Global Acrylic Adhesives Market

市场规模(十亿美元)

CAGR :

%

USD

42.88 Billion

USD

86.07 Billion

2024

2032

USD

42.88 Billion

USD

86.07 Billion

2024

2032

| 2025 –2032 | |

| USD 42.88 Billion | |

| USD 86.07 Billion | |

| % | |

|

全球丙烯酸酯市场分化,按产品类型(临时、永久)、产品类型(丙烯酸聚氨酯乳化、丙烯酸酯、甲基丙烯酸酯、紫外线可腐蚀丙烯酸酯)、应用(纸张和包装、建筑、运输、医疗、消费者、电子等)、形式(立基、粘贴、磁带)、技术(水基、溶剂基、活性等) -- -- 工业趋势和预测至2032年

Acrylic Adhesives Market Size

-

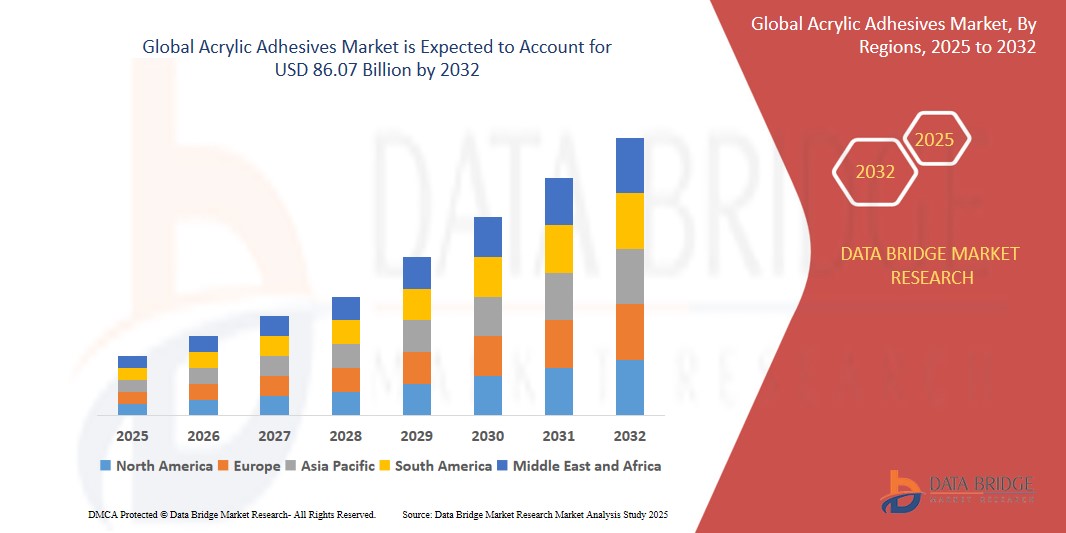

The global Acrylic Adhesives market was valued atUSD 42.88 billion in 2024 and is expected to reachUSD 86.07 billion by 2032

- During the forecast period of 2025 to 2032 the market is likely to grow at aCAGR of 9.10%, primarily driven by the high consumption of acrylic adhesives

- This growth is driven by factors such as the increase in the economic growth, expansion in the manufacturing industries and the accessibility of cheap labour

Acrylic Adhesives Market Analysis

- Acrylic adhesives are critical materials used across various industries, providing strong bonding, flexibility, and resistance to environmental factors. They are essential in Product Types such as construction, automotive, electronics, and medical devices.

- The demand for these adhesives is significantly driven by the increasing need for lightweight, durable materials and advancements in assembly technologies. Over half of the global demand is fueled by the automotive and construction sectors, with the highest consumption seen in regions experiencing rapid industrialization and infrastructure growth.

- The North America region stands out as one of the dominant regions for acrylic adhesives, driven by its robust manufacturing base, technological advancements, and the presence of key end-user industries.

- For instance, the automotive sector in the U.S. has increasingly adopted acrylic adhesives for lightweight vehicle assembly to meet stringent emission standards. From major OEMs to niche manufacturers, North America not only consumes but also drives innovations in adhesive technologies.

- Globally, acrylic adhesives rank as the second-most widely used adhesive type after epoxy adhesives and play a pivotal role in enabling high-performance bonding solutions across a range of industries.

Report Scope and Acrylic Adhesives Market Segmentation

|

Attributes |

Acrylic Adhesives Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Acrylic Adhesives Market Trends

“Shift Toward Sustainable and High-Performance Adhesive Solutions”

- One prominent trend in the global acrylic adhesives market is the shift toward sustainable and high-performance adhesive solutions.

- • This trend is fueled by growing environmental concerns, stricter regulatory standards, and increasing demand for eco-friendly products across industries like automotive, construction, and packaging.

- For instance, manufacturers are developing low-VOC (volatile organic compounds) and solvent-free acrylic adhesives that offer strong bonding performance while minimizing environmental impact. These sustainable formulations are particularly important for sectors aiming to meet green building certifications and corporate sustainability goals.

- High-performance acrylic adhesives are also being engineered for greater heat resistance, chemical durability, and flexibility, expanding their applications in extreme environments and high-tech industries.

- This trend is reshaping the competitive landscape, encouraging innovation and pushing companies to invest in greener, smarter adhesive technologies to meet evolving market expectations

Acrylic Adhesives Market Dynamics

Driver

“Growing Demand Across Key End-Use Industries”

- The rising demand for lightweight, durable, and high-performance bonding solutions across industries such as automotive, construction, electronics, and medical devices is significantly contributing to the growth of the acrylic adhesives market.

- In the automotive sector, the shift towards lightweight vehicles to improve fuel efficiency and meet emission standards has led to increased adoption of acrylic adhesives in place of traditional mechanical fasteners.

- Similarly, the construction industry's focus on energy-efficient buildings and sustainable construction practices has driven demand for low-VOC, high-strength adhesives.

- Ongoing technological advancements in adhesive formulations, including the development of UV-curable and high-temperature-resistant acrylic adhesives, further fuel their widespread application across diverse industries.

- As industries continue to innovate and prioritize performance and sustainability, the demand for acrylic adhesives grows, positioning them as a critical component in modern manufacturing processes.

For instance,

- In September 2024, according to an article published by Adhesives & Sealants Industry (ASI) magazine, the global automotive industry's growing use of multi-material structures has significantly increased the demand for acrylic adhesives, owing to their ability to bond dissimilar materials like metals and composites.

- In June 2023, the Construction Marketing Association (CMA) highlighted that green building trends and regulations are pushing construction companies to adopt adhesives that offer durability and lower environmental impact, with acrylic adhesives leading the way.

- As a result of expanding applications across industries and the push for sustainability, the demand for acrylic adhesives is expected to maintain strong growth momentum globally.

Opportunity

“Innovation in Sustainable and Bio-Based Acrylic Adhesives”

- The growing emphasis on sustainability presents a major opportunity for the development of bio-based and environmentally friendly acrylic adhesives.

- Manufacturers are increasingly investing in research and development to create adhesives derived from renewable raw materials without compromising on performance characteristics such as strength, flexibility, and durability.

- Bio-based acrylic adhesives are especially appealing to industries such as packaging, construction, and automotive, which are under pressure to meet stricter environmental regulations and corporate sustainability targets.

For instance,

- In March 2025, according to a report by Grand View Research, companies like Arkema and Henkel have expanded their product lines to include bio-based acrylic adhesives to cater to eco-conscious markets, anticipating a surge in demand for green alternatives.

- In January 2024, the European Adhesive Association (FEICA) highlighted that sustainable adhesives are one of the fastest-growing segments in the adhesives industry, driven by consumer demand for environmentally responsible products.

- The development and commercialization of sustainable acrylic adhesives not only address environmental concerns but also open new market opportunities, offering companies a competitive advantage in a rapidly evolving regulatory landscape.

Restraint/Challenge

“Fluctuating Raw Material Prices Impacting Profitability”

- The prices of key raw materials used in the production of acrylic adhesives, such as acrylic acid, methyl methacrylate (MMA), and other petroleum-based derivatives, are highly volatile and can significantly impact manufacturing costs.

- Price fluctuations are often driven by factors such as crude oil price movements, supply chain disruptions, geopolitical tensions, and changing trade policies.

- Such variability in input costs can compress profit margins for adhesive manufacturers and lead to higher product prices, making it challenging to maintain competitive pricing in sensitive end-use markets.

For instance,

- In October 2024, according to the Chemical Market Analytics report, the global price of acrylic acid surged by over 20% year-on-year due to raw material shortages and increased energy costs, putting pressure on adhesive manufacturers to raise prices or absorb losses.

- Consequently, fluctuating raw material costs create uncertainties in the supply chain and profitability outlook, posing a major challenge for market players in the acrylic adhesives industry.

Acrylic Adhesives Market Scope

The market is segmented on the basis Product Type, product type, Application, Forms, Technology, and distribution channel.

|

Segmentation |

Sub-Segmentation |

|

By Product Type |

|

|

By Type |

|

|

By Application

|

|

|

By Forms |

|

|

By Technology

|

|

|

|

|

Acrylic Adhesives Market Regional Analysis

“North America is the Dominant Region in the Acrylic Adhesives Market”

- North America dominates the acrylic adhesives market, driven by a strong manufacturing base, technological advancements, and the presence of key players across industries such as automotive, construction, and electronics.

- The U.S. holds a significant share due to increased demand for lightweight and durable bonding solutions in the automotive and aerospace sectors, as well as the rising emphasis on sustainable construction practices.

- The region benefits from robust R&D activities, high adoption of advanced adhesive technologies, and stringent regulatory standards promoting the use of environmentally friendly products.

- In addition, the presence of major automotive OEMs, increasing demand for electric vehicles (EVs), and rapid technological integration in the construction sector are fueling market expansion across North America.

“Asia-Pacific is Projected to Register the Highest Growth Rate”

- The Asia-Pacific region is expected to witness the highest growth rate in the acrylic adhesives market, fueled by rapid industrialization, urbanization, and growing investments in infrastructure development.

- Countries such as China, India, Japan, and South Korea are emerging as key markets due to the booming automotive, construction, and electronics industries, as well as increasing demand for lightweight, efficient bonding solutions.

- China, with its large-scale automotive manufacturing sector and rapid growth in renewable energy and consumer electronics, remains a crucial driver for the regional market.

- India is witnessing significant expansion in the construction and packaging sectors, creating new opportunities for acrylic adhesive applications. Additionally, Japan and South Korea, with their focus on technological innovation and high-performance materials, continue to lead in adopting advanced adhesive technologies.

- The expanding presence of global manufacturers, favorable government initiatives, and rising consumer demand for durable and sustainable products are further accelerating market growth in the region.

Acrylic Adhesives Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, Product Type dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

• Henkel Adhesives Technologies India Private Limited (India)

• H.B. Fuller Company (U.S.)

• Arkema (France)

• Illinois Tool Works Inc. (U.S.)

• Sika AG (Switzerland)

• 3M (U.S.)

• Huntsman International LLC. (U.S.)

• Avery Dennison Corporation (U.S.)

• Pidilite Industries Ltd. (India)

• TOAGOSEI CO., LTD. (Japan)

• Permabond LLC. (U.K.)

• Dymax Corporation (U.S.)

• Franklin International (U.S.)

• Parker Hannifin Corp (U.S.)

• RPM International Inc. (U.S.)

• TONSAN Adhesive, Inc. (China)

• Bostik SA (France)

• MAPEI S.p.A. (Italy)

Latest Developments in Global Acrylic Adhesives Market

- In February 2025, Henkel announced the launch of its new Loctite AA 5831, a one-component, UV-curable acrylic adhesive designed for the electronics market. This adhesive offers excellent adhesion to a wide range of substrates, enhanced environmental resistance, and is specially formulated to meet the miniaturization needs of modern electronic devices.

- In December 2024, H.B. Fuller Company introduced a new line of high-performance, low-odor acrylic adhesives for construction and automotive applications under its TEC and Advantra brands. These adhesives are engineered to offer superior bonding strength, fast curing times, and improved environmental profiles, aligning with growing sustainability demands.

- In November 2024, Arkema announced the expansion of its acrylic adhesive manufacturing capacity at its Sartomer facility in China. This strategic investment is aimed at supporting the fast-growing demand in the Asia-Pacific region, especially in electronics, medical, and flexible packaging industries.

- In October 2024, Sika AG launched its new Sikaflex-545 acrylic adhesive for construction and industrial bonding applications. The product offers high initial tack, excellent adhesion to a variety of substrates without the need for primers, and improved weather resistance, supporting green building trends globally.

- In September 2024, 3M unveiled a new line of acrylic structural adhesives under its Scotch-Weld portfolio, offering improved impact resistance, high bond strength, and environmental durability, catering primarily to the automotive and aerospace industries' demand for lightweight material bonding.

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。