Global Crispr Gene Editing Market

市场规模(十亿美元)

CAGR :

%

USD

1.83 Billion

USD

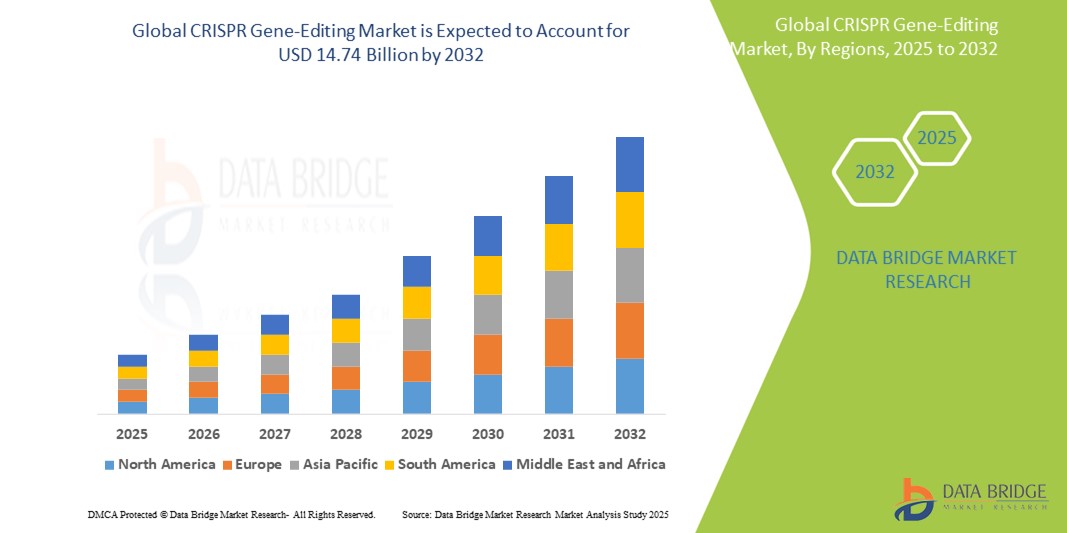

14.74 Billion

2024

2032

USD

1.83 Billion

USD

14.74 Billion

2024

2032

| 2025 –2032 | |

| USD 1.83 Billion | |

| USD 14.74 Billion | |

| % | |

|

全球 C?酶等)、最終用戶(生物技術和製藥公司、學術和政府研究機構、合約研究組織等)- 行業趨勢和預測到 2032 年

CRISPR基因編輯市場規模

- 2024 年全球 CRISPR 基因編輯市場規模為18.3 億美元 ,預計 到 2032 年將達到 147.4 億美元,預測期內 複合年增長率為 29.8%。

- 市場成長主要源於對精準高效的基因編輯解決方案日益增長的需求,這些解決方案可用於治療遺傳疾病、癌症和罕見疾病。這種日益增長的標靶治療需求推動了 CRISPR 基因編輯技術的普及,從而加速了全球 CRISPR 基因編輯市場的擴張。

- 此外,基因編輯研究的持續進展,包括新一代 CRISPR 系統(例如鹼基編輯和主要編輯)的開發,正在提高特異性並減少脫靶效應。這些技術創新正在拓展 CRISPR 的治療潛力和研究應用,顯著促進全球 CRISPR 基因編輯市場的成長。

CRISPR基因編輯市場分析

- CRISPR 基因編輯技術旨在實現 DNA 的精確高效修改,由於其多功能性、特異性和跨多個領域的變革潛力,正日益成為治療開發、農業和生物醫學研究中不可或缺的一部分

- CRISPR 基因編輯市場的成長主要得益於基因組醫學投資的增加、罕見和遺傳性疾病研究的增加,以及旨在開發針對鐮狀細胞病、癌症和遺傳性視網膜疾病等疾病的基因療法的臨床試驗的加速

- 北美在 CRISPR 基因編輯市場佔據主導地位,2024 年的收入份額最高,為 38.5%,這得益於強大的生物技術生態系統、強大的學術研究機構、有利的監管框架以及對基因組編輯創新和商業化的大量資金支持

- 亞太地區預計將成為 CRISPR 基因編輯市場成長最快的地區,預測期內複合年增長率為 7.2%,這得益於不斷擴大的生物技術能力、政府支持的基因組學計劃以及中國、日本和印度等國家之間研發合作的激增

- CRISPR 或 Cas9 技術在 CRISPR 基因編輯市場中佔據主導地位,2024 年將佔 59.4%,這得益於其廣泛採用、易於使用以及持續進步,從而提高了臨床和研究應用的精準度、效率和治療安全性

報告範圍和 CRISPR 基因編輯市場細分

|

屬性 |

CRISPR 基因編輯關鍵市場洞察 |

|

涵蓋的領域 |

|

|

覆蓋國家 |

北美洲

歐洲

亞太

中東和非洲

南美洲

|

|

主要市場參與者 |

|

|

市場機會 |

|

|

加值資料資訊集 |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

CRISPR Gene-Editing Market Trends

“Enhanced Precision Through Technological Advancements and Expanding Applications”

- A significant and accelerating trend in the global CRISPR gene-editing market is the growing focus on precision medicine, driven by increasing demand for targeted therapies to treat genetic disorders, cancer, and rare diseases. This shift is compelling biotechnology companies to refine CRISPR tools for greater accuracy, safety, and therapeutic relevance, thereby reshaping the future of gene therapy and molecular diagnostics

- For instance, the development of next-generation CRISPR systems such as base editing and prime editing is seamlessly integrating into genomic research and therapeutic pipelines. These advanced platforms offer the ability to correct mutations without inducing double-strand breaks, significantly reducing the risk of off-target effects and expanding the scope of diseases that can be treated safely and effectively

- Growing awareness among researchers, clinicians, and regulators about the therapeutic potential of CRISPR is accelerating its adoption across various sectors. This awareness is fostering earlier-stage research investments, more rapid clinical translation, and stronger support for regulatory pathways that enable faster, yet safer, market entry for gene-editing therapies

- The increasing prevalence of monogenic disorders and cancers with well-defined genetic mutations is amplifying market demand, as CRISPR-based approaches offer a precise solution to correct the root genetic cause. This clinical need is especially prominent in pediatric and orphan disease segments, where existing therapies are limited or non-existent

- The seamless integration of CRISPR tools into drug discovery, disease modeling, and regenerative medicine workflows is facilitating a more centralized and efficient research ecosystem. Through this convergence, academic institutions, biotech firms, and pharmaceutical companies are forming robust partnerships that accelerate development timelines and maximize therapeutic impact

- This trend toward more intelligent, precise, and clinically validated gene-editing applications is fundamentally reshaping expectations across healthcare and life sciences. Consequently, companies are actively investing in CRISPR technologies with improved delivery methods, regulatory compliance, and scalability, focusing on long-term therapeutic success and broader patient access. The demand for CRISPR solutions that offer curative potential and personalized interventions is growing rapidly, solidifying its role as a transformative force in modern medicine

CRISPR Gene-Editing Market Dynamics

Driver

“Rising Demand for Precision Medicine and Breakthroughs in Genomic Research”

- The growing application of precision medicine, coupled with breakthroughs in genomic sequencing and editing technologies, is a key driver accelerating the global CRISPR gene-editing market. As more conditions are linked to genetic mutations, the ability to directly modify or correct defective genes is transforming therapeutic strategies across oncology, rare diseases, and inherited disorders

- For instance, recent advancements in prime and base editing are expanding the CRISPR toolbox, enabling safer and more accurate interventions for a broader range of diseases. These innovations are reinforcing pharmaceutical and biotech investment, further stimulating clinical trials and research partnerships focused on curative genetic solutions

- As healthcare systems prioritize targeted and minimally invasive therapies, CRISPR gene-editing offers distinct advantages including one-time treatments with long-term benefits, reducing chronic care burdens. This shift is driving both government funding and regulatory support for gene-editing trials

- In addition, the growing number of patients diagnosed with genetic conditions, especially in pediatrics and oncology, has highlighted the limitations of conventional treatments. CRISPR-based therapies provide a viable alternative by addressing the root cause at the genomic level, offering hope for otherwise untreatable conditions

- The combination of increasing public awareness, scientific validation, and expanding access to genomic screening is fostering widespread enthusiasm for CRISPR-based therapeutics. This momentum is being reflected in rising R&D budgets and cross-sector collaborations aimed at scaling development and deployment globally

Restraint/Challenge

“Ethical Uncertainty, Regulatory Hurdles, and High Development Costs”

- Despite its therapeutic potential, the CRISPR gene-editing market faces significant challenges related to ethical considerations and regulatory scrutiny. The prospect of germline editing, for instance, has raised public and institutional concerns regarding the long-term implications of altering heritable traits, delaying progress in certain applications

- In addition, the high development and commercialization costs of CRISPR therapies—driven by complex validation procedures, delivery system innovation, and extensive safety profiling—pose a major barrier to market scalability. These financial demands can discourage smaller biotech firms and limit accessibility in lower-income regions

- Regulatory pathways for CRISPR therapies remain under development in many jurisdictions, creating uncertainty for developers. The absence of harmonized guidelines for gene-editing approval, especially concerning off-target effects and long-term safety, can prolong trial timelines and increase compliance burdens

- Moreover, public skepticism stemming from ethical debates and media portrayals has the potential to influence adoption rates, particularly in markets where scientific literacy or trust in biotechnology is limited

- Addressing these barriers will require strategic investment in education, ethical governance frameworks, and policy advocacy. In addition, enhancing delivery technologies, promoting affordability through biosimilar innovations, and increasing stakeholder transparency will be essential to drive equitable and sustainable growth in the CRISPR gene-editing market

CRISPR Gene-Editing Market Scope

The CRISPR gene-editing market is segmented into multiple notable segments based on therapeutic application, application type, technology, services, products, and end-users.

• By Therapeutic Application

On the basis of therapeutic application, the CRISPR gene-editing market is segmented into oncology and autoimmune or inflammatory diseases. The oncology segment accounted for a dominant market share of 43.2% in 2024, driven by the rising prevalence of cancer and the increasing adoption of CRISPR-based therapies for targeted gene modifications in tumor suppression and immunotherapy.

The autoimmune or inflammatory segment is expected to witness the fastest CAGR from 2025 to 2032, due to advances in gene-editing therapies targeting complex immune-mediated disorders.

• By Application

On the basis of application, the CRISPR gene-editing market is segmented into genome engineering, disease models, functional genomics, and others. Genome engineering held the largest share of 39.5% in 2024, fueled by its broad utility in therapeutic gene correction and synthetic biology.

Disease models is expected to witness the fastest CAGR from 2025 to 2032 as it is critical in drug discovery and understanding genetic diseases.

- By Technology

On the basis of technology, the market is segmented into CRISPR or Cas9, Zinc finger nucleases, and others. The CRISPR or Cas9 segment dominates the largest market revenue share of 59.4% in 2024. This dominance is driven by its high precision, versatility, and ease of use, making it the most widely adopted gene-editing tool across various research and therapeutic applications. Its revolutionary impact on genetic research and disease treatment fuels its market leadership.

The CRISPR or Cas9 segment is also anticipated to witness the fastest growth rate from 2025 to 2032. This rapid growth is fueled by continuous advancements in CRISPR technology, increasing investments in gene therapy research, and the expanding number of clinical trials leveraging CRISPR for treating genetic disorders and cancers.

- By Services

On the basis of services, the market is segmented into Design Tools, Plasmid and Vector, Cas9 and g-RNA, delivery system products, and others. The Cas9 and g-RNA segment (often considered as the core components for CRISPR-based services) held the largest market revenue share in 2024. This is driven by their fundamental role as the key elements required for precise gene editing experiments and therapeutic applications.

The design tools segment is expected to witness the fastest CAGR from 2025 to 2032. This growth is driven by the increasing need for user-friendly, accurate, and automated software and online platforms that facilitate the design of optimal guide RNAs (gRNAs) and CRISPR experiments, enhancing efficiency for researchers and developers.

- By Products

On the basis of products, the market is segmented into GenCrispr or Cas9 kits, GenCrispr Cas9 Antibodies, GenCrispr Cas9 Enzymes, and Others. The GenCrispr or Cas9 kits segment held the largest market revenue share in 2024, driven by the comprehensive and ready-to-use nature of these kits, which provide all necessary reagents and protocols for conducting CRISPR experiments in a standardized and efficient manner. They are essential for both research and diagnostic applications.

The GenCrispr Cas9 Enzymes segment is expected to witness the fastest CAGR from 2025 to 2032, propelled by the increasing demand for high-quality, purified Cas9 and other Cas enzymes that serve as the molecular scissors for precise DNA editing, crucial for advanced gene-editing applications and therapeutic development.

- By End-Users

On the basis of end-users, the market is segmented into biotechnology and pharmaceutical companies, academic and government research institutes, and contract research organizations, and others. The biotechnology and pharmaceutical companies segment accounted for the largest market revenue share, estimated at around 40-45% in 2024. This dominance is attributed to their significant investments in drug discovery, gene therapy development, and the commercialization of gene-edited products.

The academic and government research institutes segment is expected to witness the fastest CAGR from 2025 to 2032. This growth is fueled by increasing government funding for basic and translational research in gene editing, the proliferation of genome research projects, and the vital role these institutes play in exploring novel applications and advancing the foundational science of gene editing technologies.

CRISPR Gene-Editing Market Regional Analysis

- 北美在 CRISPR 基因編輯市場佔據主導地位,2024 年的營收份額高達 38.5%。這一領先地位歸功於該地區先進的醫療基礎設施、遺傳疾病和慢性病的高發病率以及對生物技術和製藥研究的大量投資

- 眾多關鍵產業參與者的存在,以及促進創新基因編輯療法的批准和商業化的強有力的監管框架,進一步加強了北美的市場地位

- 可支配收入較高、患者對個人化醫療的認識不斷提高以及尖端 CRISPR 技術在學術、研究和臨床環境中的日益普及,也促進了該地區市場的強勁增長和廣泛應用

美國 CRISPR 基因編輯市場洞察

2024年,美國CRISPR基因編輯市場佔據北美80.4%的主導營收份額。這得益於慢性搔癢症和遺傳性疾病的高發病率、強大的醫療基礎設施以及先進療法的持續創新。患者和醫療保健提供者優先考慮有效且持久的解決方案,例如標靶生物製劑和基因編輯療法。良好的報銷環境、大量的研發投入以及積極的患者權益倡導進一步加速了市場成長。

歐洲 CRISPR 基因編輯市場洞察

預計歐洲 CRISPR 基因編輯市場在預測期內將以 5.5% 的強勁複合年增長率成長。成長主要源於慢性皮膚病病例的增加、人口老化以及對改善患者生活品質的日益重視。診斷技術的提升和專科護理的普及促進了先進基因編輯療法的普及。歐洲持續將創新 CRISPR 療法融入主流醫療保健,從而支持市場穩步擴張。

英國 CRISPR 基因編輯市場洞察

英國CRISPR基因編輯市場預計將以5.8%的複合年增長率擴張,這得益於慢性搔癢症盛行率的上升以及旨在改善患者預後的NHS措施。患者和醫護人員意識的提高鼓勵了先進治療方案的使用。英國強大的藥物研究部門和便利的醫療基礎設施是推動這一成長的關鍵因素。

德國 CRISPR 基因編輯市場洞察

預計德國 CRISPR 基因編輯市場將以 5.3% 的複合年增長率成長,這得益於人們對皮膚病的認識不斷提高以及對創新療法的需求。德國的醫療保健體系優先考慮高品質的護理和創新,並推動生物製劑和標靶療法的普及。專科診所越來越多地採用基於 CRISPR 的解決方案,以滿足患者對有效安全治療的偏好。

亞太地區 CRISPR 基因編輯市場洞察

亞太地區 CRISPR 基因編輯市場預計將實現最快成長,2025 年至 2032 年的複合年增長率將達到 7.2%。驅動因素包括中國、日本和印度等國疾病盛行率的上升、可支配收入的提高以及醫療基礎設施的不斷擴張。政府措施和公眾健康意識的提升正在加速 CRISPR 基因編輯技術的普及。該地區製藥業的成長也提高了該技術的可負擔性和可近性。

日本 CRISPR 基因編輯市場洞察

受人口老化和高昂醫療支出的推動,日本的 CRISPR 基因編輯市場正蓬勃發展,預計複合年增長率將達到 5.9%。針對異位性皮膚炎等慢性皮膚病的創新療法需求強勁。包括 IL-31 受體拮抗劑在內的先進療法以及強勁的研發活動持續推動著醫院和專科護理領域的成長。

中國CRISPR基因編輯市場洞察

2024年,中國在亞太地區CRISPR基因編輯市場佔有顯著份額,貢獻了約35%的營收。快速的城市化、不斷壯大的中產階級以及日益加重的皮膚病負擔推動著市場擴張。國內生物製藥的進步以及創新療法可及性的不斷提升,支撐了中國在區域市場成長中的突出地位。

CRISPR基因編輯市場份額

CRISPR 基因編輯產業主要由知名公司主導,包括:

- 應用幹細胞(美國)

- LUMITOS AG(美國)

- Synthego(美國)

- 賽默飛世爾科技公司(美國)

- 金斯瑞(中國)

- Addgene(美國)

- 默克集團(德國)

- Intellia Therapeutics, Inc.(美國)

- Cellectis(法國)

- Precision Biosciences(美國)

- Caribou Biosciences, Inc.(美國)

- OriGene Technologies, Inc.(美國)

- 諾華公司(瑞士)

- 新英格蘭生物實驗室(美國)

- ROCKLAND IMMUNOCHEMICALS INC.(美國)

- ToolGen, Inc.(韓國)

- TAKARA BIO INC.(日本)

- 安捷倫科技公司(美國)

- Abcam有限公司(英國)

- CRISPR Therapeutics AG(瑞士)

全球CRISPR基因編輯市場的最新發展

- 2024年1月,CRISPR Therapeutics AG和Vertex Pharmaceuticals宣布美國FDA批准Casgevy(exagamglogene autotemcel),標誌著第一個基於CRISPR的基因編輯療法獲批,用於治療鐮狀細胞疾病和輸血依賴性β-地中海貧血。這一里程碑標誌著基因醫學的變革性突破,為患有嚴重遺傳性血液疾病的患者提供了一次性治癒方法。

- 2024年3月,Intellia Therapeutics及其合作夥伴Regeneron Pharmaceuticals發表了NTLA-2002的1期臨床試驗數據,該療法是一種基於CRISPR/Cas9的體內基因編輯療法,旨在治療遺傳性血管性水腫(HAE)。早期數據顯示,該療法顯著減少了HAE的發作,顯示在傳統醫療資源匱乏的治療領域,該療法有望實現持久的單劑量治療。

- 2024年4月,Editas Medicine宣布其CRISPR編輯細胞療法在體內臨床前試驗中取得了成功,該療法用於治療橫紋肌肉瘤(一種罕見且侵襲性極強的兒童癌症)。該公司的先導候選藥物顯示出標靶腫瘤消退和極低的脫靶效應,推動Editas的腫瘤學研發管線邁向臨床試驗階段。

- 2024年2月,美國基因組工程公司Synthego推出了其自動化細胞工程平台,該平台利用人工智慧和CRISPR技術,簡化並擴展基因編輯工作流程,用於研究和治療開發。這項創新旨在將CRISPR實驗時間縮短高達50%,從而加速藥物發現和商業化。

- 2023年11月,Beam Therapeutics公司獲得美國FDA的BEAM-101(一種用於治療鐮狀細胞疾病的鹼基編輯CRISPR療法)IND(新藥臨床試驗)批准。與傳統的CRISPR方法不同,BEAM-101使用鹼基編輯技術來模擬與降低疾病嚴重程度相關的自然發生的遺傳變異,這體現了一種更精細且可能更安全的基因編輯策略。

- 2023年12月,Caribou Biosciences發表了其領先的CAR-T細胞療法候選藥物CB-010的臨床試驗進展,該藥物採用CRISPR基因組編輯技術進行基因編輯。早期I期結果顯示,該藥物在復發/難治性B細胞非何杰金氏淋巴瘤患者中具有持久的抗腫瘤活性。這標誌著首批進入臨床試驗的同種異體CAR-T療法之一,該療法利用CRISPR技術增強細胞持久性並降低免疫排斥反應。

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。