ヨーロッパ心臓ペースメーカーの市場規模、株式、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

1.57 Billion

USD

2.42 Billion

2024

2032

USD

1.57 Billion

USD

2.42 Billion

2024

2032

| 2025 –2032 | |

| USD 1.57 Billion | |

| USD 2.42 Billion | |

| % | |

|

ヨーロッパ心臓ペースメーカー市場セグメンテーション、タイプ(磁気共鳴イメージング対応ペースメーカー、慣習的なペースメーカー、インプラント可能なペースメーカー、および外部ペースメーカー)、技術(シングルチャンバー・ペースメーカー、デュアルチャンバー・ペースメーカー、およびビベントラル/心臓再同期療法ペースメーカー)、アプリケーション(Arrhythmia、Atrial Fibrillation、Bradycardia、Tachycardia、その他センター、およびその他センター(Hoodia) 業界動向と予測 2032

ヨーロッパ心臓ペースメーカー市場規模

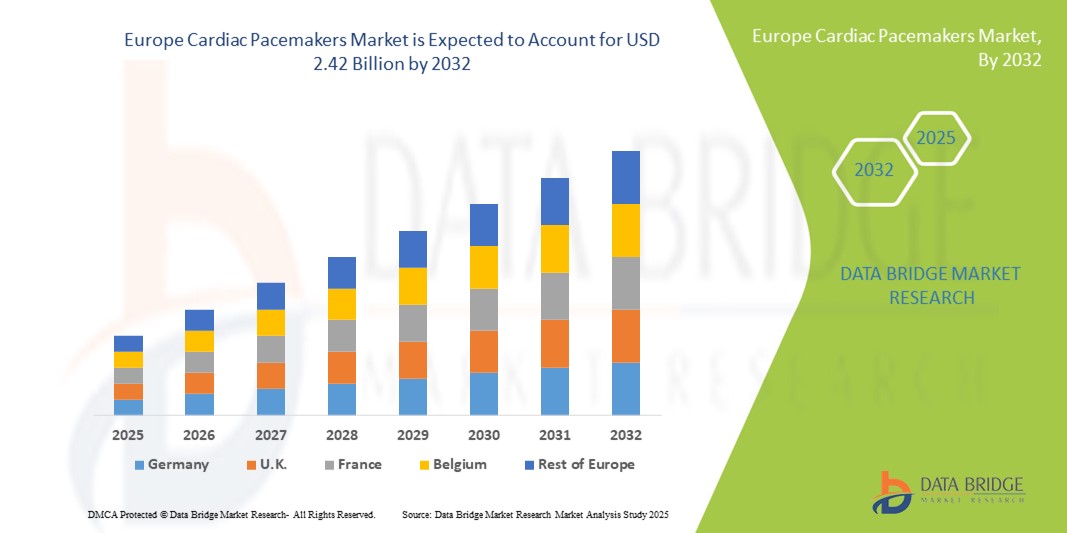

- ヨーロッパ心臓ペースメーカーの市場規模が評価されました2024年のUSD 1.57億そして到達する予定2032年までのUSD 2.42億, お問い合わせ5.50%のCAGR予報期間中

- 市場成長は、主に心臓血管疾患の高まりと、高度心臓のリズム管理ソリューションの高需要に貢献している地域全体の高齢化人口の増加によって駆動されます

- また、MRI対応ペースメーカー、リモート監視機能、および最小限の侵襲インプラント技術などの継続的な技術進歩は、患者の成果を改善し、市場の成長軌跡を拡大するための重要なソリューションとして、採用率を強化し、心臓ペースメーカーを配置しています。

ヨーロッパ心臓ペースメーカー市場分析

- 心臓ペースメーカーは、電子刺激を介して異常な心臓リズムを調節する、現代の心臓学の重要なデバイスであり、患者の生存と生活の質を向上させる上で重要な役割を果たしています。 病院と患者の信頼性、プログラム性、長期的有効性による過渡的な設定

- 心臓ペースメーカーの需要の高まりは、心臓血管疾患の増大の蔓延、高齢者の拡大、早期の診断と治療の選択肢の認知度を高めています。

- ドイツは、2024年に24.6%の最大の収益シェアを持つ欧州心臓ペースメーカー市場を支配し、強力な医療インフラ、有利な償還方針、および主要なmedtech会社の存在によって支持され、MRI互換および無鉛ペースメーカーなどの高度な舗装ソリューションの重要な採用と

- ポーランドは、ヘルスケア投資の増加、心臓ケアのアクセシビリティの向上、先進医療技術の蓄積による予測期間における欧州心臓ペースメーカー市場で最も急速に成長している国であると予想され、

- デュアルチャンバーのペースメーカーのセグメントは、2024年に45.8%の市場シェアを持つ欧州心臓ペースメーカーの市場を支配し、自然心リズムをより効果的に移行し、単一のチャンバーデバイスと比較して優れた患者結果を提供する能力に起因しています

レポートスコープと欧州心臓ペースメーカー市場セグメンテーション

| アトリビュート | ヨーロッパ心臓ペースメーカーの主要市場洞察 |

| カバーされる区分 |

|

| カバーされた国 | ヨーロッパ

|

| 主要市場プレイヤー |

|

| マーケットチャンス |

|

| 付加価値データインフォセットを追加 | 市場価値、成長率、セグメンテーション、地理的カバレッジ、主要なプレーヤーなどの市場シナリオに関する洞察に加えて、Data Bridge Market Researchがキュレーションする市場レポートには、詳細なエキスパート分析、価格設定分析、ブランドシェア分析、消費者調査、デモグラフィ分析、サプライチェーン分析、バリューチェーン分析、原材料/消耗品の概要、ベンダー選定基準、PESTLE分析、ポーター分析、規制フレームワークが含まれます。 |

ヨーロッパ心臓ペースメーカー市場動向

遠隔監視とAI対応のペースメーカーの高度化

- 欧州心臓ペースメーカー市場での有意で加速傾向は、AI対応のペースメーカーとリモート監視技術の統合であり、リアルタイムの心臓のリズム追跡と予測診断による患者ケアを改善します。

- たとえば、Medtronic Azureのペースメーカーは、臨床医が患者の心臓活動を遠隔に監視し、パッシングパラメータを調整し、頻繁な病院訪問を必要としない異常なイベントのアラートを受け取ることを可能にします

- ペースメーカーのAIインテグレーションにより、患者活動に基づく適応的なパッシング、不整脈に対する予測アラート、およびリモートモニタリングがタイムリーな医療介入と患者の結果を向上する一方で、自動調整などの機能が実現できます。

- 病院ITシステムとモバイルヘルスプラットフォームを備えたペースメーカーのシームレスな接続により、患者データの集中管理を可能にし、心臓専門医が複数の患者を同時に監視し、情報に基づいた意思決定を迅速に行うことができます。

- よりインテリジェント、接続、および患者中心の心臓デバイスに対するこの傾向は、心臓ケアに対する期待を根本的に再構築しています。 その結果、ボストン科学などの企業は、予測診断とリモート監視機能を備えたAI支援ペースメーカーを開発しています。

- ヘルスケアプロバイダがますますます効率を優先し、個人化された処置および改善された忍耐強い付着を改良するので、AI対応およびリモート・モニタリングの特徴を提供するペースメーカーのための要求は病院および外来の設定に急速に成長しています

ヨーロッパの心臓ペースメーカー市場ダイナミクス

ドライバー

心臓血管疾患の予防と老化の人口の増加

- 心血管障害、特に不整脈および心臓ブロックの状態の上昇の優先順位は、拡大する高齢者の人口と相まって、心臓ペースメーカーの成長需要のための重要なドライバーです

- たとえば、2024年3月、Abbottは、欧州におけるMRI対応ペースメーカーの新ラインを立ち上げ、複雑な心臓病の老化患者をサポートし、病院やクリニックの採用を促すことが期待されています。

- 早期診断とタイムリーな治療の増加の意識として、ペースメーカーは、デュアルチャンバーパッシング、プログラム可能な設定、および従来の療法と比較して優れた患者結果を提供するなどの高度なソリューションを提供します

- さらに、政府の医療取り組み、有利な返金方針、および心臓病管理のための国家プログラムが、ペースメーカー技術のより広い採用を促進しています

- 遠隔監視の利便性、インプラントの緩和、および治療調整の管理能力は、欧州の病院、心臓センター、および外来施設におけるペースメーカーの採用を推進する重要な要因です。

拘束/チャレンジ

高デバイスコストと規制コンプライアンスハルール

- AI対応モデルやMRI対応モデルなど、高度なペースメーカー機器やアクセサリーの比較的高いコストで、特に価格に敏感な市場での普及に挑戦

- たとえば、東ヨーロッパ諸国の小さな病院やクリニックは、予算の制約と限られた払い戻しのカバレッジによる上限のペースメーカーの採用を遅らせる可能性があります

- セリウムの印、ISOの証明および厳密な臨床試験の条件のような規制の承諾に、遅れがプロダクト進水のタイムラインを遅らせることができるので市場の記入項目および維持の装置安全基準のために重要であるように、対処して下さい

- また、デバイスの長寿、バッテリー交換手順、および潜在的な外科合併症に関する懸念は、医師や患者の採用決定に影響を与える可能性があります

- イノベーションとコストの最適化は、堅牢性を徐々に改善していますが、高い治療費と複雑な規制当局の承認プロセスは、特に新興欧州市場で急速に採用を制限し続けています。

- 長期デバイスの利益に対する価格設定戦略、合理化された規制承認、および教育を通じてこれらの課題を克服することは、持続的な市場成長のために不可欠です

ヨーロッパ心臓ペースメーカー市場スコープ

市場は、タイプ、技術、アプリケーション、エンドユーザーに基づいてセグメント化されます。

- タイプ別

タイプに基づいて、欧州の心臓ペースメーカー市場は、磁気共鳴イメージング(MRI)対応ペースメーカー、従来のペースメーカー、インプラント可能なペースメーカー、および外部ペースメーカーに分けられます。 注入可能なペースメーカーのセグメントは、2024年に48.5%の最大の収益シェアで市場を支配し、長期心臓のリズム管理における広範な使用と継続的なパッシング療法を提供する能力によって駆動しました。 移植可能なペースメーカーは、信頼性、耐久性、およびプログラム可能な機能により、慢性不整脈または線維状疱疹の患者のための心臓専門医によって優先されます。 これらの装置は遠隔監視のような高度の技術およびAIアシスト療法の調節、忍耐強い結果を高めるとまた互換性があります。 市場需要は、恒久的なパッシングソリューションの利点と定期的な心臓ケアのためのインプラント機器の採用を高めることで、患者間の意識を高めることでさらにサポートされています。

MRI対応のペースメーカーセグメントは、2025年から2032年までの19.6%の最速成長率を目撃する予定で、イメージング手順で安全であるデバイスの増加の必要性によって燃料を供給されています。 MRI 互換のペースメーカーは、患者は、デバイスを除去または妥協することなく、重要な診断スキャンを受けることを可能にします。 頻繁なイメージング検査を必要とする心臓血管患者の増加の予防は、採用を駆動しています。 また、材料や機器の小型化の技術的進歩は、MRI対応モデルをお勧めする医師を奨励し、安全性と忍耐強い快適さを改善しています。 非MRI対応のペースメーカーの制限が高まっています。また、これらの先進デバイスの急速なアップテークをサポートしています。

- テクノロジー

技術に基づき、市場はシングルチャンバーのペースメーカー、デュアルチャンバーのペースメーカー、およびバイベントラルに分けられます。心臓再同期療法(CRT)ペースメーカー デュアルチャンバーのペースメーカーのセグメントは、2024年に45.8%のシェアで市場を支配し、より密接に自然心リズムを模倣し、単一チャンバーデバイス上の優れたヘモディナムの利点を提供します。 デュアルチャンバーのペースメーカーは、アトリオベンチュラルブロックや他の複雑な不整形剤を持つ患者に広く使用され、有害および換気の収縮のより良い同期を提供します。 セグメントの優位性は、速度応答性パッシング、リモートモニタリング、プログラム可能な設定などの高度な機能の可用性によってさらに強化され、患者の成果を改善し、病院の訪問を削減します。 標準的な心臓ケアプロトコルのデュアルチャンバーデバイスのための臨床設定も市場のリーダーシップをサポートしています。

胸部/CRTペースメーカーセグメントは、2025年から2032年までの21.2%の最速のCAGRを登録すると予想され、心臓の故障の発生率を高め、CRT治療をサポートし、心臓機能を改善するための臨床的エビデンスが増加する。 胸部のペースメーカーは、心不全の症状を軽減し、忍耐強い生活の質を向上させる、両方のベントリルの調整されたパッシングを提供します。 高度心不全の患者の増加、欧州の有利な償還方針と相まって、採用を加速しています。 装置の小型化、電池の長寿およびリモート・モニタリングの両立性の連続的な革新は更に急速な市場成長に貢献します。

- 用途別

アプリケーションに基づいて、欧州の心臓ペースメーカーの市場は、不整脈、有利なフィブリレーション、bradycardia、tachycardia、等に分けられます。 ブラディカルディアセグメントは、2024年に最大の収益シェアで市場を支配しました。ペースメーカーは、主に疲労、めまい、または突然の心臓の逮捕につながることができる遅い心拍数を管理するために処方されています。 高齢化の人口と合併症の認知度を高め、需要を促進します。 病院や心臓センターは、実証済みの有効性、長期的信頼性、および患者固有の要件に応じてプログラムされる能力のために、bradycardia管理のペースメーカーを好む。 スピードレスポンシブ・パッシングやAI・アシスト・モニタリングなど、パッシング技術の継続的な革新により、セグメントの優位性をさらに強化します。

AFの高齢化と合併症の患者の間でAFの高齢化を促進し、予測期間中に最も速い成長を目撃するために投じられた有能な繊維セグメント。 激しいセンシングとパッシング機能を備えたペースメーカーは、不規則な心臓のリズムを管理し、ストロークのリスクを削減し、忍耐強い生活の質を向上させます。 AFの早期発見につながる診断手順の増加数, AF患者のCRTデバイスの成長採用とともに, 急成長をサポートしています. ヘルスケアプロバイダーや患者教育への取り組みによる意識キャンペーンは、さらなる採用を加速しています。

- エンドユーザーによる

エンドユーザーに基づいて、欧州の心臓ペースメーカー市場は、病院や心臓センター、および血管外科センター(ASC)に分けられます。 病院や心臓センターのセグメントは、2024年に最大の収益シェアで市場を支配し、設備の整ったインフラ、専門心臓専門医の可用性、複雑な注入手順を実行するための機能を備えています。 病院は、遠隔監視およびフォローアップを含む広範囲の事前および術後のケアを提供し、ペースメーカーの注入のための好まれる設定をします。 政府の払い戻し方針と高患者の足場を厳格なケアセンターでサポートしています。

血管外科センターのセグメントは、外来の手順、費用効果が大きい、およびより短い回復時間の設定を高めるために、2025から2032までの最速の成長率を目撃することが期待されます。 ASCは、特に低リスクの患者にとって、定期的なペースメーカーのインプラントメントに魅力的になっています。これにより、病院の負担を軽減し、患者様の利便性を向上させることができます。 最小限の侵襲的な技術、より短いプロシージャの持続期間および改善された装置の安全の進歩はASCsの採用を運転しています。 また、外来性心臓手術の可用性に関する患者様に対する意識向上は、このエンドユーザーセグメントの拡大をサポートしています。

ヨーロッパ心臓ペースメーカー市場地域分析

- ドイツは、2024年に24.6%の最大の収益分配で心臓ペースメーカー市場を支配し、強力な医療インフラ、有利な償還方針、および主要なmedtech会社の存在によって支持され、MRI互換および無鉛ペースメーカーなどの高度な舗装ソリューションの重要な採用と

- ドイツにおける患者およびヘルスケアプロバイダーは、現代のペースメーカーが提供する信頼性、プログラマビリティ、およびリモートモニタリング能力を非常に重視し、治療結果を改善し、病院の訪問を削減します。

- この広範囲にわたる採用は、有利な償還方針、主要な医療機器メーカーの存在、および初期の診断および治療の早期の意識を高めることでさらに支持され、ペースメーカーは、病院と全国の患者ケア設定の重要なソリューションとして確立します

英国心臓ペースメーカーのマーケットインサイト

英国心臓ペースメーカーの市場は、2024年に欧州で重要な収益シェアを占め、心臓血管疾患の増大と不整脈管理の意識を高めています。 患者およびヘルスケアプロバイダーは、治療結果を改善するために、デュアルチャンバーやMRI互換ペースメーカーなどの高度なパッシングソリューションを優先しています。 遠隔監視技術の採用が高まっています。, 支持的な医療政策と償還スキームと相まって, さらなる市場成長を推進しています。. また、英国各地の病院インフラや専門心臓センターを拡充し、慢性・急性心臓病の高度ペースメーカー治療へのアクセスを強化しています。 最小限の侵襲的な注入のプロシージャおよび改善された装置長寿への傾向はまた広範囲の採用を奨励しています。

ドイツ Cardiac Pacemakers マーケットインサイト

ドイツの心臓ペースメーカーは、2024年にヨーロッパを支配し、大規模な収益シェアを占め、健康に確立された医療インフラ、高層人口、大手医療機器メーカーの強力な存在によって支持されています。 ドイツの患者や心臓専門医は、現代のペースメーカーの信頼性、プログラマビリティ、リモート監視能力を高く評価し、病院の訪問を減らし、患者の生活の質を改善します。 好ましい償還方針と全国の心血管ケアプログラムは、市場拡大を支援しています。 ドイツの病院や心臓センターは、バイベンチュアルペースメーカーやAI支援機器などの高度なパッシング技術を採用し、患者様による結果を高めています。 MRI対応のペースメーカーを含む技術開発も採用率を高めています。

フランスの心臓ペースメーカー市場洞察

フランスの心臓ペースメーカー市場は、心不全と不整脈の増加によって駆動され、予測期間中に注目すべきCAGRで成長することが期待されます。 フランスのヘルスケアプロバイダーは、デュアルチャンバーとCRTペースメーカーを含む高度なパッシングデバイスをますます導入し、心臓機能の最適化と患者の予後を改善します。 政府のイニシアチブは心血管疾患管理と早期の検出プログラムをサポートし、患者がペースメーカーの治療法へのアクセスを強化しています。 国の洗練された病院インフラは、不整脈管理に関する意識キャンペーンと相まって、燃料化の採用です。 また、リモートモニタリングとテレヘルス機能の統合により、より優れたポストインプラントケアとフォローアップが可能になります。

ポーランドの心臓ペースメーカー市場洞察

ポーランドの心臓ペースメーカー市場は、ヘルスケアインフラを改善し、高度な心臓機器の可用性を高め、不整脈管理の意識を高めることで、予測期間中、欧州で最速のCAGRを登録することが期待されています。 病院や心臓センターは、MRI互換およびデュアルチャンバーのペースメーカーを採用し、心臓血管患者の安全かつ効果的な治療を提供します。 ペースメーカーのインプラントへの政府のイニシアチブと保険のカバレッジは、アクセシビリティを強化しています。 成長する忍耐強い意識と中心の無秩序の増加と結合される技術革新は急速な市場の採用を運転しています。 外来の手順と最小限の侵襲的な注入に対する傾向は、さらなる成長に貢献しています。

ヨーロッパ心臓ペースメーカー市場シェア

欧州の心臓ペースメーカー業界は、主に、以下を含む老舗の企業によって導かれています。

- Medtronic(アイルランド)

- BIOTRONIK SE&Co. KG(ドイツ)

- アボット(米国)

- ボストン科学株式会社(米国)

- マイクロポート科学株式会社(中国)

- LivaNova PLC (イギリス)

- メディコS.p.A.(イタリア)

- ソリングループ(イタリア)

- セント・ジュード・メディカル(米国)

- ヴィタトロン(オランダ)

- 心臓科学(米国)

- 物理制御(米国)

- ゾールメディカル株式会社(米国)

- Koninklijke Philips N.V.(オランダ)

- GEヘルスケア(英国)

- Siemens Healthineers AG(ドイツ)

- Schiller AG(スイス)

- Welch Allyn(アメリカ)

- ニホンコフデン株式会社(日本)

- Biotronik(ドイツ)

欧州心臓ペースメーカー市場における最近の発展は何ですか?

- 2025年7月、BIOTRONIKとCardioFocusは、欧州におけるパルスフィールドアボレーション(PFA)技術へのアクセスを拡大するためのパートナーシップを発表しました。 欧州17ヵ国に展開するCentauriTM PFA Systemを導入することで、アトリルフィブリレーション患者様の治療オプションを強化

- 2024年6月、Abbottは、AVEIRTM DRのデュアルチャンバー無鉛ペースメーカーシステム用のCEマークの受領を発表しました。 この革新的なデバイスは、ワイヤレスで、無鉛のペースメーカー間のビート・ツー・ビート・ビート・ビート・ビート・ビート・コミュニケーションを可能にし、複雑な不整脈を持つ患者のためのシンクロ化されたパッシングを提供します。

- 2024年1月、Medtronicは、次世代のMicraリードレスペースメーカーのCEマーク承認を受けました。Micra AV2とMicra VR2。 これらのデバイスは、以前のモデルと比較して、より長い電池寿命と簡素化されたプログラミングを提供し、患者の成果を高め、従来のペースメーカーに関連付けられている合併症を減らす

- 2023年8月、BIOTRONIKは、Amvia SkyのペースメーカーであるAmvia Skyのヨーロッパ初のインプラントで、左のバンドルブランチエリアパッシング(LBBAP)で世界初のデバイスを承認しました。 この進歩は、伝導障害のある患者のためのより生理学的なパッシングオプションを提供し、潜在的に臨床結果を改善する

- 2022年12月、欧州委員会は、Horizon Europeプログラムを立ち上げ、革新的な心臓ペースメーカー技術への資金調達研究を開始しました。 プログラムは、遠隔監視機能や強化された患者の互換性など、改善された機能性を備えた次世代ペースメーカーの開発をサポートし、欧州における先進的な心臓ケアソリューションの需要の高まりに対応

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。