The growing emphasis on preventive healthcare and nutritional wellness across Europe is significantly increasing demand for immune-support and gut-health products, particularly those containing colostrum and other bioactive dairy ingredients. Consumers are becoming more aware of the relationship between gut microbiota, digestive balance, and immune resilience, leading to stronger adoption of functional nutrition products designed to support overall well-being. This trend is especially visible among health-conscious adults, aging populations, and parents seeking scientifically backed nutritional solutions that promote natural immunity and digestive health. As a result, manufacturers are increasingly focusing on colostrum-based formulations enriched with immunoglobulins, probiotics, and bioactive proteins to cater to evolving dietary preferences.

At the same time, advances in nutritional science and ingredient processing technologies are enabling companies to develop more targeted and convenient gut-health solutions. Functional beverages, powdered supplements, capsules, and fortified dairy products are becoming increasingly popular due to their perceived benefits for digestion, recovery, and immune defense. The expansion of wellness-focused retail channels and e-commerce platforms has further accelerated consumer access to premium nutritional products across Europe. In addition, collaborations between nutrition companies, research organizations, and healthcare-focused brands are encouraging innovation in microbiome-support products, reinforcing the role of colostrum and functional dairy ingredients within the broader health and wellness industry.

Access Full Report @ https://www.databridgemarketresearch.com/reports/europe-colostrum-market

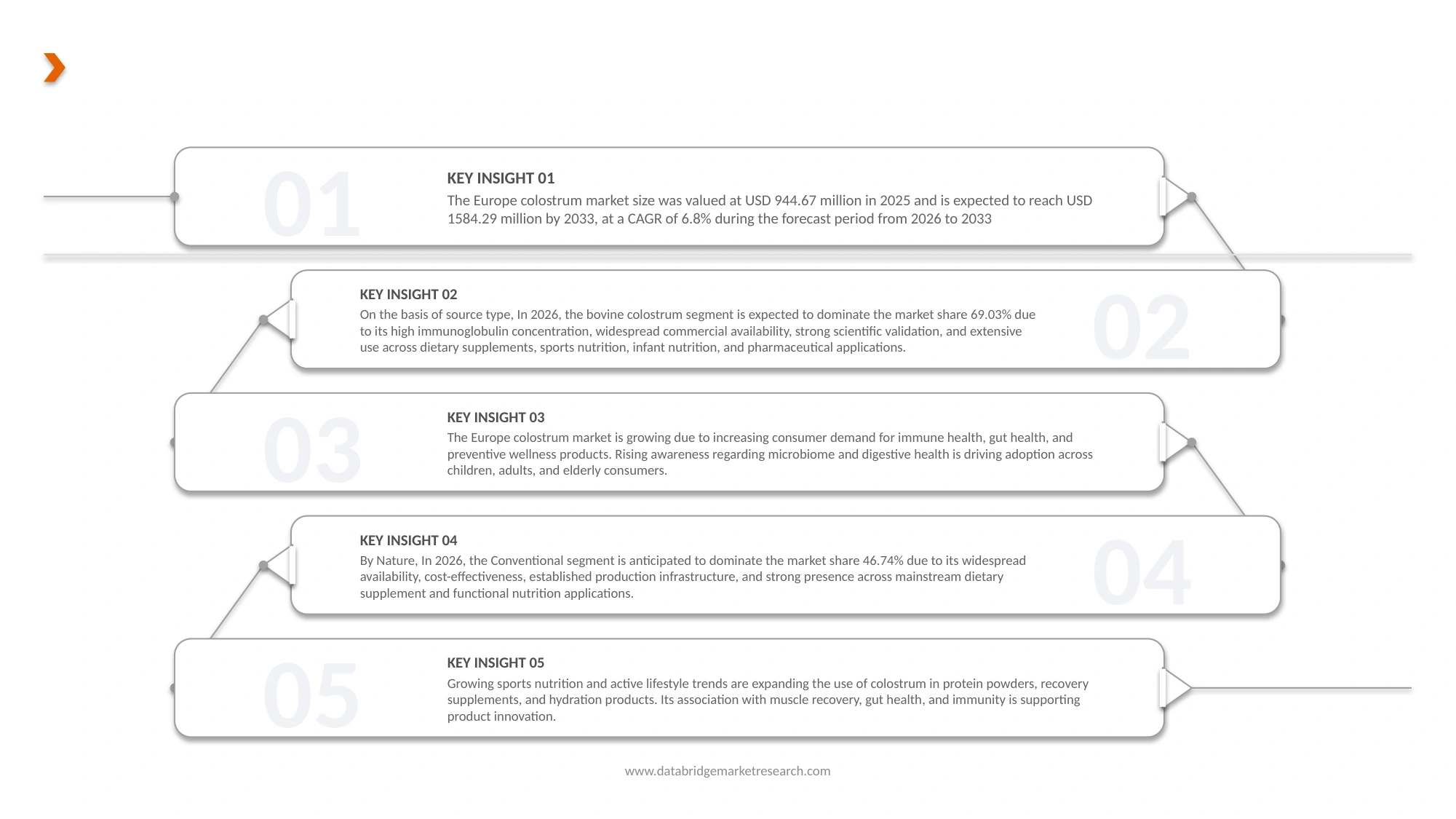

The Europe Colostrum Market size was valued at USD 944.67 million in 2025 and is expected to reach USD 1584.29 million by 2033, at a CAGR of 6.8% during the forecast period from 2026 to 2033.

Key Findings of the Study

Growth in Sports Nutrition and Active Lifestyle Products

The growing popularity of fitness culture, endurance sports, and performance-focused lifestyles across Europe is significantly increasing demand for advanced sports nutrition products. Consumers are increasingly seeking functional ingredients that support muscle recovery, stamina, immune resilience, and overall physical performance, leading to stronger adoption of protein-rich and bioactive nutritional supplements. Colostrum-based ingredients are gaining attention within this trend due to their natural composition of immunoglobulins, peptides, amino acids, and growth factors that may support post-exercise recovery and gut integrity. As professional athletes and recreational fitness enthusiasts become more focused on holistic wellness, sports nutrition brands are expanding their portfolios with scientifically backed formulations that combine performance and health benefits.

In addition, the shift toward clean-label and naturally sourced nutrition products is encouraging manufacturers to develop sports supplements with minimal processing and functional dairy-derived ingredients. Consumers are increasingly preferring nutritional products that support both athletic performance and long-term wellness, creating opportunities for colostrum-infused powders, ready-to-drink beverages, protein blends, and recovery formulations. E-commerce growth, influencer-driven fitness awareness, and expanding gym and wellness communities across Europe are further accelerating product visibility and consumer engagement. This evolving landscape is prompting nutrition companies to invest in innovation, strategic collaborations, and premium product development to address the changing preferences of active lifestyle consumers.

Report Scope and Market Segmentation

|

Report Metric

|

Details

|

|

Forecast Period

|

2026 to 2033

|

|

Base Year

|

2025

|

|

Historic Years

|

2024 (Customizable to 2018-2023)

|

|

Quantitative Units

|

Revenue in USD Million

|

|

Segments Covered

|

By Source Type (Bovine Colostrum, Goat Colostrum, Buffalo Colostrum, Sheep Colostrum, Mixed Animal Colostrum, and Others), By Nature (Conventional, Organic, Clean Label, Grass-Fed, Hormone-Free, and Others), By Product Form (Powder, Capsules, Liquid, Tablets, Gummies, Sachets & Stick Packs, Soft Gels, Chewable, Granules, and Others), By Immunoglobulin (Igg) Concentration (Below 15%, 15%–25%, 25%–35%, 35%–45%, Above 45%, Customized Igg Formulations, and Others), By Processing Technology (Spray Drying, Freeze Drying, Pasteurization, Membrane Filtration, Low-Temperature Processing, Microfiltration, Defatting, Fat Separation, Nano-Filtration, and Others), By Application (Dietary Supplements, Sports Nutrition, Functional Food & Beverages, Infant Nutrition, Pharmaceuticals, Animal Nutrition, Cosmetics, Veterinary Applications, and Others), By End User (Food and Feed), By Distribution Channel (Direct/B2B Sales, Online Retail, Pharmacies & Medical Stores, Specialty Nutrition Stores, Health & Wellness Stores, Supermarkets & Hypermarkets, Veterinary Clinics & Agri Stores, Convenience Stores, and Others), By Packaging Type (Bulk Packaging, Retail Packaging, Single-Serve Packaging, and Others), By Functionality (Immune Enhancement, Gut Microbiome Support, Nutritional Fortification, Muscle Recovery, Tissue Repair & Recovery, Anti-Inflammatory Support, Disease Prevention Support, Antioxidant Support, and Others), By Sales Model (Branded Products, Ingredient Supply, Contract Manufacturing, Private Label Manufacturing, OEM Supply, White Label Products, and Others)

|

|

Countries Covered

|

Europe

• France

• Germany

• Russia

• Italy

• Spain

• Turkey

• U.K.

• Netherlands

• Denmark

• Switzerland

• Belgium

• Sweden

• Norway

• Finland

• Rest Of Europe

|

|

Market Players Covered

|

· Colbiom SP. ZO (Poland)

· COLOSTRUM BIOTEC (Germany)

· European Colostrum Industry (Belgium)

· LacVital Colostrum (Germany)

· Vitomega Colostrum B.V. (Netherlands)

· COLOSTRUM POLSKA SP. Z O.O. (Poland)

· PEDERSEN BIOTECH A/S (Denmark)

· Goat Specialty Ingredients (Netherlands)

· ZiegenKraft GmbH (Germany)

· SwissBioColostrum AG (Switzerland)

· INGREDIA S.A. (France)

· Colostrum Biotech GmbH (Germany)

· Glanbia Nutritionals (Ireland)

· Biotaris B.V. (Netherlands)

· Bionatin B.V. (Netherlands)

|

|

Data Points Covered in the Report

|

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework.

|

Segment Analysis

The Colostrum Market is segmented into eleven notable segments based on source type, nature, product form, immunoglobulin (IGG) concentration, processing technology, application, end user, distribution channel, packaging type, functionality, and sales model.

- On the basis of source type, the Colostrum Market is segmented into Bovine Colostrum, Goat Colostrum, Buffalo Colostrum, Sheep Colostrum, Mixed Animal Colostrum, and Others.

In 2026, the Bovine Colostrum segment is expected to dominate the market

In 2026, the Bovine Colostrum segment is expected to dominate the market share 69.03% due to its high immunoglobulin concentration, widespread commercial availability, strong scientific validation, and extensive use across dietary supplements, sports nutrition, infant nutrition, and pharmaceutical applications. Established dairy infrastructure, large-scale bovine milk production, and advanced processing technologies in Europe further support consistent supply and product standardization. In addition, increasing consumer preference for immunity-supporting and protein-rich nutritional products continues to drive demand for bovine-derived colostrum formulations across both healthcare and functional nutrition industries.

- On the basis of Nature, the Colostrum Market is segmented into Conventional, Organic, Clean Label, Grass-Fed, Hormone-Free, Others.

In 2026, the Conventional segment is expected dominate the market

In 2026, the Conventional segment is anticipated to dominate the market share 46.74% due to its widespread availability, cost-effectiveness, established production infrastructure, and strong presence across mainstream dietary supplement and functional nutrition applications. Conventional colostrum products benefit from higher production volumes, easier sourcing processes, and broader distribution networks compared to premium organic alternatives. In addition, increasing consumer demand for affordable immunity-supporting supplements, combined with strong adoption in sports nutrition, animal nutrition, and pharmaceutical applications, continues to support the dominance of conventional colostrum products across Europe markets.

- On the basis of product form, the Colostrum Market is segmented into Powder, Capsules, Liquid, Tablets, Gummies, Sachets & Stick Packs, Soft Gels, Chewable, Granules, Others.

In 2026, the powder segment is anticipated to dominate the market

In 2026, the powder segment is expected to dominate the market share 39.77% due to its longer shelf life, ease of storage and transportation, higher formulation stability, and broad applicability across dietary supplements, sports nutrition, infant nutrition, and functional food products. Powdered colostrum also offers better concentration efficiency, flexible dosage customization, and compatibility with advanced processing technologies such as spray drying and freeze drying. In addition, growing demand for convenient nutritional supplements and bulk ingredient applications continues to support the widespread adoption of powdered colostrum products in Europe.

- On the basis of Immunoglobulin (Igg) Concentration, the Colostrum Market is segmented into Below 15%, 15%–25%, 25%–35%, 35%–45%, Above 45%, Customized Igg Formulations, and Others.

In 2026, the Below 15% segment is expected to dominate the market

In 2026, the Below 15% segment is anticipated to dominate the market share 32.17% due to its cost-effectiveness, wider commercial availability, and extensive usage across mainstream dietary supplements, functional foods, and animal nutrition applications. Products within this concentration range are commonly preferred for large-scale manufacturing because they offer balanced nutritional benefits while maintaining affordable pricing for mass-market consumers. In addition, lower IgG concentration colostrum products are easier to source and process in bulk quantities, supporting strong adoption across nutraceutical companies, food manufacturers, and veterinary nutrition sectors in Europe.

- On the basis of processing technology, the Colostrum Market is segmented into Spray Drying, Freeze Drying, Pasteurization, Membrane Filtration, Low-Temperature Processing, Microfiltration, Defatting, Fat Separation, Nano-Filtration, Others.

In 2026, the Spray Drying segment is projected to dominate the market

In 2026, Spray Drying segment is expected to dominate the market share 30.18% due to its cost efficiency, large-scale production capability, extended product shelf life, and widespread adoption across nutraceutical and functional food manufacturing. Spray drying enables effective moisture removal while preserving essential nutrients and bioactive compounds, making it suitable for commercial colostrum powder production. The technology also supports easier storage, transportation, and formulation flexibility for dietary supplements, sports nutrition, and infant nutrition products. In addition, its faster processing speed and lower operational costs compared to freeze drying continue to strengthen its dominance in the Europe colostrum market.

- On the basis of application, the Colostrum Market is segmented into Dietary Supplements, Sports Nutrition, Functional Food & Beverages, Infant Nutrition, Pharmaceuticals, Animal Nutrition, Cosmetics, Veterinary Applications, Others.

In 2026, the Dietary Supplements segment is expected to dominate the market

In 2026, the Dietary Supplements segment is expected to dominate the market share 29.53% due to increasing consumer awareness regarding immunity enhancement, preventive healthcare, digestive wellness, and overall nutritional supplementation. Rising demand for natural and functional ingredients, along with growing adoption of colostrum-based products in daily health routines, continues to support segment growth. Dietary supplements also benefit from broad product availability in powders, capsules, tablets, and gummies, enabling convenient consumption across different age groups. In addition, expanding e-commerce distribution, clean-label trends, and increasing focus on sports recovery and immune health further strengthen the dominance of the dietary supplements segment.

- On the basis of end use, the Colostrum Market is segmented into food and feed.

In 2026, the food segment is expected to dominate the market

In 2026, food segment is expected to dominate the market share 72.33% due to increasing consumer demand for functional nutrition, immunity-supporting products, and preventive healthcare solutions across all age groups. Rising adoption of colostrum in dietary supplements, infant nutrition, sports nutrition, and functional food products continues to strengthen segment growth. The food segment also benefits from expanding awareness regarding digestive wellness, healthy aging, and protein-rich nutritional formulations. In addition, broader retail availability, growing clean-label product demand, and increasing incorporation of colostrum into wellness beverages and fortified foods further support the dominance of the food segment in the Europe colostrum market.

- On the basis of Distribution Channel, the Colostrum Market is segmented into Direct/B2b Sales, Online Retail, Pharmacies & Medical Stores, Specialty Nutrition Stores, Health & Wellness Stores, Supermarkets & Hypermarkets, Veterinary Clinics & Agri Stores, Convenience Stores, and Others.

In 2026, the Direct/B2b Sales segment is expected to dominate the market

In 2026, Direct/B2b Sales segment is expected to dominate the market share 26.97% due to strong bulk purchasing demand from nutraceutical manufacturers, functional food producers, pharmaceutical companies, and animal nutrition suppliers. Direct sales channels enable large-volume procurement, long-term supply agreements, customized ingredient sourcing, and better pricing efficiencies for industrial buyers. In addition, manufacturers prefer direct partnerships to ensure consistent product quality, traceability, and regulatory compliance. The growing use of colostrum as a functional ingredient across dietary supplements, infant nutrition, sports nutrition, and veterinary applications further supports the dominance of the Direct/B2B Sales segment.

- On the basis of packaging type, the Colostrum Market is segmented into Bulk Packaging, Retail Packaging, Single-Serve Packaging, Others. The bulk packaging segment is further sub segmented into Drums, Bags, and Industrial Containers.

In 2026, the Bulk Packaging segment is expected to dominate the market

In 2026, Bulk Packaging segment is expected to dominate the market share 46.46% due to increasing large-scale procurement by nutraceutical manufacturers, functional food companies, pharmaceutical producers, and animal nutrition suppliers. Bulk packaging offers cost efficiency, easier transportation, reduced packaging waste, and improved storage convenience for industrial buyers handling high-volume production. In addition, growing demand for colostrum powder as a raw functional ingredient across dietary supplements, sports nutrition, and feed applications continues to support higher bulk purchasing volumes. Long-term B2B supply agreements and expanding industrial-scale manufacturing activities further strengthen the dominance of the bulk packaging segment.

- On the basis of functionality, the Colostrum Market is segmented into Immune Enhancement, Gut Microbiome Support, Nutritional Fortification, Muscle Recovery, Tissue Repair & Recovery, Anti-Inflammatory Support, Disease Prevention Support, Antioxidant Support, and Others.

In 2026, the Immune Enhancement segment is expected to dominate the market

In 2026, Immune Enhancement segment is expected to dominate the market share 28.50% due to increasing consumer awareness regarding preventive healthcare, immunity strengthening, and natural nutritional supplementation. Colostrum contains high levels of immunoglobulins, lactoferrin, growth factors, and bioactive compounds that support immune system function, making it highly preferred in dietary supplements and functional nutrition products. Rising demand for immunity-supporting formulations following Europe health concerns, along with growing adoption among sports nutrition users, elderly populations, and pediatric consumers, continues to drive segment growth. In addition, increasing clean-label and wellness-focused consumer trends further strengthen the dominance of the Immune Enhancement segment.

- On the basis of sales model, the Colostrum Market is segmented into Branded Products, Ingredient Supply, Contract Manufacturing, Private Label Manufacturing, OEM Supply, White Label Products, and Others.

In 2026, the Branded Products segment is expected to dominate the market

In 2026, Branded Products segment is expected to dominate the market share 35.87% due to increasing consumer preference for trusted, quality-certified, and clinically positioned nutritional products. Branded colostrum products benefit from strong marketing strategies, established customer loyalty, premium product positioning, and wider retail availability across pharmacies, online platforms, and specialty nutrition stores. In addition, growing awareness regarding immunity support, gut health, and sports recovery has encouraged consumers to prefer recognized brands offering standardized formulations and transparent sourcing practices. Continuous product innovation, clean-label positioning, and expansion into functional wellness categories further support the dominance of the branded products segment.

Major Players

Colbiom SP. ZO (Poland), COLOSTRUM BIOTEC (Germany), European Colostrum Industry (Belgium), LacVital Colostrum (Germany)

Market Developments

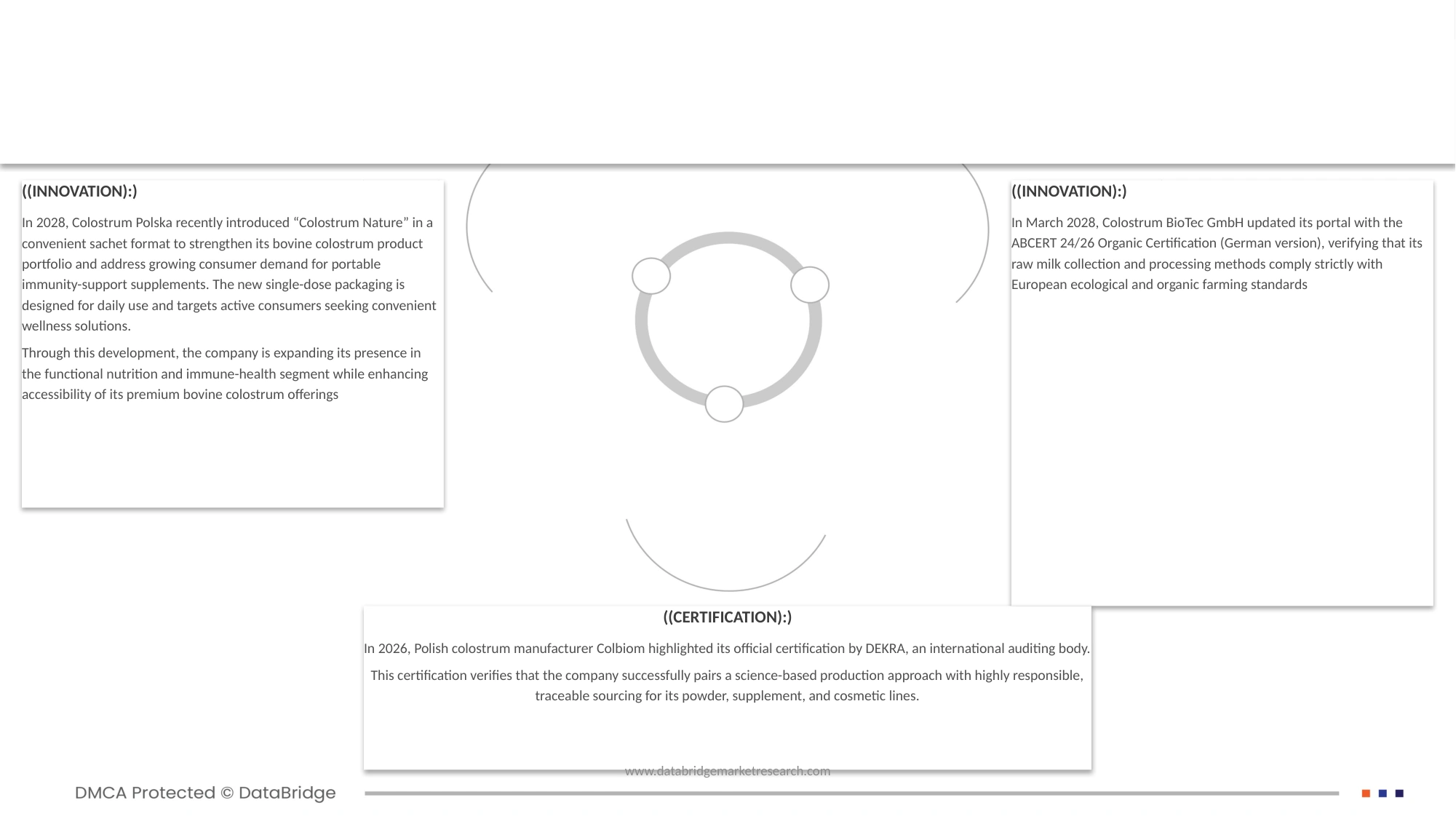

- In 2028, Colostrum Polska recently introduced “Colostrum Nature” in a convenient sachet format to strengthen its bovine colostrum product portfolio and address growing consumer demand for portable immunity-support supplements. The new single-dose packaging is designed for daily use and targets active consumers seeking convenient wellness solutions. Through this development, the company is expanding its presence in the functional nutrition and immune-health segment while enhancing accessibility of its premium bovine colostrum offerings.

- In March 2028, Colostrum BioTec GmbH updated its portal with the ABCERT 24/26 Organic Certification (German version), verifying that its raw milk collection and processing methods comply strictly with European ecological and organic farming standards.

- In 2026, Polish colostrum manufacturer Colbiom highlighted its official certification by DEKRA, an international auditing body. This certification verifies that the company successfully pairs a science-based production approach with highly responsible, traceable sourcing for its powder, supplement, and cosmetic lines.

- In 2025 Biotaris B.V. is using a special cold-state processing technology for colostrum, designed to preserve bioactive components such as immunoglobulins, proteins, vitamins, and growth factors. This method avoids heat treatment to maintain the natural quality of bovine colostrum during production. The company states that its production process involves direct freezing of colostrum after milking and gentle processing without heating, ensuring maximum retention of bioactive substances in the final product.

As per Data Bridge Market Research analysis:

Geographically, the countries covered in the Europe Sleep apnea devices Market report are Germany, U.K., France, Spain, Belgium, Russia, Netherlands, Italy, Turkey, Switzerland, Sweden, Denmark, Norway, Finland, and Rest of Europe.

Germany is the dominating Region in Europe colostrum market

- Germany is expected to be one of the leading contributors to the Europe colostrum market with fastest growing and dominating, accounting for 18.60% market share in 2025. The country is projected to grow at a CAGR of 8.4% during 2026–2033, supported by increasing consumer awareness regarding immune health, digestive wellness, and nutritional supplements. Growth is further driven by the rising adoption of premium bovine colostrum products, advanced distribution networks, and strong demand for natural health ingredients across functional food and nutraceutical applications.

Asia-Pacific is expected to be the fastest growing region in Europe colostrum market

- The U.K. colostrum market is anticipated to witness steady expansion, holding approximately 14.60% market share in 2025 and registering a CAGR of 6.9% from 2026 to 2033. Market growth is attributed to increasing interest in preventive healthcare, sports nutrition, and immunity-enhancing supplements. The growing preference for clean-label and naturally derived ingredients, along with expanding availability of colostrum-based dietary supplements through online and retail channels, is expected to support market development across the country.

As per Data Bridge Market Research analysis:

For more detailed information about theEurope colostrum market report, click here – https://www.databridgemarketresearch.com/reports/europe-colostrum-market