North America Interventional Neurology Devices Market

市场规模(十亿美元)

CAGR :

%

USD

3.10 Billion

USD

5.80 Billion

2024

2032

USD

3.10 Billion

USD

5.80 Billion

2024

2032

| 2025 –2032 | |

| USD 3.10 Billion | |

| USD 5.80 Billion | |

| % | |

|

North America Interventional Neurology Devices Market Segmentation By Product Type (Embolic Coils, Flow Diversion Devices, Liquid Embolic Devices, Carotid Artery Stents, Embolic Protection Systems, Micro Support Devices, Microguidewires, Microcatheters, Neurothrombectomy Devices, CLOT Retrieval Devices, Suction and Aspiration Devices, Snares), Applications (Arteriovenous Malformation and Fistulas, Cerebral Aneurysms, Schemic Strokes, Intracranial Atherosclerotic Disease), Techniques (Angioplasty and Stenting, Neurothrombectomy, Pre OperativerTumor Embolization, Vertebroplasty, Stroke Therapy), End Use (Ambulatory Care Centers, Hospitals, Neurology Clinics)- Industry Trends and Forecast to 2032

Interventional Neurology Devices Market Size

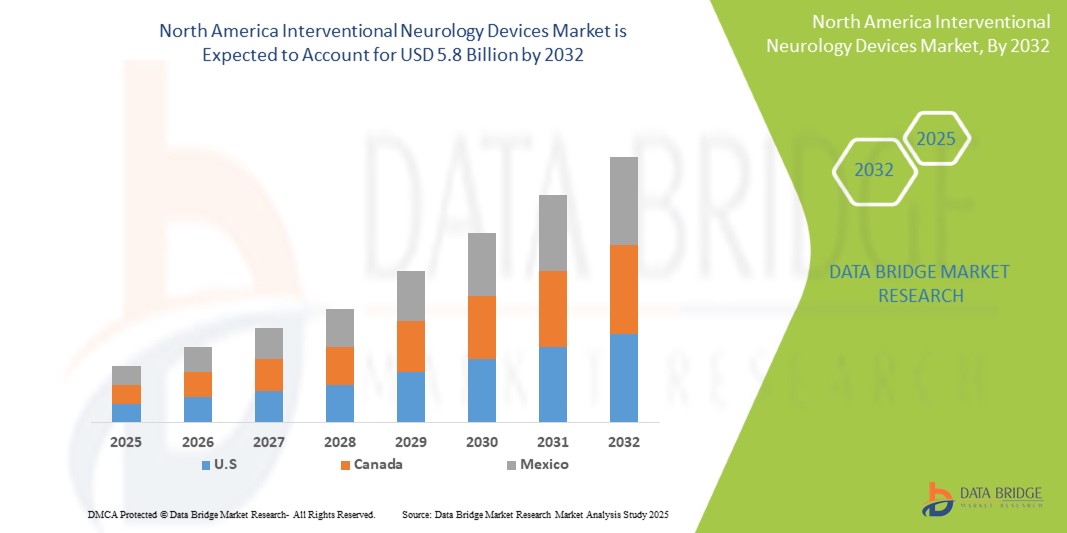

- The North America Interventional Neurology Devices Market was valued atUSD 3.1 Billion in 2024and is expected to reachUSD 5.8 Billion by 2032,at aCAGR of 7.1%during the forecast period.

- The growth of the North America Interventional Neurology Devices Market is primarily driven by the rising prevalence of neurovascular disorders such as stroke, cerebral aneurysms, and arteriovenous malformations, fueled by an aging population and increasing incidence of lifestyle-related conditions like hypertension and diabetes. Technological advancements in minimally invasive neurointerventional procedures, including the development of innovative devices like stent retrievers, embolic coils, and flow diverters, are significantly enhancing treatment outcomes and driving adoption.

North America Interventional Neurology Devices Market Analysis

- Interventional neurology devices are essential in the minimally invasive treatment of neurovascular disorders such as ischemic stroke, intracranial aneurysms, arteriovenous malformations (AVMs), and carotid artery disease. These devices—including clot retrieval systems, embolic coils, stent retrievers, balloon catheters, and flow diversion devices—enable precise navigation and treatment within the cerebral vasculature, significantly improving patient outcomes. They are commonly used in hospitals, neuro-specialty centers, and ambulatory surgical units.

- The demand for interventional neurology devices in North America is primarily driven by the rising incidence of stroke and other cerebrovascular diseases, which are closely associated with an aging population, hypertension, diabetes, and sedentary lifestyles. The region also sees strong adoption due to growing awareness of early intervention benefits, increased screening rates, and the high burden of neurovascular-related morbidity and mortality.

- U.S. dominates the North America interventional neurology devices market, supported by advanced healthcare systems, the presence of leading medical device companies, and widespread adoption of cutting-edge neurosurgical technologies. The United States, in particular, holds a leading market share, driven by favorable reimbursement policies, high healthcare expenditure, and robust clinical research and innovation pipelines.

Report ScopeInterventional Neurology DevicesMarket Segmentation

|

Attributes |

Interventional Neurology DevicesKeyMarket Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Interventional Neurology Devices Market Trends

“Technological Innovation and Expanding Clinical Applications”

- Advancements in neuroimaging and catheter-based technologies are transforming interventional neurology by enabling more precise navigation and targeted therapy within the brain’s complex vasculature. Innovations such as next-generation stent retrievers, embolic coils, and flow diverters are improving clinical outcomes and procedural safety.

- Growing adoption of minimally invasive endovascular procedures is a major trend, driven by increased physician and patient preference for non-surgical approaches to treating conditions like ischemic stroke, aneurysms, and arteriovenous malformations.

- For instance, the U.S. has seen increased use of thrombectomy devices for acute ischemic stroke treatment, encouraged by updated American Heart Association guidelines and growing physician preference for minimally invasive endovascular procedures.

- Integration of artificial intelligence (AI) and robotics in neurointerventional procedures is enhancing decision-making, reducing procedure time, and improving real-time visualization. These technologies are supporting the shift toward precision medicine in neurology.

- Expansion of mechanical thrombectomy as a standard of care for acute ischemic stroke is shaping product development and procedural protocols, supported by favorable clinical guidelines and improved reimbursement frameworks.

- Rising focus on personalized and image-guided therapies is encouraging the development of patient-specific solutions and hybrid devices, tailored to individual anatomical and pathological needs, particularly in complex neurovascular cases.

Interventional Neurology Devices Market Dynamics

Driver

““High Adoption of Advanced Neurointerventional Technologies”

- The North America Interventional Neurology Devices Market is primarily driven by the increasing adoption of advanced neurointerventional technologies aimed at improving diagnosis and treatment of acute neurological conditions such as ischemic stroke, cerebral aneurysms, and arteriovenous malformations. Devices like stent retrievers, embolic coils, and flow diverters are gaining widespread acceptance due to their ability to enable minimally invasive, precise interventions with faster recovery times and improved patient outcomes.

- Government-backed healthcare initiatives across the U.S. and Canada, including stroke awareness campaigns, NIH-funded neurovascular research, and expanding reimbursement coverage for endovascular procedures, are accelerating the adoption of interventional neurology devices in clinical practice.

- The presence of leading neuroscience research institutions, high procedural volumes in advanced stroke centers, and increasing investments in surgical robotics and AI-driven imaging are further fueling innovation and clinical integration across the region.

- Moreover, the post-COVID-19 emphasis on enhancing critical care infrastructure has reinforced the importance of rapid and effective stroke intervention technologies, contributing to continued growth in neurointerventional device deployment across hospitals and specialized neurology centers.

For instance,

- According to the American Heart Association, mechanical thrombectomy procedures for acute ischemic stroke have increased significantly in the U.S. since the 2018 guidelines expanded the treatment window for eligible patients.

- In January 2024, Stryker announced a 15% year-over-year growth in its neurovascular segment, driven by strong demand for its advanced thrombectomy and access device systems across North American stroke centers

- This trend is further supported by rising public awareness of stroke symptoms, improvements in tele-neurology and remote diagnostic support, and government investments to expand comprehensive stroke care networks throughout North America.

Opportunity

“Expansion of Interventional Neurology into Ambulatory and Community-Based Care Settings”

- he ongoing shift toward decentralized healthcare delivery is creating strong opportunities for the expansion of interventional neurology services into ambulatory surgical centers (ASCs), outpatient stroke units, and tele-neurology-enabled facilities across North America.

- Growing demand for timely, minimally invasive treatment of neurological emergencies—especially strokes—is fueling interest in bringing advanced neurointerventional capabilities closer to patients in community hospitals, mobile stroke units, and rural settings through portable imaging and catheter-based systems.

For instance,

- In February 2024, the American College of Radiology (ACR) reported a marked increase in the use of mobile stroke units equipped with CT scanners and telemedicine platforms, enabling faster diagnosis and initiation of endovascular therapies in pre-hospital environments.

- Penumbra Inc. announced the expansion of its Lightning™ Aspiration System into outpatient and regional care centers across the U.S., highlighting the growing decentralization of neurovascular care

- This trend is further supported by healthcare providers’ growing need for rapid, precise interventions, especially in stroke management, coupled with regulatory efforts to expand access to thrombectomy-capable centers. These developments are attracting significant investment in compact, AI-powered imaging tools and next-generation catheter systems designed for use in lower-acuity or remote care settings throughout North America.

Restraint/Challenge

“High Costs of Neurointerventional Devices and Regulatory Complexity”

- Interventional neurology devices—such as stent retrievers, embolic coils, flow diverters, and navigation systems—are often high-cost technologies that require substantial capital investment for acquisition, operation, and maintenance. These costs pose a challenge for smaller healthcare facilities, particularly in rural and resource-limited areas of North America, limiting widespread adoption.

- Stringent regulatory pathways mandated by agencies like the U.S. Food and Drug Administration (FDA) and Health Canada require extensive clinical validation, safety trials, and post-market surveillance, which can delay the launch of new neurointerventional products and significantly increase time-to-market for manufacturers.

For instance,

- In October 2024, a white paper by the Medical Device Innovation Consortium (MDIC) revealed that the total cost of developing and commercializing a new neurovascular device in the U.S. can exceed USD 120 million, with regulatory compliance and clinical testing accounting for over 40% of that figure.

- Smaller medtech companies face additional hurdles due to limited resources for navigating the complex approval processes and scaling manufacturing to meet safety and efficacy standards

- These high financial and procedural burdens can hinder innovation, restrict access to cutting-edge stroke care technologies in underserved regions, and intensify competitive pressures—especially for startups and mid-sized firms operating in the North America interventional neurology devices market

Interventional Neurology Devices Market Scope

The market is segmented on the basis, product type, techniques, application and end user.

|

Segmentation |

Sub-Segmentation |

|

By Product Type |

|

|

By Techniques |

|

|

By Application |

|

|

ByEnd User

|

|

In 2025, the Neurothrombectomy is projected to dominate the market with a largest share in application segment

In 2025, neurothrombectomy devices segment is expected to dominate the North America Interventional Neurology Devices Market, with the largest share of 37.22% in 2025 due to increasing use in the treatment of acute ischemic stroke. The strong clinical efficacy of mechanical thrombectomy procedures—especially when performed within the extended therapeutic window recommended by updated guidelines—has significantly expanded their adoption across stroke centers and tertiary care hospitals. The rapid development of innovative stent retrievers, aspiration catheters, and clot retrieval systems, along with favorable reimbursement policies in the U.S. and Canada, is reinforcing the leadership of this segment. Additionally, advancements in device design for better navigability, reduced procedural times, and improved outcomes are encouraging both neurologists and interventional radiologists to adopt these tools as frontline treatment options for eligible stroke patients.

The hospitals is expected to account for the largest share during the forecast period in end user market

In 2025, the hospitals and surgical centers segment is expected to dominate the market with the largest market share of 23.31%. This dominance is attributed to their central role in performing complex neurointerventional procedures, including thrombectomy, aneurysm coiling, and flow diversion. These facilities benefit from high patient volumes, access to trained specialists, and advanced infrastructure, making them key hubs for the deployment of cutting-edge neurovascular technologies. Moreover, the rise in comprehensive stroke centers and neurocritical care units across the region is expanding the reach and utilization of interventional neurology devices. The push for better stroke outcomes, integration of hybrid operating rooms, and the availability of 24/7 neurointervention teams are further positioning hospitals as the primary drivers of growth in this segment.

Interventional Neurology Devices Market Regional Analysis

“U.S. is the Dominant Country in the Interventional Neurology Devices Market”

- The U.S. leads the North America Interventional Neurology Devices Market, accounting for the largest share due to its highly advanced healthcare infrastructure, a robust medical device market, and substantial investments in life sciences research. The country’s well-established healthcare system, coupled with widespread adoption of cutting-edge medical technologies, positions it as the dominant player in this sector.

- The growing incidence of neurological disorders such as stroke, cerebral aneurysms, and arteriovenous malformations is driving significant demand for neurointerventional devices. With a high burden of cardiovascular and cerebrovascular diseases, the need for effective and timely interventions is pushing the adoption of advanced devices like stent retrievers, aspiration catheters, and thrombectomy systems.

- Key industry players such as Medtronic, Stryker, Johnson & Johnson (Cerenovus), and Penumbra contribute to the region's technological leadership, offering innovative neurovascular solutions and expanding the availability of cutting-edge devices in hospitals and surgical centers.

- Favorable reimbursement policies and increasing government and private healthcare funding in the U.S. continue to drive market growth. The establishment of comprehensive stroke centers and advancements in stroke care protocols are contributing to the country’s leadership position in the interventional neurology devices market.

“Canada is Projected to Register the Highest Growth Rate”

- Canada is expected to witness the highest growth rate in the North America Interventional Neurology Devices Market, driven by its universal healthcare system and a national focus on improving disease surveillance, early diagnosis, and neurointerventional care. The Canadian healthcare model, which emphasizes equitable access to medical services, is positioning the country for strong growth in advanced neurovascular procedures.

- Strategic government investments in neurovascular research and molecular diagnostics are contributing to the growing adoption of interventional neurology technologies. Initiatives such as funding for stroke care programs and research into new neurointerventional techniques are enhancing Canada’s capacity to treat complex neurological conditions, further supporting the demand for neurovascular devices.

- The expansion of personalized medicine and genomics programs, such as those led by Genome Canada, is fostering greater use of image-guided and minimally invasive neurosurgical solutions. As personalized treatments for conditions like stroke and aneurysms become more prevalent, demand for tailored neurointerventional devices is set to grow.

- Increased collaborations between Canadian academic research centers, medical device companies, and healthcare institutions are promoting innovation in neurointerventional technologies. The growing awareness of stroke symptoms, coupled with enhanced public health education, is driving greater patient and physician engagement in neurovascular care

Interventional Neurology Devices Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, North America presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Abbott Laboratories (U.S.)

- Balt USA (U.S.)

- Integra LifeSciences Corporation (U.S.)

- Johnson & Johnson (Cerenovus) (U.S.)

- Medtronic plc (U.S.)

- MicroVention, Inc. (U.S.)

- Penumbra, Inc. (U.S.)

- Stryker Corporation (U.S.)

Latest Developments in North America Interventional Neurology Devices Market

- In March 2023, Johnson & Johnson launched its new CEREPAK Detachable Coils in the U.S. The coils offer three distinct shapes and multiple sizes, providing physicians with various options to treat brain aneurysms. These coils are designed for concentric aneurysm filling, contributing large volumetric filling to enhance treatment outcomes and improve patient care.

- In June 2023, BIOTRONIK, a leading medical device company, introduced the limited release of its Oscar (One Solution: Cross. Adjust. Restore) multifunctional peripheral catheter. This catheter offers innovative features for vascular procedures, allowing physicians to cross, adjust, and restore vascular access efficiently. It aims to improve procedural efficiency and patient outcomes in peripheral artery disease treatments

- In April 2022, Integer Holdings Corporation acquired Connemara Biomedical Holdings Teoranta, including its subsidiaries Aran Biomedical and Proxy Biomedical. This acquisition enhances Integer’s portfolio, enabling it to offer comprehensive solutions for complex delivery and therapeutic devices. The move strengthens Integer’s presence in high-growth markets like neurovascular, cardiovascular, and general surgery, advancing their medical device capabilities.

- In December 2020, Terumo Corporation announced the release of their WEBTM Embolization System, which is a novel intravascular device that can be used to treat intracranial wide neck bifurcation aneurysms that cannot be surgically clipped.

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。