additionally, their compatibility with oil-immersed insulation systems and widespread adoption across existing grid infrastructure further reinforce their leading market position.

On the basis of output voltage type, the global station service voltage transformer (SSVT) market is segmented into 240 V to 480 V, 110 V to 240 V.

In 2026, the 240 V to 480 V segment is expected to dominate the market

In 2026, the 240 V to 480 V segment is expected to dominate the market with a market share 57.72%, due to its widespread use in substation auxiliary systems that require higher power output for critical equipment such as control panels, protection systems, cooling units, and heavy-duty operational loads. This voltage range supports better efficiency in power distribution within substations and is more suitable for industrial and utility-scale applications. Additionally, the increasing complexity and load requirements of modern grid infrastructure further drive the demand for higher output voltage configurations, reinforcing the segment’s leading position.

On the basis of functional type, the global station service voltage transformer (SSVT) market is segmented into power only SSVT, dual function SSVT.

In 2026, the power only SSVT segment is expected to dominate the market

In 2026, the power only SSVT segment is expected to dominate the market with a market share 60.98%, due to its simplicity, cost-effectiveness, and widespread deployment in conventional substation applications where the primary requirement is auxiliary power supply. These systems are easier to install, maintain, and integrate into existing grid infrastructure, making them the preferred choice for utilities and transmission operators. Additionally, the large installed base of traditional substations and ongoing replacement demand further support the dominance of power-only configurations over more complex dual-function systems

On the basis of substation type, the global station service voltage transformer (SSVT) market is segmented into transmission substations, collector substations, switching substations.

In 2026, the transmission substations segment is expected to dominate the market

In 2026, the transmission substations segment is expected to dominate the market with a market share 52.39%, due to its critical role in high-voltage power transfer across long-distance grid networks and the extensive deployment of SSVTs for auxiliary power supply in these installations. Transmission substations operate at higher voltage levels and require reliable, continuous power for protection, control, monitoring, and cooling systems, driving higher SSVT demand per installation. Additionally, ongoing grid expansion, cross-border interconnections, and modernization of aging transmission infrastructure globally further reinforce the segment’s leading market share.

On the basis of application, the global station service voltage transformer (SSVT) market is segmented into substation auxiliary power supply, industrial transmission infrastructure, renewable energy integration, remote grid electrification, data center power support.

In 2026, the substation auxiliary power supply segment is expected to dominate the market

In 2026, the substation auxiliary power supply segment is expected to dominate the market with a market share 34.63%, due to fundamental role of SSVTs in supplying reliable auxiliary power for critical substation operations, including protection systems, control panels, monitoring equipment, lighting, and cooling systems. Every transmission and distribution substation requires a dependable internal power source, making this application universal across grid infrastructure. Additionally, the continuous expansion and modernization of substations globally, along with the need for uninterrupted power for grid stability and automation, further drive the dominance of this segment in the SSVT market.

On the basis of end user, the global station service voltage transformer (SSVT) market is segmented into utilities, transmission system operators, renewable energy developers, industrial infrastructure operators, data center operators.

In 2026, the utilities segment is expected to dominate the market

In 2026, the utilities segment is expected to dominate the market with a market share 34.25%, due to their primary responsibility for power generation, transmission, and distribution infrastructure, which requires extensive deployment of SSVTs for reliable auxiliary power in substations. Utilities operate the largest network of substations globally, resulting in high installation volumes and consistent replacement demand. Additionally, ongoing grid expansion, electrification initiatives, and modernization of aging infrastructure further strengthen their dominant share in the SSVT market.

On the basis of mounting and structural design, the global station service voltage transformer (SSVT) market is segmented into free standing units, compact integrated units.

In 2026, the free standing units segment is expected to dominate the market

In 2026, the free standing units segment is expected to dominate the market with a market share 64.13%, due to their widespread deployment in conventional transmission and distribution substations, where space availability is less constrained and flexibility in installation is required. These units offer easier maintenance access, higher mechanical stability, and suitability for high-voltage outdoor environments. Additionally, their compatibility with existing grid infrastructure and lower integration complexity compared to compact systems make them the preferred choice for utilities, reinforcing their dominant share in the global SSVT market.

On the basis of Standards and Compliance, the global station service voltage transformer (SSVT) market is segmented into IEC Standard Compliant SSVT, ANSI Standard Compliant SSVT.

In 2026, the IEC standard compliant SSVT segment is expected to dominate the market

In 2026, the IEC standard compliant SSVT segment is expected to dominate the market with a market share 68.27%, due to its widespread global adoption across Europe, Asia-Pacific, the Middle East, and Africa, where IEC standards form the primary regulatory framework for power equipment. IEC-compliant SSVTs offer strong interoperability, standardized testing protocols, and compatibility with international grid infrastructure projects. Additionally, the increasing number of cross-border transmission projects, renewable energy installations, and utility-scale developments in IEC-dominant regions further drive the demand for IEC-compliant systems, reinforcing their leading market share globally.

On the basis of grid connectivity type, the global station service voltage transformer (SSVT) market is segmented into direct line connected SSVT, hybrid grid connected SSVT.

In 2026, the direct line connected SSVT segment is expected to dominate the market

In 2026, the direct line connected SSVT segment is expected to dominate the market with a market share 63.34%, due to its widespread use in conventional transmission and distribution substations, where direct integration with the primary grid ensures reliable and continuous auxiliary power supply. These systems offer simpler design, lower installation complexity, and higher operational reliability compared to hybrid configurations. Additionally, the large installed base of traditional grid infrastructure and ongoing substation expansion projects globally continue to drive strong demand for direct line connected SSVTs, reinforcing their leading market position.

On the basis of digital integration level, the global station service voltage transformer (SSVT) market is segmented into conventional SSVT, smart SSVT, advanced digital SSVT.

In 2026, the conventional SSVT segment is expected to dominate the market

In 2026, the conventional SSVT segment is expected to dominate the market with a market share 52.25%, due to its large installed base across existing transmission and distribution substations and its proven reliability in delivering stable auxiliary power without the need for complex digital infrastructure. These systems are more cost-effective, easier to maintain, and widely compatible with legacy grid setups. Additionally, while digital substations are growing, their adoption remains gradual, particularly in developing regions, which sustains strong demand for conventional SSVTs and reinforces their leading market share.

Major Players

"Data Bridge Market Research analyzes major players, including Hitachi Energy Ltd (Switzerland), Trench Group (Germany), Sieyuan Electric Co., Ltd (China), Arteche (Spain), Guangdong Sihui (China) and Sandian Group (China).

Market Developments

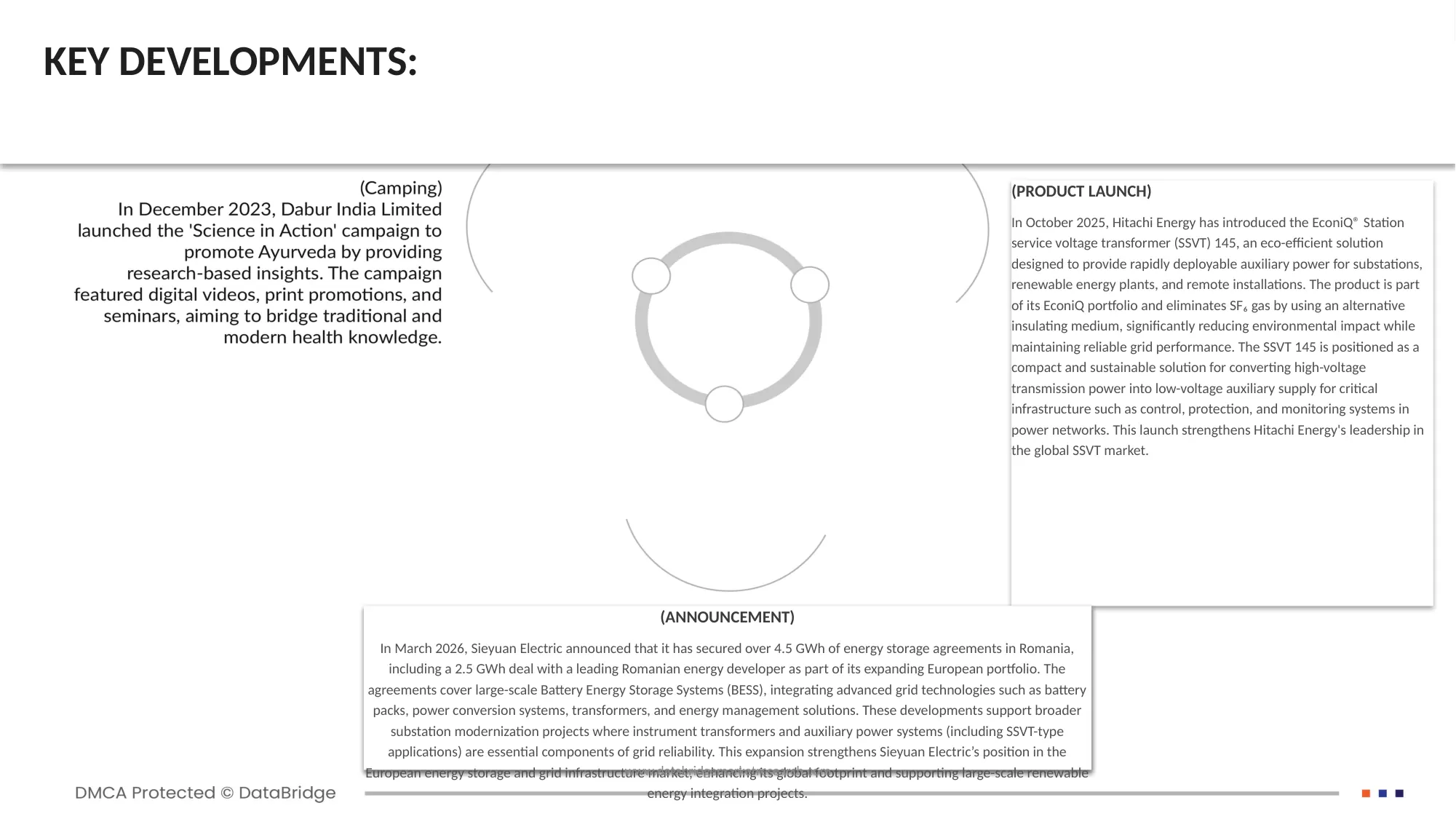

- In October 2025, Hitachi Energy has introduced the EconiQ® Station service voltage transformer (SSVT) 145, an eco-efficient solution designed to provide rapidly deployable auxiliary power for substations, renewable energy plants, and remote installations. The product is part of its EconiQ portfolio and eliminates SF₆ gas by using an alternative insulating medium, significantly reducing environmental impact while maintaining reliable grid performance. The SSVT 145 is positioned as a compact and sustainable solution for converting high-voltage transmission power into low-voltage auxiliary supply for critical infrastructure such as control, protection, and monitoring systems in power networks. This launch strengthens Hitachi Energy’s leadership in the global SSVT market.

- In 2024, Trench Group collaborated with Pfalzwerke and supplied sixClean Air Station service voltage transformers (SSVTs), branded as “Blue Power Voltage Transformers,” to Pfalzwerke in Germany as part of a low-carbon grid modernization initiative. Three of these units were successfully energized at a construction site in Hohenecken, providing auxiliary power for substation operations with reduced environmental impact. The project has been positioned as a “lighthouse project” supporting Germany’s transition toward sustainable and SF₆-free power infrastructure through advanced instrument transformer technology.

- In March 2026, Sieyuan Electric announced that it has secured over 4.5 GWh of energy storage agreements in Romania, including a 2.5 GWh deal with a leading Romanian energy developer as part of its expanding European portfolio. The agreements cover large-scale Battery Energy Storage Systems (BESS), integrating advanced grid technologies such as battery packs, power conversion systems, transformers, and energy management solutions. These developments support broader substation modernization projects where instrument transformers and auxiliary power systems (including SSVT-type applications) are essential components of grid reliability. This expansion strengthens Sieyuan Electric’s position in the European energy storage and grid infrastructure market, enhancing its global footprint and supporting large-scale renewable energy integration projects.

- In February 2020, Arteche Group supplied UGP 420 gas-insulated Power Voltage Transformers (PVT/SSVT) to Iberdrola’s Núñez de Balboa photovoltaic plant in Spain, one of Europe’s largest solar installations. The equipment enables direct conversion of high-voltage transmission lines into low-voltage auxiliary power used for substation operations, including control, protection, and auxiliary systems. This project strengthens Arteche’s position in the global SSVT and PVT market by demonstrating real deployment of station service voltage transformers in large-scale renewable energy infrastructure.

Regional Analysis

Geographically, the country covered in the global station service voltage transformer (SSVT) market report is U.S., Canada, Mexico, Germany, U.K., France, Italy, Spain, Russia, Turkey, Netherlands, Norway, Finland, Denmark, Sweden, Poland, Switzerland, Belgium, Rest of Europe, China, Japan, India, South Korea, Australia, Indonesia, Thailand, Malaysia, Singapore, Philippines, Rest of Asia-Pacific, Brazil, Argentina, rest of South America. Saudi Arabia, U.A.E., South Africa, Egypt, Israel, and rest of Middle East and Africa.

As per Data Bridge Market Research analysis:

Asia-Pacific is the dominant region in the global station service voltage transformer (SSVT) market

Asia-Pacific is the dominant region in the global station service voltage transformer (SSVT) market. due to rapid expansion of power transmission and distribution infrastructure, increasing electricity demand from industrialization and urbanization, and substantial investments in smart grid and renewable energy integration projects. Countries such as China, India, Japan, and South Korea are continuously upgrading substations and expanding grid networks to support growing energy consumption and improve power reliability. Additionally, government initiatives focused on electrification, grid modernization, and renewable energy deployment are driving strong demand for SSVTs across the region.

Asia-Pacific is estimated to be the fastest-growing region in the global station service voltage transformer (SSVT) market

Asia-Pacific is estimated to be the fastest-growing region in the global station service voltage transformer (SSVT) market due to the increasing deployment of ultra-high-voltage (UHV) transmission corridors, rising cross-border power interconnection projects, and growing investments in railway electrification and large-scale infrastructure developments. The region is also benefiting from the expansion of data centers, manufacturing hubs, and energy-intensive industries that require stable and efficient power networks. In addition, favorable regulatory policies supporting grid resilience, energy security, and advanced substation technologies are accelerating the adoption of SSVTs across emerging and developed economies in the region.

As per Data Bridge Market Research analysis: For more detailed information about station service voltage transformer (SSVT) market click here – https://www.databridgemarketresearch.com/reports/global-station-service-voltage-transformer-ssvt-market