The demand for energy-efficient HVAC systems in Poland is growing rapidly, driven by strict EU energy regulations, rising energy costs, and the country’s aging, inefficient building stock, much of which predates modern insulation standards. Policies such as the revised EPBD and EED are accelerating large-scale thermal modernization, pushing adoption of heat pumps, smart ventilation, and low-emission heating solutions, while government programs like “Clean Air” further support the replacement of fossil-fuel-based systems. Reports from 2025 highlight that buildings account for around 40% of Poland’s energy use and may require trillions of PLN in upgrades to meet climate targets, with EU pressure also phasing out incentives for standalone fossil-fuel boilers. Overall, regulatory mandates, decarbonization goals, and renovation initiatives are collectively driving strong growth in energy-efficient HVAC technologies across the country.

Access Full Report @ https://www.databridgemarketresearch.com/reports/poland-hvac-market

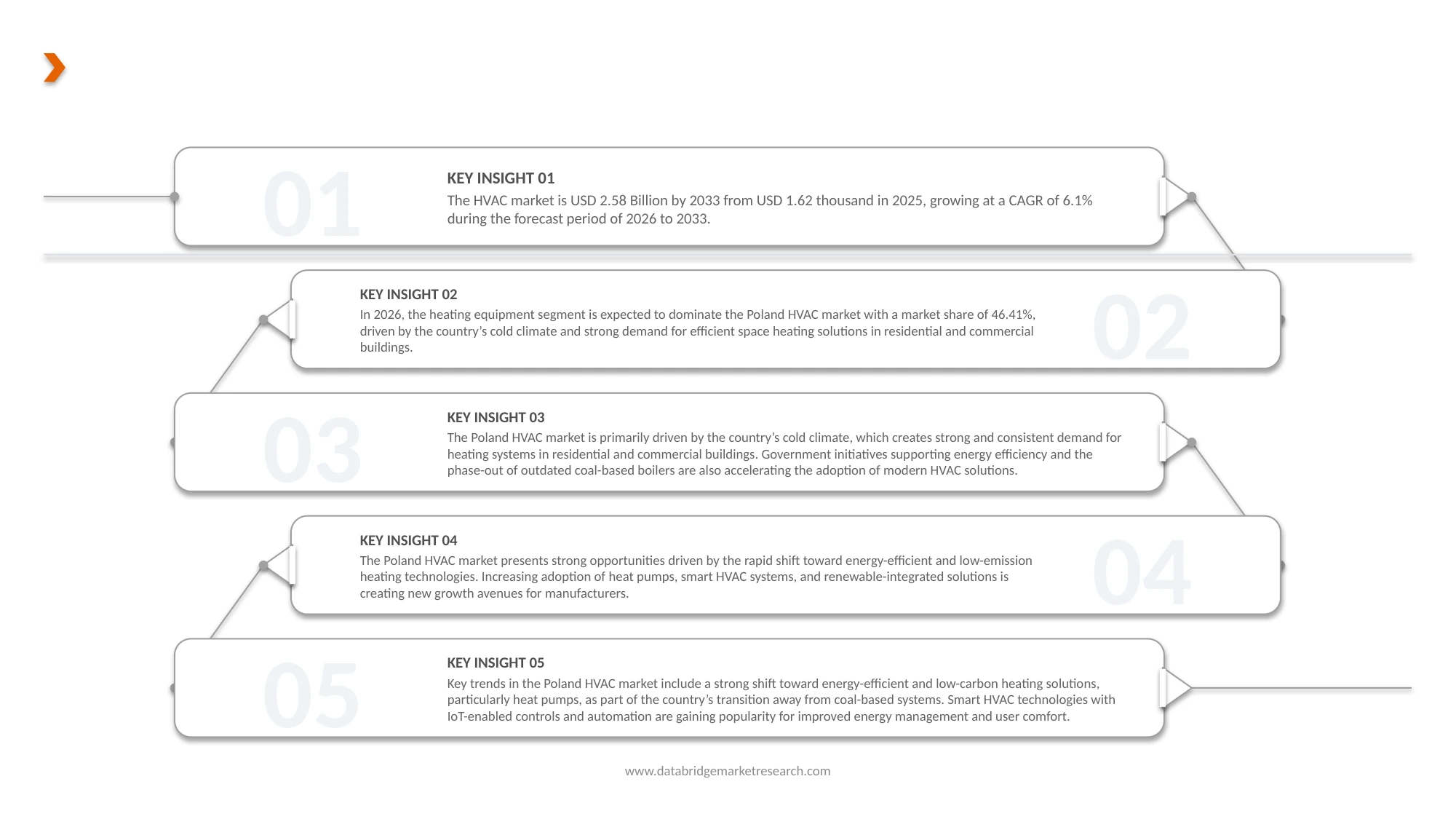

Data Bridge Market Research analyzes that Poland HVAC Market is expected to reach USD 2.58 billion by 2033 from USD 1.62 billion in 2025, growing with a substantial CAGR of 6.1% in the forecast period of 2026 to 2033.

Key Findings of the Study

Growth In Construction, Infrastructure, And Green Building Projects

The growth in construction, infrastructure, and green building projects is significantly driving demand for HVAC systems in Poland, as rising investments in commercial offices, industrial facilities, renewable energy infrastructure, and sustainable urban development require advanced heating, ventilation, and cooling solutions. Increasing focus on net-zero buildings, EU-aligned sustainability standards, and certifications such as LEED and BREEAM is accelerating adoption of technologies like heat pumps, smart ventilation, building automation, and integrated energy systems across new developments. Recent projects, including Skanska’s net-zero Nowy Rynek C office in Poznań with heat pumps and AI-driven building management, SPIE’s HVAC installations at Daikin’s manufacturing complex, and Eiffage’s sustainable Frontex headquarters, highlight how large-scale green and industrial developments are embedding energy-efficient HVAC solutions. Additionally, renewable energy and infrastructure initiatives such as photovoltaic farms by Budimex, biomass-based district heating projects by Unibep, and Poland’s updated green bond framework are further strengthening long-term demand for modern, low-carbon HVAC technologies across the country.

Report Scope and Market Segmentation

|

Report Metric

|

Details

|

|

Forecast Perio

|

2026 to 2033

|

|

Base Year

|

2025

|

|

Historic Year

|

2024 (Customizable 2018-2024)

|

|

Quantitative Units

|

Revenue in USD billion

|

|

Segments Covered

|

By Product Type (Heating Equipment, Air Conditioning Systems, Ventilation Equipment, Refrigeration Systems, and Others), By End User Industry (Residential, Commercial, Industrial, and Others), By Technology (Conventional HVAC Systems, Energy-Efficient HVAC Systems, Smart HVAC Systems (IoT-Enabled), District Heating & Cooling Integration, and Others), By Distribution Channel (Distributors & Wholesalers, HVAC Contractors, OEM (Direct Sales), Retail Sales, Online Channels, and Others)

|

|

Region Covered

|

Poland

|

|

Market Players Covered

|

Daikin Industries, Ltd. (Japan), Vaillant Group (Germany), Bosch Thermotechnology Ltd. (U.K.), LG Electronics (South Korea), Midea Group (China), Cooper&Hunter (U.S.), GREE Electric Appliances Inc. (China), VBW Engineering sp. z o.o. (Poland), Klimor (Poland), Flexit AS (Norway), and Samsung (South Korea) and others

|

|

Data Points Covered in the Report

|

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand.

|

Segment Analysis

The Poland HVAC market is segmented into four notable segments based on the product type, end user industry, technology, and distribution channel.

On the basis of product type, the Poland HVAC market is segmented into heating equipment, air conditioning systems, ventilation equipment, and refrigeration systems.

In 2026, the heating equipment segment is expected to dominate the Poland HVAC market

In 2026, the heating equipment segment is expected to dominate the Poland HVAC market with a market share of 46.41%, driven by the country’s cold climate and strong demand for efficient space heating solutions in residential and commercial buildings. Government initiatives promoting energy-efficient heating systems and the replacement of outdated coal-based boilers are further supporting market growth. Rising adoption of heat pumps and modern central heating technologies is also contributing to the segment’s leading position.

On the basis of end user industry, the Poland HVAC market is segmented into residential, commercial, industrial, and others.

In 2026, the residential segment is expected to dominate the Poland HVAC market

In 2026, the residential segment is expected to dominate the Poland HVAC market market with a market share of 48.68%, driven by increasing housing construction activities and rising consumer spending on home comfort solutions. Growing awareness regarding energy-efficient heating and cooling systems, along with government incentives for sustainable residential infrastructure, is boosting adoption. Additionally, the increasing popularity of smart HVAC systems and heat pumps in households is further supporting segment growth.

On the basis of technology, the Poland HVAC market is segmented into conventional HVAC systems, energy-efficient HVAC systems, smart HVAC systems (IoT-enabled), district heating & cooling integration, and others.

In 2026, the conventional HVAC systems segment is expected to dominate the Poland HVAC market

In 2026, the conventional HVAC systems segment is expected to dominate the Poland HVAC market with a market share of 44.58%, driven by their widespread installation base, lower upfront costs, and strong presence across residential, commercial, and industrial applications. Many consumers and businesses continue to prefer conventional systems due to their familiarity, ease of maintenance, and established service networks. Additionally, ongoing replacement and retrofit demand for existing HVAC infrastructure is supporting the segment’s market leadership.

On the basis of distribution channel, the Poland HVAC market is segmented into distributors & wholesalers, HVAC contractors, OEM (direct sales), retail sales, online channels, and others.

2026, the distributors & wholesalers segment is expected to dominate the Poland HVAC market

In 2026, the distributors & wholesalers segment is expected to dominate the Poland HVAC market with a market share of 34.87%, driven by their extensive distribution networks and strong relationships with HVAC manufacturers, contractors, and installers. These channels offer a wide range of products, bulk purchasing advantages, and efficient supply chain management, making them the preferred choice for large-scale residential and commercial projects. Additionally, their ability to provide after-sales support and timely product availability further strengthens their market position.

Major Players

Data Bridge Market Research analyzes Daikin Industries, Ltd. (Japan), Vaillant Group (Germany), Bosch Thermotechnology Ltd. (Germany), LG Electronics (South Korea), and Midea Group (China), as the major market players of the market.

Market Development

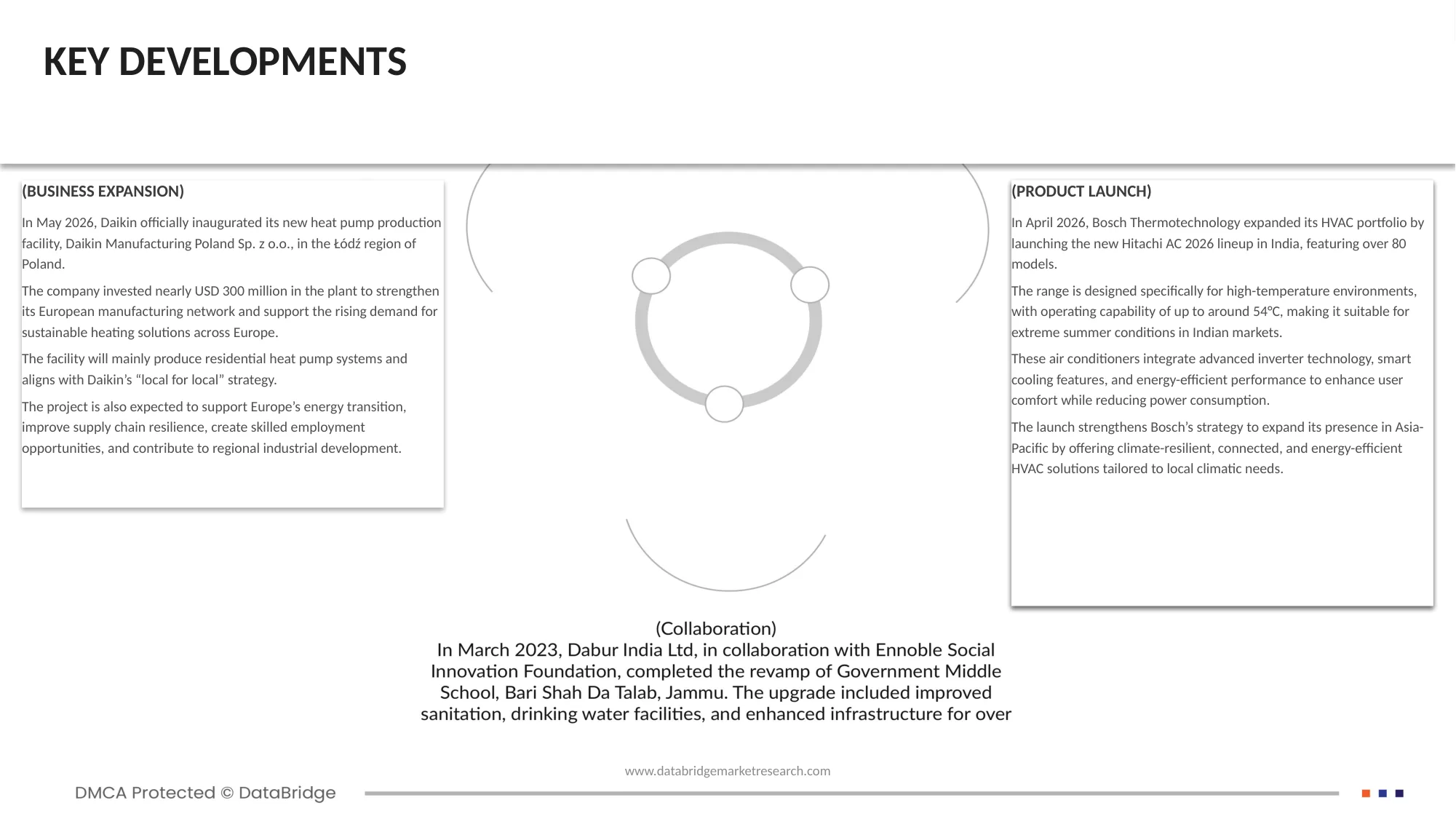

- In May 2026, Daikin officially inaugurated its new heat pump production facility, Daikin Manufacturing Poland Sp. z o.o., in the Łódź region of Poland. The company invested nearly USD 300 million in the plant to strengthen its European manufacturing network and support the rising demand for sustainable heating solutions across Europe. The facility will mainly produce residential heat pump systems and aligns with Daikin’s “local for local” strategy. The project is also expected to support Europe’s energy transition, improve supply chain resilience, create skilled employment opportunities, and contribute to regional industrial development.

- In March 2025, Vaillant Group strengthened its European heat pump business strategy through the expansion of its next-generation heat pump portfolio and intelligent energy management ecosystem showcased at ISH 2025.

- In April 2026, Bosch Thermotechnology expanded its HVAC portfolio by launching the new Hitachi AC 2026 lineup in India, featuring over 80 models. The range is designed specifically for high-temperature environments, with operating capability of up to around 54°C, making it suitable for extreme summer conditions in Indian markets. These air conditioners integrate advanced inverter technology, smart cooling features, and energy-efficient performance to enhance user comfort while reducing power consumption. The launch strengthens Bosch’s strategy to expand its presence in Asia-Pacific by offering climate-resilient, connected, and energy-efficient HVAC solutions tailored to local climatic needs.

- In May 2026, LG continued expanding its smart appliance and climate solution portfolio in India with additional premium appliance and cooling product launches aimed at energy efficiency and consumer convenience.

For more detailed information about the Poland HVAC Market report, click here – https://www.databridgemarketresearch.com/reports/poland-hvac-market