Global Display Market

市场规模(十亿美元)

CAGR :

%

USD

176.72 Billion

USD

336.91 Billion

2024

2031

USD

176.72 Billion

USD

336.91 Billion

2024

2031

| 2025 –2031 | |

| USD 176.72 Billion | |

| USD 336.91 Billion | |

| % | |

|

Global Display Market Segmentation, By Display Type (Flat Panel Display, Flexible Panel, and Transparent Panel Display), Product (Automotive Display, Smart Wearable, Tablet, Automotive Display, Television, Smartphone, PC Monitor and Laptop, and Signage), Technology (Direct-View LED, Micro-LED, OLED, and LCD), End Use (Automotive, Healthcare, Defence and Aerospace, Education, Sports and Entertainment, Consumer, Retail and Hospitality, Banking, Financial Services and Insurance, Transportation, and Industrial)), Panel Sizes (Micro displays, Large Panels, and Small and Medium-sized Panels ) - Industry Trends and Forecast to 2032

Display Market Size

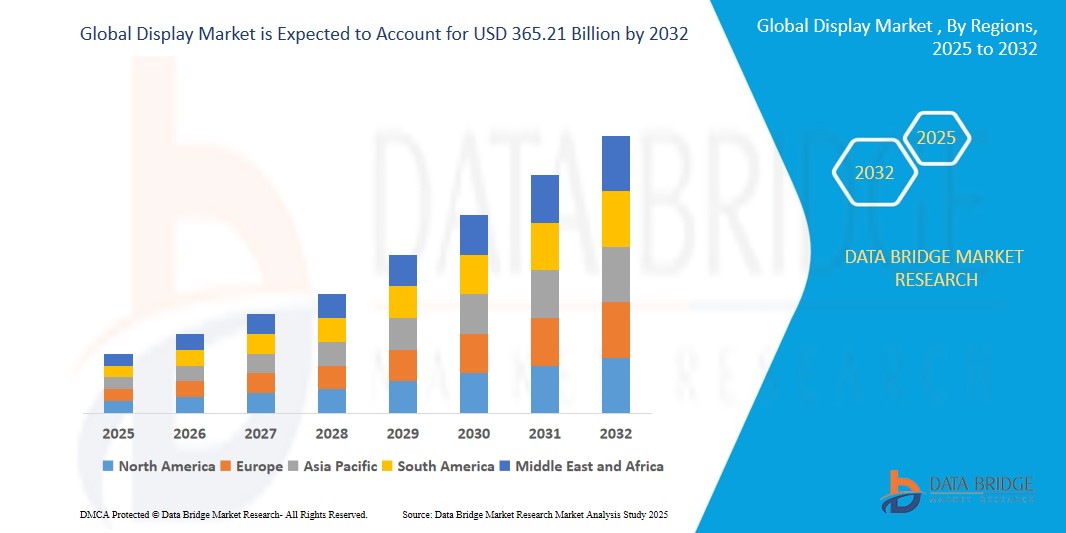

- The global display market was valued atUSD 191.56 billion in 2024 and is expected to reachUSD 365.21 billion by 2032

- During the forecast period of 2025 to 2032 the market is likely to grow at aCAGR of 8.7%, primarily driven by the advancements in OLED and mini-LED technologies

- This growth is driven by factors such as rising demand for advanced display solutions in smartphones, TVs, and automotive displays, growing consumer preference for high-definition and flexible displays, and increased adoption of displays in various industries like healthcare, retail, and automotive

Display Market Analysis

- Displays are essential components used in various consumer electronics and industrial applications, providing high-quality visual output. They are critical for devices like smartphones, televisions, automotive dashboards, digital signage, and medical imaging systems

- The demand for displays is significantly driven by the increasing adoption of smartphones, televisions, and wearable devices, along with advancements in OLED, microLED, and quantum dot technologies. The highest demand is seen in regions with robust consumer electronics markets, such as North America, Europe, and Asia Pacific

- The Asia Pacific region stands out as one of the dominant regions for the global display market, driven by its strong manufacturing capabilities, high demand for smartphones, televisions, and automotive displays, and technological advancements in display panels. Major players in countries like South Korea, Japan, and China contribute to both supply and innovation in the global market

- For instance, South Korea is home to leading display manufacturers like Samsung and LG, which are pioneers in OLED technology. As a result, the region continues to influence the global market, driving trends in high-definition and flexible displays

- Globally, displays rank as one of the most important components in the consumer electronics industry, with smartphone displays leading the demand, followed closely by television screens and automotive displays. The ongoing evolution in display technologies continues to enhance the user experience across a wide range of applications, ensuring their critical role in the future of electronic devices and beyond

Report Scope and Display Market Segmentation

|

Attributes |

Global Display Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Global Display Market Trends

“Increasing Adoption of Flexible and Foldable Displays”

- One prominent trend in the global display market is the growing adoption of flexible and foldable displays

- These advanced display technologies enhance the versatility and portability of electronic devices by allowing screens to bend, fold, and adapt to new form factors, enabling innovations in smartphones, tablets, and wearables

- For instance,foldable smartphones provide users with larger screens in compact, portable designs, while flexible OLED displays offer new possibilities for curved or wraparound screens, which is revolutionizing the user experience in both consumer electronics and automotive displays

- Digital integration of these displays also facilitates enhanced user interaction, providing more immersive experiences for augmented reality (AR) and virtual reality (VR) applications, where flexible screens are crucial for creating more dynamic, adaptable interfaces

- This trend is reshaping the design and functionality of electronic devices, driving the demand for advanced display technologies and creating new opportunities for innovation across multiple industrie

Global Display Market Dynamics

Driver

“Increasing Demand for High-Resolution Displays in Consumer Electronics”

- The growing demand for high-resolution displays in consumer electronics such as smartphones, televisions, gaming devices, and wearables is significantly driving the growth of the global display market

- As consumer expectations for visual quality continue to rise, there is an increasing need for 4K, 8K, and OLED displays that offer superior color accuracy, contrast, and clarity, especially in entertainment and multimedia consumption

- Smartphones are a key driver of this trend, with users seeking higher-quality displays for streaming, gaming, and photography. Similarly, smart TVs and gaming consoles are adopting advanced display technologies to provide immersive viewing experiences

- The growing trend of virtual reality (VR) and augmented reality (AR) applications further accelerates the need for displays with higher pixel density and better responsiveness, driving innovation in microLED and OLED technologies

- As more consumers prioritize high-definition and immersive experiences, the demand for advanced display technologies is expected to continue expanding, creating opportunities for manufacturers to introduce new products and innovate within the market

For instance,

- In 2023, the adoption of OLED technology in smartphones surged, with leading manufacturers like Samsung and Apple incorporating OLED panels in their flagship models to meet the growing demand for sharper, more vibrant screens

- By 2025, it is projected that 4K TVs will become mainstream, pushing the demand for advanced display panels to support the next wave of ultra-high-definition content consumption

Opportunity

“Leveraging Artificial Intelligence for Enhanced Display Experiences”

- AI integration in display technologies can revolutionize user experiences by optimizing display performance, automating settings, and providing personalized content delivery

- AI-powered displays can adapt to environmental conditions, adjusting brightness, contrast, and color balance in real-time for optimal viewing based on the surrounding lighting and the user’s preferences

- Additionally, AI algorithms can enhance image quality by automatically upscaling content, reducing motion blur, and improving visual sharpness, especially in 4K or 8K displays, making them more effective for gaming, media consumption, and professional use

For instance,

- In 2024, AI-powered smart TVs are able to offer automatic scene optimization, where the TV adapts its display settings based on what content is being shown, improving user experience in real-time

- In 2025, AI-driven content recommendation systems in digital signage will allow for dynamic content delivery that adjusts based on audience engagement, time of day, and environmental factors, creating more effective marketing and communication experiences

- The integration of AI in wearable displays (like AR glasses) opens up new opportunities for personalized and adaptive experiences, with the AI optimizing the display based on real-time data, improving user interaction and immersion

Restraint/Challenge

“High Production and Material Costs Hindering Market Growth”

- The high cost of advanced display technologies such as OLED, MicroLED, and quantum dot displays poses a significant challenge to the global display market, particularly impacting price-sensitive consumers and businesses

- These display panels, which offer superior color accuracy, contrast, and resolution, often require expensive materials (like rare metals) and complex manufacturing processes, which contribute to their high cost

- This substantial financial barrier can deter smaller manufacturers and budget-conscious consumers from adopting high-end display technologies, limiting the overall market adoption, especially in developing regions or lower-cost segments

For instance,

- In 2023, according to an article published by Display Supply Chain Consultants, the high production cost of OLED panels remains a key factor in limiting the widespread adoption of OLED TVs, as they remain significantly more expensive than traditional LCD displays, affecting mass-market penetration

- In 2024, the increasing cost of raw materials for MicroLED displays, such as gallium and indium, is impacting the profitability of manufacturers, slowing down the scaling of this technology for broader consumer applications

- As a result, these high production and material costs create barriers for smaller players in the industry, restricting competition and the speed at which advanced display technologies can reach the global market

Global Display Market Scope

The market is segmented on the basis of display type, product type, technology, end use, and panel sizes.

|

Segmentation |

Sub-Segmentation |

|

By Display type |

|

|

By Product Type |

|

|

By Technology |

|

|

By End use |

|

|

By Panel size |

|

Global Display Market Regional Analysis

“North America is the Dominant Region in the Global Display Market”

- North America dominates the global display market, driven by its advanced technological infrastructure, high consumer demand for cutting-edge display technologies, and the presence of leading display manufacturers

- The U.S. holds a significant share due to the increasing demand for high-definition displays in smartphones, televisions, and digital signage, as well as the growing adoption of OLED and MicroLED technologies

- The availability of strong consumer spending power, robust distribution channels, and continuous investments in research & development by key players like Apple, Samsung, and LG further strengthen the market

- In addition, the rising adoption of advanced displays in industries such as automotive,healthcare, and entertainment, alongside a high rate of technological innovation, is driving market expansion across the region

“Asia-Pacific is Projected to Register the Highest Growth Rate”

- The Asia-Pacific region is expected to witness the highest growth rate in the global display market, driven by rapid expansion in consumer electronics, increasing demand for smartphones, televisions, and wearables, and significant technological advancements

- Countries such as China, Japan, South Korea, and India are emerging as key markets due to the growing demand for OLED and 4K/8K display panels, along with the rising popularity of flexible and foldable displays

- South Korea and Japan continue to lead in display panel production, with giants like Samsung, LG, and Sony at the forefront of innovation in OLED and MicroLED technologies. These countries are crucial hubs for high-end display manufacturing and research

- China and India, with their large consumer bases and rising middle-class populations, are seeing increased investments from both local and global companies in display technologies, with a particular focus on making advanced display solutions more accessible at affordable prices

Global Display Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Samsung Display (South Korea)

- LG Display (South Korea)

- BOE Technology Group (China)

- AU Optronics (Taiwan)

- Sharp Corporation (Japan)

- Innolux Corporation (Taiwan)

- Japan Display Inc. (Japan)

- Universal Display Corporation (U.S.)

- Hisense (China)

- TCL Technology (China)

Latest Developments in Global Ophthalmic Operational Microscope Market

- In June 2023, BOE partnered with ThundeRobot, to develop gaming displays for competitive gamers. This collaboration may strengthen the integration of technologies and product designs in the e-sports display domain, aiming to create high-end display solutions. This collaboration enhances technological integration and product design, fostering the creation of advanced display solutions

- In March 2022, Samsung Electronics launched the Smart Monitor series, the M8, featuring an upgraded, stylish design. The M8 delivers Samsung's iconic slim design in four new colors, warm white, sunset pink, daylight blue, and spring green. This move boosts market growth by catering to varied preferences and attracting a broader range of potential buyers

- In December 2022, Samsung Electronics Co., partnered with Google to take smart home interoperability to the next level. This integration fosters demand for displays in smart home devices, driving growth globally as consumers seek seamless connectivity and enhanced user experiences across their connected devices

- In May 2022, LG Electronics unveiled its 2022 OLED TV lineup, featuring a broad range of models, including the LG OLED EVO, the world’s largest OLED TV at 246 cm in width. This launch highlights LG’s continued leadership in advanced display technologies and premium viewing experiences

- In May 2022, Panasonic launched its 2022 TV lineup, featuring both core and premium models with OLED and Core LED options ranging from 42 inches to 77 inches. These models incorporate Ultra HD OLED screens with advanced sensors that optimize picture quality by adjusting ambient color and brightness for an enhanced viewing experience

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。