Sternotomy and sternal closure are procedures performed before and after cardiac surgery, respectively. Furthermore, significant technological advances, such as the use of biocompatible polymers such as PEEK, tritium, and nitinol, pre-sternotomy plates, and the development of minimally invasive median sternotomy techniques, are projected to boost market expansion. Globally, an increase in the number of surgical procedures has increased demand for surgical tools, resulting in market growth.

Access Full Report @ https://www.databridgemarketresearch.com/reports/global-sternal-closure-systems-market

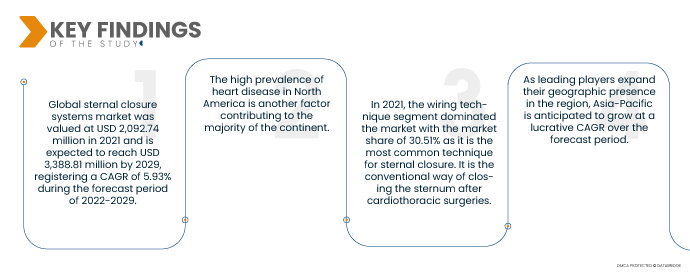

Global Sternal Closure Systems Market was valued at USD 2,092.74 million in 2021 and is expected to reach USD 3,388.81 million by 2029, registering a CAGR of 5.93% during the forecast period of 2022-2029. The rise in the senior population undergoing open-heart surgery using median sternotomy is one of the primary factors driving the growth of the sternal closure devices market. The advancement of technology in sternotomy techniques to improve the operation accelerates market expansion.

Rising prevalence of unhealthy lifestyleis expected to drive the market's growth rate

Globally, sedentary lifestyles, increased alcohol and tobacco use, and poor diet are increasing the prevalence of heart disorders. As a result, surgical operations are increasing, which will likely accelerate the use of sternal closure devices in surgeries throughout the next years. The Centres for Disease Control and Prevention found that 28.1 million adults in the U.S. had a heart disease diagnosis in 2016. This will act as a ppositive determinant for the growth of the market.

Report Scope and Market Segmentation

Report Metric

|

Details

|

Forecast Period

|

2022 to 2029

|

Base Year

|

2021

|

Historic Years

|

2020 (Customizable to 2014- 2019)

|

Quantitative Units

|

Revenue in USD Million, Volumes in Units, Pricing in USD

|

Segments Covered

|

Product (Closure Devices, Bone Cement), Procedure (Median Sternotomy, Hemisternotomy, Bilateral Thoracosternotomy), Fixation Techniques (Wiring Fixation Techniques, Plate-Screw Systems, Interlocking Systems, Cementing, Vacuum Assisted Closure), Material (Stainless Steel, PEEK, Titanium, Others), End Users (Hospitals, Specialized Surgical Centres)

|

Countries Covered

|

U.S., Canada and Mexico in North America, Germany, France, U.K., Netherlands, Switzerland, Belgium, Russia, Italy, Spain, Turkey, Rest of Europe in Europe, China, Japan, India, South Korea, Singapore, Malaysia, Australia, Thailand, Indonesia, Philippines, Rest of Asia-Pacific (APAC) in the Asia-Pacific (APAC), Saudi Arabia, U.A.E, South Africa, Egypt, Israel, Rest of Middle East and Africa (M.E.A.) as a part of Middle East and Africa (M.E.A.), Brazil, Argentina and Rest of South America as part of South America

|

Market Players Covered

|

Zimmer Biomet(美國)、Medical Devices Business Services, Inc.(美國)、KLS Martin Group(德國)、Acute Innovations LLC(美國)、IDEAR SRL(阿根廷)、A&E Medical Corporation(美國)、Praesidia(義大利)、Kinamed Incorporated(美國)、JACE Medical, LLC(美國)、Dispomedica(德國) CORPORATION(韓國)、常州華森醫療器材有限公司(中國)、Teleflex Incorporated(美國)、B. Braun Melsungen AG(德國)和 Sklar Surgical Instruments(美國)

|

報告涵蓋的數據點

|

除了市場價值、成長率、細分市場、地理覆蓋範圍、市場參與者和市場情景等市場洞察外,由 Data Bridge 市場研究團隊策劃的市場報告還包括深入的專家分析、患者流行病學、管道分析、定價分析和監管框架

|

細分分析:

全球胸骨閉合系統市場根據產品、材料、固定技術、程序、最終用戶和分銷管道分為六個顯著的部分。

- 根據產品,全球胸骨閉合系統市場分為閉合裝置和骨水泥。 2021 年,與僅用於有限手術的骨水泥相比,封閉裝置應用範圍更加廣泛,佔據了市場主導地位,市場份額達到 88.06%。

- 根據材料,全球胸骨閉合系統市場分為不銹鋼、鈦、鎳鈦合金、聚醚醚酮、氚和其他。 2021 年,不銹鋼佔據市場主導地位,市場份額為 32.86%,這得益於其在電線、板材、螺絲、電纜等封閉裝置中的大量應用。

- 根據固定技術,全球胸骨閉合系統市場分為佈線技術、板螺絲系統、連鎖系統、水泥固定、真空輔助閉合、胸骨鉗等。 2021 年,佈線技術佔據市場主導地位,市場佔有率為 30.51%,因為它是最常見的胸骨閉合技術。這是心胸外科手術後關閉胸骨的常規方法。

- 根據手術程序,全球胸骨閉合系統市場分為正中胸骨切開術、半胸骨切開術和雙側胸骨切開術。 2021 年,正中胸骨切開術佔據市場主導地位,市佔率為 46.13%,是心胸外科最常見的手術方式。它主要用於接受開胸心臟手術且需要植入 ICD 的患者。

- 根據最終用戶,全球胸骨閉合系統市場分為醫院、專科外科中心和其他。

2021 年,醫院終端用戶部分佔據了胸骨閉合系統市場的主導地位

2021 年,由於發展中國家醫院的擴張、醫療保健提供者數量的增加以及全球大小醫院迅速採用先進技術,醫院部門佔據了 66.11% 的市場份額。

- 根據分銷管道,全球胸骨閉合系統市場分為直接招標和零售。

2021 年,分銷通路領域的直接投標部分佔據了胸骨閉合系統市場的主導地位

直接採購佔據市場主導地位,佔有 76.98% 的市場份額,是醫院採購的主要來源。隨著醫療費用的不斷增加,醫院越來越注重為客戶提供更好的服務,同時降低整體成本。

主要參與者

Data Bridge Market Research 將以下公司視為主要市場參與者:Zimmer Biomet(美國)、Medical Devices Business Services, Inc.(美國)、KLS Martin Group(德國)、Acute Innovations LLC(美國)、IDEAR SRL(阿根廷)、A&E Medical Corporation(美國)、Praesidia(義大利)、Kinamed Incorporated(美國)、JYAated(美國)、JAS AACE,a. INC.(美國)、JEIL MEDICAL CORPORATION(韓國)、常州 Waston 醫療器材有限公司(中國)、Teleflex Incorporated(美國)、B. Braun Melsungen AG(德國)和 Sklar Surgical Instruments(美國)。

市場開發

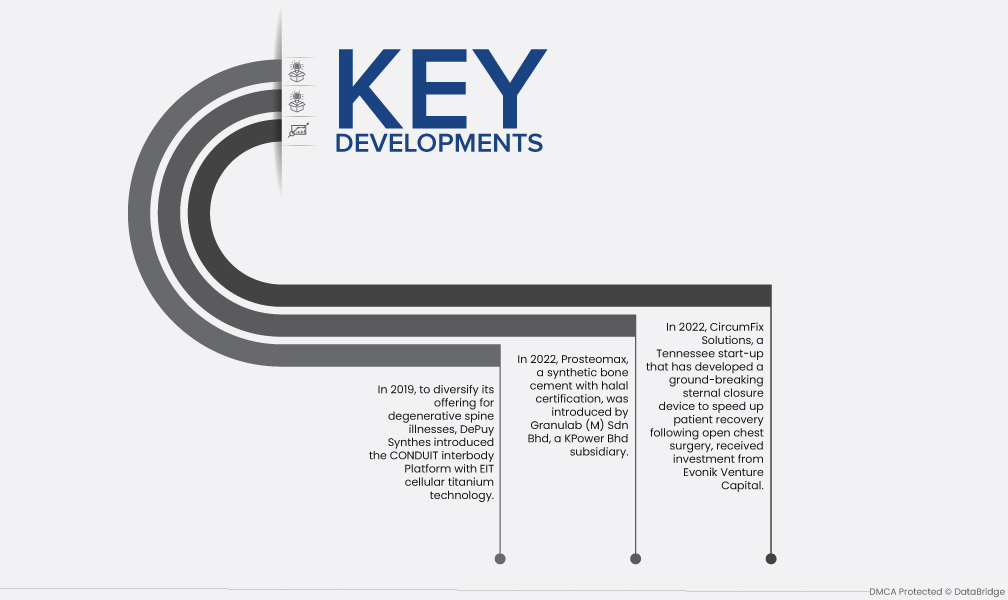

- 2019 年,為了豐富其針對退化性脊椎疾病的產品組合,DePuy Synthes 推出了採用 EIT 細胞鈦技術的 CONDUIT 椎間平台。

- 2022 年,KPower Bhd 的子公司 Granulab (M) Sdn Bhd 推出了經過清真認證的合成骨水泥 Prosteomax。 Prosteomax 已獲得馬來西亞伊斯蘭發展部的清真認證,並獲得馬來西亞醫療器材管理局的許可,可用於骨科、顱骨、牙科和顎面應用。

- 2022 年,田納西州的新創公司 CircumFix Solutions 獲得了贏創創投公司的投資,該公司開發了一種突破性的胸骨閉合裝置,可以加快患者在開胸手術後的康復速度。

區域分析

從地理上看,市場報告涵蓋的國家有:北美洲的美國、加拿大和墨西哥、歐洲的德國、法國、英國、荷蘭、瑞士、比利時、俄羅斯、義大利、西班牙、土耳其、歐洲其他地區、中國、日本、印度、韓國、新加坡、馬來西亞、澳洲、泰國、印尼、菲律賓、亞太地區(APAC)的其他地區、沙烏地阿拉伯、阿聯酋、南非、澳洲、其他國家的歐洲、歐洲、歐洲地區和其他國家的歐洲地區(歐洲地區的歐洲國家。

根據 Data Bridge 市場研究分析:

2022 年至 2029 年預測期內,北美是胸骨閉合系統市場的主導地區

北美心臟病發病率高是導致該大陸大部分地區心臟病發病率高的另一個因素。例如,美國疾病管制與預防中心的一項調查發現,2,810 萬美國人被診斷出患有心臟病,例如心臟瓣膜疾病或心臟驟停。

預計2022 年至 2029 年預測期內,亞太地區將成為胸骨閉合系統市場成長最快的地區

隨著領先企業擴大在該地區的地理影響力並專注於以相當低的成本行銷其產品,預計亞太地區在預測期內將以豐厚的複合年增長率 (CAGR) 成長。

有關胸骨閉合系統市場 報告的更多詳細信息,請單擊此處 - https://www.databridgemarketresearch.com/reports/global-sternal-closure-systems-market