The increasing prevalence of obesity and lifestyle-related disorders in India is a major structural driver of the sleep apnea market. Rapid urbanization, sedentary occupations, long working hours, unhealthy dietary patterns, and declining physical activity levels have accelerated the incidence of obesity, diabetes, hypertension, and cardiovascular diseases. Obesity remains a clinically established risk factor for obstructive sleep apnea (OSA), as excess adipose tissue around the neck and upper airway contributes to airway collapse during sleep, increasing the probability of sleep-disordered breathing. Data from the National Family Health Survey (NFHS-5, October 2021) highlighted a notable rise in overweight and obesity prevalence, particularly in urban populations. In June 2023, The Economic Times reported national obesity estimates of ~28.6% (generalised) and ~39.5% (abdominal), while September 2025 insights from UNICEF indicated that adult overweight and obesity nearly doubled among both men and women over recent years.

Simultaneously, the growing burden of cardiometabolic disorders has strengthened clinical awareness of sleep apnea as a critical comorbidity. A June 2023 study published in The Lancet, funded by the Indian Council of Medical Research and the Ministry of Health and Family Welfare, reported that over 101 million Indians (11.4%) are living with diabetes, with an additional 136 million classified as pre-diabetic, with high prevalence observed in states such as Goa, Puducherry, and Kerala. In March 2025, the Government of India strengthened NP-NCD initiatives to standardize diabetes and hypertension management nationwide. As screening for OSA becomes increasingly integrated into routine care for high-risk cardiometabolic patients, the expanding lifestyle disease burden is expected to sustain long-term demand for sleep apnea diagnostic and therapeutic solutions across urban and semi-urban India.

Access Full Report @ https://www.databridgemarketresearch.com/reports/india-sleep-apnea-market

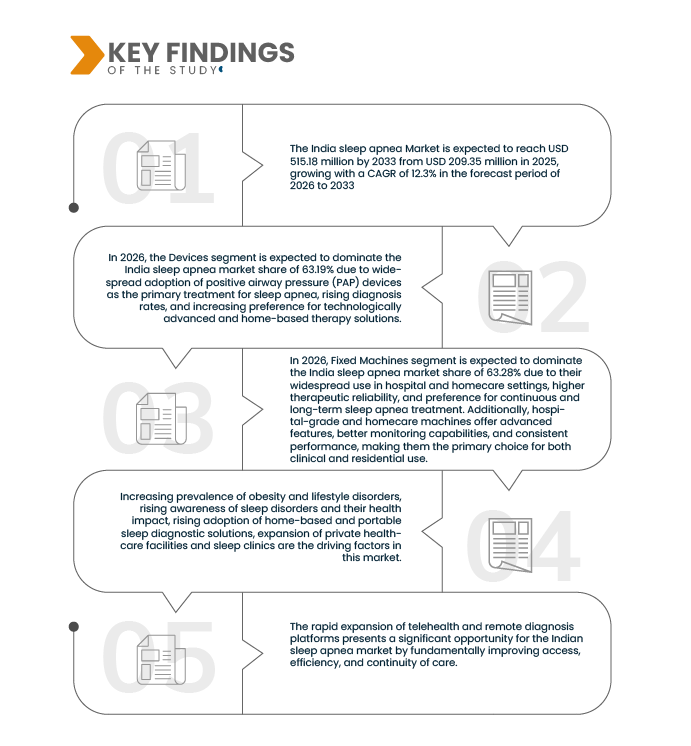

Data Bridge market research analyzes that India Sleep Apnea Market is expected to reach USD 515.18 million by 2033 from USD 209.35 million in 2025, growing with a substantial CAGR of 12.3% in the forecast period of 2025 to 2033.

Key Findings of the Study

Emerging Telehealth and Remote Diagnosis Platforms

The rapid expansion of telehealth and remote diagnosis platforms presents a significant opportunity for the Indian sleep apnea market by fundamentally improving access, efficiency, and continuity of care. Telemedicine services are increasingly incorporating sleep health into their portfolios, enabling virtual specialist consultations, preliminary risk assessments, interpretation of home sleep tests, and structured follow-up without repeated in-person visits. This model mitigates geographic and infrastructure constraints, particularly in semi-urban and rural regions where access to sleep laboratories and trained sleep medicine specialists remains limited. Remote platforms further facilitate asynchronous transmission of data from portable sleep monitors, pulse oximeters, and wearable devices, enabling clinicians to deliver timely, data-driven management decisions.

Policy and digital health infrastructure developments are accelerating adoption. In August 2023, the Government of India strengthened remote care delivery through the Telemedicine Practice Guidelines (TPG) 2023, formalizing clinical and operational standards for virtual consultations. In June 2025, eSanjeevani integrated remote monitoring capabilities to support virtual management of sleep-related conditions in underserved regions. Additionally, the Ayushman Bharat Digital Mission and the Unified Health Interface enhanced interoperability of digital health records, with over 49 million records linked to Ayushman Bharat Health Accounts (ABHA) by early 2025. Collectively, these advancements are expected to improve early detection, strengthen therapy adherence, reduce overall cost of care, and expand the addressable market for integrated sleep apnea diagnostics and long-term management solutions in India.

Report Scope and Market Segmentation

|

Report Metric

|

Details

|

|

Forecast Period

|

2026 to 2033

|

|

Base Year

|

2025

|

|

Historic Years

|

2024 (Customizable to 2018-2023)

|

|

Quantitative Units

|

Revenue in USD billion

|

|

Segments Covered

|

By Product Type (Devices, Consumables & Accessories, Oral Appliances

Others), By Machinery Type (Fixed Machines, Portable Machines), By Function (Basic PAP Therapy, Smart PAP (Auto-Titration), Connected PAP, Remote Monitoring, Integrated Oxygen Therapy, Humidification-Enabled PAP, Alarm-Enabled Devices, Others), Application (Obstructive Sleep Apnea, Central Sleep Apnea, Complex Sleep Apnea Syndrome, Others), Age Group (Adult, Geriatric, Pediatric), End User (Hospitals, Home Care Settings, Sleep Laboratories & Clinics, Ambulatory Surgical Centers, Others), Distribution Channel (Indirect, Direct)

|

|

Countries Covered

|

|

|

Market Players Covered

|

|

|

Data Points Covered in the Report

|

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework.

|

Segment Analysis

The India Sleep Apnea market is segmented into six segments based on product type, machinery type, function, application, age group, end user and distribution channel.

- On the basis of product type, the market is segmented Devices, Consumables & Accessories, Oral Appliances, and Others.

In 2026, the Devices segment is expected to dominate the market

In 2026, the Devices segment is expected to dominate the India sleep apnea market share of 63.19% due to widespread adoption of positive airway pressure (PAP) devices as the primary treatment for sleep apnea, rising diagnosis rates, and increasing preference for technologically advanced and home-based therapy solutions.

- On the basis of Machinery Type, the market is segmented into Fixed Machines and Portable Machines.

In 2026, the Fixed Machines segment is expected to dominate the market

In 2026, Fixed Machines segment is expected to dominate the India sleep apnea market share of 63.28% due to their widespread use in hospital and homecare settings, higher therapeutic reliability, and preference for continuous and long-term sleep apnea treatment. Additionally, hospital-grade and homecare machines offer advanced features, better monitoring capabilities, and consistent performance, making them the primary choice for both clinical and residential use.

- On the basis of Function, the market is segmented into Basic PAP Therapy, Smart PAP (Auto-Titration), Connected PAP, Remote Monitoring, Integrated Oxygen Therapy, Humidification-Enabled PAP, Alarm-Enabled Devices, and Others.

In 2026, the Basic PAP Therapy segment is expected to dominate the market

In 2026, the Basic PAP Therapy segment is anticipated to dominate the India sleep apnea market share of 34.66% due to its proven clinical effectiveness, wide availability, and cost-effectiveness compared to advanced therapy options. Additionally, basic PAP devices are commonly prescribed as the first line of treatment for sleep apnea, especially in newly diagnosed patients, which supports their continued high adoption.

- On the basis of Application, the market is segmented into Obstructive Sleep Apnea, Central Sleep Apnea, Complex Sleep Apnea Syndrome, and Others.

In 2026, the Obstructive Sleep Apnea segment is expected to dominate the market

In 2026, the Obstructive Sleep Apnea segment is anticipated to dominate the India sleep apnea market share of 72.85% due to its significantly higher prevalence compared to other sleep apnea types, increasing awareness and diagnosis rates, and strong demand for PAP devices and related accessories as the primary treatment approach. Additionally, lifestyle factors such as obesity, sedentary habits, and aging population trends further support the dominance of this segment.

- On the basis of Age Group, the market is segmented into Adult, Geriatric, and Pediatric.

In 2026, the adult segment is expected to dominate the market

In 2026, the adult segment is anticipated to dominate the India sleep apnea market share of 64.86% due to the higher prevalence of sleep apnea among the working-age population, increased exposure to lifestyle risk factors such as obesity, stress, and sedentary habits, and greater diagnosis rates driven by rising health awareness and access to sleep diagnostic services.

- On the basis of End User, the market is segmented into Hospitals, Home Care Settings, Sleep Laboratories & Clinics, Ambulatory Surgical Centers, and Others.

In 2026, the Hospitals segment is expected to dominate the market

In 2026, the Hospitals segment is anticipated to dominate the India sleep apnea market share of 36.76% due to the availability of advanced diagnostic and treatment infrastructure, higher patient inflow for sleep disorder evaluation, and the presence of skilled healthcare professionals for accurate diagnosis and management of sleep apnea. Additionally, hospitals serve as the primary point of care for moderate to severe cases, supporting their leading market share.

- On the basis of Distribution Channel, the market is segmented into Direct and indirect.

In 2026, the Direct segment is expected to dominate the market

In 2026, the Direct segment is anticipated to dominate the India sleep apnea market share of 61.97% due to stronger manufacturer-to-customer engagement, better pricing control, availability of customized solutions, and direct technical support and after-sales services, which are particularly important for sleep apnea devices and therapy equipment.

Major Players

RESMED INC. (U.S.), PHILIPS RESPIRONICS (KONINKLIJKE PHILIPS N.V.) (Netherlands), ZOLL Medical Corporation (U.S.), Fisher & Paykel Healthcare Limited (New Zealand), Yuwell - Jiangsu Yuyue Medical Equipment & Supply Co., Ltd. (China) among others.

Latest Developments in India Sleep Apnea Market

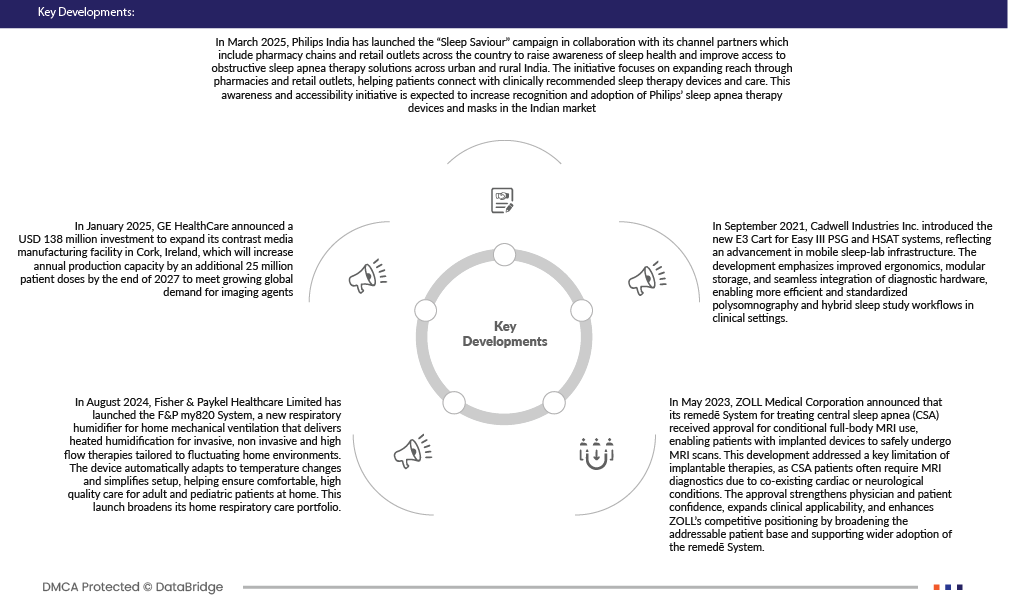

- In March 2025, Philips India has launched the “Sleep Saviour” campaign in collaboration with its channel partners which include pharmacy chains and retail outlets across the country to raise awareness of sleep health and improve access to obstructive sleep apnea therapy solutions across urban and rural India. The initiative focuses on expanding reach through pharmacies and retail outlets, helping patients connect with clinically recommended sleep therapy devices and care. This awareness and accessibility initiative is expected to increase recognition and adoption of Philips’ sleep apnea therapy devices and masks in the Indian market.

- In May 2023, ZOLL Medical Corporation announced that its remedē System for treating central sleep apnea (CSA) received approval for conditional full-body MRI use, enabling patients with implanted devices to safely undergo MRI scans. This development addressed a key limitation of implantable therapies, as CSA patients often require MRI diagnostics due to co-existing cardiac or neurological conditions. The approval strengthens physician and patient confidence, expands clinical applicability, and enhances ZOLL’s competitive positioning by broadening the addressable patient base and supporting wider adoption of the remedē System.

- In August 2024, Fisher & Paykel Healthcare Limited has launched the F&P my820 System, a new respiratory humidifier for home mechanical ventilation that delivers heated humidification for invasive, non invasive and high flow therapies tailored to fluctuating home environments. The device automatically adapts to temperature changes and simplifies setup, helping ensure comfortable, high quality care for adult and pediatric patients at home. This launch broadens its home respiratory care portfolio.

- In September 2021, Cadwell Industries Inc. introduced the new E3 Cart for Easy III PSG and HSAT systems, reflecting an advancement in mobile sleep-lab infrastructure. The development emphasizes improved ergonomics, modular storage, and seamless integration of diagnostic hardware, enabling more efficient and standardized polysomnography and hybrid sleep study workflows in clinical settings.

- In January 2025, GE HealthCare announced a USD 138 million investment to expand its contrast media manufacturing facility in Cork, Ireland, which will increase annual production capacity by an additional 25 million patient doses by the end of 2027 to meet growing global demand for imaging agents

For more detailed information about the India sleep apnea Market report, click here – https://www.databridgemarketresearch.com/reports/india-sleep-apnea-market