Global Pigmentation Disorders Treatment Market

市场规模(十亿美元)

CAGR :

%

USD

645.80 Million

USD

1,134.75 Million

2024

2032

USD

645.80 Million

USD

1,134.75 Million

2024

2032

| 2025 –2032 | |

| USD 645.80 Million | |

| USD 1,134.75 Million | |

| % | |

|

全球色素沉著障礙治療市場細分,按疾病類型(黃褐斑、白斑、白癜風、白化病、發炎後色素沉著過度等)、治療類型(藥物治療、非侵入性治療和手術)、藥物(鈣調磷酸酶抑製劑、促黑素細胞激素等)、給藥途徑(口服、外用等)、最終用戶(皮膚科、診所、診所和商店2032 年

色素沉著障礙治療市場規模

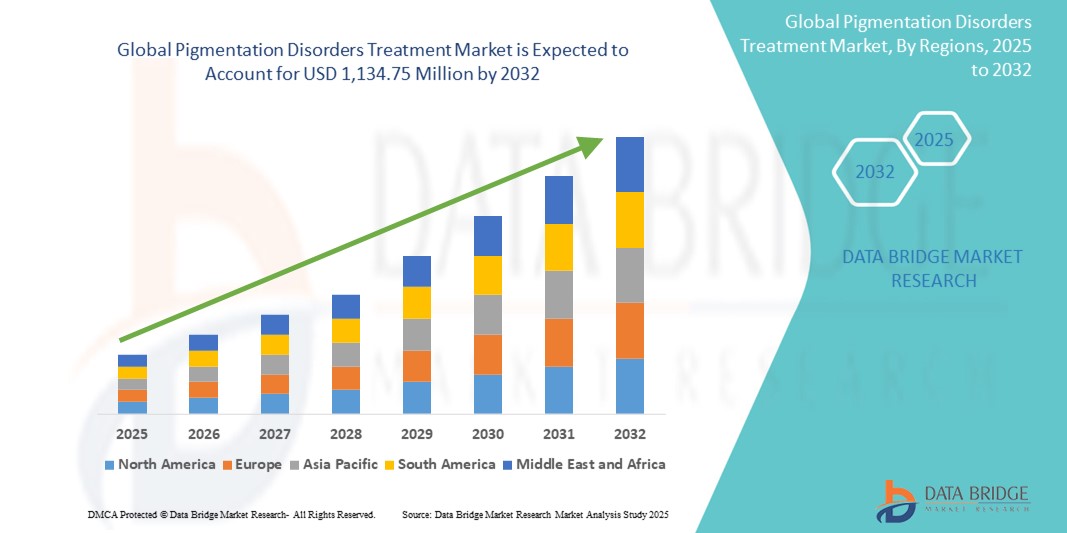

- 2024 年全球色素沉著障礙治療市場規模為6.458 億美元 ,預計 到 2032 年將達到 11.3475 億美元,預測期內 複合年增長率為 7.30%。

- 市場成長主要得益於黃褐斑、白斑症和色素沉澱等皮膚相關疾病的日益流行,以及全球人口對美容皮膚病學和皮膚健康的認識不斷提高

- 此外,雷射療法、外用藥物和微創手術等皮膚病治療技術的進步,也推動了對有效色素沉著障礙解決方案的需求。這些因素共同加速了色素沉著障礙治療的普及,顯著促進了該行業的成長。

色素沉著障礙治療市場分析

- 色素沉著障礙治療,包括外用藥物、雷射治療和化學換膚,由於其在治療黃褐斑、白斑症和發炎後色素沉著等疾病方面有效,在皮膚病護理中變得越來越重要

- 色素沉著障礙解決方案的需求不斷增長,主要是由於全球範圍內人們對皮膚健康的認識不斷提高、美學意識不斷增強以及先進皮膚病治療的普及程度不斷提高

- 北美在色素沉著障礙治療市場佔據主導地位,2024 年其收入份額最高,達 38.6%。該地區醫療保健支出高昂,皮膚科診所數量眾多,且對美容皮膚治療的需求不斷增長。預計該地區在預測期內的複合年增長率將達到 5.2%。

- 亞太地區預計將成為色素沉著障礙治療市場成長最快的地區,預測期內複合年增長率達7.8%。推動這一成長的因素包括:可支配收入的提高、色素沉著障礙的高發病率、消費者對護膚方案的認知度不斷提升,以及印度、韓國和泰國等國醫療旅遊中心的快速擴張。

- 局部用藥在色素沉著障礙治療市場佔據主導地位,2024 年的市場份額為 43.2%,這歸因於其非侵入性、非處方和處方可廣泛獲得,以及消費者對經濟高效且易於使用的解決方案的強烈偏好

報告範圍和色素沉著障礙治療市場細分

|

屬性 |

色素沉著障礙治療關鍵市場洞察 |

|

涵蓋的領域 |

|

|

覆蓋國家 |

北美洲

歐洲

亞太

中東和非洲

南美洲

|

|

主要市場參與者 |

|

|

市場機會 |

|

|

加值資料資訊集 |

除了對市場價值、成長率、細分、地理覆蓋範圍和主要參與者等市場情景的洞察之外,Data Bridge Market Research 策劃的市場報告還包括深入的專家分析、定價分析、品牌份額分析、消費者調查、人口統計分析、供應鏈分析、價值鏈分析、原材料/消耗品概述、供應商選擇標準、PESTLE 分析、波特分析和監管框架。 |

色素沉著障礙治療市場趨勢

“治療方式的進步和以消費者為中心的創新”

- A significant and accelerating trend in the global pigmentation disorders treatment market is the continuous innovation in treatment options, including laser therapies, topical formulations, chemical peels, and light-based devices. These advancements are offering patients faster, more effective, and less invasive solutions for managing skin discoloration conditions

- For instance, picosecond and Q-switched lasers are now widely used in clinical settings to target melanin deposits with greater precision, minimizing damage to surrounding skin tissue. Similarly, combination therapies using retinoids, hydroquinone, corticosteroids, and antioxidants are being developed to improve outcomes for patients with stubborn or recurrent pigmentation issues

- The integration of dermatology with digital platforms has enabled patients to access tele-dermatology consultations, personalized skincare regimens, and post-treatment monitoring through mobile applications. This approach not only improves treatment adherence but also allows dermatologists to deliver more consistent follow-up care

- The development of cosmeceuticals—skincare products that combine cosmetic and pharmaceutical benefits—is creating a growing market segment for consumers seeking over-the-counter pigmentation solutions. These products, often enriched with ingredients such as niacinamide, kojic acid, vitamin C, and tranexamic acid, are widely adopted for daily pigmentation control and maintenance

- The shift toward non-invasive and home-use treatments is fundamentally reshaping consumer expectations in dermatology. Consequently, companies are investing in at-home devices such as LED therapy masks, microdermabrasion tools, and handheld laser gadgets to cater to this emerging demand for accessible and convenient pigmentation care

- The demand for effective, safe, and convenient pigmentation disorder treatments is growing rapidly across both clinical and consumer sectors, as individuals increasingly prioritize skin health, aesthetics, and long-term preventive care

Pigmentation Disorders Treatment Market Dynamics

Driver

“Growing Demand for Aesthetic Appearance and Rising Dermatological Awareness”

- Increasing awareness regarding skin health and the growing desire for even-toned, blemish-free skin are key drivers fueling the demand for pigmentation disorder treatments globally

- For instance, in March 2024, L'Oréal announced the expansion of its dermatological beauty division with targeted pigmentation solutions that combine cosmetic appeal with clinically validated active ingredients. Such initiatives by leading players are expected to boost the Pigmentation Disorders Treatment industry in the coming years

- The growing influence of social media, beauty influencers, and visual content platforms is driving individuals—particularly younger demographics—to seek professional and over-the-counter solutions for melasma, hyperpigmentation, and post-inflammatory dark spots

- Furthermore, rising disposable incomes and increased access to dermatological care in emerging economies are making both clinical treatments and skincare products more accessible to broader populations

- The expansion of medical tourism, especially in Asia-Pacific countries such as India, Thailand, and South Korea, is contributing to increased uptake of pigmentation treatments, including laser therapy, chemical peels, and topical regimens

Restraint/Challenge

“Side Effects and High Treatment Costs”

- Potential side effects such as skin irritation, redness, dryness, and photosensitivity associated with certain topical and laser-based treatments pose challenges for consistent and widespread adoption, especially among individuals with sensitive or darker skin tones

- For instance, hydroquinone—though effective—is under regulatory scrutiny in several countries due to safety concerns with long-term use, prompting regulatory restrictions that limit its availability and use

- In addition, cost remains a major barrier, particularly for advanced treatments such as picosecond lasers or prescription-grade cosmeceuticals. These options may be unaffordable for price-sensitive consumers, especially in low- and middle-income regions

- Insurance limitations on aesthetic or non-life-threatening conditions further exacerbate the affordability issue, as many pigmentation treatments are not covered under standard health plans

- Overcoming these restraints requires greater investment in R&D to develop safer, more effective, and cost-efficient therapies, along with enhanced consumer education on prevention, maintenance, and safe usage of skin lightening products

Pigmentation Disorders Treatment Market Scope

The market is segmented on the basis of disease type, treatment type, drugs, route of administration, end user and distribution channel.

- By Disease Type

On the basis of disease type, the pigmentation disorders treatment market is segmented into melasma, vitiligo, albinism, post-inflammatory hyperpigmentation (PIH), and others.

The Melasma segment dominated the market with the largest revenue share of 34.6% in 2024, owing to its high prevalence among women, especially in regions with greater sun exposure, and the availability of various topical and laser-based treatment options.

The post-inflammatory hyperpigmentation (PIH) segment is expected to witness the fastest CAGR of 8.9% from 2025 to 2032, driven by increasing incidences of acne and cosmetic procedures that trigger PIH, along with a surge in demand for fast-acting topical solutions.

-

- By Treatment Type

On the basis of treatment type, the pigmentation disorders treatment market is segmented into pharmacological treatment, non-invasive treatment, and surgery. The pharmacological treatment segment held the largest market share of 47.8% in 2024, due to the widespread use of topical creams, serums, and oral medications prescribed for long-term management of pigmentation disorders.

The non-invasive treatment segment is projected to record the fastest CAGR of 9.3% during 2025–2032, fueled by growing demand for laser therapy, chemical peels, and other light-based therapies that offer visible improvements with minimal downtime.

-

- By Drugs

On the basis of drugs, the pigmentation disorders treatment market is segmented into calcineurin inhibitors, melanocyte-stimulating hormone, and others. The calcineurin inhibitors segment captured the largest revenue share of 39.5% in 2024, attributed to their effective use in treating vitiligo and inflammatory skin pigmentation conditions without the side effects associated with corticosteroids.

The melanocyte-stimulating hormone segment is anticipated to grow at the fastest CAGR of 10.1% from 2025 to 2032, supported by advancing research in targeted melanogenesis pathways and improved clinical outcomes.

-

- By Route of Administration

On the basis of route of administration, the pigmentation disorders treatment market is categorized into oral, topical, and others. The topical segment held the largest market share of 43.2% in 2024, owing to ease of application, high patient compliance, and widespread availability of OTC and prescription creams.

The oral segment is expected to witness the fastest CAGR of 8.5% during 2025–2032, driven by innovations in oral formulations aimed at enhancing systemic efficacy for widespread pigmentation concerns.

-

- By End-Users

Based on end-users, the pigmentation disorders treatment market is segmented into dermatology clinics, aesthetic clinics, homecare, hospitals, and others. The dermatology clinics segment dominated the market with a market share of 36.7% in 2024, as patients often seek professional diagnosis and targeted treatment plans from dermatologists.

The homecare segment is expected to grow at the fastest CAGR of 9.6% from 2025 to 2032, boosted by the increasing availability of advanced home-use treatment devices and topical kits designed for convenience and privacy.

-

- By Distribution Channel

根據分銷管道,色素沉著障礙治療市場可細分為醫院藥房、零售藥房和線上藥房。零售藥房市場在2024年佔據了最大的收入份額,達到41.9% ,這得益於非處方色素沉著產品的可及性和廣泛的藥房網絡。

預計線上藥局領域在 2025 年至 2032 年間將以 11.3% 的最快複合年增長率增長,這得益於電子商務平台的日益普及、送貨上門以及護膚和皮膚病學領域的數位參與度的不斷提高。

色素沉著障礙治療市場區域分析

- 北美在色素沉著障礙治療市場佔據主導地位,2024 年其收入份額最大,為 38.6%,這得益於黃褐斑和白斑等色素沉著障礙治療的高發性,以及先進的醫療基礎設施和日益增強的審美意識

- 該地區受益於早期採用創新治療方案,包括外用藥妝品、雷射療法和先進生物製劑,並得到強大的研發投資和監管部門批准的支持

- 此外,患者對非侵入性美容手術的偏好日益增加,以及領先的皮膚科和美容診所的存在,對美國和加拿大的市場成長做出了巨大貢獻

美國色素沉著障礙治療市場洞察

2024年,美國色素沉著障礙治療市場佔北美地區最大收入份額,達81.3%,這主要得益於黃褐斑、白斑症和發炎後色素沉澱等皮膚病的高發性。先進的皮膚病學基礎設施、美容皮膚科診所的強大影響力以及處方藥和非處方藥的廣泛使用,這些因素顯著增強了美國市場的主導地位。此外,消費者對非侵入性美容手術的日益青睞以及完善的皮膚病治療報銷體系,也支撐了市場的持續成長。外用藥物、雷射治療和生物製劑的持續創新進一步推動了美國市場的發展。

歐洲色素沉著障礙治療市場洞察

受人口老化加劇和美容皮膚科需求成長的推動,歐洲色素沉著障礙治療市場預計將在2025年至2032年間以7.9%的複合年增長率大幅擴張。越來越多的消費者尋求老年斑、黃褐斑和其他色素沉著障礙的治療,將其作為日常護膚和美容提升的一部分。該地區受益於廣泛的皮膚科醫生資源、強大的醫藥基礎以及包括雷射換膚和外用藥物在內的聯合療法的普及。公眾意識宣傳活動和皮膚科大會也正在促進治療的普及。

英國色素沉著障礙治療市場洞察

由於人們對皮膚健康、紫外線傷害的擔憂日益加劇,以及美容服務日益普及,英國色素沉著障礙治療市場預計在預測期內將以8.3%的複合年增長率增長。非處方產品(例如美白霜和處方藥)的需求持續增長,尤其是在治療黃褐斑和發炎後色素沉著方面。此外,領先護膚品牌的湧現以及醫學美容行業的蓬勃發展,正在推動各年齡層對色素沉著治療的接受度。

德國色素沉著障礙治療市場洞察

預計德國色素沉著障礙治療市場在預測期內將以7.6%的複合年增長率擴張,這得益於該國強大的臨床研究基礎、高水平的醫療保健可及性以及消費者對皮膚病學創新產品日益增長的需求。民眾對美容皮膚科的認知度不斷提高,加上對天然和有機外用產品的偏好,正在推動市場需求的成長。德國也是醫療器材公司的重要樞紐,這些公司提供用於色素矯正的非侵入性雷射和光療法。

亞太色素沉著障礙治療市場洞察

受美妝意識提升、都市化進程加快以及中產階級人口成長的推動,亞太地區色素沉著障礙治療市場可望在2025年至2032年間以7.8%的複合年增長率保持高速成長。中國、日本、韓國和印度等國家由於注重膚色均勻、無瑕疵的文化美學標準,對色素沉著治療的需求正在激增。價格實惠的治療方案、美容皮膚科診所的日益普及以及蓬勃發展的護膚品電商市場,正在加速該地區的市場成長。

日本色素沉著障礙治療市場洞察

The Japan pigmentation disorders treatment market is gaining momentum, with a projected CAGR of 9.8%, due to the country’s focus on aesthetic wellness and a growing elderly population seeking treatments for age spots and sun damage. Japan leads in dermatological R&D, particularly in the development of melanogenesis inhibitors and gentle, skin-friendly formulations. High consumer trust in dermatologists and strong demand for cosmeceuticals and prescription-based therapies are key growth drivers.

China Pigmentation Disorders Treatment Market Insight

The China pigmentation disorders treatment market accounted for the largest revenue share in Asia-Pacific in 2024, with 34.5%, driven by increasing awareness of skin health, rising consumer spending, and a booming aesthetic medicine sector. The popularity of whitening products, demand for hyperpigmentation treatments, and strong influence of beauty trends on social media are propelling the market. In addition, growing medical tourism, robust manufacturing capabilities, and digital healthcare platforms make pigmentation treatment accessible across urban and semi-urban areas.

Pigmentation Disorders Treatment Market Share

The pigmentation disorders treatment industry is primarily led by well-established companies, including:

- Zerigo Health (U.S.)

- Bausch Health Companies Inc. (Canada)

- GLENMARK PHARMACEUTICALS LTD (India)

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Dr. Reddy’s Laboratories Ltd. (India)

- Viatris Inc. (U.S.)

- Bayer AG (Germany)

- CLINUVEL PHARMACEUTICALS LTD (Australia)

- Incyte (U.S.)

- Strides Pharma Science Limited (India)

- Panacea Biotec (India)

- Belcher Pharmaceuticals, LLC (U.S.)

- LEO Pharma A/S (Denmark)

- Astellas Pharma Inc. (Japan)

- Episciences (U.S.)

- Obagi Cosmeceuticals LLC (U.S.)

Latest Developments in Global Pigmentation Disorders Treatment Market

- In April 2024, Incyte Corporation announced new positive Phase III clinical trial results for its ruxolitinib cream, which significantly improved symptoms of non-segmental vitiligo in adolescents and adults. This development strengthens Incyte’s dermatology pipeline and highlights the growing innovation in topical therapies for pigmentation disorders

- In March 2024, Glenmark Pharmaceuticals launched a novel combination topical therapy for melasma under its dermatology portfolio in India. The product offers a steroid-free alternative to existing treatments and caters to the rising demand for safe, long-term pigmentation management options in the Indian market

- In February 2024, Obagi Cosmeceuticals LLC unveiled its new pigment-correcting skincare line featuring arbutin and tranexamic acid for hyperpigmentation, expanding its reach in aesthetic dermatology. The launch aims to meet consumer demand for non-invasive, cosmetic treatments across the U.S. and Europe

- In January 2024, CLINUVEL PHARMACEUTICALS LTD received regulatory clearance in Europe to market SCENESSE (afamelanotide) for the treatment of vitiligo in adult patients with Fitzpatrick skin types IV–VI. The approval marks a significant step forward in expanding treatment options for underrepresented patient populations

- In December 2023, Dr. Reddy’s Laboratories Ltd. announced the launch of its generic version of tacrolimus ointment in North America for the treatment of Pigmentation Disorders Treatment such as vitiligo and post-inflammatory hyperpigmentation. This move enhances access to cost-effective pharmacological treatments in the region

- In November 2023, Bausch Health Companies Inc. completed the acquisition of a novel skin-lightening product portfolio to strengthen its position in the aesthetic and dermatological treatment segment. The acquisition includes formulations that target melasma and sun-induced hyperpigmentation, signaling strategic market expansion

- In October 2023, Pfizer Inc. entered a collaboration with a biotech startup to develop oral melanocortin receptor modulators for pigmentation disorders. The partnership aims to pioneer systemic treatments for widespread or difficult-to-treat Pigmentation Disorders Treatment such as albinism and extensive vitiligo

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。