慢性うつ病性人格障害治療市場規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

1.70 Billion

USD

2.90 Billion

2024

2032

USD

1.70 Billion

USD

2.90 Billion

2024

2032

| 2025 –2032 | |

| USD 1.70 Billion | |

| USD 2.90 Billion | |

| % | |

|

慢性うつ病性人格障害(PD)治療の世界市場:作用機序別(選択的セロトニン再取り込み阻害薬(SSRI)、 三環系抗うつ薬(TCA)、セロトニン・ノルエピネフリン再取り込み阻害薬(SNRI)、薬剤別(アミトリプチリン、ブプロピオン、セルトラリン、 デュロキセチン)、診断別(身体検査、臨床検査、心理評価)、治療別(投薬、心理療法)、流通チャネル別(病院薬局、薬局、オンライン薬局)、エンドユーザー別(病院、在宅ケア、専門クリニック、その他) - 2032年までの業界動向と予測

慢性うつ病性人格障害治療市場規模

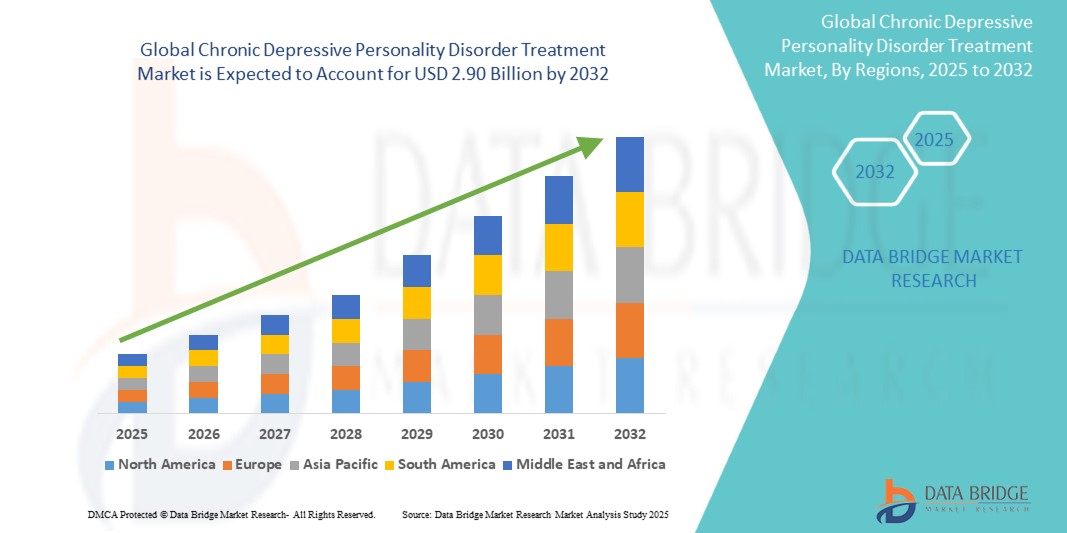

- 世界の慢性うつ病性人格障害治療市場規模は2024年に17億ドルと評価され、予測期間中に6.90%のCAGRで成長し、2032年には29億ドル に達すると予想されています 。

- 市場の成長は、うつ病の罹患率の増加、メンタルヘルスに関する意識の高まり、臨床および外来診療の両方における高度な薬理学的および非薬理学的治療アプローチの採用の増加によって主に促進されています。

- さらに、医療インフラの拡大、メンタルヘルス研究への投資の増加、そして個別化治療戦略への注目の高まりが、革新的な慢性うつ病性人格障害(CDPD)治療ソリューションの需要を促進しています。これらの要因が相まって、抗うつ薬、心理療法、デジタルメンタルヘルスプラットフォームといった効果的な治療選択肢の導入が加速し、慢性うつ病性人格障害治療市場の成長を大きく押し上げています。

慢性うつ病性人格障害治療市場分析

- 慢性うつ病性人格障害の治療市場は、メンタルヘルスに対する意識の高まり、慢性うつ病の有病率の増加、治療法の進歩により、世界的に大きな成長を遂げています。

- 慢性うつ病性人格障害の治療に対する需要の高まりは、主にメンタルヘルスへの意識の高まり、個別化された治療計画の採用、薬理学的および心理療法的介入の革新によって推進されている。

- 北米は、2024年には慢性うつ病性パーソナリティ障害治療市場において最大の収益シェア40.5%を占め、市場を席巻しました。これは、先進的な治療プロトコルの早期導入、医療費の高騰、そして主要な製薬会社やメンタルヘルスサービス提供者の強力な存在感を特徴としています。米国では、特に都市部において、既存のヘルスケア企業とAI支援療法や遠隔精神医学に注力するスタートアップ企業の双方によるイノベーションによって、治療導入が大幅に増加しました。

- アジア太平洋地域は、急速な都市化、可処分所得の増加、メンタルヘルス介入に対する意識の高まりにより、予測期間中に慢性うつ病性人格障害治療市場で最も急速に成長する地域になると予想されています。

- 医薬品は、その広範な採用、症状管理における一貫した有効性、および薬理学的介入に対する強力な臨床的サポートにより、2024年には55.6%という最大の市場収益シェアを占めました。

レポートの範囲と慢性うつ病性人格障害治療市場のセグメンテーション

|

属性 |

慢性うつ病性人格障害治療における主要市場洞察 |

|

対象セグメント |

|

|

対象国 |

北米

ヨーロッパ

アジア太平洋

中東およびアフリカ

南アメリカ

|

|

主要な市場プレーヤー |

|

|

市場機会 |

|

|

付加価値データ情報セット |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Chronic Depressive Personality Disorder Treatment Market Trends

Enhanced Patient Outcomes Through Innovative Therapeutics

- A significant and accelerating trend in the global chronic depressive personality disorder treatment market is the development and adoption of innovative therapeutic approaches aimed at improving patient outcomes. These include advancements in pharmacological treatments, psychotherapy techniques, and combined treatment regimens that address both depressive symptoms and underlying personality disorder traits

- For instance, recent clinical studies have highlighted the effectiveness of novel antidepressants and mood-stabilizing agents when used alongside cognitive-behavioral therapy (CBT) or dialectical behavior therapy (DBT), offering patients a more comprehensive treatment approach. Similarly, long-acting formulations are enabling more consistent symptom management, reducing the frequency of relapses and hospitalizations

- Ongoing research is focused on personalized treatment plans, where patient-specific factors such as genetics, comorbid conditions, and treatment history inform therapy selection. This individualized approach aims to enhance adherence, minimize side effects, and maximize therapeutic efficacy

- Integration of multidisciplinary care models allows psychiatrists, psychologists, and social workers to collaboratively manage patient care, addressing both psychological and social aspects of the disorder. Through coordinated care, patients can receive comprehensive support, from symptom management to lifestyle interventions and social rehabilitation

- This trend towards more patient-centered and evidence-based treatment options is fundamentally reshaping expectations in mental health care for CDPD. Consequently, pharmaceutical companies and mental health service providers are focusing on developing combination therapies, digital monitoring tools, and structured psychotherapy programs tailored for chronic depressive personality disorder

- The demand for effective, long-term, and individualized treatment solutions is growing rapidly across both clinical and outpatient settings, as healthcare providers and patients increasingly prioritize improved quality of life, functional recovery, and sustained symptom management

Chronic Depressive Personality Disorder Treatment Market Dynamics

Driver

Growing Need Due to Rising Awareness and Advancements in Treatment Options

- The increasing prevalence of chronic depressive personality disorder, coupled with growing awareness among healthcare providers and patients, is a significant driver for the heightened demand for effective treatment solutions

- For instance, in April 2024, leading pharmaceutical companies expanded their research programs for novel antidepressants and combination therapies aimed at improving long-term outcomes for patients with chronic depressive personality disorder. Such strategic initiatives are expected to drive the market growth over the forecast period

- As patients and clinicians become more aware of the benefits of early diagnosis and personalized treatment plans, the demand for innovative pharmacological interventions, including SSRIs, SNRIs, and tricyclic antidepressants, is rising. These treatments offer improved efficacy and reduced side effects compared to older medications, enhancing patient adherence and overall quality of life

- Furthermore, the growing adoption of integrated treatment approaches, combining medication with psychotherapy and digital health tools, is creating a more comprehensive care model for patients. Digital platforms for therapy management, remote consultations, and symptom tracking are increasingly being incorporated into patient care, further boosting market expansion

- The increasing focus on mental health awareness, patient education programs, and support networks are key factors propelling the adoption of chronic depressive personality disorder treatment solutions globally. Expanding access to affordable and clinically effective treatments in both developed and emerging regions further contributes to sustained market growth

Restraint/Challenge

Concerns Regarding Treatment Accessibility and Cost

- Limited access to specialized mental health services and trained professionals in certain regions poses a challenge to broader market penetration. Many patients, particularly in rural or underserved areas, may not receive timely diagnosis or appropriate therapeutic interventions

- For instance, disparities in healthcare infrastructure and the availability of antidepressant medications have made it difficult for some patients to consistently access treatment for chronic depressive personality disorder

- Addressing these challenges through initiatives such as telemedicine, mobile mental health apps, and government-supported mental health programs is crucial for expanding treatment access. In addition, the relatively high cost of certain advanced therapies and combination treatment plans can be a barrier for price-sensitive patients, especially in developing countries

- While the adoption of generic medications and increasing insurance coverage is gradually reducing costs, the perceived premium for specialized therapies can still hinder widespread treatment uptake

- Overcoming these challenges through improved healthcare infrastructure, expanded patient education, and the development of affordable, evidence-based treatment options will be vital for the sustained growth of the chronic depressive personality disorder treatment market

Chronic Depressive Personality Disorder Treatment Market Scope

The market is segmented on the basis of mechanism of action, drugs, diagnosis, treatment, distribution channel, and end-users.

• By Mechanism of Action

On the basis of mechanism of action, the chronic depressive personality disorder treatment market is segmented into selective serotonin reuptake inhibitors (SSRIs), tricyclic antidepressants (TCAs), serotonin and norepinephrine reuptake inhibitors (SNRIs) and others. The selective serotonin reuptake inhibitors (SSRIs) segment dominated the largest market revenue share of 47.2% in 2024, driven by their favorable safety profile, efficacy in long-term management, and widespread clinical adoption. SSRIs are often preferred as the first-line therapy due to lower side effects compared with TCAs and SNRIs, as well as their effectiveness in improving both depressive symptoms and overall patient functioning. The segment benefits from extensive clinical guidelines, physician familiarity, and strong patient adherence programs.

The serotonin and norepinephrine reuptake inhibitors (SNRIs) segment is expected to witness the fastest CAGR of 8.1% from 2025 to 2032, fueled by their dual action on serotonin and norepinephrine pathways, providing enhanced therapeutic effects for patients with treatment-resistant or comorbid depressive conditions. Growing awareness among clinicians and ongoing research on SNRIs’ efficacy and tolerability support this expansion. In addition, the increasing use of SNRIs in combination therapy regimens, and their ability to target multiple symptoms of chronic depressive personality disorder simultaneously, are further boosting adoption. Emerging clinical studies highlighting improved functional outcomes and lower relapse rates are also expected to contribute to sustained growth.

• By Drugs

On the basis of drugs, the market is segmented into amitriptyline, bupropion, sertraline, duloxetine and others. Sertraline dominated the largest market revenue share of 41.5% in 2024, owing to its proven clinical efficacy, favorable tolerability, and established presence in treatment guidelines. Sertraline is widely prescribed for both acute management and long-term therapy, benefiting from extensive physician confidence and patient familiarity.

Bupropion is expected to witness the fastest CAGR of 7.6% from 2025 to 2032, driven by its stimulating effect, lower sexual side effect profile, and suitability for patients with fatigue and low energy associated with chronic depressive personality disorder. Furthermore, increasing clinical evidence on Bupropion’s efficacy in managing comorbid anxiety and attentional deficits, along with its incorporation into personalized treatment plans, is expected to drive higher adoption rates across both hospital and outpatient settings. Rising patient awareness about side-effect profiles and improved adherence programs are further supporting market growth.

• By Diagnosis

On the basis of diagnosis, the market is segmented into physical exam, lab tests, psychological evaluation and others. Psychological evaluation dominated the largest market revenue share of 53.0% in 2024, owing to its critical role in assessing symptom severity, comorbidities, and personality traits. Psychological evaluation provides actionable insights for individualized treatment planning and monitoring therapeutic progress. The segment benefits from increasing use of standardized diagnostic tools and clinical guidelines across psychiatric practice.

Lab tests are expected to witness the fastest CAGR of 7.8% from 2025 to 2032, fueled by advances in biomarker research, genetic profiling, and the integration of laboratory diagnostics to support personalized medicine approaches in chronic depressive personality disorder management. In addition, the growing adoption of lab tests for early detection, monitoring treatment response, and identifying risk factors for relapse is contributing to rapid market expansion. Investments in advanced diagnostic technologies, including automated testing platforms and point-of-care devices, are expected to further accelerate growth.

• By Treatment

On the basis of treatment, the market is segmented into medication, psychotherapy and others. Medication dominated the largest market revenue share of 55.6% in 2024, due to its widespread adoption, consistent efficacy in symptom management, and strong clinical support for pharmacological interventions. Ongoing development of newer antidepressants and better safety profiles enhances physician confidence and patient adherence. In addition, increasing awareness campaigns and inclusion of medication management in clinical guidelines further reinforce the segment’s growth and adoption.

心理療法は、非薬物療法への認知度の高まり、認知行動療法や精神力動的アプローチの有効性、そして包括的なメンタルヘルス管理に対する患者の選好の高まりを背景に、2025年から2032年にかけて8.5%という最も高い年平均成長率(CAGR)を記録すると予想されています。遠隔療法やアプリベースの介入を含むデジタルプラットフォームの利用拡大、そしてメンタルヘルスケアへのアクセスを促進する支援政策は、心理療法の導入を加速させると予想されます。セラピスト向けの研修・認定プログラムも拡充され、専門的なケアへのアクセスが向上しています。

• 流通チャネル別

流通チャネルに基づいて、市場は病院薬局、小売薬局、オンライン薬局、その他に分類されます。病院薬局は、処方薬への集中的なアクセス、医師による監督、保険償還制度に牽引され、2024年には市場収益シェアの48.3%を占め、最大のシェアを占めました。病院は、体系的な治療計画と統合的なケアを提供し、服薬遵守と長期的な成果を支援しています。

オンライン薬局セグメントは、デジタル化の進展、患者の自宅配送への嗜好、処方箋の履行を容易にする遠隔医療プラットフォームの拡大を背景に、2025年から2032年にかけて9.2%という最も高いCAGRを達成すると予想されています。認証済みオンライン薬局に対する患者の信頼の高まり、慢性疾患治療のための柔軟なサブスクリプションモデル、そしてオンラインプラットフォームと医療機関との提携は、このセグメントの成長をさらに促進すると予想されます。利便性、プライバシー、そして競争力のある価格設定は、都市部と準都市部の両方における浸透の拡大に貢献しています。

• エンドユーザーによる

エンドユーザーに基づいて、市場は病院、在宅ケア、専門クリニック、その他に分類されます。病院は2024年に51.7%という最大の市場収益シェアを占めました。これは、患者数の増加、統合的な精神科医療、そして治療計画を監督する強力な医師ネットワークに起因しています。病院は、投薬管理、心理療法、フォローアップモニタリングを含む包括的なケアを提供しています。また、このセグメントは、確立されたインフラストラクチャと高度な診断・治療リソースへのアクセスという恩恵を受けており、効果的かつ継続的な患者管理を可能にしています。

在宅ケアは、患者の在宅治療への嗜好、遠隔医療サポート、そして在宅精神科サービスの利用可能性の向上に牽引され、2025年から2032年にかけて8.9%という最も高いCAGR(年平均成長率)を達成すると予想されています。遠隔モニタリング技術の拡充、個別ケアプランの策定、そして在宅精神科治療に対する保険適用の拡大は、在宅精神科治療の導入をさらに加速させています。慣れ親しんだ環境で治療を受けられる利便性は、患者の服薬遵守と全体的な治療成果の向上にもつながります。

慢性うつ病性人格障害治療市場の地域分析

- 北米は、2024年に40.5%の最大の収益シェアで慢性うつ病性人格障害治療市場を支配し、高度な治療プロトコルの早期導入、高い医療費、主要な製薬およびメンタルヘルスサービスプロバイダーの強力な存在を特徴としています。

- 特に都市部では、既存のヘルスケア企業とAI支援療法、遠隔精神医学、個別ケアプランに焦点を当てたスタートアップ企業の両方によるイノベーションによって、治療の採用が大幅に増加しています。

- メンタルヘルスに対する高い意識、政府の取り組み、そして強力な医療インフラが市場拡大をさらに後押しした。

米国における慢性うつ病性人格障害治療市場の洞察

米国の慢性うつ病性パーソナリティ障害治療市場は、デジタルヘルスツール、遠隔医療プラットフォーム、AIを活用した治療ソリューションの統合拡大に支えられ、北米で最大の収益シェアを獲得しました。薬物療法と心理療法を含む複合治療アプローチの導入は、患者の転帰改善と長期的な治療遵守の強化に重点が置かれ、急速に増加しています。さらに、病院、クリニック、専門治療センターにおけるメンタルヘルスプログラムの拡大も、市場の成長に大きく貢献しています。

欧州における慢性うつ病性人格障害治療市場の洞察

欧州における慢性うつ病性パーソナリティ障害(CPAD)治療市場は、予測期間中、精神疾患への意識の高まり、心理ケアに対する政府の支援、そして革新的な治療法の導入増加を背景に、大幅なCAGRで拡大すると予測されています。さらに、医療インフラの改善、都市化の進展、そして地域の病院やクリニックにおける遠隔精神医学(テレサイキアトリー)およびデジタルセラピー・プラットフォームの統合も、成長を支えています。

英国における慢性うつ病性人格障害治療市場の洞察

英国の慢性うつ病性パーソナリティ障害治療市場は、メンタルヘルスへの意識向上、予防的介入、そして慢性うつ病性パーソナリティ障害の早期診断への関心の高まりを背景に、予測期間中に注目すべきCAGRで成長すると予想されています。専門治療センターの拡充、充実したヘルスケアプログラム、そしてメンタルヘルスを促進する政府の取り組みが、市場の大幅な成長を牽引すると期待されます。

ドイツにおける慢性うつ病性人格障害治療市場の洞察

The Germany chronic depressive personality disorder treatment market is expected to expand at a considerable CAGR during the forecast period, supported by increasing government initiatives for mental health, rising adoption of advanced therapy protocols, and strong healthcare infrastructure. The availability of digital mental health tools and integration of psychotherapy and pharmacological treatment options are driving the adoption of CDPD treatment across both residential and institutional care settings.

Asia-Pacific Chronic Depressive Personality Disorder Treatment Market Insight

The Asia-Pacific chronic depressive personality disorder treatment market is expected to grow at the fastest CAGR during the forecast period, driven by rapid urbanization, rising disposable incomes, and increasing awareness of mental health interventions. Expanding pharmaceutical and mental health services, government support, and adoption of digital therapy solutions such as telepsychiatry and app-based monitoring tools are key factors contributing to growth. Countries such as China, India, and Japan are witnessing increasing investments in mental health infrastructure, awareness campaigns, and accessibility of affordable treatments.

Japan Chronic Depressive Personality Disorder Treatment Market Insight

The Japan chronic depressive personality disorder treatment market is gaining momentum due to a high-tech healthcare environment, rising urban population, and increasing emphasis on mental wellness. The adoption of integrated treatment approaches combining psychotherapy, pharmacotherapy, and digital health tools is driving market expansion, particularly among middle-aged and elderly patients.

China Chronic Depressive Personality Disorder Treatment Market Insight

The China chronic depressive personality disorder treatment market accounted for the largest share of the Asia-Pacific region in 2024, attributed to growing awareness of mental health issues, rising healthcare expenditure, and rapid urbanization. Increasing availability of advanced treatment protocols, government initiatives promoting mental wellness, and the expansion of telemedicine platforms are facilitating broader access to care. The country’s focus on digital mental health solutions and integration of AI-assisted therapy for patient management are also key factors propelling market growth.

Chronic Depressive Personality Disorder Treatment Market Share

The chronic depressive personality disorder treatment industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- AstraZeneca (U.K.)

- Lilly USA, LLC (U.S.)

- Merck & Co., Inc. (U.S.)

- Novartis AG (Switzerland)

- GSK plc (U.K.)

- Johnson & Johnson and its affiliates (U.S.)

- Regeneron Pharmaceuticals Inc. (U.S.)

- Boehringer Ingelheim International GmbH (Germany)

- Abbott (U.S.)

- AbbVie Inc (U.S.)

- Astellas Pharma Inc. (U.S.)

- Daiichi-Sankyo Company Limited (Japan)

- Endo Pharmaceuticals Inc (Ireland)

慢性うつ病性人格障害治療市場における最新動向

- 2022年8月、米国食品医薬品局(FDA)は、 Axsome Therapeutics社が開発した経口薬「Auvelity」を、成人の大うつ病性障害(MDD)の治療薬として承認しました。Auvelityは、MDD治療薬として承認された、初めてかつ唯一の速効性経口NMDA受容体拮抗薬として注目されています。臨床試験では、プラセボと比較してうつ症状を有意に改善することが示され、効果は1週間という早い段階で観察されました。この承認は、MDDの治療選択肢における大きな進歩を示しました。

- 2025年1月、ジョンソン・エンド・ジョンソン社のスプラバト(エスケタミン)点鼻スプレーは、治療抵抗性うつ病の成人に対する世界初かつ唯一の単剤療法としてFDAの承認を取得しました。この承認は、スプラバトがプラセボと比較してうつ病症状の迅速かつ優れた改善をもたらし、その効果は24時間という早い段階で観察されたことを示すデータに基づいています。注目すべきは、この承認により、毎日の経口抗うつ薬を服用することなくスプラバトを使用できるようになったことです。

- 2025年7月、精神科治療パイプラインのレビューにおいて、この分野における重要な進展が明らかになりました。特に、BPL-003は治療抵抗性うつ病において迅速かつ強力な抗うつ効果を示し、29日目までにモンゴメリー・オースバーグうつ病評価尺度(MADRS)スコアが有意に低下しました。これは、慢性うつ病に対する新たな治療法の開発における有望な進歩を示しています。

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。