Africa's data center facility market is witnessing significant growth due to increasing investments by global hyperscale cloud providers, rising demand for data localization, and the rapid expansion of digital services. Major technology companies are strengthening their presence across the continent to support cloud computing, artificial intelligence (AI), and digital transformation initiatives. For example, Microsoft and G42 announced a USD 1 billion investment in a data center and cloud region project in Kenya to expand cloud services in East Africa. In addition, the International Finance Corporation (IFC), a member of the World Bank Group, committed USD 100 million to Raxio Group to accelerate the development of data centres across multiple African countries. Governments and enterprises are also placing greater emphasis on storing data within national borders to improve security, regulatory compliance, and data sovereignty.

Access Full Report @ https://www.databridgemarketresearch.com/reports/sub-saharan-africa-data-center-facility-market

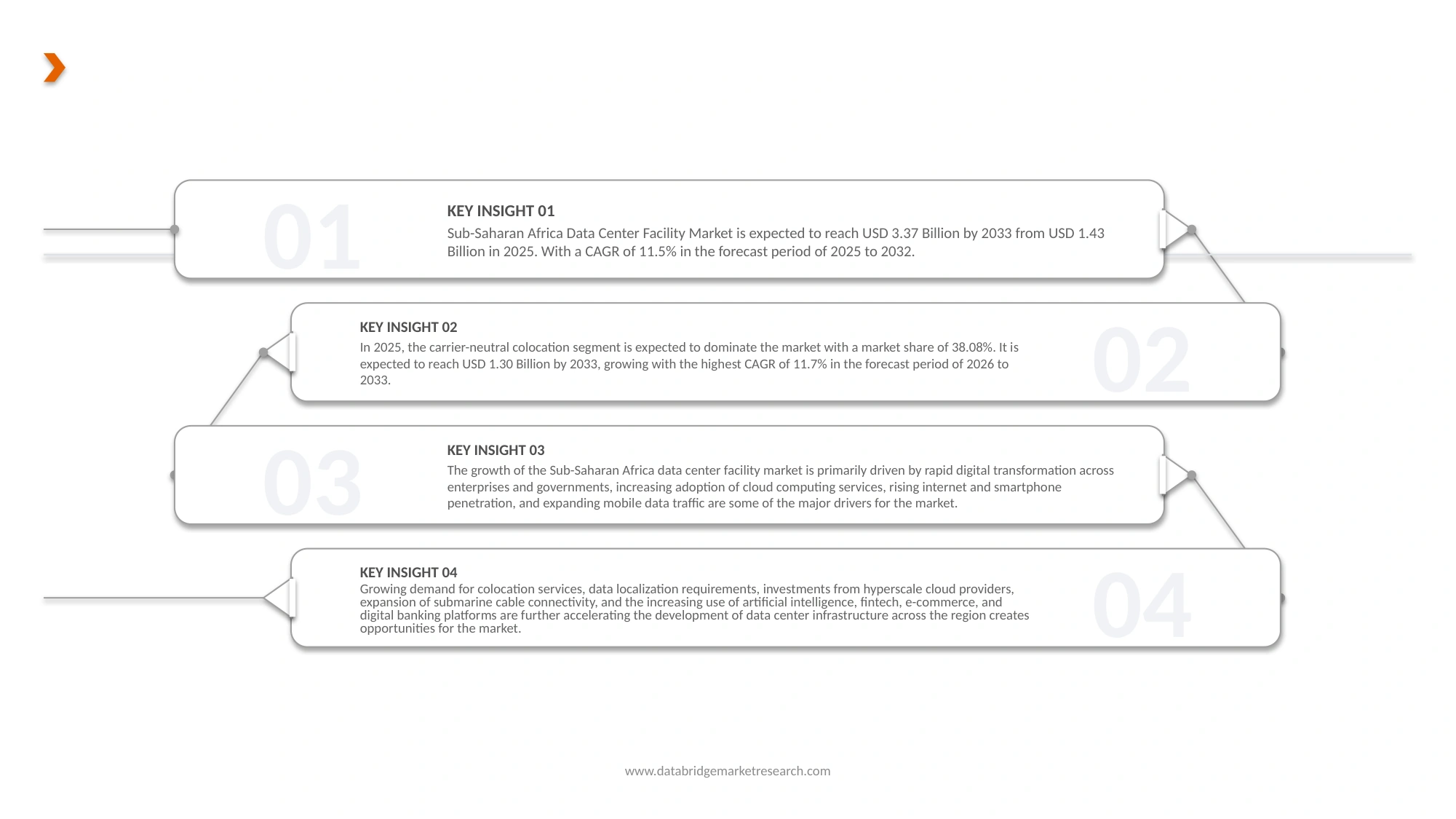

Data Bridge market research analyzes that the Sub-Saharan Africa Data Center Facility Market is expected to reach USD 3.37 billion by 2033 from USD 1.43 billion in 2025, growing at a substantial CAGR of 11.5% in the forecast period of 2026 to 2033.

Key Findings of the Study

Rising Demand for Data Localization

The rising demand for data localization is becoming a significant driver of the Africa Data Center Facility Market as governments, businesses, and organizations seek greater control over how data is stored, managed, and protected. With the rapid growth of digital banking, fintech, e-commerce, healthcare, telecommunications, and e-government services, large volumes of sensitive data are being generated across the continent. To strengthen cybersecurity, protect citizen information, and ensure regulatory compliance, several African countries have introduced data protection laws and frameworks that encourage or require certain data to be stored within national borders. At the same time, businesses are increasingly looking for faster data access, lower latency, and improved operational reliability, which local data centers can provide. This shift is reducing dependence on overseas data storage facilities and creating strong demand for domestic data center infrastructure.

Report Scope and Market Segmentation

|

Report Metric

|

Details

|

|

Forecast Period

|

2026 to 2033

|

|

Base Year

|

2025

|

|

Historic Years

|

2024 (Customizable to 2018-2023)

|

|

Quantitative Units

|

Revenue in USD billion

|

|

Segments Covered

|

By Product Type (Carrier-Neutral Colocation, Hyperscale Data Centers, Enterprise / Private Data Centers, Telecom Core Data Centers, Sovereign / Government Data Centers, and Edge Telecom / Containerized Data Centers), By Tier Standards (Tier III, Tier IV, Tier II, and Tier I), By Design (Traditional and Modular), By PUE Outlook (5–2.0, 1.2–1.5, >2.0, and <1.2), By Connectivity (Carrier-Neutral Facilities, Carrier-Owned Facilities, Internet Exchange Connected Facilities, Submarine Cable Landing Station Connected Facilities), By Deployment Model (On-Premise and Cloud), By Ownership Model (Owned & Operated, Leased, Joint Venture, Build-to-Suit, By Power Capacity (Below 1 MW, 1–5 MW, 5–20 MW, 20–50 MW, 50–100 MW, 100 MW+ (AI / Hyperscale Campuses)), By Investment Type (New Builds, Expansion, Retrofit, M&A Activity), By Sustainability / Energy Profile (Renewable-Powered Data Centers, Green Data Centers (LEED Certified), Carbon-Neutral Data Centers, Net-Zero Data Centers), By End User (IT and Telecommunication, Banking, Financial Services and Insurance (BFSI), Government and Defense, Retail & E-Commerce, Healthcare and Life Sciences, Manufacturing, Power and Energy, Transportation, Media and Entertainment, Research & Academic, Education, Semiconductor, Others)

|

|

Countries Covered

|

Sub-Saharan Africa

|

|

Market Players Covered

|

· Digital Realty Trust (U.S.)

· NTT DATA Inc. (Japan)

· Equinix Inc. (U.S.)

· Africa Data Centres (South Africa)

· RACK CENTRE (Nigeria)

· Paratus Africa (Namibia)

· Microsoft Corporation (U.S.)

· Huawei Technologies Africa (Pty) Ltd (China)

· Raxio Group (Uganda)

· iXAfrica Data Centre (Kenya)

· Vantage Data Centers (U.S.)

· Onix Data Centres Ltd (Nigeria)

· Digital Parks Africa (South Africa)

· Wingu Africa (Tanzania)

· N+ONE DATACENTERS (South Africa)

· ST DIGITAL (South Africa)

· PAIX Data Centres (Kenya)

· Open Access Data Centres (U.K.)

|

|

Data Points Covered in the Report

|

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis.

|

Segment Analysis

The Sub-Saharan Africa Data Center Facility Market is categorized into twelve notable segments based on the product type, tier standards, design, PUE outlook, connectivity, deployment model, redundancy level, ownership model, power capacity, investment type, sustainability/energy profile, and end user.

- On the basis of product type, the South Africa data center facility market is segmented into carrier-neutral colocation, hyperscale data centers, enterprise/private data centers, telecom core data centers, sovereign/government data centers, and edge telecom/containerized data centers.

In 2026, the carrier-neutral colocation segment is expected to dominate the market

In 2026, the carrier-neutral colocation segment is expected to dominate with 38.08% market share, while the edge telecom/containerized data centers segment is projected to register the highest CAGR of 12.5% during the forecast period of 2026 to 2033, driven by increasing demand for low-latency computing, expansion of 5G networks, rural connectivity initiatives, and rapid deployment of modular edge infrastructure across emerging digital markets.

- On the basis of tier standards, the South Africa data center facility market is segmented into Tier III, Tier IV, Tier II, and Tier I.

In 2026, the Tier III segment is expected to dominate the market.

In 2026, the Tier III segment is expected to dominate with 65.20% market share, while the Tier IV segment is projected to witness the highest CAGR of 11.9% during the forecast period of 2026 to 2033, supported by growing enterprise demand for mission-critical infrastructure, higher uptime requirements, and increasing investments from hyperscale cloud providers.

- On the basis of design, the South Africa data center facility market is segmented into traditional and modular. In 2026, the traditional segment is expected to dominate with 82.52% market share, while the modular segment is projected to grow at the highest CAGR of 11.9% during the forecast period of 2026 to 2033, driven by faster deployment timelines, lower upfront investment requirements, and increasing adoption in remote and rapidly developing locations.

- On the basis of PUE outlook, the South Africa data center facility market is segmented into 1.5–2.0, 1.2–1.5, >2.0, and <1.2. In 2026, the 1.5–2.0 PUE segment is expected to dominate with 47.12% market share, while the <1.2 PUE segment is projected to register the highest CAGR of 12.3% during the forecast period of 2026 to 2033, driven by the adoption of advanced cooling technologies, energy-efficient facility designs, and sustainability-focused investments.

- On the basis of connectivity, the South Africa data center facility market is segmented into carrier-neutral facilities, carrier-owned facilities, internet exchange connected facilities, and submarine cable landing station connected facilities. In 2026, the carrier-neutral facilities segment is expected to dominate with 47.65% market share, while the same segment is also projected to register the highest CAGR of 12.0% during the forecast period of 2026 to 2033, owing to rising interconnection demand, multi-cloud connectivity, and increasing investments from colocation providers.

- On the basis of deployment model, the South Africa data center facility market is segmented into on-premise and cloud. In 2026, the on-premise segment is expected to dominate with 56.74% market share, while the cloud segment is projected to grow at the highest CAGR of 11.9% during the forecast period of 2026 to 2033, driven by accelerating cloud migration, digital transformation initiatives, and increasing adoption of hybrid IT infrastructure.

- On the basis of redundancy level, the South Africa data center facility market is segmented into N+1, 2N, N, and 2N+1. In 2026, the N+1 segment is expected to dominate with 42.70% market share, while the 2N+1 segment is projected to record the highest CAGR of 12.3% during the forecast period of 2026 to 2033, supported by growing demand for fault-tolerant infrastructure in hyperscale and financial service facilities.

- On the basis of ownership model, the South Africa data center facility market is segmented into owned & operated, leased, joint venture, and build-to-suit. In 2026, the owned & operated segment is expected to dominate with 44.20% market share, while the joint venture segment is projected to witness the highest CAGR of 12.2% during the forecast period of 2026 to 2033, driven by strategic partnerships between international investors, infrastructure developers, and regional operators.

- On the basis of power capacity, the South Africa data center facility market is segmented into 5–20 MW, 20–50 MW, 1–5 MW, 50–100 MW, below 1 MW, and 100 MW+ (AI/hyperscale campuses). In 2026, the 5–20 MW segment is expected to dominate with 31.82% market share, while the 100 MW+ (AI/hyperscale campuses) segment is projected to register the highest CAGR of 12.5% during the forecast period of 2026 to 2033, supported by increasing hyperscale investments, AI workloads, and next-generation cloud infrastructure development.

- On the basis of investment type, the South Africa data center facility market is segmented into new builds, expansion, retrofit, and M&A activity. In 2026, the new builds segment is expected to dominate with 42.06% market share, while the expansion segment is projected to grow at the highest CAGR of 11.9% during the forecast period of 2026 to 2033, driven by increasing capacity upgrades, rising occupancy rates, and continued demand from cloud service providers.

- On the basis of sustainability/energy profile, the South Africa data center facility market is segmented into renewable-powered data centers, green data centers (LEED certified), carbon-neutral data centers, and net-zero data centers. In 2026, the renewable-powered data centers segment is expected to dominate with 36.59% market share, while the carbon-neutral data centers segment is projected to witness the highest CAGR of 12.0% during the forecast period of 2026 to 2033, driven by sustainability regulations, renewable energy adoption, and corporate ESG commitments.

- On the basis of end user, the South Africa data center facility market is segmented into IT and telecommunication, banking, financial services and insurance (BFSI), government and defense, retail & e-commerce, healthcare and life sciences, manufacturing, power and energy, transportation, media and entertainment, research & academic, education, semiconductor. In 2026, the IT and telecommunication segment is expected to dominate with 27.89% market share, while the retail & e-commerce segment is projected to register the highest CAGR of 13.4% during the forecast period of 2026 to 2033, driven by rapid digital commerce growth, increasing online payment adoption, cloud-based retail platforms, and expanding digital consumer services across Sub-Saharan Africa.

Major Players

- Digital Realty Trust (U.S.)

- NTT DATA Inc. (Japan)

- Equinix Inc. (U.S.)

- Africa Data Centres (South Africa)

- RACK CENTRE (Nigeria)

- Paratus Africa (Namibia)

- Microsoft Corporation (U.S.)

- Huawei Technologies Africa (Pty) Ltd (China)

- Raxio Group (Uganda)

- iXAfrica Data Centre (Kenya)

- Vantage Data Centers (U.S.)

- Onix Data Centres Ltd (Nigeria)

- Digital Parks Africa (South Africa)

- Wingu Africa (Tanzania)

- N+ONE DATACENTERS (South Africa)

- ST DIGITAL (South Africa)

- PAIX Data Centres (Kenya)

- Open Access Data Centres (U.K.)

Market Developments

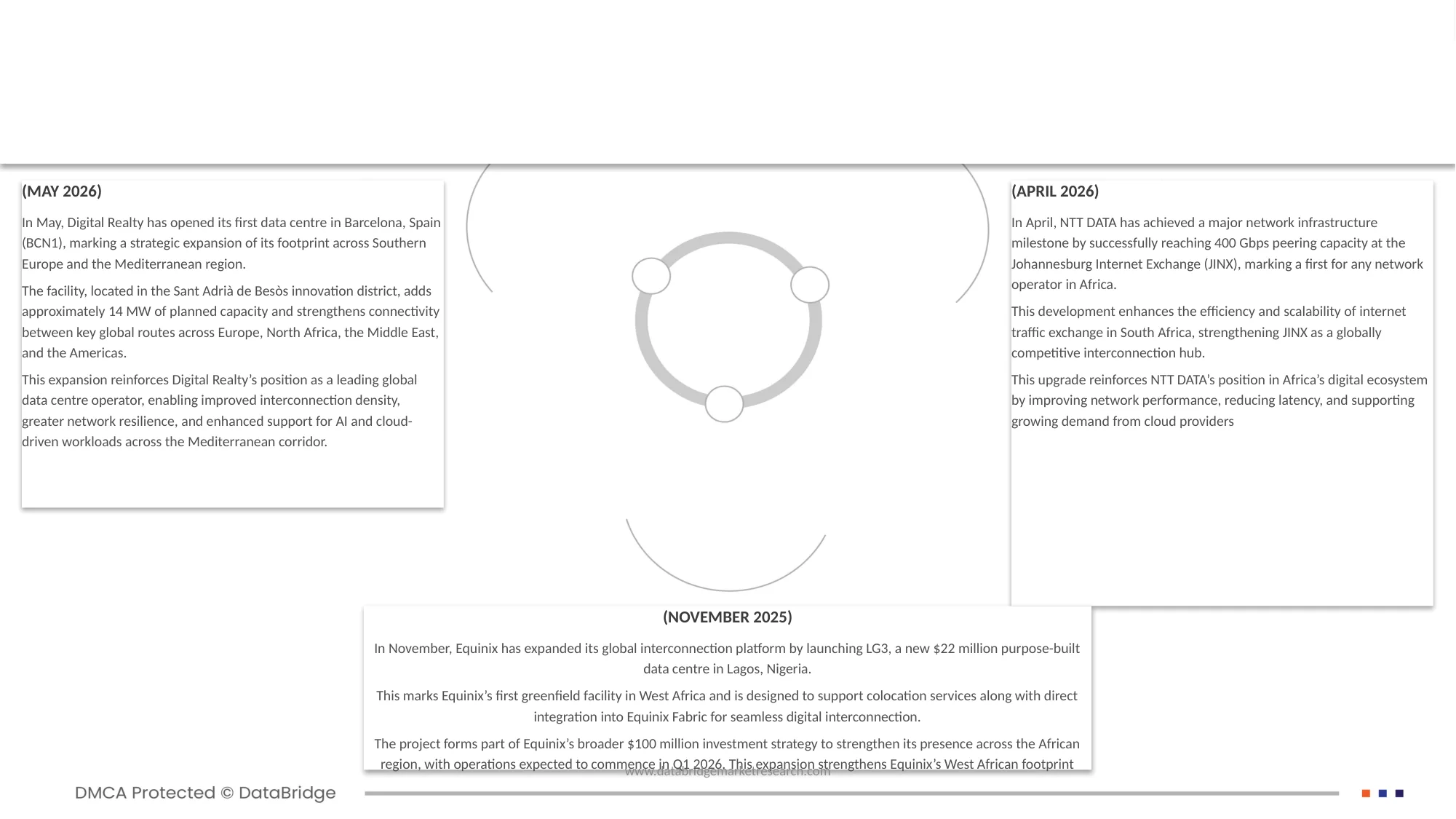

- In May 2026, Digital Realty has opened its first data centre in Barcelona, Spain (BCN1), marking a strategic expansion of its footprint across Southern Europe and the Mediterranean region. The facility, located in the Sant Adrià de Besòs innovation district, adds approximately 14 MW of planned capacity and strengthens connectivity between key global routes across Europe, North Africa, the Middle East, and the Americas. This expansion reinforces Digital Realty’s position as a leading global data centre operator, enabling improved interconnection density, greater network resilience, and enhanced support for AI and cloud-driven workloads across the Mediterranean corridor.

- In April 2026, NTT DATA has achieved a major network infrastructure milestone by successfully reaching 400 Gbps peering capacity at the Johannesburg Internet Exchange (JINX), marking a first for any network operator in Africa. This development enhances the efficiency and scalability of internet traffic exchange in South Africa, strengthening JINX as a globally competitive interconnection hub. This upgrade reinforces NTT DATA’s position in Africa’s digital ecosystem by improving network performance, reducing latency, and supporting growing demand from cloud providers

- In November 2025, Equinix has expanded its global interconnection platform by launching LG3, a new USD 22 million purpose-built data centre in Lagos, Nigeria. This marks Equinix’s first greenfield facility in West Africa and is designed to support colocation services along with direct integration into Equinix Fabric for seamless digital interconnection. The project forms part of Equinix’s broader USD 100 million investment strategy to strengthen its presence across the African region, with operations expected to commence in Q1 2026. This expansion strengthens Equinix’s West African footprint.

- In February 2026, Cassava Technologies has received a key regulatory approval milestone in South Africa for the proposed sale of a stake in its Africa Data Centres (ADC) business to STANLIB Infrastructure Investments, a unit backed by Standard Bank and Liberty Group. The approval from the Competition Tribunal allows STANLIB to acquire joint control of ADC, supporting its broader investment strategy in Africa’s digital infrastructure sector. This development accelerates capital inflow into Africa Data Centres.

- In May 2026, Digital Parks Africa expanded its global connectivity capabilities by bringing Tier 1 carrier Cogent Communications into its Samrand data centre in South Africa. The partnership provides DPA customers with direct access to one of the world’s largest IP backbone networks, enabling improved global routing, traffic exchange, and low-latency connectivity across more than 300 business markets in 57 countries. This development strengthens DPA’s position as a leading interconnection hub in Africa.

As per Data Bridge Market Research analysis:

Geographically, the countries covered in the Sub-Saharan Africa Data Center Facility Market report are South Africa, Nigeria, Kenya, Ivory Coast, Senegal, Tanzania, Uganda, Zambia, Togo, Benin, Rest of Sub-Saharan Africa.

South Africa is the dominating state in Sub-Saharan Africa Data Center Facility Market

South Africa dominated the Sub-Saharan Africa data center facility market and accounted for the largest revenue share of 20.50% in 2025, supported by its well-established digital infrastructure, strong connectivity ecosystem, extensive submarine cable networks, and concentration of hyperscale and colocation data center investments. The country benefits from a mature telecommunications sector, growing cloud adoption, favorable business environment, and increasing demand for data localization, making it the primary hub for data center development and digital services across the region.

Nigeria Africa Data Center Facility Market Insight

Nigeria is the fastest-growing state in data center market in Sub-Saharan Africa, driven by rapid digitalization, strong population growth, expanding internet penetration, and increasing adoption of cloud services. The country's thriving fintech, e-commerce, telecommunications, and digital banking sectors are generating significant demand for colocation and hyperscale infrastructure. Growing investments from global and regional data center operators, alongside increasing data localization requirements, continue to strengthen Nigeria’s position as a major digital infrastructure hub in West Africa.

For more detailed information about theSub-Saharan Africa Data Center Facility Market report, click here – https://www.databridgemarketresearch.com/reports/sub-saharan-africa-data-center-facility-market