North America Dental Radiology Equipment Market

市场规模(十亿美元)

CAGR :

%

USD

1.20 Billion

USD

2.54 Billion

2024

2032

USD

1.20 Billion

USD

2.54 Billion

2024

2032

| 2025 –2032 | |

| USD 1.20 Billion | |

| USD 2.54 Billion | |

| % | |

|

North America Dental Radiology Equipment Market Segmentation By Type (Diagnostic Dental Equipment), End-User (Hospitals, Diagnostic Centers, Dental Clinics)- Industry Trends and Forecast to 2032

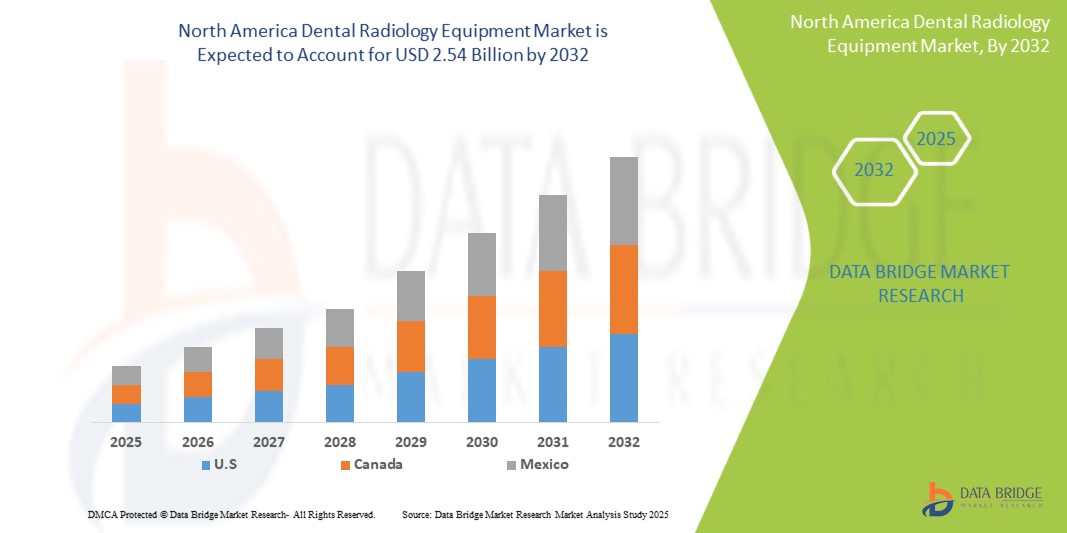

Dental Radiology Equipment Market Size

- The North America Dental Radiology Equipment Market was valued atUSD1.20 Billionin 2024and is expected to reachUSD2.54 Billionby 2032,at aCAGR of 7.1%during the forecast period

- The North America Dental Radiology Equipment Market is primarily driven by several key factors. These include the increasing prevalence of dental disorders, such as dental caries, periodontal disease, and oral cancers, which are fueling demand for advanced diagnostic imaging.

North America Dental Radiology Equipment Market Analysis

- Dental radiology equipment plays a critical role in diagnosing a wide range of oral health conditions, including dental caries, periodontal disease, impacted teeth, jaw disorders, and oral cancers. These imaging systems—including intraoral X-rays, extraoral panoramic and cephalometric systems, and advanced 3D imaging technologies such as cone beam computed tomography (CBCT)—enable accurate visualization of dental structures, aiding in effective treatment planning and improved patient outcomes. These tools are widely adopted across dental clinics, hospitals, diagnostic centers, and academic institutions.

- The demand for dental radiology equipment in North America is primarily driven by a rising incidence of dental diseases, increasing awareness of preventive dental care, and a growing elderly population that requires frequent dental evaluations. Additionally, the growing emphasis on cosmetic dentistry and orthodontics, where precise imaging is crucial, is significantly boosting the uptake of dental imaging solutions.

- North America is a leading region in the global dental radiology equipment market, supported by a well-developed healthcare infrastructure, early adoption of advanced technologies, and favorable reimbursement policies. The United States holds a dominant share, driven by a high number of dental professionals, growing dental insurance coverage, and strong investment in digital health and imaging innovations.

- The North American dental radiology equipment market is also shaped by regulatory approvals, including FDA clearances for novel and safer imaging systems. Furthermore, rising healthcare spending, increasing demand for chairside imaging solutions, and advancements in AI-based diagnostics and image-guided surgeries are enhancing diagnostic capabilities. The market is also witnessing increased adoption of mobile and handheld X-ray devices, particularly in remote or mobile dental care settings. Overall, the focus on personalized and precision dentistry is driving the adoption of innovative radiology equipment across the region

Report ScopeDental Radiology EquipmentMarket Segmentation

|

Attributes |

Dental Radiology EquipmentKeyMarket Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Dental Radiology Equipment Market Trends

“Digital Imaging and 3D Radiology Innovation”

- Advancements in dental imaging—such as cone-beam computed tomography (CBCT), digital panoramic and cephalometric systems—are revolutionizing diagnostics by delivering faster, clearer, and more accurate imaging. These technologies support enhanced visualization of oral structures, enabling better treatment planning in implantology, orthodontics, endodontics, and oral surgery.

- AI-powered dental radiology solutions are improving image analysis, diagnosis accuracy, and clinical decision-making. AI tools are being integrated into radiology software to automate the detection of dental anomalies, caries, bone loss, and more, streamlining the workflow for dental practitioners.

- For instance, the U.S. has seen a surge in the adoption of digital radiography and CBCT systems, fueled by the shift towards paperless workflows, integration with electronic health records (EHRs), and demand for high-resolution imaging in minimally invasive procedures.

- This combination reduced diagnostic time, improved accuracy in implant and orthodontic planning, and streamlined clinical workflows, leading to better patient outcomes and more informed treatment decisions.

Dental Radiology Equipment Market Dynamics

Driver

“High Adoption of Advanced Dental Imaging Technologies”

- The North America Dental Radiology Equipment Market is experiencing significant growth due to the widespread adoption of advanced imaging modalities, particularly digital and 3D imaging systems, for enhanced diagnostic accuracy and treatment planning in dental care.

- Technological innovations such as cone-beam computed tomography (CBCT), digital panoramic and cephalometric imaging, and intraoral sensors are revolutionizing dental diagnostics by offering high-resolution, real-time imaging with reduced radiation exposure.

- Government initiatives in the U.S. and Canada aimed at improving oral health infrastructure and increasing access to advanced dental care are fueling the demand for modern radiology equipment in both public and private dental facilities.

- The integration of imaging technologies into electronic health records (EHR), along with the rising use of AI-based diagnostic tools in dentistry, is improving diagnostic speed, efficiency, and accuracy, thereby driving market growth.

For instance,

- According to the American Dental Association (ADA), CBCT systems have become a preferred modality in implant planning and complex endodontic procedures due to their 3D visualization capabilities.

- In January 2024, Dentsply Sirona announced the launch of a next-generation digital imaging suite in North America, offering faster image processing, enhanced clarity, and seamless integration with CAD/CAM systems

- The ongoing shift toward digital dentistry, supported by investments in clinic modernization and dental IT infrastructure, is further accelerating the adoption of state-of-the-art radiology equipment across North America.

Opportunity

“Integration of Dental Imaging into Digital and Decentralized Care Models”

- The growing transition toward digital and decentralized dental care delivery in North America is opening new opportunities for the adoption of portable, cloud-connected, and AI-integrated dental radiology equipment.

- Demand is rising for advanced imaging solutions that can be seamlessly used in mobile dental units, community health centers, and outpatient settings—enabling broader access to quality dental diagnostics, especially in rural and underserved regions.

- The expansion of teledentistry platforms is also driving the need for digital radiology equipment capable of generating and sharing high-resolution images in real-time, improving remote consultations and treatment planning.

For instance,

- In February 2024, the Canadian Dental Association highlighted the growing use of mobile CBCT and portable intraoral imaging devices to support oral health outreach programs in remote communities.

- Companies such as Planmeca and Carestream Dental have launched compact and wireless imaging systems designed for use in decentralized settings, enhancing diagnostic flexibility and efficiency

- This trend is further bolstered by healthcare providers’ growing focus on same-day diagnostics and treatment workflows, particularly in orthodontics, implantology, and emergency dental care.

- Additionally, the rising availability of cloud-based image storage and analysis tools is fostering the development of integrated radiology platforms, enabling multi-site practices to centralize and streamline imaging data.

Restraint/Challenge

“High Equipment Costs and Regulatory Compliance Barriers”

- One of the major challenges in the North America Dental Radiology Equipment Market is the high cost of advanced imaging systems, such as cone-beam computed tomography (CBCT), panoramic X-ray machines, and digital intraoral scanners. These technologies require significant capital investment, ongoing maintenance, and staff training—posing financial strain on small dental practices and community clinics.

- The stringent regulatory approval processes enforced by agencies like the U.S. Food and Drug Administration (FDA) and Health Canada further add to the complexity and cost of launching new dental radiology devices. These requirements demand extensive clinical validation, safety assessments, and quality certifications.

For instance,

- According to a 2024 analysis by the Dental Trade Alliance (DTA), the average upfront cost of installing a CBCT machine in a private dental clinic can range from USD 100,000 to USD 200,000, making it less accessible for solo practitioners and rural care providers.

- Additionally, compliance with evolving data privacy regulations, such as HIPAA and PHIPA, adds another layer of complexity for digital imaging systems that store or transmit patient data

- These financial and regulatory hurdles can delay product adoption, especially among smaller dental operators, and limit access to modern imaging technologies in less urbanized regions.

- Furthermore, the high pace of technological innovation can lead to faster equipment obsolescence, deterring investment and contributing to disparities in imaging capabilities across the region

Dental Radiology Equipment Market Scope

The market is segmented on the basis, type, end user.

|

Segmentation |

Sub-Segmentation |

|

By Type |

|

|

ByEnd User |

|

In 2025, the Diagnostic is projected to dominate the market with a largest share in type segment.

The digital X-ray systems in the diagnostic segment are expected to dominate the North America Dental Radiology Equipment Market with the largest share of 46.22% in 2025 due to the high growth of high-resolution, real-time imaging, which significantly enhances diagnostic accuracy and workflow efficiency in dental practices. Digital X-ray systems offer numerous advantages over conventional film-based systems, including faster image acquisition, lower radiation exposure, easy image storage and sharing, and integration with electronic health records (EHRs).

The Dental Clinics is expected to account for the largest share during the forecast period in end user market

In 2025, the dental clinics segment is expected to dominate the market with the largest market share of 54.56% due to its high prevalence and demand for precision. This is attributed to the high volume of outpatient dental procedures, ranging from routine check-ups to orthodontic and endodontic treatments that require precise radiographic evaluation. The growing number of independent and group dental practices, along with rising investments in in-office imaging capabilities, is driving the adoption of compact and user-friendly radiology equipment. Dental clinics are increasingly transitioning to digital and 3D imaging solutions to improve diagnostic precision, reduce turnaround time, and enhance patient engagement.

Dental Radiology Equipment Market Regional Analysis

“U.S. is the Dominant Country in the Dental Radiology Equipment Market”

- The United States dominates the North America Dental Radiology Equipment Market, accounting for the largest share due to its advanced healthcare infrastructure, widespread adoption of digital dentistry, and significant investments in dental technology and research.

- The increasing prevalence of oral health conditions, including periodontal diseases, dental caries, and the growing elderly population, is driving demand for accurate diagnostic tools and imaging solutions in the U.S. The adoption of digital X-ray systems, cone beam computed tomography (CBCT), and 3D imaging has become the norm in both private dental practices and hospital-based dental departments.

- The presence of key industry players, such as Carestream Health, Planmeca, and Sirona Dental Systems, contributes to the region's technological leadership. These companies offer innovative and user-friendly imaging systems designed to enhance diagnostic accuracy and improve patient outcomes.

- Government-backed initiatives and programs aimed at improving oral health awareness and prevention in the U.S. further solidify the country's leadership position in the North American dental radiology equipment market. Additionally, favorable insurance reimbursement policies for advanced imaging techniques are fostering widespread adoption of these technologies.

“Canada is Projected to Register the Highest Growth Rate”

- Canada is expected to register the fastest growth in the North America Dental Radiology Equipment Market. The country's universal healthcare system and increasing focus on preventative care are driving adoption of advanced dental imaging systems.

- Strategic government investments in healthcare infrastructure, particularly oral health initiatives and disease prevention programs, are accelerating the adoption of digital radiology solutions across the country. Additionally, public awareness of the importance of regular dental screenings and diagnostics is contributing to the rising demand for high-quality imaging technologies.

- The growth of dental service organizations (DSOs), which are expanding their presence across the Canadian provinces, is driving the demand for state-of-the-art radiology equipment that supports efficient patient care and high-volume diagnostics. Moreover, collaborations between academic research centers, dental schools, and biotech firms are helping to further the adoption of advanced imaging technologies, especially for orthodontics, implantology, and oral surgery.

- Increased focus on personalized dental care and the adoption of 3D imaging for treatment planning are also accelerating growth in the Canadian dental radiology market

Dental Radiology Equipment Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Dentsply Sirona Inc. (U.S.)

- Carestream Dental LLC (U.S.)

- Envista Holdings Corporation (U.S.)

- Midmark Corporation (U.S.)

- Planmeca USA Inc. (Finland)

- Vatech America, Inc (South Korea)

- Acteon Group (France)

- Owandy Radiology Inc (France)

- LED Dental Inc. (U.S.)

- PreXion Inc (Japan)

Latest Developments in Global Dental Radiology Equipment Market

- In August 2024, Carestream Health introduced an innovative digital radiology system designed to offer high-resolution imaging with lower radiation exposure. The system is equipped with advanced sensor technology and user-friendly interfaces, enabling faster imaging and improved patient comfort.

- In July 2024, Planmeca introduced an upgraded Cone Beam Computed Tomography (CBCT) system that combines high-definition 3D imaging with enhanced software tools for treatment planning and surgical guidance. This new system offers superior image quality with reduced exposure to radiation, providing optimal imaging for implantology, orthodontics, and oral surgery

- In May 2024, Sirona Dental Systems launched a revolutionary intraoral X-ray system, which offers improved image resolution and quicker diagnostic workflows. This system features a compact design with wireless capabilities, making it ideal for smaller dental practices and clinics with limited space.

- In April 2024, Vatech launched a portable dental radiography solution aimed at improving dental access in rural and underserved regions. The compact, battery-operated system is designed for mobile dental units and emergency settings, providing high-quality images on-site with reduced radiation exposure.

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。