Global Chronic Inflammatory Demyelinating Polyneuropathy Cidp Market

市场规模(十亿美元)

CAGR :

%

USD

1.87 Billion

USD

3.33 Billion

2024

2032

USD

1.87 Billion

USD

3.33 Billion

2024

2032

| 2025 –2032 | |

| USD 1.87 Billion | |

| USD 3.33 Billion | |

| % | |

|

全球慢性發炎性脫髓鞘性多發性神經病變 (CIDP) 市場細分,按治療(靜脈注射免疫球蛋白、皮質類固醇、血漿置換、物理治療等)、診斷(電診斷測試、神經傳導、肌電圖、脊髓液分析等)、給藥途徑(靜脈注射、口服等)、最終用戶(醫院、家庭護理、專科診所等行業 20 20 2036666666666666666666666666666666666666藥房)。年)

慢性發炎性脫髓鞘多發性神經病變(CIDP)市場規模

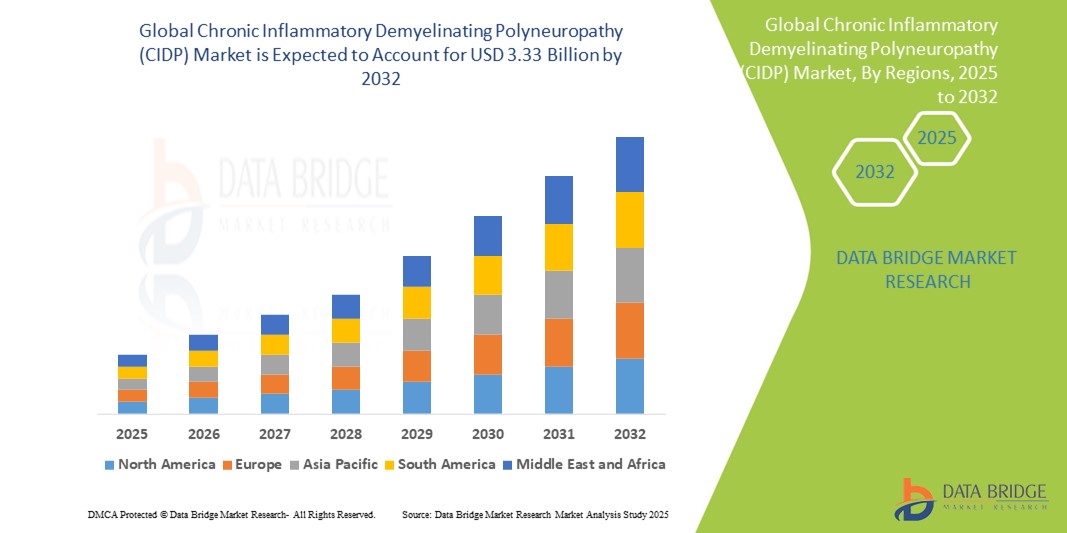

- 2024 年全球慢性發炎性脫髓鞘多發性神經病變 (CIDP) 市場規模為18.7 億美元 ,預計 到 2032 年將達到 33.3 億美元,預測期內 複合年增長率為 7.50%

- 市場成長主要源自於CIDP認知度和診斷水準的提高,以及治療方案和治療介入措施的進步。自體免疫疾病的盛行率不斷上升以及老年人口的不斷增長進一步促進了市場擴張。

- 此外,研發投入的不斷增加,以及全球醫療基礎設施的改善,正在促進患者更好地獲得有效的治療。這些因素共同加速了CIDP新型療法和管理解決方案的採用,從而大幅推動預測期內的市場成長。

慢性發炎性脫髓鞘多發性神經病變(CIDP)市場分析

- 慢性發炎性脫髓鞘多發性神經病變 (CIDP) 是一種罕見的自體免疫神經系統疾病,其特徵是由周邊神經損傷引起的進行性無力和感覺功能障礙。隨著診斷工具的改進以及醫護人員和病患意識的提高,CIDP 的認知度也不斷提高。

- 對有效CIDP治療的需求不斷增長,主要原因是自體免疫疾病和神經系統疾病的盛行率上升、全球人口老化以及先進醫療服務的普及。免疫療法和支持療法的創新正在進一步推動市場成長。

- 北美在慢性發炎性脫髓鞘性多發性神經病變 (CIDP) 市場中佔據主導地位,2024 年其收入份額最大,為 38.9%,其特點是醫療保健基礎設施完善、疾病意識增強、新療法可用,以及領先製藥公司的強大影響力

- 由於醫療保健基礎設施的改善、患者人數的增加以及中國、日本和印度等國家越來越多地採用先進的治療方式,預計亞太地區將成為預測期內慢性發炎性脫髓鞘性多發性神經病變 (CIDP) 市場成長最快的地區

- 靜脈注射免疫球蛋白在慢性發炎性脫髓鞘性多發性神經病變 (CIDP) 市場中佔據主導地位,2024 年的市場份額為 55.5%,這得益於其作為標準一線療法的療效,可緩解症狀並改善患者預後

報告範圍和慢性發炎性脫髓鞘性多發性神經病變(CIDP)市場細分

|

屬性 |

慢性發炎性脫髓鞘多發性神經病變(CIDP)關鍵市場洞察 |

|

涵蓋的領域 |

|

|

覆蓋國家 |

北美洲

歐洲

亞太

中東和非洲

南美洲

|

|

主要市場參與者 |

|

|

市場機會 |

|

|

加值資料資訊集 |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Chronic Inflammatory Demyelinating Polyneuropathy (CIDP) Market Trends

“Enhanced Convenience Through AI and Voice Integration”

- A significant and emerging trend in the CIDP market is the integration of artificial intelligence (AI) and voice-controlled technologies to enhance patient care and convenience, particularly for individuals with mobility challenges

- For instance, patients with CIDP are increasingly utilizing voice-activated systems to control adjustable beds and other assistive devices. These systems can be integrated with popular voice assistants such as Amazon Alexa and Google Assistant, allowing patients to adjust their environment through simple voice commands, thereby reducing physical strain and improving quality of life

- AI integration in CIDP management is also being explored to predict treatment outcomes. Early changes in nerve conduction study (NCS) variables, analyzed through AI algorithms, can serve as reliable predictors of treatment efficacy, enabling personalized treatment plans and better patient outcomes

- The adoption of AI and voice-controlled technologies in CIDP care reflects a broader trend towards personalized and patient-centric healthcare solutions. These technologies not only enhance patient autonomy but also facilitate remote monitoring and management, which is particularly beneficial for chronic conditions such as CIDP

- As the demand for more convenient and accessible treatment options grows, the integration of AI and voice control in CIDP management is expected to become increasingly prevalent, offering new avenues for improving patient care and quality of life

Chronic Inflammatory Demyelinating Polyneuropathy (CIDP) Market Dynamics

Driver

“Growing Demand Due to Rising Prevalence and Advancements in Diagnostic and Therapeutic Solutions”

- The increasing prevalence of CIDP, a chronic autoimmune neurological disorder, is a significant driver for the heightened demand for effective treatment and diagnostic modalities in both clinical and homecare settings

- For instance, in June 2024, argenx received FDA approval for Vyvgart Hytrulo as a treatment for CIDP, marking a major advancement in therapy options and underscoring the market's progression toward targeted immunotherapies. This regulatory milestone is expected to significantly accelerate treatment uptake and broaden therapeutic choices for patients worldwide

- As awareness of CIDP continues to rise among healthcare professionals and patients, earlier and more accurate diagnoses are being made using advanced tools such as EMG, nerve conduction studies, and cerebrospinal fluid analysis—resulting in more timely and effective intervention strategies

- Furthermore, the growing development and use of home-based immunoglobulin therapies and corticosteroids are making CIDP treatment more accessible and patient-friendly, reinforcing the trend toward personalized and flexible care models

- The convenience of self-administered treatments, coupled with technological improvements in monitoring disease progression through connected health platforms, is propelling the adoption of CIDP management strategies across both hospital and homecare sectors. The broader availability of these options and increased R&D investments are contributing to the continued expansion of the global CIDP market.

Restraint/Challenge

“Limited Awareness, High Treatment Costs, and Diagnostic Delays”

- Despite advances in treatment, limited awareness of Chronic Inflammatory Demyelinating Polyneuropathy (CIDP) among patients and general practitioners continues to hinder early diagnosis and timely intervention. The rarity and complex nature of the disease often lead to misdiagnosis or underdiagnosis, which delays the start of appropriate treatment and exacerbates disease progression

- For instance, various clinical studies have noted that many CIDP patients go undiagnosed for months or even years due to the overlapping symptoms with other neurological disorders such as multiple sclerosis or diabetic neuropathy. This delay in recognition and proper referral remains a significant challenge in disease management

- Addressing these diagnostic delays requires enhanced physician education, access to specialized neurologists, and wider availability of advanced diagnostic tools such as nerve conduction studies and spinal fluid analysis. In addition, the high cost of CIDP treatments, particularly intravenous immunoglobulin (IVIg) and corticosteroids, poses a financial burden on both healthcare systems and patients, especially in low- and middle-income countries

- While biosimilar IVIg formulations and insurance coverage are helping to reduce costs in some regions, the affordability and long-term accessibility of CIDP therapies remain a concern, particularly for chronic cases requiring sustained treatment over time

Chronic Inflammatory Demyelinating Polyneuropathy (CIDP) Market Scope

The market is segmented on the basis of treatment, diagnosis, route of administration, end-users, and distribution channel.

- By Treatment

On the basis of treatment, the chronic inflammatory demyelinating polyneuropathy (CIDP) market is segmented into intravenous immunoglobulin (IVIG), corticosteroids, plasmapheresis, physiotherapy, and others. The intravenous immunoglobulin (IVIG) segment dominates the market with the largest revenue share of 55.5% in 2024, attributed to its high efficacy, quick response rates, and wide clinical preference as a first-line therapy. Its non-invasive administration and fewer long-term side effects compared to steroids enhance its adoption in both acute and maintenance therapies.

The physiotherapy segment is expected to witness the fastest CAGR from 2025 to 2032, driven by growing awareness of supportive therapies to improve patient mobility and quality of life. As a non-pharmacological intervention, physiotherapy complements medical treatment and helps in managing chronic symptoms, especially among aging populations and long-term patients.

- By Diagnosis

On the basis of diagnosis, the chronic inflammatory demyelinating polyneuropathy (CIDP) market is segmented into electrodiagnostic testing, nerve conduction studies, electromyography (EMG), spinal fluid analysis, and others. Electrodiagnostic testing dominated the diagnostic segment in 2024 due to its critical role in confirming CIDP by assessing nerve functionality and damage. It is often the gold standard for differentiating CIDP from other neuropathies and has strong clinical validation, making it a routine diagnostic tool.

The spinal fluid analysis segment is projected to show notable growth through 2032, as advances in lumbar puncture techniques and biomarker analysis improve diagnostic precision. This segment is also gaining attention in research for early detection and disease monitoring.

- By Route Of Administration

On the basis of route of administration, the chronic inflammatory demyelinating polyneuropathy (CIDP) market is segmented into intravenous, oral, and others. The Intravenous segment holds the largest market share in 2024, owing to the widespread use of IVIG and plasmapheresis, which are administered through IV routes. The reliability, controlled dosing, and hospital-based administration contribute to its dominance in both acute and chronic treatment settings.

The Oral segment is expected to witness the fastest CAGR from 2025 to 2032 due to the increasing prescription of oral corticosteroids and the development of oral immunomodulatory drugs, offering convenience and compliance benefits in long-term maintenance therapy.

- By End Users

On the basis of end-users, the chronic inflammatory demyelinating polyneuropathy (CIDP) market is segmented into hospitals, homecare, specialty clinics, and others. Hospitals account for the largest revenue share in 2024 due to the availability of advanced diagnostic and treatment infrastructure, including IVIG infusion facilities and neurological expertise. The demand for hospital-based treatments is driven by the complexity and monitoring required for CIDP therapy initiation.

Homecare is anticipated to grow at the fastest CAGR from 2025 to 2032, supported by the increasing trend of home-based IVIG administration, rising healthcare cost-efficiency needs, and patient preference for at-home management of chronic conditions.

- By Distribution Channel

On the basis of distribution channel, the chronic inflammatory demyelinating polyneuropathy (CIDP) market is segmented into hospital pharmacy, retail pharmacy, online pharmacies, and others. The Hospital Pharmacy segment dominated the market in 2024, benefiting from the direct supply of high-cost treatments such as IVIG and corticosteroids during inpatient and outpatient visits.

The Online Pharmacies segment is projected to witness the fastest growth through 2032, fueled by increasing digitalization, patient convenience, and the expansion of specialty drug delivery services. The growing adoption of telehealth platforms also supports the demand for online procurement of CIDP medications.

Chronic Inflammatory Demyelinating Polyneuropathy (CIDP) Market Regional Analysis

- North America dominates the chronic inflammatory demyelinating polyneuropathy (CIDP) market with the largest revenue share of 38.9% in 2024, driven by well-established healthcare infrastructure, increased disease awareness, availability of novel therapies, and a robust presence of leading pharmaceutical companies

- Patients in the region benefit from wide access to specialized neurology clinics, reimbursement support for expensive treatments such as IVIG and plasmapheresis, and increasing awareness initiatives around rare neurological disorders such as CIDP

- This strong market performance is further bolstered by ongoing research efforts, favorable regulatory environments, and the growing adoption of home-based therapies, making North America a hub for innovation and access in the CIDP treatment landscape

U.S. Chronic Inflammatory Demyelinating Polyneuropathy (CIDP) Market Insight

2024年,美國慢性發炎性脫髓鞘多發性神經病變 (CIPD) 市場佔據北美地區最大收入份額,這得益於早期診斷能力、廣泛的宣傳活動以及靜脈注射免疫球蛋白 (IVIG) 和皮質類固醇等先進免疫療法的普及。美國擁有強大的醫療基礎設施、對罕見疾病的良好保險覆蓋,以及主要市場參與者在研究和臨床試驗方面的積極參與。此外,向家庭免疫球蛋白輸注的轉變以及神經科醫生在早期診斷中的參與度不斷提高,正在推動住院和門診治療的持續成長。

歐洲慢性發炎性脫髓鞘多發性神經病變 (CIDP) 市場洞察

預計歐洲慢性發炎性脫髓鞘性多發性神經病變 (CIPD) 市場將在整個預測期內以顯著的複合年增長率擴張,主要得益於強大的神經病學專業知識、政府支持的醫療報銷模式以及自體免疫神經病患病率的上升。一些歐盟國家製定了 CIPD 治療指南,並強調準確的電生理和脊髓液評估,從而提高了診斷率。此外,由於便利性、住院時間的減少以及患者生活品質的提高,對門診和居家護理療法的需求也在不斷增長。

英國慢性發炎性脫髓鞘多發性神經病變 (CIDP) 市場洞察

英國慢性發炎性脫髓鞘性多發性神經病變 (CIPD) 市場預計將以顯著的複合年增長率成長,這得益於人們對慢性週邊神經病變認識的提高,以及透過英國國家醫療服務體系 (NHS) 和私人神經病學中心獲得專科治療的便利性。靜脈注射免疫球蛋白 (IVIG) 療法的廣泛應用、類固醇緩釋療法的持續研究以及電生理檢查的普及是關鍵因素。家庭護理靜脈注射免疫球蛋白 (IVIG) 給藥需求的不斷增長以及以患者為中心的管理策略,進一步推動了市場的發展。

德國慢性發炎性脫髓鞘性多發性神經病變 (CIDP) 市場洞察

預計德國慢性發炎性脫髓鞘性多發性神經病變 (CIPD) 市場在預測期內將以可觀的複合年增長率擴張,這得益於高度先進的診斷框架、結構化的護理路徑以及靜脈注射免疫球蛋白 (IVIG)、血漿置換和皮質類固醇的廣泛臨床應用。德國重視透過肌電圖 (EMG) 和神經傳導研究進行精準診斷,以及 CIPD 治療的全面保險覆蓋,這些因素提升了市場滲透率。此外,免疫調節療法的創新以及醫生對罕見神經免疫疾病的教育水平的提高,也為持續增長創造了有利條件。

亞太地區慢性發炎性脫髓鞘性多發性神經病變 (CIDP) 市場洞察

亞太地區慢性發炎性脫髓鞘性多發性神經病變 (CIPD) 市場預計在 2025 年至 2032 年間以最快的複合年增長率增長,這得益於醫療保健覆蓋範圍的擴大、認知度的提高以及中國、日本和印度等國家免疫介導性神經病變發病率的上升。政府致力於改善罕見疾病診斷,免疫球蛋白療法逐漸納入公共衛生覆蓋,以及三級神經病學中心的成長,這些都是加速該領域應用的關鍵因素。此外,該地區也見證了 IVIG 產品在地化生產的轉變,臨床試驗的增多,從而擴大了治療覆蓋範圍,惠及更廣泛的人群。

日本慢性發炎性脫髓鞘多發性神經病變 (CIDP) 市場洞察

日本慢性發炎性脫髓鞘多發性神經病變 (CIPD) 市場發展勢頭強勁,得益於該國對神經病學研究的投入、結構化的醫療保健體係以及患者的高度認知。 CIPD 管理已納入國家神經病學項目,診斷檢測的廣泛普及也為準確及時的治療提供了保障。日本人口老化、神經病變的高發生率以及早期採用家庭靜脈注射免疫球蛋白 (IVIG) 和皮質類固醇療法,這些因素都顯著促進了市場擴張。

印度慢性發炎性脫髓鞘多發性神經病變 (CIDP) 市場洞察

2024年,印度慢性發炎性脫髓鞘多發性神經病變 (CIPD) 市場佔據亞太地區最大收入份額,這得益於患者群體的快速增長、神經內科治療可及性的不斷提升以及強大的本土製藥能力。在教育措施和罕見疾病倡導團體的支持下,印度神經科醫生和患者的認知度正在不斷提高。政府為罕見疾病覆蓋率而採取的舉措以及國內靜脈注射免疫球蛋白 (IVIG) 產量的增長,使得 CIDP 治療更加便捷且經濟實惠,尤其是在城市中心和三級醫院。

慢性發炎性脫髓鞘多發性神經病變(CIDP)市場份額

慢性發炎性脫髓鞘多發性神經病變 (CIDP) 產業主要由知名公司主導,包括:

- Grifols, SA .(西班牙)

- Octapharma AG(瑞士)

- CSL(澳洲)

- Kedrion SpA(義大利)

- Biotest AG(德國)

- 武田藥品工業株式會社(日本)

- 輝瑞公司(美國)

- 百特國際公司(美國)

- Hansa Biopharma AB(瑞典)

- Alexion Pharmaceuticals, Inc.(美國)

- Biogen公司(美國)

- 基因泰克公司(美國)

- Teleflex Incorporated(美國)

- 生物產品實驗室有限公司(英國)

- 日本製藥株式會社(日本)

- Argenx SE(荷蘭)

- Sanquin Plasma Products BV(荷蘭)

- 費森尤斯卡比股份公司(德國)

- Rhein-Minapharm Biogenetics SAE(埃及)

全球慢性發炎性脫髓鞘多發性神經病變 (CIDP) 市場的最新發展

- 2025年3月,對CIDP產品線的全面分析凸顯了新興療法的光明前景。值得關注的進展包括賽諾菲的Riliprubart(一種處於III期臨床試驗的IgG4人源化單株抗體)以及Immunovant Sciences GmbH的Batoclimab(一種處於II期臨床試驗的FcRn拮抗劑)。這些進展表明,業界正轉向新的治療模式,並堅定地致力於滿足CIDP群體中尚未滿足的需求。

- 2025年5月,Nuvig Therapeutics宣布其NVG-2089用於治療CIDP的2期臨床試驗已完成首例患者給藥。 NVG-2089是一種重組人類IgG1-Fc融合蛋白,旨在模擬靜脈注射免疫球蛋白(IVIg)的免疫調節機制,旨在提供一種比現有標準治療更一致、更可擴展且更方便的替代方案。

- 2025年3月,肌肉萎縮症協會臨床與科學會議強調了CIDP對醫療保健系統、護理人員和患者的巨大臨床和經濟負擔。這凸顯了持續改善管理策略和支援網路的需求,從而推動該領域的進一步研究和發展。

- 2024年1月,武田藥品工業株式會社獲得FDA批准,其GAMMAGARD LIQUID可作為靜脈注射免疫球蛋白(IVIG)療法,用於治療CIDP成人患者。此核准支持長期疾病管理,旨在改善神經肌肉功能,鞏固IVIG作為CIDP治療基石的地位。

- 2024年6月,美國食品藥物管理局核准Vyvgart Hytrulo(依夫加替莫德α和透明質酸酶-qvfc)用於治療成人CIDP。這種皮下注射劑為患者提供了一種新的治療選擇,經證實,與安慰劑相比,該藥物可顯著延長臨床惡化時間。

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。