North America Intumescent Coatings For Fireproofing And Spray

市场规模(十亿美元)

CAGR :

%

USD

454.95 Million

USD

667.07 Million

2025

2033

USD

454.95 Million

USD

667.07 Million

2025

2033

| 2026 –2033 | |

| USD 454.95 Million | |

| USD 667.07 Million | |

| % | |

|

北美防火和喷雾应用防火材料集成炉,按产品类型(防火和喷雾应用防火材料集成炉),类型(Thick-Film和Thin-Film),Resin(Epoxy、Acrylic、Alkyd、聚氨酯等),底物(钢铁和铸铁、木材、复合元素等),技术(以催化为主、以水为主、以溶剂为主和以粉为主)、应用(Hydrocarp和Cellulosic),最终用途(建筑和建筑、石油和天然气、工业、汽车、航空航天等)——2033年工业趋势和预测

北美防火和喷洒-活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性

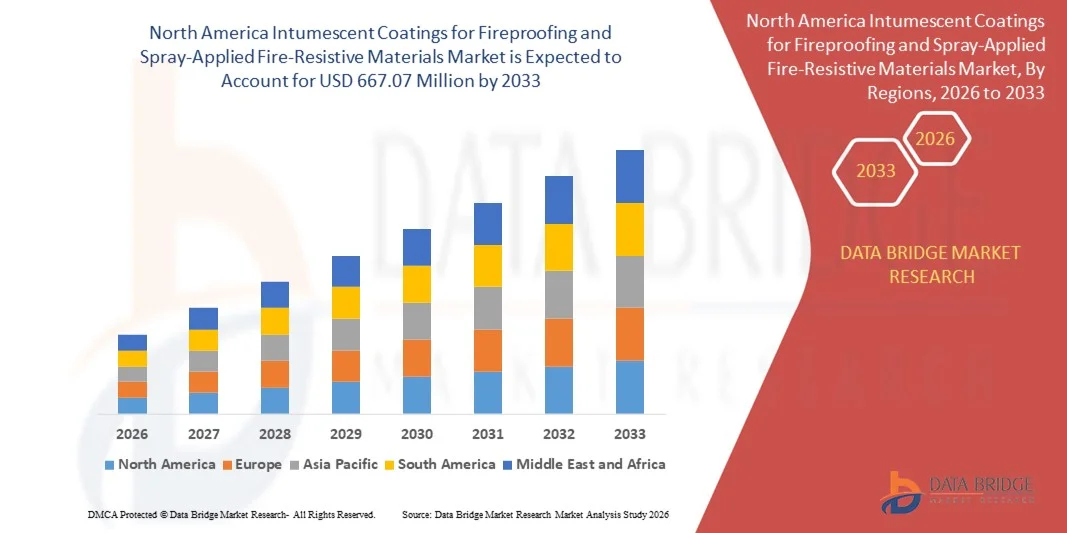

- 北美用于防火和喷雾喷射的防火用涂层市场规模估价2025年4.5495亿美元并可望达到截至2033年的66,707万美元, 以美元计CAGR为 4.90%预测期间

- 市场增长主要得益于基础设施的不断发展以及住宅、商业和工业部门严格的消防安全条例,从而驱动了对被动消防解决方案的需求,如无动于衷的涂层和喷雾式防火材料

- 此外,对结构消防安全的认识日益提高,加上以水为基础的和生态友好型涂层技术的进步,正在加速在建筑和制造业采用这些材料,从而大大地推动市场的扩大。

防火和喷雾应用防火材料市场“Intumescent Coatings”的主要出口品是什么?

- 扰动涂层和喷雾式灭火材料是被动防火解决方案,适用于结构元素,通过在暴露于高温时形成隔热炭层来增强防火能力,在火灾事件中有助于保持结构完整性

- 特别是在高层建筑、石油和天然气设施以及公共基础设施中越来越多地实施消防安全守则,加上建筑中越来越多地使用钢和复合材料,正在推动全球对这些涂层的需求

- 在商业建筑、工业设施、石油和天然气基础设施、发电和运输项目需求强劲的推动下,美国主导了北美防火和喷雾式防火材料市场,2025年收入份额估计为58.2%。

- 加拿大预计在预测期间将登记最快的CAGR,为11.02%,其动力是基础设施的日益发展、商业建设的不断提高以及公共和私人建筑严格执行防火条例。

- 2024年,防火部分的无常涂层因其优美美观,易被应用,以及在不影响结构外观的情况下提供被动防火的能力,占据了最大的市场份额.

防火和喷洒应用防火材料市场分解的范围和冲击力报告

| 属性 | 用于防火和喷洒-应用防火材料的喷涂 |

| 覆盖部分 |

|

| 涵盖国家 | 北美

|

| 关键市场玩家 |

|

| 市场机会 |

|

| 添加数据信息集的值 | 除了对市场价值、增长率、分块化、地域覆盖和主要参与者等市场假设的见解之外,数据桥市场研究所编写的市场报告还包括深入的专家分析、定价分析、品牌份额分析、消费者调查、人口分析、供应链分析、价值链分析、原材料/可消耗品概览、供应商选择标准、PESTLE分析、波特分析以及监管框架。 |

防火和喷雾应用防火材料市场中的主要趋势是什么?

增加消防安全条例

- 全世界日益增长的消防安全条例是刺激无常涂层和喷雾式防火材料增长的主要动力。 高层、工业结构和公共基础设施的新建筑规范越来越多地要求使用先进的被动消防,刺激了新建筑和翻修项目的需求

- 例如,亚太的监管制度,例如中国和印度最近的高层消防法规,现在要求24米以上的高塔采用薄膜的无序涂层,使第三方认证和遵守成为市场准入的先决条件。 欧盟对低VOC配方和可持续性的推动,进一步加快了传统材料向现代、环境友好的无序涂层的转变。

- 美国国家消防协会(NFPA)等消防安全主管部门记录了持续上升的火灾事件,为商业、工业和住宅建筑实施更严格的消防安全标准和检查制度增加了紧迫性。

- 提高耐受性涂层——如纳米强化涂层、石墨浸入涂层和以水为基的配方——的耐受性,以更薄的地层为主,支持现代建筑设计并遵守不断演变的规范

- 可持续性目标,包括使用生物树脂和可回收防火系统,正在影响产品创新,因为环境影响成为监管框架和开发者决定的一个因素

- 正在出现混合解决方案,将被动涂层与主动监测(IOT传感器、智能涂层)相混合,确保整个建筑物生命周期的维护和性能跟踪

防火和喷洒-抗火材料市场的 " 浸泡涂料 " 的主要驱动力是什么?

- 世界各地野火日益频繁和严重,明显加快了对防火解决方案的投资。 风险地区荒地-城市对接区,重要基础设施和工业设施要优先提供先进消防物资,以保护资产并完成保险和监管任务.

- 例如,在美国西部和澳大利亚发生创纪录的野火后,政府和私营部门运营商都增加了防火预算,为周边结构、应急设施和交通基础设施具体规定了无序涂层和SFRMs,以尽量减少损失和损坏。

- 技术革新——例如AI驱动的风险模型、基于无人机的检查和实时探测——在针对和优化高风险地区防火投资方面发挥关键作用。

- 现在,防火被认为是新建和改造现有建筑物的必要要求,特别是在火灾事件给更强有力的抗灾能力和备灾战略带来压力的情况下

- 政策激励措施、更严格的保险范围要求和减灾资金,进一步刺激了市场超越传统工业部门的扩张。

为防火和喷洒应用的防火材料市场挑战刺激性凝胶增长的因素是什么?

- 尽管不稳涂层和SFRMs的优点——包括重量更轻、美学灵活性和复杂钢结构的优异性能——诸如水泥喷雾和矿物纤维板等传统防火材料继续构成重大竞争,特别是在价格敏感和工业规模的应用方面。

- 例如,对于大型结构钢铁项目来说,水泥防火往往更受青睐,因为它的前期成本较低,易于批量应用,而且管制认可也十分完善,尽管它可能很庞大,可能会损害空间或设计优雅。

- 不稳定的涂层通常需要更专业的应用技术,并可以承担更高的初始成本,这可以阻止预算所限制的项目或消防安全规范不太严格的区域采用

- 已确立的供应链、承包商的熟悉程度以及与传统产品相关的传统规格,使得较新的配方难以迅速被保守的建筑市场接受

- 在一些工业和商业环境中,尽管在扰动技术方面进行了创新,但维护和环境接触方面的关切(如湿度或撞击损害)可能会尖锐地采取更古老、更坚固、甚至更优雅的防火办法。 解决价格敏感性问题并提高对生命周期惠益的认识,仍然是推动对遗留替代品采用无序和喷雾材料的关键

防火和喷雾应用防火材料市场如何分离?

市场按产品类型、类型、树脂、底物、技术、应用和最终用户.

- 按产品类型

根据产品类型,将市场分出为防火和喷雾相接活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性活性 防火部分的起伏涂层因其优美美观,易被应用,在不损害结构外观的情况下提供被动防火的能力而占据了2024年最大的市场份额. 这些涂层在商业和高层建筑中非常受欢迎,在高温下膨胀,形成一个能隔绝下层材料的焦炭层,从而延迟了起火时的结构倒塌. 它们越来越多地被用在钢结构的建筑中,并且越来越遵守有关消防安全标准的规定,这些都正在推动部分的主导地位。

喷洒式活火材料部分预计将在2025至2032年期间增长最快,原因是其成本效益高并广泛应用于工业和大型基础设施项目。 特别在防火必须覆盖复杂地貌或宽地表区域的情况下,SFRMs因其快速安装和强烈的绝热特性而更受欢迎。 它们越来越多地用于改造老旧建筑和石油及天然气设施,提高了它们的增长前景。

- 按类型

根据类型,市场被分出为厚膜和薄膜涂层. 厚膜地段主导了2024年收入份额最高的市场,其驱动力在于其在油气防火方面的广泛应用,特别是在石油化工和能源厂等高风险环境中. 厚薄薄膜涂层可提供更耐久性,更佳的绝热性能,并有更长的耐火时间,使它们成为重型基础设施的关键选择.

薄膜部分预计将在2025至2032年间呈现出最快的增长速度,这主要是因为它在美学至高的建筑应用中日益被采用. 薄膜涂层在商业建筑和办公室中很受青睐,因为它们的平整完好,重量低,在纤维活火条件下表现可靠. 它们与装饰性上衣的相容性和较低的应用厚度促使它们越来越偏好建筑师和承包商。

- 通过Resin

根据树脂类型,市场被分出为环氧,丙烯,烯烃,聚氨酯等. 在2024年,环氧部分因其特殊的粘合、防腐蚀和机械强度而拥有59%的最大市场份额。 以叶氧为原料的防火涂层被广泛用于石油和天然气、海洋和工业部门,这些部门的耐久性和化学耐受性至关重要。 在极端环境条件下工作的能力支持他们在高风险设施中发挥领导作用。

由于绿色建筑项目对水基低VOC涂层的需求,丙烯基部分预计将从2025年增长到2032年的最高CAGR. 丙烯树脂能提供快速干燥,成本效益高,符合环境要求,使它们成为住宅和轻型商业防火应用的理想. 它们越来越多地被用在薄膜系统和装饰涂层上,进一步促进了片段生长.

- 按底盘

以地基为基础,将市场分出为结构铸铁和铸铁,木材,复合元素等. 结构铸铁和铸铁在2024年占据了市场主导地位,辅以它们在大型钢框架中被广泛使用,并迫切需要为这种有载重的部件提供防火. 金属底物的强热导能需要先进的防火涂层,以便在火灾情况下保持结构完整性。

由于模块化建筑、住宅楼和室内设计方面的应用不断增加,木材部分预计将在2025年至2032年期间增长最快。 随着木结构在可持续建筑中更加突出,在确保安全的同时需要保护美学的阻燃剂解决方案,正驱动着对能与木材相容的特制扰动涂层的需求。

- 按技术分列

根据技术,市场分为环氧基,取水基,溶剂基和取粉基. 以Epoxy为主的涂装在2024年占据了市场主导地位,因其在近海和石油天然气应用方面的出色表现. 这些涂层能抵抗水分,化学物质,以及机械压力,使得它们理想地适应恶劣的环境,火险与腐蚀性暴露相结合.

预计从2025年到2032年,以水为基的涂层增长最快,这得到环境条例和低VOC和无毒防火材料的推动。 它们方便用户的应用、快速干燥的时间和最微小的气味使它们越来越适合占用的建筑物、学校和医疗保健环境。

- 通过应用程序

根据应用情况,市场被分割成碳氢化合物和纤维素防火。 碳氢防火在2024年由于石油天然气,化工加工,外出工业的严格安全规范而带动了市场,由燃料燃烧所引发的高温火灾造成了严重的结构风险. 这些应用中使用的涂装是为了在爆炸条件下能承受快速升温并保持完整性而设计的.

由于商业和住宅建筑使用量增加,预计在预测期间,Cellulosic防火工作增长最快。 这些由木材、纸张和家具所驱动的火灾需要有效和可视接受的防火解决方案,使建筑师和开发商倾向于采用无动于衷的涂层。

- 按最终用户

在最终用户的基础上,市场被分割成建筑和建筑、石油和天然气、工业、汽车、航空航天等。 2024年,建筑和建筑部分主导了市场,其基础是扩大城市基础设施,更加注重占用安全,发达国家和发展中国家越来越多地采用消防安全守则。 高层住宅和商业项目钢木结构防火继续推动需求.

据预测,石油和天然气部门在2025年至2032年期间增长最快,原因是安全条例加强,不断对炼油和勘探进行投资,以及迫切需要防止火灾事故造成灾难性损害。 在这些环境下的防火涂层保护了生命,也确保了在高风险环境中操作的连续性.

哪个地区拥有防火和喷雾应用防火材料市场最大的份额?

- 在商业建筑、工业设施、石油和天然气基础设施、发电和运输项目需求强劲的驱动下,美国主导了北美防火和喷雾式防火材料市场的无常涂层,2025年的收入份额估计为58.2%。 严格的消防安全条例,高楼建筑广泛采用防火材料,老化基础设施不断翻新等,都极大地支撑了市场增长.

- 越来越注重消防合规、资产安全、结构完整性和减少风险,加快了工业和商业应用中先进的无序涂层的采用。 主要涂层厂商的存在、强大的研发能力以及对防火材料技术的持续投资进一步加强了区域市场领导力

加拿大防火和喷洒-应用防火材料喷涂市场透视

预计加拿大在预测期间将登记最快的CAGR,为11.02%,其动力是基础设施的日益发展、商业建筑的不断兴起以及公共和私人建筑严格执行消防安全条例。 石油和天然气设施、工业厂房和运输基础设施的日益采用进一步支持了市场的扩大。

墨西哥防火和喷雾应用防火材料喷雾系统

墨西哥在制造业活动扩大、基础设施现代化以及对工业和商业建设的投资增加等支持下稳步增长。 提高工厂和公共基础设施对消防安全标准的认识并采用防护涂层,正在推动全国市场持续增长。

在防火和喷雾应用防火材料市场上的顶级公司是哪些?

防火和喷洒应用防火材料的Intumescent Coatings主要由一些历史悠久的公司领导,其中包括:

- P2i有限公司 (英国).

- NEI Corporation (美国).

- UltraTech国际公司(美国)

- Aculon Inc. (美国)

- 莲花叶可口可乐股份有限公司(美国).

- Rust-Oleum (美国).

- 西通尼克斯 (美国).

- 纳西奥·纳诺·科阿廷斯(土耳其)

- 哈佛学院院长和研究员(美国)

- LiquiGlide Inc. (美国).

- 冲浪技术(法国)

- 佩尔纳诺 (美国).

- Henkel AG & Co. KGaA(德国)

- 克罗尼特语 (英国).

- 纳诺希尔有限责任公司(美国)

- 纳诺尔 (美国).

北美防火和喷雾应用防火材料市场的近况如何?

- 2025年6月,亨特斯曼推出了以聚氨酯为主的POLYRESYST EV5005涂层系统,专门设计用于汽车应用. 这一创新通过在不损害设计灵活性的情况下加强金属和复合电池组件的被动防火,应对了电动车辆面临的重大消防安全挑战。 预计该次发射将扩大在汽车部门,特别是在EV电池安全方面使用无序涂层,加强与运输有关的防火解决方案的市场增长

- 2023年6月,乔通扩大了其"全球Intumescent"研发实验室,以推进产品创新和技术进步. 这一扩展旨在加强产品开发和消防测试能力,并加速创造创新和先进产品。 此外,它还为乔通现有的产品范围提供认证支持,加强了其在无忧涂料市场的地位.

- 2022年1月,PPG Industries为钢结构定制的PPG AMERCOAT被动防火涂装范围揭幕. 这些涂层作为以水为基础的动荡解决方案,有助于提高安全标准,同时符合日益增长的环境和监管预期。 发射加强了PPG在支持工业和基础设施消防安全方面的作用,进一步推动市场采用可持续的防火材料

- 2020年5月,谢尔温-威廉斯引入了Firetex M90/03,这是一种能为现场和场外应用提供长达90分钟的防火阻力的无常涂层. 该产品对不同建筑环境的适应性支持了模块化和预制建筑做法的不断增长的趋势. 这一创新有助于在多功能建筑环境中扩大防火涂层的使用,支持传统和现代建筑方法的市场扩张

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。