The global cast films market has been significantly propelled by the rising demand for high-performance flexible packaging solutions across key end-use sectors such as food & beverage, personal care, pharmaceuticals, and consumer goods. Flexible packaging formats including pouches, sachets, overwraps, and laminated structures are increasingly preferred over rigid counterparts due to their superior combination of lightweight properties, mechanical strength, clarity, and barrier performance, all of which are hallmarks of cast films such as cast polypropylene (CPP) and related structures. This shift stems from evolving consumer preferences toward convenience, extended shelf life, attractive product presentation, and cost efficiencies in transportation and material usage, which rigid packaging often cannot match.

Flexible packaging also adapts to diverse product types and shapes, enabling manufacturers and brand owners to optimize logistics and reduce environmental footprint a priority in today’s competitive packaging landscape. Furthermore, the flexible packaging continues to capture a dominant share of cast films demand, particularly in food packaging which is attributed to different packaging formats thus reflecting a structural transition in packaging strategy across industries.

Access Full Report @ http://httpswww.databridgemarketresearch.comreportsglobal-cast-films-market

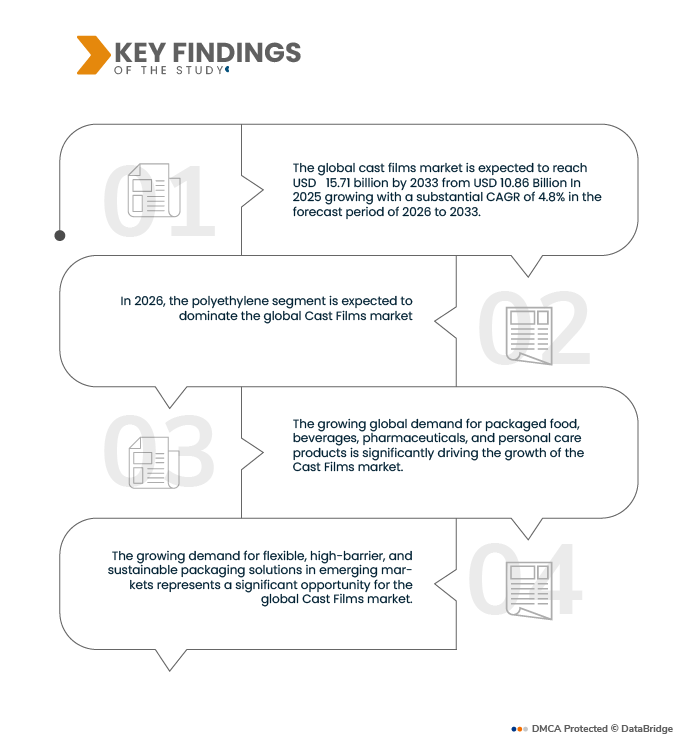

Data Bridge Market Research analyzes that the Global Cast Films Market is expected to reach USD 15.71 billion by 2033 from USD 10.86 Billion In 2025 growing with a substantial CAGR of 4.8%in the forecast period of 2026 to 2033.

Key Findings of the Study

Strong Growth in Packaged and Convenience Food Sector

The strong expansion of the packaged and convenience food sector has emerged as a pivotal factor driving increased demand for cast films in the global packaging market. Ongoing shifts in consumer preferences—such as a greater reliance on ready-to-eat, easy-to-prepare meals and on-the-go snacks—are reshaping food production and distribution patterns worldwide. These changes require packaging materials that ensure product protection, extended shelf life, portability, and clear brand visibility. Flexible packaging films, including cast films, meet these needs effectively, positioning them at the forefront of modern food packaging solutions.

Report Scope and Market Segmentation

|

Report Metric

|

Details

|

|

Forecast Period

|

2026 to 2033

|

|

Base Year

|

2025

|

|

Historic Year

|

2024 (Customizable 2018-2022)

|

|

Quantitative Units

|

Revenue in USD Billion

|

|

Segments Covered

|

By Material (Polyethylene (Linear Low-Density Polyethylene (LLDPE), Low-Density Polyethylene (LDPE) and High-Density Polyethylene (HDPE)), Polypropylene (Cast Polypropylene (CPP), Biaxially Oriented Polypropylene (BOPP)), Polyamide, PVC and Others), By Thickness (31–50 Microns, Up To 30 Microns, 51–70 Microns and Above 70 Microns), By Packaging Format (Pouches, Bags, Laminates, Wraps and Labels), By Layer Structure (Multilayer, Monolayer,) By Application (Food & Beverages (Processed Meat & Poultry, Frozen Products, Fruits & Vegetables, Fresh Meat & Poultry, Confectionery Products, Dairy Products, Dry Fruits and Others), Industrial, Personal Care, Pharmaceuticals (Drug Packaging, Vaccine Packaging and Others), Electricals & Electronics, Textile and Others)

|

|

Countries Covered

|

Asia-Pacific

Europe

North America

South America

Middle East and Africa

|

|

Market Players Covered

|

|

|

Data Points Covered in the Report

|

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework.

|

Segment Analysis

Global cast films market is segmented into five notable segments which are based on based on material, thickness, packaging format, layer structure, and application

- On the basis of material, the global cast films market is segmented into polyethylene, polypropylene, polyamide, PVC, others. Polyethylene is further segmented into linear low-density polyethylene (LLDPE), low-density polyethylene (LDPE), high-density polyethylene (HDPE). Polypropylene is further segmented into cast polypropylene (CPP), biaxially oriented polypropylene (BOPP).

In 2026, the polyethylene segment is expected to dominate the global Cast Films market

- In 2026, the Polyethylene segment is expected to dominate the global cast film market with a 65.03% share, driven by its widespread adoption across packaging, agriculture, and industrial applications. Its dominance is attributed to its cost-effectiveness, excellent sealability, high flexibility, and recyclability, which make it a preferred choice for manufacturers aiming to balance performance with sustainability. In addition to holding the largest market share, the Polyethylene segment is witnessing strong growth due to increasing demand for lightweight and durable packaging solutions, rising consumer preference for recyclable materials, and the expansion of the food, pharmaceutical, and consumer goods industries that rely heavily on polyethylene films for product protection and shelf-life extension.

- On the basis of thickness, the global cast films market is segmented into 31–50 microns, up to 30 microns, 51–70 microns, above 70 microns.

In 2026, 31–50 microns segment is expected to dominate the global Cast Films market

- In 2026, the 31–50 microns segment is expected to dominate the global cast film market with a 38.16% share, driven by its optimal balance of strength, flexibility, and clarity for a wide range of applications. This thickness range is highly preferred in packaging, agriculture, and industrial uses, as it provides excellent durability while maintaining cost-efficiency. In addition to holding the largest market share, the 31–50 microns segment is also experiencing steady growth due to increasing demand for high-performance films that ensure product protection, ease of handling, and compatibility with automated processing and sealing equipment across diverse industries.

- On the basis of packaging format, the global cast films market is segmented into pouches, bags, laminates, wraps, labels.

In 2026, the pouches segment is expected to dominate the market

- In 2026, the pouches segment is expected to dominate the global cast film market with a 38.73% share, driven by their versatility, convenience, and lightweight nature. Pouches are increasingly preferred in food, beverage, pharmaceutical, and personal care packaging due to their excellent barrier properties, portability, and ability to support innovative designs like stand-up, spout, and resealable options. In addition to holding the largest market share, the pouches segment is also witnessing strong growth as brands focus on sustainable, user-friendly, and visually appealing packaging solutions that enhance shelf presence and consumer experience.

- On the basis of layer structure, the global cast films market is segmented into multilayer, monolayer.

In 2026, multilayer segment is expected to dominate the market

- In 2026, the multilayer segment is expected to dominate the global cast film market with a 68.72% share, driven by its superior barrier properties, mechanical strength, and versatility in packaging applications. Multilayer films are widely used in food, pharmaceutical, and industrial packaging due to their ability to combine multiple materials, offering enhanced protection against moisture, oxygen, and UV light. In addition to holding the largest market share, the multilayer segment is also experiencing rapid growth as manufacturers increasingly adopt it to improve product shelf life, ensure safety, and meet evolving consumer and regulatory demands.

- On the basis of application, the global cast films market is segmented into food & beverages, industrial, personal care, pharmaceuticals, electricals & electronics, textile, others.

In 2026, the food & beverages segment is expected to dominate the market

- In 2026, the food & beverages segment is expected to dominate the global cast film market with a 34.08% share, driven by the increasing demand for packaged and processed foods that require extended shelf life and enhanced product protection. Cast films in this segment offer excellent barrier properties, flexibility, and durability, making them ideal for pouches, wraps, and multilayer packaging. Alongside holding the largest market share, the food & beverages segment is also witnessing significant growth due to the rising trend of ready-to-eat meals, on-the-go consumption, and stringent hygiene and safety regulations in the food industry.

Major Players

Data Bridge Market Research analyzes Amcor plc (Switzerland), Berry Global (U.S.), Uflex Ltd (India), Inteplast Group (U.S.), Jindal Poly Films Limited (India), and Oben Holding Group S.A.C. (Peru), among others, as some of the key players in the global cast film market.

Market Developments

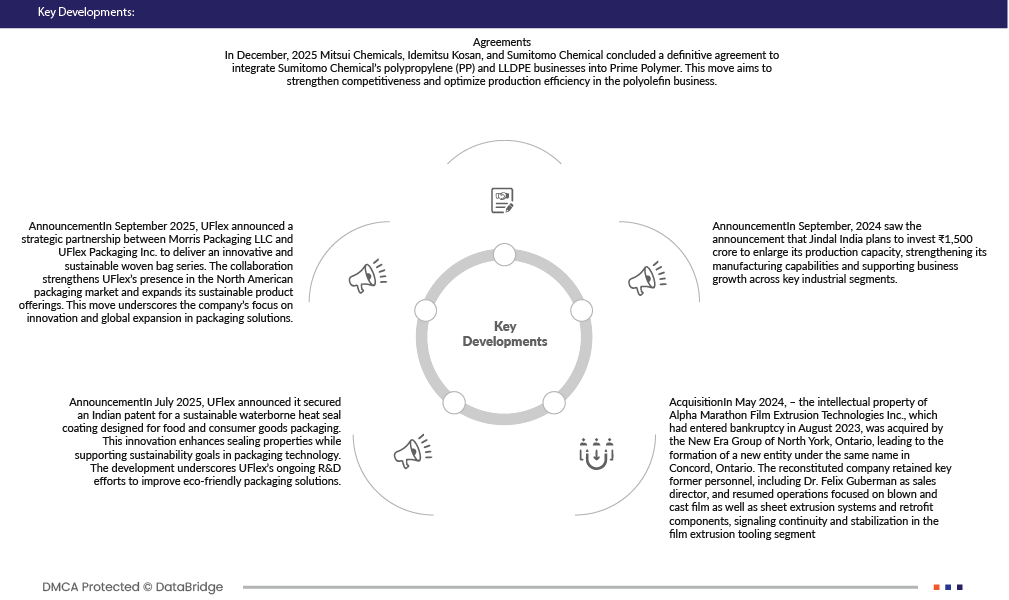

- In July, 2025, Inteplast Group has acquired Perga, a plastics film manufacturer based in Walldürn, south-western Germany. The decision marks Inteplast’s first move into Europe and brings Perga into the company’s engineered films division. This development help the company to ear revenue in the company year.

- In June 2025, Amcor has launched a first-of-its-kind, more sustainable Perflex shrink bag with an integrated handle for Butterball’s turkey breast packaging, replacing the traditional net wrap. The new design reduces packaging material and improves production efficiency, eliminating the need for manual netting. Compared with the incumbent packaging, the Perflex bag achieves a 22% reduction in carbon footprint and 22% lower water consumption. This innovation enhances Amcor’s sustainability portfolio by offering a lower-impact packaging solution that meets growing customer and regulatory demand for eco-friendly materials.

- In, August, 2024 Jindal Poly Films to add a new BOPP film production line in India. The expansion is intended to increase output capacity and cater to growing demand in flexible packaging. It strengthens the company’s position in the packaging films market.

- In September 2025, UFlex announced a strategic partnership between Morris Packaging LLC and UFlex Packaging Inc. to deliver an innovative and sustainable woven bag series. The collaboration strengthens UFlex’s presence in the North American packaging market and expands its sustainable product offerings. This move underscores the company’s focus on innovation and global expansion in packaging solutions.

Regional Analysis

Geographically, the countries covered in the global cast films market report is U.S., Canada, Mexico, Germany, U.K., Italy, France, Spain, Switzerland, Russia, Turkey, Belgium, Netherlands, Denmark, Norway, Finland, Sweden, Japan, China, South Korea, India, Singapore, Thailand, Indonesia, Malaysia, Philippines, Australia, New Zealand, Hong Kong, Taiwan, Argentina, Bolivia, Brazil, Chile, Colombia, Ecuador, Paraguay, Peru, Uruguay, Venezuela, South Africa, Egypt, Saudi Arabia, United Arab Emirates, Israel, Bahrain, Kuwait, Oman, Qatar and others.

As per Data Bridge Market Research analysis:

For more detailed information about the Global Cast Films Market report, click here – https://www.databridgemarketresearch.com/reports/global-cast-films-market