グローバルバイポーラ処理市場規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

5.47 Billion

USD

6.72 Billion

2024

2032

USD

5.47 Billion

USD

6.72 Billion

2024

2032

| 2025 –2032 | |

| USD 5.47 Billion | |

| USD 6.72 Billion | |

| % | |

|

グローバルバイポーラ処理市場セグメンテーション、バイポーラディスオーダータイプ(バイポーラIとバイポーラII)、ドラッグクラス(抗凝集剤、抗不安剤、気分安定剤、抗精神薬、抗うつ病剤、その他)、行動のメカニズム(選択的セロトニン抑制剤、セロトニンノレピュリンリアップテーク阻害剤、Tricyclic Antidepressants、モノアミンアミン阻害剤、その他)、行動のメカニズム(選択的セロトニン再取消毒剤、その他) 業界動向と予測 2032

Bipolar Disorderの処置の市場のサイズ

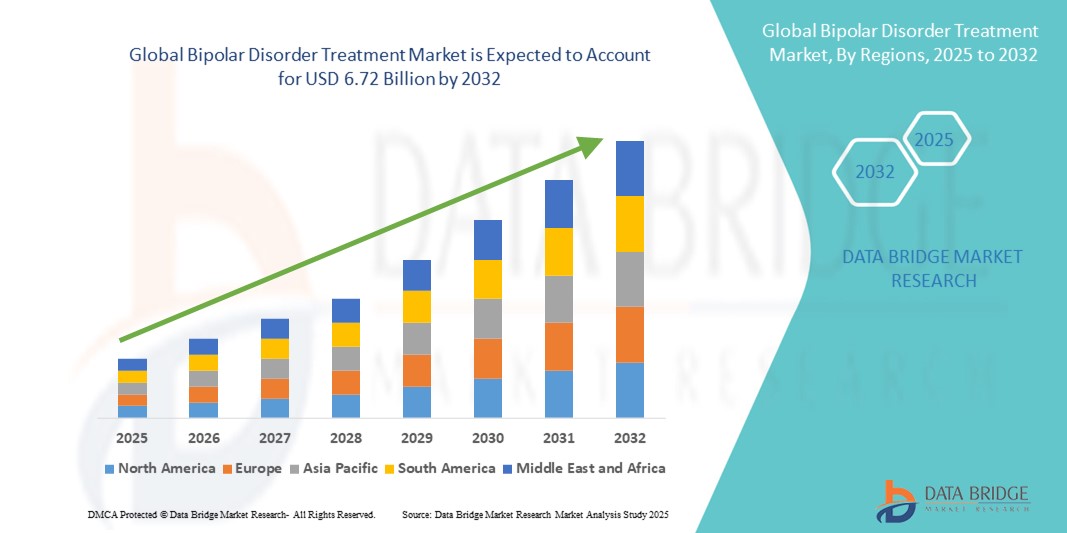

- 世界的な二極性の無秩序の処置の市場のサイズはで評価されました2024年のUSD 5.47億そして到達する予定2032年までのUSD 6.72億, お問い合わせ2.60%のCAGR予報期間中

- 市場成長は、主に双極性障害の上昇優先順位によって駆動され、精神的な健康状態の意識を高め、開発および新興国における精神科ケアへのより大きなアクセス

- さらに、高度薬理学療法の高度化の採用は、典型的な抗精神薬および気分安定装置のような、革新的な処置のアプローチの投資を拡大し、市場拡大を支えます。 これらの結合要因は有効で、忍耐強い中心の処置の解決のための推進の要求です、それによってかなり双極性の無秩序の処置の企業の成長を高めます

Bipolar Disorderの処置の市場分析

- 双極性障害の治療、薬理療法、心理療法、および新興のデジタル介入を網羅するバイポーラ疾患は、気分の揺れを安定させ、再燃を防ぎ、多様な臨床設定で生活の忍耐強い品質を向上させることを目的とした精神医療の重要な分野です

- 効果的な治療に対する増加の需要は、主に精神的健康障害の増大率によって駆動され、意識キャンペーンの増加、診断率の向上、慢性精神疾患の長期的管理へのシフト

- 北アメリカは2024年に41.8%の最大の収益分配で二極性障害治療市場を支配し、高い精神的健康意識、強力な医療インフラ、有利な償還方針、および主要な製薬会社の存在が積極的に新しい治療に投資しました

- アジア・パシフィックは、予報期間中にバイポーラ障害治療市場で最も急速に成長する地域であることが期待され、ヘルスケア支出の増加、精神科ケアへのアクセス拡大、政府やNGO主導の精神医療への取り組みが増加しています。

- 抗精神薬のセグメントは、2024年に45.1%の市場シェアでバイポーラ障害治療市場を支配し、急性マニアを管理し、再燃率を削減し、開発市場における第一線治療として広く処方されている

報告書 スコープおよびバイポーラの分解の処置の市場区分

| アトリビュート | Bipolar Disorderの処置のキー マーケットの洞察 |

| カバーされる区分 |

|

| カバーされた国 | 北アメリカ

ヨーロッパ

アジアパシフィック

中東・アフリカ

南米

|

| 主要市場プレイヤー |

|

| マーケットチャンス |

|

| 付加価値データインフォセットを追加 | 市場価値、成長率、セグメンテーション、地理的カバレッジ、主要なプレーヤーなどの市場シナリオに関する洞察に加えて、Data Bridge Market Researchがキュレーションする市場レポートには、詳細なエキスパート分析、価格設定分析、ブランドシェア分析、消費者調査、デモグラフィ分析、サプライチェーン分析、バリューチェーン分析、原材料/消耗品の概要、ベンダー選定基準、PESTLE分析、ポーター分析、規制フレームワークが含まれます。 |

Bipolar Disorderの処置の市場の傾向

パーソナライズされたデジタルメンタルヘルスソリューションへのシフト

- 世界的な二極性障害治療市場での有意で加速傾向は、デジタル精神的健康プラットフォームと望遠によって支えられたパーソナライズされた治療アプローチに成長している焦点です。 このシフトは、アクセス、遵守、および患者の成果を改善しています。

- たとえば、TalkspaceやBetterHelpなどのデジタルプラットフォームは、仮想精神科の相談を提供しており、バイポーラ障害のある患者が適時薬物管理と治療を受けることを可能にします。 同様に、企業が気分変動を監視し、早期再燃アラートを提供するAI対応アプリを開発しています。

- 精密精神医学およびバイオマーカーの研究の進歩により、よりターゲットを絞った療法、個々の忍耐強いプロフィールに薬および心理療法の組合せを合わせることを可能にし、それによって処置の有効性を改善し、副作用を減らします

- ウェアラブルデバイスとスマートフォンアプリの統合により、睡眠、気分、アクティビティの継続的な監視が可能になり、精神科医がデータ主導の調整を行なうことができます。

- デジタル、パーソナライズ、コネクティッドケアへのこの傾向は、精神的医療の配信に対する期待を根本的に再構築し、製薬企業やデジタルヘルスのスタートアップをプッシュして、ハイブリッド治療モデルのコラボレーション

- 医薬品とデジタルソリューションを統合する需要は、開発市場と新興市場の両方で急速に成長しています。患者やプロバイダは、ますますます価値のアクセシビリティ、ケアの継続性、リアルタイム監視機能として

Bipolar Disorderの処置の市場 動的

ドライバー

精神健康障害の有利化と拡大意識

- 双極性障害の世界的な優先順位を上げ、国民の認知度を高め、早期診断のイニシアチブと相まって、効果的な治療のための需要の重要なドライバーです。

- たとえば、2024年、WHOは、世界規模の障害者のトップ20の原因のうち、偏光性障害を強調し、スケーラブルな治療ソリューションの緊急の必要性を強調した。 国際機関によるそのような認識は、新しい治療法や医療インフラへの投資を燃料化しています

- 精神疾患の悪化と国民医療制度における精神科サービスの包摂へのシフトは、治療への患者のアクセスを拡大しています

- さらに、副作用の少ない次世代抗精神薬の開発など、医薬品の進歩は、採用を促進しています

- サポートケア、ライフスタイル管理、デジタル監視ツールによる治療の統合により、さまざまなヘルスケア設定で患者のコンプライアンスと結果を高めることで、より包括的な治療を実現

拘束/チャレンジ

副作用、再燃リスク、規制バリア

- 双極性障害治療市場のための主要な課題は、薬物関連の副作用、再燃のリスク、および精神科薬の厳しい規制要件の持続性です

- 例えば、一般的に、リチウムや特定の抗精神薬などの薬を処方することは、体重増加、甲状腺機能障害、または心臓血管の問題を引き起こす可能性があり、長期密着性を損なう

- 持続的な薬物使用および連続的な療法への限られたアクセスによる再燃率は高く、有効な病気管理にハードルを投げます

- 新しい精神科薬を承認するための規制ハードル, 長い臨床試験のタイムラインと相まって, 革新的な治療法の可用性を遅く

- また、長期治療の費用は、市場浸透を制限する低所得国および中所得国における患者にとって禁止することができます。 ジェネリック医薬品は手頃な価格を向上させながら、先進的な療法とデジタルサポートへのアクセスは、世界中に不均一です

- 薬物の革新、より強い忍耐強い忍耐強い教育、テレメディシンの採用および政策レベルの介入によってこれらの障壁を克服することは支持された市場成長のために重要になります

Bipolar Disorderの処置の市場規模

市場は、バイポーラ障害タイプ、薬物クラス、行動のメカニズム、管理のルート、エンド ユーザー、および配分チャネルに基づいてセグメント化されます。

- バイポーラの注文のタイプ

タイプに基づいて、バイポーラの無秩序の処置はバイポーラIおよびバイポーラIIに分けられます。 Bipolar Iの区分は2024年に市場を、pharmacotherapy、緊急の心配および頻繁な入院を必要とする急性のマニカルのエピソードのより高い率によって支えられた支配しました。 ペイアの注意と臨床ガイドラインは、多くの場合、マニアの安定化を優先順位付けします。, 抗精神薬および気分安定装置のための支持需要は、一般的にバイポーラIで使用される. より大きい診断可視性およびtertiaryの中心の確立された心配の経路は更に利用を補強します。 ファーマパイプラインは、抗マニカルの有効性を持つ代理店に向けるだけでなく、バイポーラIに商業的な焦点を持続します。 インパティエントおよび集中的なアウトパティエンプログラムでは、このサブタイプにリンクされた有意義な収益ストリームを追加します。

バイポーラIIセグメントは、2025年から2032年までの最速成長を目撃し、第一次ケアと望遠における低マニアのスクリーニングと抑圧優勢の優先順位を改善することによって推進されています。 混合機能とソフトバイポーラスペクトラムの臨床医の意識を高めることで、ケース識別が広くなります。 Bipolar IIで一般に使用されるデジタル監視および心理療法のadjunctsと連続的な、不足分の管理のための忍耐強い好みは一直線に合わせます。 stigma が減少するにつれて、以前のヘルプ・シークは治療の開始と遵守を改善します。 ガイドラインは、急性マニアを超えて縦方向の気分安定化を強調し、対象となる人口を拡大します。

- ドラッグクラス

薬物クラスに基づいて、双極性障害治療は、抗凝集剤、抗不安剤、気分安定剤、抗精神薬、抗鬱剤、その他に分けられます。 抗精神医学のセグメントは、2024年に45.1%の市場シェアで市場を支配し、急性マニアとメンテナンス、広範なラベルのカバレッジ、および臨床医の精通のための最初のラインの役割を反映しています。 二次世代の抗精神薬は急速な徴候制御を提供し、経口および長期作用の注射可能な形態で広く利用できます。 好ましい式位置決めと広範な現実世界証拠サポート継続使用. 気分の安定装置との組合せ療法は複雑な場合の持続性を高めます、容積をボルスタリングします。

気分安定器セグメントは、最も速い成長を目撃し、古典的なエージェント(例えば、リチウム、valproate)の最適化と長期再燃防止に使用される新しいオプションによって推進されることが期待されます。 自殺リスクの低減と、リチウムリフトガイドラインの過敏の神経保護の可能性に重点を置いた臨床をリニューアルしました。 治療薬の監視の進歩およびデジタル付着力用具は許容およびpersistenceを改善します。 新興市場では、費用対効果の高いジェネリックが公共システムへのアクセスを拡大します。 SGA による気分安定装置を組み合わせたコンビネーション戦略は、患者のカバレッジを広げています。

- 行動のメカニズムによって

メカニズムに基づいて、バイポーラ障害治療は、選択的セロトニン抑制剤(SSRI)、セロトニンノレピネフリンリアップテーク阻害剤(SNRI)、Tricyclic Antidepressants、モノアミンオキシダーゼ阻害剤、ベンゾジアゼピン、およびベータブロッカーに分けられます。 SSRIs のセグメントは、2024 年に最大のシェアを保持しました。, 気分安定装置コセラピーとバイポーラのうつ病の広範な使用によって支持されています。, 広範な処方熟知, 有利な償還. 彼らの比較的良性安全プロファイル対TCA/MAOIsと豊富な一般的な可用性ドライブの採用。 プライマリケアの医師は、精神科の指導の下にあるSSRIsを開始し、処方者ベースを拡大しています。 ポストマーケティングデータとガイドラインのオンゴングは、自信を維持します。 複雑な不安と強迫的な症状の彼らの役割は、さらなる利用率を高めます。

SNRISセグメントは、治療耐性のうつ病期およびエネルギーや認知などの機能的結果の有効性によって支えられ、最速で成長する予定です。 測定ベースのケアディフューズとして、臨床医はSNRIが恩恵を受ける可能性がある症状領域に向かってレジメンを仕立てます。 気分安定剤による共演に関するより良い教育は、スイッチリスクを軽減し、使用を奨励します。 ジェネリックペネトレーションの拡大は、価格に敏感な市場での手頃な価格性を高めます。 リアルワールドのデータレグニストは、選択された患者で有利な結果を集め、ニュアンスされた採用を導きます。 このエビデンス主導の患者主導のアプローチ燃料は、SNRIの蓄積を加速しました。

- 行政のルートで

経路に基づいて、バイポーラ障害の治療は、経口、括弧、その他に分けられます。 口腔セグメントは、2024年に市場を支配し、メンテナンス療法および急性設定からステップダウンケアのためのタブレット/カプセルの普及を反映しています。 口腔投薬は、柔軟で広範な汎用性、高い患者様の受け入れをサポートします。 ファーマシーズとテレヘルスモデルは、すぐに偽りをしたり、経口レジメンを配信したり、付着力を上げます。 健康システムは、コストの消費とスケーラビリティのための経口オプションを好む。 広範なガイドラインの裏付けと臨床医の習慣は、さらなるエントレンチ経口療法を習慣します。 その結果、口腔は、慢性双極管理の大部分のアカウントをルーティングします。

慣性セグメント(著しく長時間作用する注射可能な)は、付着力の利点によって駆動され、再燃/出血リスクを削減し、最も急速に成長することが期待されています。 LAIの抗精神医学は安定した血漿レベルおよびより少ない医院の訪問を可能にしましたり、価値に基づくケアの目的と一直線に並べます。 ペイアーズは、カバレッジを改善し、少数の急なエピソードから下流の節約を認識し、ますます認識しています。 統合コミュニティメンタルヘルスプログラムは、LAIを効率的に管理し、アクセスの幅を広げることができます。 新製品の発売および拡大された徴候は臨床医の信任を高めます。 付着力は根本的なアンメットの必要性のままに、LAIsは加速の採用を見ます。

- エンドユーザーによる

エンドユーザーに基づき、バイポーラ障害の治療は、病院、ホームケア、専門クリニック、その他に分けられます。 病院は、急性マニアの治療、緊急入場、複雑なレジメンの開始の集中による2024年に市場を支配しました。 複数の分野のチームおよび診断資源は急速な安定化およびcomorbidity管理を可能にします。 病院はまた臨床試験を固定し、規準のパターンを形づけるガイドラインのdisseminationを導きます。 排出計画は頻繁に種子の長期外来療法を排出し、下流利用に入院ケアをリンクします。 償還メカニズムは、通常、より高いレベルの介入をサポートし、収益を持続させます。 したがって、病院は、ケア経路と市場キャプチャにピボタルを維持しています。

専門医は、外来患者、縦方向管理、協調ケアへのシフトを反映し、最速成長を目撃する見込みです。 これらのセンターは、精神科医主導の薬物管理、心理療法、および1つの屋根の下のデジタル監視を提供し、遵守と結果を改善します。 より短い待ち時間と両極スペクトル障害のためのカスタマイズされたプログラムは、患者を引き付けます。 鍼灸治療の受診と受診の軽減は、クリニックモデルを強化します。 Telepsychiatry インテグレーションは、保護されたエリアへのアクセスを拡張します。 地域密着型のケアにピボットする医療システムとして、専門クリニックは急速に拡大しています。

- 流通チャネル

流通チャネルに基づいて、二極障害治療は、病院薬局、オンライン薬局、小売薬局に分けられます。 病院薬局の分野は、2024年に最大のシェアを保持し、入学および調整された排出分配の間に治療の開始によって固定されています。 複雑なレジメン、制限薬、およびLAI管理は通常、病院薬局によって管理されます。 入院式との強い統合は容積を運転します。 放電時のファーマシスト主導のカウンセリングは、ケアの移行、チャネルの好みの補強をサポートしています。 臨床統治および在庫管理は重要な薬物の可用性を保障します。 その結果、病院薬局は重要な治療の瞬間に相当する価値を捉えます。

オンライン薬局のセグメントは、最も速く成長するために計画されています。, テレ精神医学の拡張によって推進, 電子処方, そして、付着力を向上させるための戸棚配達. サブスクリプション補充とリマインダーは、慢性療法のギャップを減らします。 ジェネリックおよび控えめなサービスに関する競争力のある価格設定は、シグマを管理する患者にアピールします。 デジタルプラットフォームは、薬物情報、副作用の追跡、および薬剤師のチャットを統合し、患者の経験を強化します。 多くの地域での電子薬局の規制対応は、ポストパンデミックを強化しています。 デジタルケアが正常化するにつれて、オンライン薬局はメンテナンス薬を介した重要な増分率を得ることができます。

Bipolar Disorderの処置の市場地域分析

- 北アメリカは2024年に41.8%の最大の収益分配で二極性障害治療市場を支配し、高い精神的健康意識、強力な医療インフラ、有利な償還方針、および主要な製薬会社の存在が積極的に新しい治療に投資しました

- 地域における患者は、先進的な療法、有利な償還方針、早期診断および双極障害の長期的管理を促す啓発キャンペーンへの広範なアクセスから恩恵を受ける

- デジタルヘルスプラットフォーム、テレ精神医学、および長時間作用の注射可能な抗精神薬の広範な採用により、治療の可用性と遵守率が向上

U.S. バイポーラの分解の処置の市場洞察

米国バイポーラ障害治療市場は、高診断率、広範なヘルスケアカバレッジ、主要な医薬品イノベーターの存在によって燃料を供給し、北米における2024年に最大83%の収益シェアを獲得しました。 患者は高度の薬理学療法、心理療法のアクセスおよび遠隔監視および望遠療法を支えるデジタル健康のプラットホームの急速なアップテークからのますます寄与します。 精神科治療を覆うメディケアやメディケアなどの民間保険者や政府プログラムの強力な役割は、より広範なアクセスを保証します。 また、新規のムードスタビライザーや長時間作用の注射剤の臨床試験やFDAの承認は、さらなる市場拡大を推進しています。

ヨーロッパバイポーラ障害治療市場インサイト

欧州の両極性疾患治療市場は、国家精神保健プログラム、成長意識キャンペーン、および支持的な政府の償還方針によって主に運転された予測期間中に実質的なCAGRで拡大することを計画しています。 都市のストレスレベルやライフスタイルの変化を増加させ、効果的なバイポーラ療法の需要が高まっています。 欧州の患者は、広範囲にわたる精神科のインフラ、学術研究のパートナーシップ、および統合されたコミュニティクリニックなどの革新的な治療のデリバリーモデルからも恩恵を受けています。 再燃防止および長期管理のためにますます普及するデジタル監視のプラットホームがinpatientおよびoutpatientの心配のまわりで採用は増加しています。

U.K. Bipolar Disorderの処置の市場洞察

英国バイポーラ障害治療市場は、国家保健サービス(NHS)の取り組みが支援し、精神科サービスへのアクセスを拡大し、精神的健康状態を低下させるための注目すべきCAGRで成長することを期待しています。 早期診断や治療のアップテークを改善し、「タイム・トゥ・チェンジ」などの意識キャンペーンをライジング。 テレ精神医学とデジタル処方プラットフォームの国の成長の採用は、治療の配信を合理化しています。 さらに、臨床研究への強い参加とジェネリックへのアクセスは、英国の成長軌道を強化し、手頃な価格とイノベーションの両方に貢献します。

ドイツ・バイポーラ・ディフューザー・マーケット・インサイト

ドイツのバイポーラ障害治療市場は、国の強力な医療インフラ、普遍的な保険のカバレッジ、精神科研究に重点を置いて、予測期間中にかなりのCAGRで拡大することが期待されています。 ドイツは革新的で持続可能な医療ソリューションに焦点を合わせ、先進の薬理学療法と統合されたデジタルツールの採用をサポートしています。 長時間作用性注射剤の増大使用, 精密精神医学およびバイオマーカーベースの診断の投資と組み合わせ, 治療の効率性を高めます. 患者のプライバシーと安全なデジタルヘルスアプリケーションに重点を置き、国の厳格な規制基準に適合します。

アジア・パシフィック・バイポーラ・ディスオーダー・トリートメント・マーケット・インサイト

アジア太平洋二極障害治療市場は、2025年から2032年の間に23%の最も速いCAGRで成長し、精神的な健康意識、政府主導のデジタル健康への取り組み、中国、日本、インドのヘルスケア支出を増加させることによって燃やされます。 急速な都市化と変化するライフスタイルは、精神的な健康の負担を増加させ、治療ソリューションの需要を高めることに貢献しました。 ジェネリック医薬品の有用性や、テレプシキアトリー採用の高まりは、農村人口と都市人口の両方で治療をよりアクセス可能にします。 APACにおける医薬品の拡大と研究開発のコラボレーションにより、治療の可用性と有用性を強化します。

ジャパン・バイポーラ・ディスオーダー・トリートメント・マーケット・インサイト

日本バイポーラ障害治療市場は、先進医療インフラ、研究に重点を置き、デジタルヘルス技術の急速な採用により勢いを増大しています。 診断率の上昇、特に若い人口の中では、効果的な治療のための燃料消費需要です。 日本は、薬理学療法とテクノロジー対応のモニタリングと統合する包括的なアプローチを強調しています。 老化人口は、単純化された、遵守しやすい治療法の要求も作成します。 デジタル精神健康アプリと精密精神医学の研究との統合は、さらなる成長をサポートすることが期待されます。

インドバイポーラディスオーダー治療市場インサイト

2024年にアジア・パシフィックで最大の収益シェアを占めるインドのバイポーラ障害治療市場は、拡大する医療アクセス、中級の人口の増加、そして精神的健康インフラを強化するための政府の取り組みに由来しています。 国民の精神保健プログラムの普及啓発キャンペーンやロールアウトは、診断と治療率を改善しました。 手頃な価格のジェネリック医薬品と現地の医薬品製造能力は、幅広い人口によりアクセス可能な治療を可能にします。 テレ精神医学のプラットフォームと電子薬局サービスの急速な拡大は、精神科のケアデリバリーのギャップを埋め、都市と農村の両方の設定で二極障害の治療の採用を著しく運転しています。

Bipolar Disorderの処置の市場シェア

バイポーラの無秩序の処置の企業は主に下記のものを含んでいる十分に確立された会社によって、導きます:

- ジョンソン&ジョンソンとその関連会社(米国)

- AbbVie Inc.(米国)

- Mallinckrodt(アイルランド)

- サン製薬工業株式会社(インド)

- Novartis AG(スイス)

- エンドウ医薬品 plc(アイルランド)

- Zydus Cadila(インド)

- マインファーマグループリミテッド(オーストラリア)

- ティバ製薬工業株式会社(イスラエル)

- アムニール製薬株式会社(米国)

- Avet Pharmaceuticals Inc.(米国)

- ランネット(アメリカ)

- Aurobindo Pharma(インド)

- Wockhardt(インド)

- Currax Pharmaceuticals LLC(米国)

- アストラゼネカ(イギリス)

- F.ホフマン・ラ・ロチェ株式会社(スイス)

- リリーUSA、LLC(米国)

グローバルバイポーラ処理市場における最近の発展は何ですか?

- 2025年8月、BioXcel Therapeuticsは、BXCL501(Igalmi)の事前補完ニュードラッグアプリケーション(Pre-sNDA)会議に従ったFDAから正式な書面によるフィードバックを受けました。 目的: 双極性障害または schizophrenia の患者の急性攪拌の処置の自宅での使用を拡大して下さい。 これは、分散型、患者管理の介入に対する潜在的なシフトを表します

- 2025年7月、米国食品医薬品局(FDA)は、CAPLYTA(lumateperone)の徴候の拡大を正式に含み、二極IおよびIIの無秩序に関連した憂鬱なエピソードを、モノセラピーとリチウムまたはvalproateとのadjunctive使用のために含んでいます。 この承認は、潜在的に改善された公差の双極性障害のうつ病相をターゲティングする多目的な非典型的な抗精神症としての潤滑油の進化の役割をアンダースコアします

- 2025年4月、Vanda Pharmaceuticalsは、Acute bipolar I障害およびschizophreniaの処置のためのFDAの承認を求めるiloperidoneの活動的な新薬剤の塗布、Bysanti (milsaperidone)のための新しい薬剤の塗布を、提出しました。 承認された場合、Bysantiは2026年まで米国で利用可能

- 2025年4月、NRx PharmaceuticalsはNRX-100のFDAからの速いトラックの指定を、防腐剤なしの静脈内ケタミンの公式受け取りましたり、うつ病の患者のsuicidalの思索を扱うことを目的としていました。 これは、急激な危機シナリオにおける命を救う介入のための緊急の必要性を強調します

- 2025年2月、Teva PharmaceuticalsとMedincellは、FDAがUZEDYのサプリメントニュードラッグアプリケーション(SNDA)を承認したことを発表しました。 RISPERIDONEの拡張放出可能な処方、双極I障害で成人のメンテナンス処理のために - schizophreniaのためにのみ承認しました。 この長時間作用性注射薬は、バイポーラI管理の既知の障壁、薬物不利を対処するのに役立ちます

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。