The rapid acceleration of digital transformation initiatives across global economies has significantly reshaped infrastructure priorities within both public and private sector organizations. Governments, financial institutions, telecom operators, and enterprises are increasingly digitizing operations to enhance efficiency, scalability, and service delivery. As critical processes migrate to cloud-based and online environments, continuous system availability has become a non-negotiable requirement. Power interruptions are no longer viewed as isolated technical failures but as direct threats to business continuity, data integrity, customer trust, and regulatory compliance.

In parallel, there is a growing global emphasis on data localization and sovereign cloud infrastructure, driven by cybersecurity concerns, regulatory frameworks, and latency optimization requirements. Countries across North America, Europe, Asia-Pacific, and the Middle East are prioritizing domestic data hosting to maintain control over sensitive information and ensure compliance with evolving data protection laws. This has led to a surge in the development of hyperscale data centers, edge computing facilities, and localized cloud infrastructure. As a result, power reliability is being embedded into infrastructure planning from the initial design phase, with stable and conditioned power supply becoming a foundational requirement for safeguarding digital assets and ensuring uninterrupted operations.

Within this evolving digital ecosystem, uninterruptible power supply (UPS) systems are increasingly integrated into large-scale infrastructure investments. Higher uptime standards—often exceeding 99.999%—are being mandated across data centers, banking networks, government platforms, and telecom infrastructure. As digital ecosystems expand into smart cities, AI-driven platforms, and interconnected service environments, UPS solutions are being recognized as critical enablers of operational resilience, fault tolerance, and long-term digital sustainability.

Access Full Report @ https://www.databridgemarketresearch.com/reports/global-uninterruptible-power-supply-ups-market

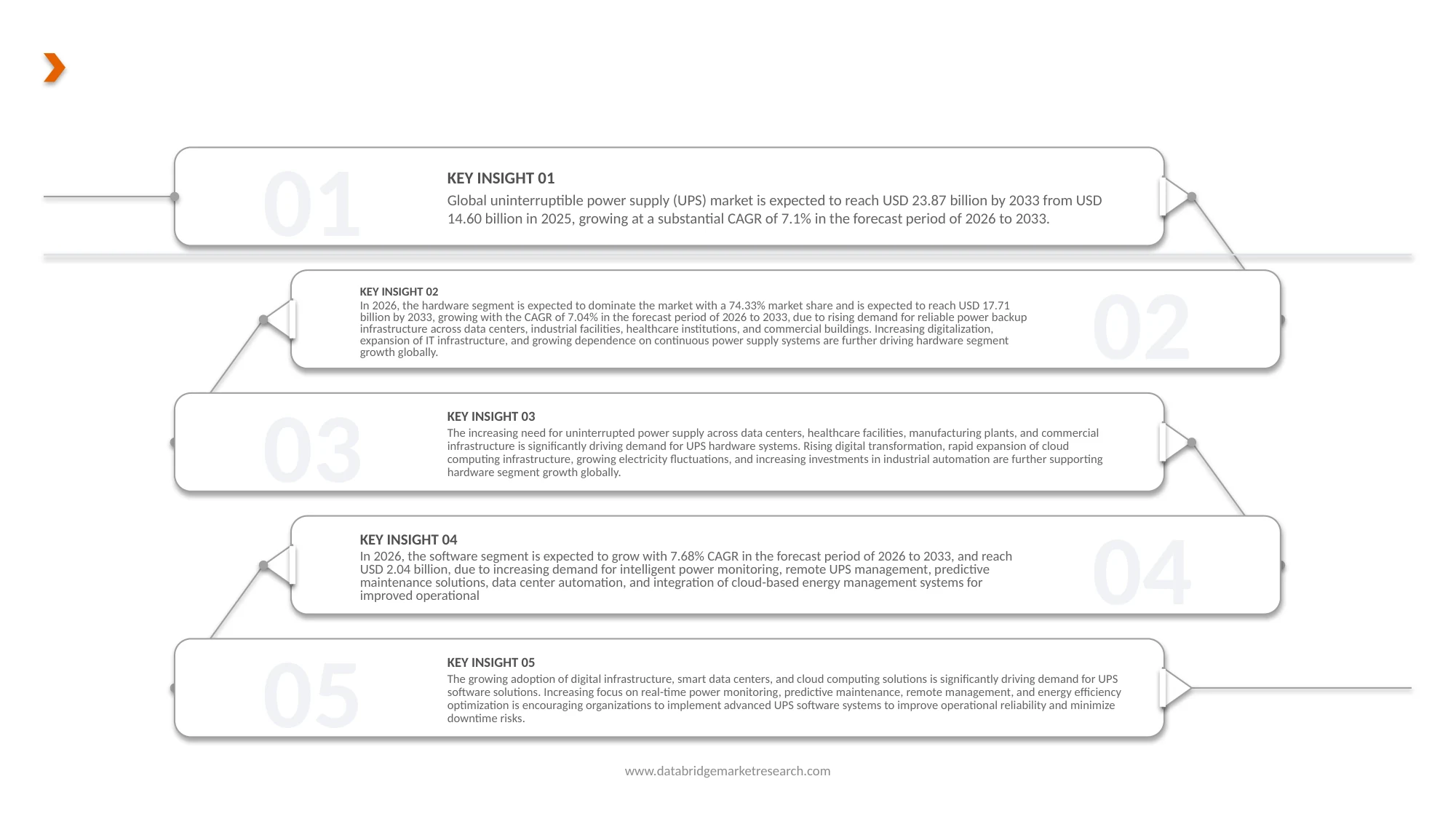

Data Bridge market research analyses that Global Uninterruptible Power Supply (UPS) Market is expected to reach USD 23.87 billion by 2033 from USD 14.60 billion in 2025, growing with a substantial CAGR of 7.1% in the forecast period of 2025 to 2033.

Key Findings of the Study

Growth in Telecom Network Densification and Fiber Broadband Penetration Initiatives

Growth in telecom network densification and fiber broadband penetration initiatives across global markets has been significantly reshaping the digital connectivity landscape. Expansion of mobile networks, 5G deployment, tower upgrades, and fiber-to-the-home (FTTH) rollouts are being accelerated to meet rising demand for high-speed data services, enterprise connectivity, and digital applications. As data consumption continues to surge across developed and emerging economies, telecom infrastructure is being strengthened to ensure wider coverage, enhanced bandwidth capacity, and improved service reliability.

Substantial investments are being directed toward upgrading switching centers, expanding transmission networks, and modernizing core telecom infrastructure. Fiber backbone expansion is being prioritized globally to support increasing traffic from cloud computing, video streaming, digital payments, IoT ecosystems, and enterprise platforms. Telecom facilities, including base transceiver stations, edge nodes, and data switching hubs, are increasingly required to operate with minimal interruption, making power continuity and voltage stability critical for maintaining network uptime and service quality.

As telecom operators expand connectivity into rural, remote, and underserved regions, infrastructure resilience is becoming a key component of deployment strategies. Remote tower sites and distributed network nodes are often exposed to grid instability and localized outages, particularly in emerging markets. As a result, reliable backup power solutions, including UPS systems, are being widely integrated into telecom infrastructure projects to ensure uninterrupted operations, protect sensitive equipment, and support global digital inclusion initiatives.

Report Scope and Market Segmentation

|

Report Metric

|

Details

|

|

Forecast Period

|

2026 to 2033

|

|

Base Year

|

2025

|

|

Historic Years

|

2024 (Customizable to 2018-2023)

|

|

Quantitative Units

|

Revenue in USD billion

|

|

Segments Covered

|

By Offering (Hardware, Software, Service), By Power Rating (Less Than 3 KVA, 3-10 KVA, 10 KVA–20 KVA, 20 KVA–50 KVA, 50–100 KVA, 100–200 KVA, 200–500 KVA, 500–1000 KVA, and ABOVE 1000 KVA), By Organization (Small Enterprise Size, Medium Enterprise Size, and Large Enterprise Size), By Form Factor (Standalone UPS, Embedded UPS, and Containerized UPS Systems), By Application (Backup Power, Emergency Power, Voltage Regulation, Power Conditioning, and Critical Power Protection), By Phase (Three Phase, and Single Phase), By Installation (Rack-Mounted, Tower-Based, Floor Standing, Cabinet Ups, and Wall Mounted), By Price Range (Low, Mid, and High), By Energy Storage (VRLA, Lithium-Ion, Flywheel-Based UPS, and Supercapacitor-Based Systems), By Topology (Line Interactive, Standby/Offline, and Online / Double Conversion), By Design (Modular UPS, and Conventional (Monolithic) UPS), By Vertical (Government & Public Sector, It & Telecom, Hospitality & Tourism, Construction & Real Estate, Healthcare, Energy & Utilities, Media And Entertainment, Manufacturing, Gaming, Data Center Residential, Retail, BFSI, Education, and Oil & Gas E-Commerce, Others), By Sales Channel (Direct, and Indirect)

|

|

Countries Covered

|

North America

Europe

Asia-Pacific

Middle East and Africa

South America

Rest of South America

|

|

Market Players Covered

|

|

|

Data Points Covered in the Report

|

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand.

|

Segment Analysis

Global uninterruptible power supply (UPS) market is categorized into thirteen notable segments which are based on offering, power rating, organization, form factor, application, price range, phase, installation, energy storage, topology, design, vertical, sales channel.

- On the basis of offering, Global uninterruptible power supply (UPS) market is segmented into Hardware, Software, Service

In 2026, the hardware segment is expected to dominate the market

In 2026, hardware is expected to dominate the market with a 74.33% share, driven by substantial investments in data centers, telecommunications infrastructure, healthcare facilities, industrial manufacturing, and commercial real estate. Increasing grid instability and voltage fluctuations in several regions are further accelerating demand for reliable power backup systems. Additionally, the expansion of hyperscale and edge data centers, along with infrastructure modernization initiatives, is fueling large-scale procurement of UPS hardware components such as batteries, inverters, rectifiers, and power modules, reinforcing the segment’s leading position.

- On the basis of power rating, the Global uninterruptible power supply (UPS) market is segmented into Less than 3 kVA, 3–10 kVA, 10–20 kVA, 20–50 kVA, 50–100 kVA, 100–200 kVA, 200–500 kVA, 500–1000 kVA, and Above 1000 kVA

In 2026, the Less Than 3 kVA segment is expected to dominate the market

In 2026, the Less Than 3 kVA segment is expected to dominate the market with a 11.68% share, driven by strong demand from residential users, small offices/home offices (SOHO), retail outlets, and small commercial establishments. The increasing use of personal computers, routers, surveillance systems, and point-of-sale (POS) terminals is fueling consistent demand for low-capacity, cost-effective backup solutions. Additionally, frequent short-duration outages and voltage fluctuations across many regions are encouraging households and SMEs to invest in compact UPS systems for basic power protection.

- On the basis of organization, the Global uninterruptible power supply (UPS) market is segmented into Small Enterprise Size, Medium Enterprise Size, and Large Enterprise Size

In 2026, the Large Enterprise Size segment is expected to dominate the market

In 2026, the Large Enterprise Size segment is expected to dominate the market with a 63.24% share, driven by substantial investments in mission-critical infrastructure, including data centers, telecommunications networks, BFSI institutions, oil & gas operations, large-scale manufacturing facilities, and healthcare systems. Large enterprises require high-capacity, redundant, and scalable UPS systems to ensure uninterrupted operations, protect sensitive equipment, and meet stringent uptime, compliance, and data security requirements. Their higher capital expenditure capabilities and focus on operational continuity further strengthen demand for advanced UPS solutions.

- On the basis of form factor, the Global uninterruptible power supply (UPS) market is segmented into Standalone UPS, Embedded UPS, and Containerized UPS Systems

In 2026, the Standalone UPS segment is expected to dominate the market

In 2026, the Standalone UPS segment is expected to dominate the market with a 73.91% share, driven by its broad applicability across residential, commercial, and industrial sectors, along with advantages such as ease of installation, cost-effectiveness, and operational flexibility. Standalone systems are widely preferred by SMEs, offices, retail outlets, healthcare facilities, and telecom sites due to their ability to support varying load requirements and their suitability for both new installations and retrofit applications. Additionally, the growing demand for decentralized and plug-and-play power backup solutions further reinforces the segment’s leading position globally.

- On the basis of application, the Global uninterruptible power supply (UPS) market is segmented into Backup Power, Emergency Power, Voltage Regulation, Power Conditioning, and Critical Power Protection

In 2026, the Backup Power segment is expected to dominate the market

In 2026, the Backup Power segment is expected to dominate the market with a 43.90% share, driven by the increasing occurrence of power outages, voltage fluctuations, and grid instability across residential, commercial, and industrial sectors. The growing reliance on digital infrastructure, data centers, telecommunications networks, healthcare systems, and financial institutions has significantly increased the need for uninterrupted operations. Additionally, the expansion of SMEs and rising awareness regarding equipment protection and business continuity are further supporting the widespread adoption of UPS systems primarily for backup power applications.

- On the basis of phase, the Global uninterruptible power supply (UPS) market is segmented into Three Phase and Single Phase

In 2026, the Three Phase segment is expected to dominate the market

In 2026, the Three Phase segment is expected to dominate the market with a 63.30% share, driven by strong demand from data centers, industrial manufacturing facilities, oil & gas operations, large commercial complexes, and healthcare institutions that require high-capacity and stable power backup solutions. Three-phase UPS systems are well-suited for handling heavy electrical loads, supporting critical infrastructure, and enabling scalable operations, while also offering higher efficiency and improved load balancing compared to single-phase systems. Ongoing infrastructure development and the expansion of enterprise-scale operations across global markets further reinforce the segment’s leadership.

- On the basis of installation type, the Global uninterruptible power supply (UPS) market is segmented into Rack-Mounted, Tower-Based, Floor Standing, Cabinet UPS, and Wall Mounted.

In 2026, the Rack-Mounted segment is expected to dominate the market

In 2026, the Rack-Mounted segment is expected to dominate the market with a 30.49% share, driven by the rapid expansion of data centers, server rooms, telecom infrastructure, and enterprise IT environments. Rack-mounted UPS systems offer space efficiency, scalability, and seamless integration with standardized server racks, making them highly suitable for structured IT setups. Additionally, increasing digital transformation, rising cloud adoption, and the growth of colocation and edge data centers are further accelerating demand for rack-based UPS deployments globally.

- On the basis of price range, the Global uninterruptible power supply (UPS) market is segmented into Low, Mid, and High

In 2026, the Mid segment is expected to dominate the market

In 2026, the Mid segment is expected to dominate the market with a 59.97% share, driven by its balanced cost-to-performance ratio, making it the preferred choice across small and medium enterprises (SMEs), commercial establishments, healthcare facilities, and mid-sized industrial units. Mid-range UPS systems typically offer enhanced features such as improved battery life, basic remote monitoring, voltage regulation, and higher energy efficiency—without the significant capital expenditure associated with premium systems. Increasing demand for reliable yet cost-efficient power backup solutions across both developed and emerging markets continues to support strong adoption of this segment.

- On the basis of energy storage, the Global uninterruptible power supply (UPS) market is segmented into VRLA, Lithium-Ion, Flywheel-Based UPS, and Supercapacitor-Based Systems

In 2026, the VRLA segment is expected to dominate the market

In 2026, the VRLA segment is expected to dominate the market with a 61.28% share, driven by its cost-effectiveness, established supply chain, and proven operational reliability across a wide range of applications. VRLA batteries are extensively used in small to mid-sized UPS systems across residential, commercial, and industrial environments due to their lower upfront cost and ease of replacement. Continued adoption across SMEs, telecom infrastructure, retail outlets, and institutional facilities further supports sustained demand, particularly in cost-sensitive markets..

- On the basis of topology, the Global uninterruptible power supply (UPS) market is segmented into Line Interactive, Standby/Offline, and Online / Double Conversion.

In 2026, the Line Interactive segment is expected to dominate the market

In 2026, the Line Interactive segment is expected to dominate the market with a 26.49% share, driven by its optimal balance between cost and performance, offering both voltage regulation and battery backup capabilities. Line interactive UPS systems are widely adopted across small and medium enterprises (SMEs), commercial establishments, and residential applications, where protection against voltage fluctuations, brownouts, and short-duration outages is essential. Compared to standby systems, they provide enhanced power conditioning, while remaining more cost-effective than online/double conversion UPS, making them a preferred mid-range solution globally.

- On the basis of design type, the Global uninterruptible power supply (UPS) market is segmented into Modular UPS and Conventional (Monolithic) UPS.

In 2026, the Conventional (Monolithic) UPS segment is expected to dominate the market

In 2026, the Conventional (Monolithic) UPS segment is expected to dominate the market with an 82.30% share, driven by its widespread adoption across commercial buildings, industrial facilities, healthcare institutions, and mid-sized data centers. Conventional UPS systems are favored for their proven reliability, lower upfront capital cost, and suitability for stable, fixed-load applications. Additionally, the large installed base of monolithic systems globally continues to generate steady demand for replacement, refurbishment, and capacity upgrades, reinforcing the segment’s market leadership.

- On the basis of vertical, the Global uninterruptible power supply (UPS) market is segmented into Government & Public Sector, IT & Telecom, Hospitality & Tourism, Construction & Real Estate, Healthcare, Energy & Utilities, Media and Entertainment, Manufacturing, Gaming, Data Center, Residential, Retail, BFSI, Education, Oil & Gas, E-Commerce, and Others

In 2026, the Data Center segment is expected to dominate the market

In 2026, the Data Center segment is expected to dominate the market with a 25.16% share, driven by substantial global investments in digital infrastructure, including hyperscale data centers, colocation facilities, and cloud computing ecosystems. The rapid increase in internet penetration, data consumption, fintech expansion, and e-commerce activity, along with regulatory requirements for data localization, is accelerating data center construction across regions. These facilities require highly reliable, scalable, and redundant UPS systems to ensure zero downtime, maintain uptime standards, and meet stringent service-level agreements (SLAs). Additionally, the growing focus on energy efficiency and sustainability in data center operations is further strengthening demand for advanced UPS solutions

- On the basis of sales channel, the Global uninterruptible power supply (UPS) market is segmented into Direct and Indirect.

In 2026, the Indirect segment is expected to dominate the market

In 2026, the Indirect segment is expected to dominate the market with a 61.02% share, driven by the extensive distribution networks established by resellers, distributors, and system integrators, enabling UPS manufacturers to penetrate a broader customer base across commercial, industrial, and residential sectors. Indirect channels also offer significant value-added services, including installation, system integration, maintenance, and after-sales support, which are particularly attractive to end-users seeking turnkey power solutions. Furthermore, strategic partnerships between global UPS manufacturers and regional distributors enhance product accessibility, improve service reach, and strengthen market penetration across both developed and emerging economies.

Major Players

ABB Ltd (Switzerland), Schneider Electric (France), Huawei Technologies (China), Vertiv Group Corp. (U.S.), Eaton (U.S.), COMEX (Egypt), Delta Electronics (Taiwan), EL Fateh Est. (Egypt), EPS Electric (Egypt), FOX ELECTRONICS POWER (Egypt), IPS Power (Egypt), Mitsubishi Electric Corporation (Japan), Legrand (France), Phoenix Contact (Germany), Riello UPS (Italy), SALICRU S.A. (Spain), Sentafe (Egypt), Socomec Group (France), Tescom Elektronik A.Ş. (Turkey)among others.

Latest Developments in Global Uninterruptible Power Supply (UPS) Market

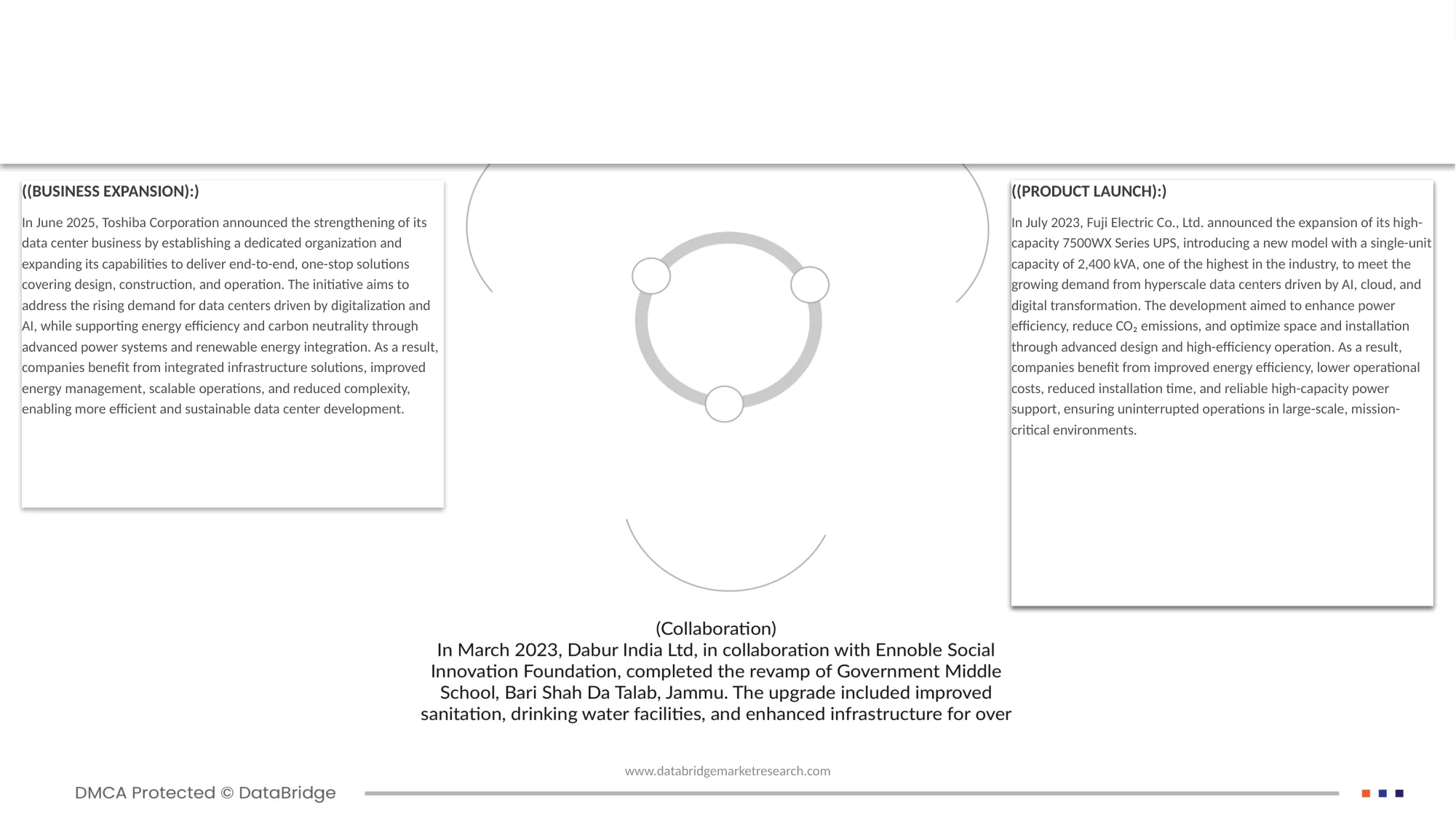

- In May 2025, ABB has expanded its PowerValue UPS product range for enterprise data centers, offering modular, efficient, and reliable power backup solutions. The new UPS systems are designed to enhance critical IT infrastructure, improve safety, and reduce energy consumption. This UPS expansion strengthens ABB’s position in the global data center market and drives growth in critical power solutions.

- In November 2025, Schneider Electric and Digital Realty have entered a $373 million Supply Capacity Agreement to secure guaranteed capacity for Uninterruptible Power Supplies (UPS), low‑voltage switchgear, and prefabricated skids to meet rising demand for digital infrastructure. The pact aims to accelerate power deployment and supply‑chain resilience amid surging capacity needs driven by AI and cloud growth, this is expected to strengthen company portfolio.

- In September 2025, Huawei Digital Power showcased its strategy to accelerate high quality, innovative data center construction for the AI era at Huawei Connect 2025, emphasizing integration of digital and power technologies to build reliable, agile, and sustainable AI ready infrastructure. The company highlighted modular design, prefabricated solutions, and advanced power supply and thermal management innovations to meet the explosive growth in AI computing demands. This innovative approach strengthens Huawei’s role in the global data center ecosystem and enhances its credibility in delivering comprehensive, energy efficient infrastructure.

As per Data Bridge Market Research analysis:

Geographically, the countries covered in the global uninterruptible power supply (UPS) Market report are North America, Europe, Asia-Pacific, Middle East and Africa, South America. Europe is further segmented into Italy, U.K., Germany, France, Spain, Belgium, Netherlands, Poland, Russia, Denmark, Sweden, Switzerland, Turkey and Rest of Europe. The Asia-Pacific is further segmented into China, Japan, South Korea, Vietnam, Indonesia, India, Philippines, Thailand, Singapore, New Zealand, Malaysia, Australia, Rest of Asia-Pacific. The North America is further segmented into U.S., Canada, and Mexico. The South America is further segmented into Brazil, Argentina, Colombia, Chile, Peru, Venezuela, Ecuador, Uruguay, Paraguay, Bolivia, and rest of South America. The Middle East and Africa is further segmented into South Africa, Saudi Arabia, UAE, Oman, Qatar, Kuwait, and Rest of Middle East and Africa.

North America is the dominating Region in global Uninterruptible power supply (UPS) Market

North America dominates the global uninterruptible power supply (UPS) market due to the strong presence of data centers, advanced IT infrastructure, and increasing demand for reliable backup power solutions across commercial, industrial, and healthcare sectors. The region's leadership is further supported by rapid cloud computing adoption, growing investments in digital transformation, and stringent regulations regarding power reliability. Additionally, the expansion of hyperscale data centers and rising demand for uninterrupted power in mission-critical applications continue to drive market growth across the United States and Canada.

Asia-Pacific is expected to be the fastest growing region in global Uninterruptible power supply (UPS) Market

Asia-Pacific is expected to be the fastest-growing region in the global uninterruptible power supply (UPS) market due to rapid industrialization, expanding data center infrastructure, increasing digital transformation initiatives, and growing investments in telecommunications and cloud computing. Rising demand for reliable power backup systems across countries such as China, India, Japan, and South Korea is further driving market growth. Additionally, increasing adoption of smart manufacturing technologies and government support for critical infrastructure development are accelerating UPS deployment throughout the region..

For more detailed information about the global uninterruptible power supply (UPS) market report, click here – https://www.databridgemarketresearch.com/reports/global-uninterruptible-power-supply-ups-market