サービス市場規模、シェア、トレンド分析レポートとしてのグローバルバッテリー

Market Size in USD Billion

CAGR :

%

USD

750.00 Million

USD

5,218.04 Million

2024

2032

USD

750.00 Million

USD

5,218.04 Million

2024

2032

| 2025 –2032 | |

| USD 750.00 Million | |

| USD 5,218.04 Million | |

| % | |

|

サービス市場セグメンテーションとしてのグローバルバッテリー、サービスタイプ(サブスクリプションモデルおよび有料モデル)、エネルギーストレージ容量(50kWh、50-100kWh以上、100kWh以上)、アプリケーション(エネルギーストレージ、自動車および輸送、産業アプリケーション、その他)、エンドユーザー(Automotive、電気通信、エネルギー&ユーティリティ、住宅、商業&産業など) - 業界動向と予測20323232

サービス市場規模と成長率としてのグローバルバッテリーとは?

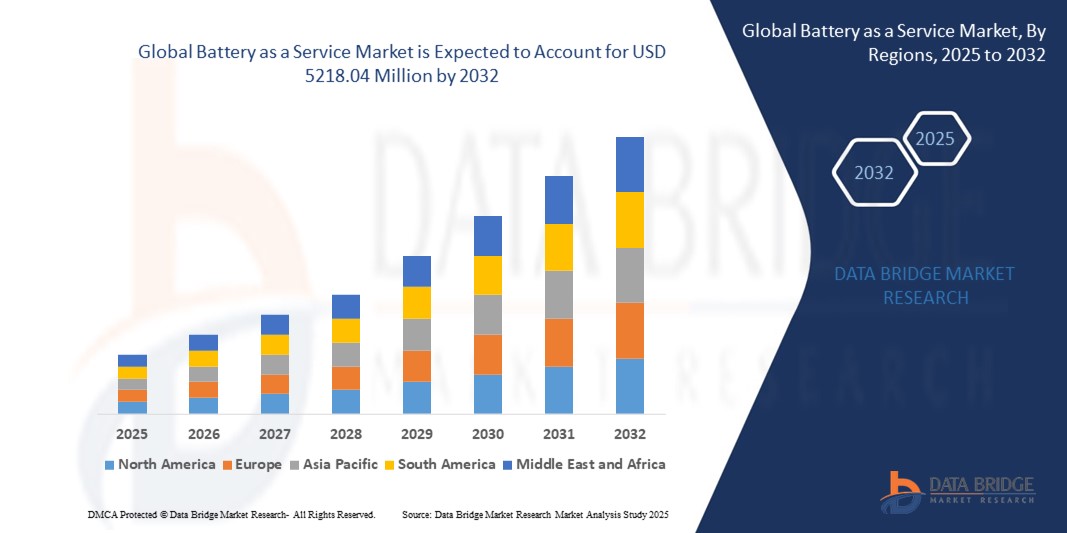

- サービス市場規模のグローバルバッテリーは、2024年のUSD 750百万そして到達する予定米ドル 5218.04 百万によって 2032, お問い合わせ27.44%のCAGR予報期間中

- 成長は主に上昇の採用によって運転されます電気自動車(EV) および、BaaS を消費者とフリート オペレータの両方に魅力的なモデルにすることで、高いバッテリーコストを克服する必要がある

- また、自動車メーカーとエネルギープロバイダー間の戦略的パートナーシップ、および支援政府のインセンティブは、世界中のBaaSソリューションの大規模な採用を加速し、業界の拡大を著しく推進しています。

サービス市場としてのバッテリーの主なテイクアウトは何ですか?

- EV所有者が車両から電池を別々にリースし、購入コストを削減し、バッテリー交換を高速化し、エネルギー効率管理を向上

- BaaSの需要は、主にEVの普及、持続可能なエネルギーソリューションの推進、および消費者の負担を軽減する柔軟なオーナーシップモデルの必要性によって供給されています。

- 駅のネットワークを交換し、自動車やエネルギー分野を横断するコラボレーションを成長させ、費用対効果の高いEVオーナーシップに対する消費者の需要が高まっています。BaaSは、世界的なEVエコシステムにおける変革モデルとして誕生しています。

- アジア・パシフィックは、2024年に42.5%の最大の収益シェアを誇るサービス市場としてバッテリーを占拠し、急速な都市化、電気自動車の普及、および支援政府のイニシアチブは、バッテリー交換インフラを奨励

- サービス市場としての北米バッテリーは、2025年から2032年までの10.6%の最速のCAGRで成長し、EVの採用を加速し、環境意識を高め、インフラを充電および交換するための強力な投資を計画しています

- サブスクリプションモデルセグメントは、2024年に61.4%の最大の収益シェアで市場を支配し、予測可能なコスト構造と個々のEV所有者とフリートオペレータの両方の利便性によって駆動しました

レポートスコープとバッテリーをサービス市場区分として

| アトリビュート | サービスキーマーケットの洞察として電池 |

| カバーされる区分 |

|

| カバーされた国 | 北アメリカ

ヨーロッパ

アジアパシフィック

中東・アフリカ

南米

|

| 主要市場プレイヤー |

|

| マーケットチャンス |

|

| 付加価値データインフォセットを追加 | 市場価値、成長率、セグメンテーション、地理的カバレッジ、主要なプレーヤーなどの市場シナリオに関する洞察に加えて、Data Bridge Market Researchがキュレーションする市場レポートには、詳細なエキスパート分析、価格設定分析、ブランドシェア分析、消費者調査、デモグラフィ分析、サプライチェーン分析、バリューチェーン分析、原材料/消耗品の概要、ベンダー選定基準、PESTLE分析、ポーター分析、規制フレームワークが含まれます。 |

サービス市場としてのバッテリーの重要な傾向は何ですか?

スマートエネルギー管理のためのIoTとAIの統合

- サービス(BaaS)市場として世界電池を形づける主要な傾向は、人工知能(AI) モノのインターネット(IoT)プラットフォームでエネルギー使用量を最適化し、バッテリーのパフォーマンスを監視し、ライフサイクルの効率性を拡張します。 この傾向は、より大きな採用を運転しています電気自動車(EV)ユーザーとエネルギー貯蔵事業者

- 例えば、NIOやGogoroなどの企業は、ユーザーの行動、充電サイクル、およびグリッドの要求を評価するために、バッテリースワップネットワークでAI搭載予測分析を組み込んでおり、よりスマートなエネルギー分布とコスト効率性を実現

- AI ベースのソリューションにより、サービスプロバイダはメンテナンスニーズを予測し、突然の故障を防ぎ、リアルタイムのインサイトをバッテリーヘルスに提供し、IoT 接続により、リモート監視と EV 艦隊とのシームレスな統合が可能になります。

- インテリジェントで接続されたBaaSプラットフォームへのこのシフトは、利便性、コストの透明性、信頼性を提供し、ユーザーの期待を再定義しています。

- 企業は、ユーザーの信頼を強化し、運用効率を向上させるために、スマートでAI対応のBaaSソリューションにますます投資し、電気化に向けた広範なシフトをサポートしています

- 予測、AI主導、IoT統合型BaaSモデルの需要が高まっています。今後数年間でEVおよび再生可能エネルギーアプリケーションにおける採用の加速が期待されています。

サービス市場としてのバッテリーのキードライバーは何ですか?

- 電動車両(EV)の普及が進んでおり、グリーンモビリティを推進する政府のインセンティブと相まって、サービス市場としてのバッテリーの第一次ドライバーです。

- たとえば、2024年、GogoroはEnel Xと提携し、欧州におけるバッテリー交換インフラを拡大し、スケーラブルで費用対効果の高いソリューションによるEV導入の加速を目指しています。

- EV バッテリーのコストが高いため、初期購入価格を下げ、サブスクリプションベースのオーナーシップモデルに移行することで、BaaS は魅力的なオプションになります。 この手頃な価格の要因は、個々の消費者とフリートのオペレータのための重要な有効化装置です

- 持続可能な公共および商業輸送のための都市化そして要求を育てることはBaaSの採用を、それ減らされたダウンタイムおよび容易な電池の取り替えを保障します高めます

- バッテリー交換、予測可能なサブスクリプションコスト、およびエネルギー貯蔵統合のサポートの利便性は、市場を前方に推進しています。

- また、循環型経済モデルに重点を置き、使用される電池のリサイクルは、サービスソリューションとしてのバッテリーの持続可能性のアピールを強化しています。

バッテリーの増大をサービス市場としてチャレンジする要因は?

- 大規模バッテリー交換ステーションとサービスネットワークの確立に伴う高インフラコストは、市場拡大の大きな障壁を維持

- 例えば、東南アジアの複数のEVスタートアップが、首都圏の要件が高まるため、スワップネットワークを拡大し、都市圏を超えた採用を制限するのに苦労しています。

- 異なるEVメーカー間でバッテリー標準化に関する問題は、相互運用性の欠如がスケーラビリティを制限し、クロスブランドの採用を損なうため、別の課題をポーズします

- スワップステーションの信頼性と可用性に関する消費者の懐疑的、特に開発されていない地域では、採用ハードルを追加します。

- 加えて、リチウム、ニッケル、コバルトの原料価格の変動は運用コストを増加させ、サービス価格の安定化を低減

- これらの課題を克服することは、EVメーカー、政府、エネルギープロバイダーの間でより大きなコラボレーションを必要とし、標準化されたプラットフォームを構築し、インフラを拡大し、長期の手頃な価格を保証します。

バッテリーは、サービス市場としてどのように区分されますか?

市場はサービス タイプに基づいて区分されます、エネルギー貯蔵容量, アプリケーションとエンドユーザー.

- サービスタイプ別

サービスタイプに基づき、サービス市場としてのバッテリーをサブスクリプションモデルと有料モデルに分割します。 サブスクリプションモデルセグメントは、2024年に61.4%の最大の収益シェアで市場を支配し、予測可能なコスト構造と個々のEV所有者とフリートオペレータの利便性によって駆動しました。 サブスクリプションは、顧客が必要に応じてバッテリーを交換したりアップグレードしたり、柔軟性を高め、高い所有権コストの負担を軽減することができます。 EVリースプログラムや政府によるサブスクリプションパイロットの人気が高まっています。このモデルの優勢さをさらにサポートしています。

パーユースモデルは、2025年から2032年まで22.1%の最速のCAGRを目撃することを期待しています。これは、長期的な約束なしにオンデマンドサービスを好むユーザーのための費用対効果を提供します。 共有モビリティサービス、乗り継ぎフリート、地域に限らず、インフラの拡大を図っています。 その魅力は、新興市場のための手頃な価格、スケーラビリティ、適合性にあります。

- エネルギー貯蔵容量によって

蓄電容量に基づき、サービス市場としてのバッテリーを50kWh、50~100kWh、100kWh以上に分割します。 50-100 kWhセグメントは、主に主流電気自動車、二輪車、軽商用車への適合性のために、2024年に最大48.7%の収益シェアを占めています。 この容量範囲は、範囲、コスト効率、および充電/スワッピングの利便性のバランスを提供し、消費者とフリートの両方のオペレータによって最も広く採用されています。

2025年から2032年にかけて最も速いCAGRを目撃し、大型トラック、バス、長距離電気自動車の採用を増加させることで燃料を供給する。 商業用物流と都市間輸送により、電気化に向け、大容量バッテリーサービスが高まり、耐久性と運用効率の要件を満たす必要があります。 高容量バッテリー交換ステーションへの投資を増加させ、このセグメントをさらに加速します。

- 用途別

用途に応じて、サービス市場としてのバッテリーはエネルギー貯蔵、自動車・輸送、産業用途、その他に分けられます。 自動車及び輸送の区分は2024年に55.2%の最大の収益のシェアと、特に都市のモビリティ、公共交通機関、および配達サービスで電気車両の採用のサージによって運転しました。 BaaSは、高バッテリーのコストと充電遅延に関する消費者の懸念に対応し、自動車業界にとって魅力的なソリューションです。

2025年から2032年までの21.8%の最も速いCAGRを目撃するエネルギー貯蔵の区分は、再生可能エネルギーの統合および格子安定性を高める役割によって支えられます。 ユーティリティプロバイダとエネルギー会社は、モジュール式ストレージユニットをデプロイするBaaSモデルを採用し、柔軟性とコスト削減を実現します。 このトレンドは、クリーンエネルギーと分散型発電に向けたグローバル・プッシュと密接に連携しています。

- エンドユーザーによる

エンドユーザーに基づいて、サービス市場としてのバッテリーは、自動車、通信、エネルギーおよびユーティリティ、住宅、商業および産業に分けられます。 自動車部門は、2024年に最大58.6%の市場収益シェアを占め、EVの普及とコスト節約、サブスクリプションベースのバッテリー所有権の好みによって燃料を供給しました。 EVメーカーおよびモビリティサービスプロバイダは、BaaS事業者と提携し、ユーザーの利便性を高め、採用を加速します。

テレコム企業は5Gタワーおよびデータセンターのバックアップ電力ソリューションのためのBaaSを採用しているため、通信部門は2025から2032までの22.9%の最速のCAGRで成長することが期待されます。 高速ネットワーク接続を維持するための信頼性の高い、無停電電力の必要性は、この分野での需要を駆動しています。 電気通信事業者とエネルギーサービスプロバイダ間のパートナーシップは、このアプリケーションをさらに拡大するなどです。

どの地域は、サービス市場としてバッテリーの最大のシェアを保持していますか?

- アジア・パシフィックは、2024年に42.5%の最大の収益シェアを誇るサービス市場としてバッテリーを占拠し、急速な都市化、電気自動車の普及、および支援政府の主導により、バッテリー交換インフラを奨励しています。 中国、日本、インドなどの国々は、その強力な製造生態系の拡大、EVフリートの拡大、持続可能なエネルギーソリューションに重点を置いています。

- 地域内の消費者は、特にEV貫通が急激に上昇する人口密度の高い都市エリアで、バッテリーが提供するコスト効率、柔軟性、および充電ダウンタイムに描画されます

- 有利な政策、EV技術のローカルイノベーション、および地域の選手の優位性は、BaaSの採用のためのグローバルハブとしてアジア太平洋を置き、業界最大かつ最も影響力のある市場に形成しました

サービスの市場洞察として中国電池

2024年にアジア・パシフィックで最大68%の収益率を占めるサービス市場としての中国バッテリーは、広大なEVユーザーベース、強力な政府のバックアップ、およびバッテリー・スワッピングステーションの大規模ロールアウトによって燃料を供給しました。 NIO や CATL などの国内巨人の実績と、手頃な価格のサブスクリプションモデルが採用を加速しています。 国のスマートシティのイニシアチブと共有モビリティサービスの好みは、市場拡大を推進します。

サービス市場インサイトとしてのジャパンバッテリー

サービス市場としての日本電池は、国家の先進技術インフラを主導し、EV貫通を成長させ、予測期間中に重要なCAGRで成長することを期待しています。 日本の高齢化の人口と信頼性、安全性、利便性を重視し、シームレスなバッテリースワッピングソリューションの需要を燃料供給しています。 接続されたデバイスとスマートモビリティサービスを備えたBaaSの統合も、住宅と商業分野における採用を強化しています。

インド バッテリー サービス市場 Insight

サービス市場としてのインドバッテリーは、都市化、EV導入のための政府の補助金、および2輪車と3輪車EVセグメントをブームさせることにより、堅牢な成長を目撃しています。 スタートアップやローカルメーカーは、低コストでスケーラブルなバッテリースワッピングネットワークに投資し、手頃な価格のモビリティの需要に応えています。 車両の排出削減と、BaaS導入のさらなる強化に重点を置いています。

どの地域が最も急速に成長する地域をバッテリーサービス市場として?

サービス市場としての北米バッテリーは、2025年から2032年までの10.6%の最速のCAGRで成長し、EV導入の加速、環境意識の上昇、およびインフラの充電と交換の強力な投資によって推進されています。 米国とカナダの消費者は、コスト効率の高いエネルギーソリューションを優先していますが、フリートオペレータは、ダウンタイムと予測可能なサブスクリプションベースの所有権モデルの恩恵を受けています。

米国のバッテリーをサービス市場インサイトとして

米国の市場は、2024年に北米の収益シェアの約79%を占め、EVの普及、サブスクリプションサービスの強力な消費者好み、および自動車メーカーとエネルギープロバイダー間のコラボレーションを成長させました。 EVインフラを支える連邦イニシアチブは、コネクティッドテクノロジーの広範な採用と組み合わせ、米国を地域の主要な成長エンジンとして位置付けています。

カナダのバッテリーをサービスマーケットインサイトとして

サービス市場としてのカナダバッテリーは、そのクリーンエネルギー政策、EV導入のための政府補助金によって燃料を供給し、持続可能な輸送ソリューションに重点を置いて、勢いをあげています。 長距離EVの需要が高まっています。都市の移動インフラの投資と相まって、ユーティリティとモビリティサービスプロバイダが柔軟なバッテリースワッピングモデルを採用しています。

バッテリーのトップ企業は、サービス市場ですか?

サービス業界としてのバッテリーは、主に、以下のような広範な企業によって供給されています。

- NIO(中国)

- VinFast(ベトナム)

- Lectrix E-Vehicle Pvt. Ltd (インド)

- ゴゴゴロ(台湾)

- マヒンドラ&マヒンドラ株式会社(インド)

- ヒュンダイ モーター会社(韓国)

- 株式会社XPENG(中国)

- バウンスインフィニティ(インド)

- ヤマハモーター株式会社(日本)

- SAICモーター株式会社(中国)

- Vinson Green Technologies(マレーシア)

- 日産自動車株式会社(日本)

サービス市場としてのグローバルバッテリーの最近の発展は何ですか?

- 2025年1月、JSW MG Motor Indiaは、Kotak Mahindra Prime(India)と提携し、EVの所有コストを削減し、販売を奨励することを目指し、バッテリーの資金調達ソリューションを提供しました。 インドの消費者にとってEV導入がより経済的にアクセスできると予想される

- 2024年12月、マヒンドラ&マヒンドラ株式会社(インド)の子会社であるLast Mile Mobility(Last Mile Mobility)は、電気自動車向けサービスプログラムとしてバッテリーを発売し、マヒンドラのZEO(4W)、ザーグランド、トレオプラス(3W)などのモデルをカバーしています。 このイニシアチブは、EVの所有権の障壁を大幅に低下させ、インドの成長するモビリティセクターの売上高を増加させることを期待しています

- MG Motor Indiaは、2024年9月に、Vidut(インド)と手を組み、乗用車用の新しい融資モデルをロールアウトし、MG Comet EV、MG Windsor EV、MG ZS EVなどのEVサービスオプションとして電池を統合しました。 このコラボレーションは、インドでのEV導入を迅速化し、有益性を高め、

- 2024年8月、VinFast(ベトナム)は、VF5電気自動車のフィリピンのバッテリーサブスクリプションモデルを導入し、顧客は高額なコストを支払うのではなく、バッテリーをリースすることができます。 このアプローチは、東南アジア市場でより魅力的で経済的に活気のあるEVを作るように設計されています

- 2024年7月、ヒュンダイ・モーター・カンパニー(韓国)は、韓国で2025年計画された初期の可用性で、電気自動車に縛られた新しいサブスクリプションサービスを発表しました。 現在、その実証フェーズでは、本プログラムは、フル導入後、ヒュンダイのEV戦略を強化することが期待されています。

- 2024年4月、VinFast(ベトナム)は、インドネシアのバッテリーサブスクリプションポリシーを立ち上げ、バッテリーの健全性および長期メンテナンスコストに関する消費者の懸念に対応しました。 このプログラムは、消費者の信頼を高め、地域におけるEVの採用を促進するために配置されます

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。