世界の糖尿病性胃不全麻痺治療市場規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

13.73 Billion

USD

18.08 Billion

2024

2032

USD

13.73 Billion

USD

18.08 Billion

2024

2032

| 2025 –2032 | |

| USD 13.73 Billion | |

| USD 18.08 Billion | |

| % | |

|

糖尿病性胃不全麻痺治療の世界市場:適応症別(代償性胃不全麻痺および胃不全麻痺)、治療(薬物療法および外科手術)、薬剤別(胃運動促進剤、制吐剤、ボツリヌス毒素、その他)、投与経路別(経口および注射剤)、エンドユーザー別(病院、在宅ケア、専門クリニック、その他)、流通チャネル別(病院薬局、小売薬局、その他) - 2032年までの業界動向および予測

糖尿病性胃不全麻痺治療市場規模

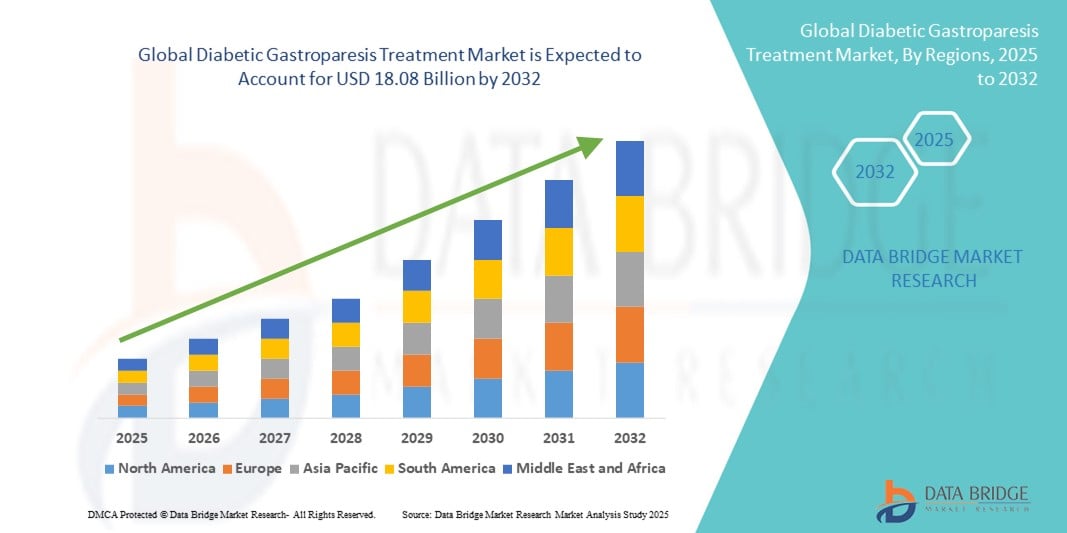

- 世界の糖尿病性胃不全麻痺治療市場規模は2024年に137億3000万米ドルと評価され、予測期間中に3.50%のCAGRで成長し、2032年には180億8000万米ドル に達すると予想されています 。

- 市場の成長は、主に世界的な糖尿病罹患率の増加によって牽引されており、糖尿病性胃不全麻痺の発症率も高まっています。医療と胃治療の進歩、そして診断方法の改善も、治療の選択肢とアクセスの拡大に貢献しています。

- さらに、新たな薬物療法や外科的介入の開発により、治療効果と患者の転帰は向上しています。糖尿病性胃不全麻痺に対する医療従事者と患者の意識の高まりにより、糖尿病管理における重要な焦点領域としての地位がさらに確立されつつあります。

糖尿病性胃不全麻痺治療市場分析

- 糖尿病性胃不全麻痺の治療は、薬物療法、外科的介入、食事管理などを含み、胃の運動性を改善し、吐き気や嘔吐などの症状を軽減し、患者の全体的な生活の質を向上させる能力があるため、糖尿病治療においてますます重要な要素となっている。

- 糖尿病性胃不全麻痺治療の需要の高まりは、主に世界中で糖尿病の罹患率が増加していること、医療従事者と患者の意識が高まっていること、そして新しい胃運動促進薬や制吐薬などの治療選択肢の進歩によって促進されている。

- 北米は、2024年に42.5%の最大の収益シェアで糖尿病性胃不全麻痺治療市場を支配し、高度な医療インフラ、高い患者意識、大手製薬会社の強力な存在を特徴とし、米国では新しい薬理学的治療法と臨床介入の大幅な導入が見られる。

- アジア太平洋地域は、糖尿病罹患率の増加、医療アクセスの改善、医療インフラへの投資の増加により、予測期間中に糖尿病性胃不全麻痺治療市場で最も急速に成長する地域になると予想されています。

- 胃運動促進薬は、胃運動機能を改善する効果が確立されており、胃不全麻痺の症状を管理するための第一選択療法として広く臨床的に採用されているため、2024年には糖尿病性胃不全麻痺治療市場において46.5%の市場シェアを占めました。

レポートの範囲と糖尿病性胃不全麻痺治療市場のセグメンテーション

|

属性 |

糖尿病性胃不全麻痺治療の主要市場洞察 |

|

対象セグメント |

|

|

対象国 |

北米

ヨーロッパ

アジア太平洋

中東およびアフリカ

南アメリカ

|

|

主要な市場プレーヤー |

|

|

市場機会 |

|

|

付加価値データ情報セット |

データブリッジマーケットリサーチがまとめた市場レポートには、市場価値、成長率、セグメンテーション、地理的範囲、主要プレーヤーなどの市場シナリオに関する洞察に加えて、専門家による詳細な分析、価格設定分析、ブランドシェア分析、消費者調査、人口統計分析、サプライチェーン分析、バリューチェーン分析、原材料/消耗品の概要、ベンダー選択基準、PESTLE分析、ポーター分析、規制の枠組みも含まれています。 |

糖尿病性胃不全麻痺治療市場の動向

薬物療法と低侵襲介入の進歩

- A significant and accelerating trend in the global diabetic gastroparesis treatment market is the development of novel pharmacological therapies, including next-generation gastroprokinetic and antiemetic agents, as well as minimally invasive interventions such as gastric electrical stimulators. These innovations are improving symptom management, patient compliance, and overall quality of life

- For instance, newer prokinetic agents in clinical trials aim to enhance gastric motility with fewer side effects, while devices such as Enterra gastric stimulators are increasingly used in refractory cases to improve gastric emptying

- Integration of digital health solutions, such as remote monitoring of gastric motility and symptom tracking apps, enables more personalized treatment plans and timely interventions, enhancing patient outcomes

- The growing adoption of combination therapies and tailored treatment regimens allows healthcare providers to optimize therapy based on individual patient profiles, creating a more precise and effective management approach

- This trend towards more targeted, patient-centric, and technologically supported treatment strategies is reshaping expectations for diabetic gastroparesis management, with companies such as Motus GI and Allergan developing advanced therapeutic options

- The demand for treatments that offer improved efficacy, reduced side effects, and convenience is increasing rapidly across both hospital and homecare settings as patients and clinicians seek better management of gastroparesis symptoms

Diabetic Gastroparesis Treatment Market Dynamics

Driver

Rising Diabetes Prevalence and Growing Awareness of Gastroparesis

- The increasing prevalence of diabetes globally, coupled with growing awareness among patients and healthcare professionals about diabetic gastroparesis, is a significant driver of market growth

- For instance, in 2024, the U.S. reported rising diabetic complications awareness campaigns, which encouraged early diagnosis and adoption of targeted therapies, driving market demand

- As more patients are diagnosed early, healthcare providers increasingly prescribe pharmacological therapies and lifestyle interventions, leading to wider adoption of available treatments

- Furthermore, expanding clinical research, educational initiatives, and guidelines for diabetic gastroparesis management are making treatment options more accessible, particularly in specialized diabetes and gastroenterology clinics

- The increasing availability of homecare therapies and patient-friendly drug formulations further supports market growth by enabling long-term management outside hospital settings

- Rising investment by pharmaceutical companies in clinical trials and new product launches is expanding the therapeutic portfolio and encouraging physician adoption of newer treatments

- Growing patient advocacy and support programs are improving disease awareness, adherence to treatment, and timely diagnosis, indirectly boosting market expansion

Restraint/Challenge

Limited Treatment Efficacy and High Costs of Advanced Therapies

- The limited efficacy of existing treatments for some patients and the high cost of advanced pharmacological therapies or surgical interventions pose significant challenges to market penetration. Many patients continue to experience persistent symptoms despite treatment.

- For instance, some gastroprokinetic drugs may cause adverse effects such as cardiovascular issues, limiting their use in certain patient populations

- High costs of novel therapies and devices, coupled with limited insurance coverage in many regions, can hinder access, particularly in emerging markets.

- In addition, the slow adoption of newer therapies in regions with limited healthcare infrastructure can restrict overall market growth

- Fragmented reimbursement policies across different countries further restrict access to advanced therapies and affect market adoption rates

- Limited awareness among general practitioners about specialized treatment options may delay referral to gastroenterology specialists, slowing early intervention and therapy uptake

- Overcoming these challenges through the development of safer, more effective therapies, improved insurance coverage, and patient education on disease management will be crucial for sustained market expansion

Diabetic Gastroparesis Treatment Market Scope

The market is segmented on the basis of indication type, treatment, drugs, route of administration, end-users, and distribution channel.

- By Indication Type

On the basis of indication type, the diabetic gastroparesis treatment market is segmented into compensated gastroparesis and gastric failure. The compensated gastroparesis segment dominated the market with the largest revenue share in 2024, driven by the higher prevalence of early-stage gastroparesis among diabetic patients. Patients in this category typically respond well to pharmacological therapies, including gastroprokinetic and antiemetic drugs, which are widely prescribed by healthcare professionals. Early diagnosis and symptom management strategies contribute to sustained demand for compensated gastroparesis treatments. In addition, increasing awareness programs and patient education initiatives improve early treatment adoption, reinforcing the dominance of this segment. Hospitals and specialty clinics often focus on managing compensated cases to prevent progression to gastric failure, which further supports market revenue.

The gastric failure segment is expected to witness the fastest growth rate during the forecast period, fueled by rising awareness of advanced treatment options and the growing prevalence of severe diabetic complications. Patients with gastric failure often require surgical interventions or gastric stimulators, driving demand for specialized therapies. Advancements in minimally invasive procedures, coupled with increasing adoption in tertiary care centers, are expanding treatment accessibility. Furthermore, improved diagnostic tools allow earlier identification of high-risk patients, supporting the growth of this segment. The increasing emphasis on individualized patient management and combination therapy approaches also contributes to the rapid expansion of the gastric failure treatment segment.

- By Treatment

On the basis of treatment, the diabetic gastroparesis treatment market is segmented into medication and surgery. The medication segment dominated the market in 2024, owing to the widespread adoption of gastroprokinetic and antiemetic drugs as first-line therapies. Oral pharmacological treatments are convenient, cost-effective, and widely available, making them the preferred choice for most patients. Continuous development of novel drugs with improved efficacy and reduced side effects enhances adoption. In addition, clinicians often prescribe medications for long-term management, increasing the volume of repeat prescriptions. The dominance of this segment is reinforced by healthcare infrastructure in developed markets, where early intervention and outpatient management are common.

The surgery segment is expected to witness the fastest growth rate during forecast period, driven by the rising prevalence of refractory gastroparesis and gastric failure cases unresponsive to medications. Surgical interventions, including gastric electrical stimulation and pyloroplasty, are increasingly adopted in specialized healthcare centers. Technological advancements in minimally invasive techniques reduce recovery times and improve patient outcomes, making surgical treatment more attractive. Growing awareness among physicians and patients about advanced therapeutic options further supports this growth. Expansion of hospital infrastructure in emerging markets also facilitates higher adoption of surgical interventions.

- By Drugs

薬剤に基づいて、糖尿病性胃不全麻痺治療市場は、胃運動促進剤、制吐剤、ボツリヌス毒素、その他に分類されます。胃運動促進剤セグメントは、胃の運動機能の改善と症状緩和への有効性が牽引し、2024年には46.5%という最大シェアで市場を席巻しました。これらの薬剤は、臨床効果が確立されており、治療ガイドラインにも含まれているため、広く処方されています。継続的な研究開発により、副作用の少ない処方が開発され、採用が進んでいます。胃運動促進剤は経口投与と注射投与の両方に対応しており、医師と患者に柔軟性を提供します。病院、専門クリニック、在宅ケアの現場では、長期管理にこれらの薬剤が広く使用されており、市場での優位性をさらに強化しています。

ボツリヌス毒素分野は、主に難治性胃不全麻痺症例への臨床適用の増加により、予測期間中に最も高い成長率を示すと予想されています。ボツリヌス毒素注射は幽門機能不全を標的とし、従来の薬剤では効果が得られない症状の緩和をもたらします。注射技術の進歩と医師の専門知識の向上が、より広範な適用を後押ししています。患者と医療従事者の間で代替治療選択肢に対する意識が高まっていることも、この分野の急速な成長に貢献しています。さらに、臨床試験で良好な結果が得られたことで、より多くの地域で規制当局の承認が促進され、市場の潜在性が向上しています。

- 投与経路

投与経路に基づき、糖尿病性胃不全麻痺治療市場は経口薬と注射薬に分類されます。2024年には、利便性、患者の服薬コンプライアンス、そして長期管理への適合性から、経口薬が市場を席巻しました。ほとんどの胃運動促進薬および制吐薬は経口剤で入手可能であり、自宅での自己投与が可能です。病院や外来診療所では、早期管理および慢性疾患治療において経口治療が好まれています。経口薬は注射薬に比べて入手しやすく、コストが低いことから、このセグメントの優位性をさらに強化しています。

注射剤セグメントは、重症または難治性症例に対する病院および専門クリニックでの使用増加に牽引され、予測期間中に最も高い成長率を示すと予想されています。ボツリヌス毒素や特定の高度な消化管運動促進製剤などの注射剤療法は、作用発現が速く、投与量も制御可能です。投与デバイスや低侵襲技術の技術向上により、患者の受け入れが向上しています。三次医療センターでの採用増加と有効性に関する臨床的エビデンスの増加が、このセグメントの拡大を支えています。医師の間で注射剤に対する認知度が高まっていることも、セグメントの成長に貢献しています。

- エンドユーザー別

エンドユーザーに基づいて、糖尿病性胃不全麻痺治療市場は、病院、在宅ケア、専門クリニック、その他に分類されます。病院セグメントは、専門的なケア、高度な診断、薬物療法と外科的介入の両方へのアクセスが可能であることから、2024年には最大のシェアを占め、市場を席巻しました。病院は初期段階から重症まで幅広い症例に対応しており、糖尿病性胃不全麻痺治療に対する継続的な需要を確保しています。消化器専門医と多職種チームの存在は、患者の転帰を向上させ、治療の採用を促進します。

在宅ケア分野は、外来管理と利便性に対する患者の嗜好の高まりを背景に、予測期間中に最も高い成長率を示すと予想されています。在宅ケアは、長期的な治療遵守を可能にし、通院回数を減らし、経口薬の自己投与をサポートします。遠隔モニタリング技術と遠隔医療サービスの導入増加も、成長をさらに加速させます。患者と介護者の間で在宅での症状管理に関する意識が高まることで、市場の潜在性は高まります。この分野は、高齢者人口が増加し、慢性疾患管理のニーズが高まっている地域において特に重要です。

- 流通チャネル別

流通チャネルに基づいて、糖尿病性胃不全麻痺治療市場は、病院薬局、小売薬局、その他に分類されます。入院患者への処方薬の直接提供と専門治療へのアクセスの容易さから、病院薬局セグメントは2024年に市場を席巻しました。病院薬局はまた、注射剤や高度な治療機器の調剤も行っており、市場における優位性を強化しています。

小売薬局セグメントは、外来処方箋の増加と在宅ケアの導入増加に牽引され、予測期間中に最も高い成長率を示すと予想されています。小売薬局は患者の利便性を高め、服薬アドヒアランスを向上させ、経口薬の広範な入手をサポートします。また、新興市場における薬局チェーンの拡大とサプライチェーンネットワークの改善も成長を支えています。患者が地域密着型の医薬品へのアクセスを希望していることも、このセグメントの拡大を後押ししています。

糖尿病性胃不全麻痺治療市場の地域分析

- 北米は、高度な医療インフラ、高い患者意識、大手製薬会社の強力な存在を特徴とし、2024年には糖尿病性胃不全麻痺治療市場で42.5%の最大の収益シェアを獲得して市場を支配した。

- この地域の患者は、早期診断、専門の消化器内科センターへの容易なアクセス、薬物療法と高度な外科治療の両方を利用できるという恩恵を受けています。新しい治療法と併用療法の普及率の高さも、市場における優位性をさらに支えています。

- The widespread adoption is reinforced by strong research and development activities, favorable reimbursement policies, and a high standard of clinical care, establishing North America as a key market for diabetic gastroparesis management. Hospitals, specialty clinics, and homecare services collectively contribute to the region’s leading position in the global market

U.S. Diabetic Gastroparesis Treatment Market Insight

The U.S. diabetic gastroparesis treatment market captured the largest revenue share of 38% in North America in 2024, fueled by the rising prevalence of diabetes and increasing awareness of gastroparesis complications. Patients and healthcare providers are increasingly prioritizing early diagnosis and effective management through pharmacological therapies and advanced interventions. The growing trend of personalized treatment plans, combined with strong adoption of combination therapies and minimally invasive procedures, further propels market growth. Moreover, robust healthcare infrastructure, favorable reimbursement policies, and the presence of key pharmaceutical companies contribute significantly to market expansion.

Europe Diabetic Gastroparesis Treatment Market Insight

The Europe diabetic gastroparesis treatment market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing diabetes prevalence and the rising need for effective management of complications. Growth is supported by advanced healthcare systems, well-established gastroenterology centers, and a focus on patient-centric therapies. European patients are increasingly seeking convenient and effective pharmacological options, and hospitals are adopting advanced therapies, including gastric stimulators and combination drug treatments. The market is witnessing notable growth in both newly diagnosed patients and those with long-term diabetic complications, fostering adoption across multiple healthcare settings.

U.K. Diabetic Gastroparesis Treatment Market Insight

The U.K. diabetic gastroparesis treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the increasing prevalence of diabetes and the demand for enhanced disease management. Awareness campaigns and educational initiatives among patients and healthcare providers are encouraging early diagnosis and adoption of effective treatments. In addition, the availability of specialized clinics, coupled with strong healthcare infrastructure, supports patient access to pharmacological and surgical interventions. Rising concerns over diabetic complications and hospital-based management programs further stimulate market growth in the region.

Germany Diabetic Gastroparesis Treatment Market Insight

The Germany diabetic gastroparesis treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by growing awareness of gastroparesis and advanced treatment availability. Germany’s well-developed healthcare system, combined with a focus on research and innovation, encourages adoption of both pharmacological therapies and minimally invasive interventions. Hospitals and specialty clinics are increasingly integrating digital monitoring and patient management systems, improving treatment adherence and outcomes. The demand for safe, effective, and technologically advanced treatments aligns with local patient expectations, supporting steady market growth.

Asia-Pacific Diabetic Gastroparesis Treatment Market Insight

The Asia-Pacific diabetic gastroparesis treatment market is poised to grow at the fastest CAGR of 23% during the forecast period of 2025 to 2032, driven by the rising prevalence of diabetes, increasing healthcare access, and awareness of diabetic complications in countries such as China, India, and Japan. Growing urbanization and rising disposable incomes are facilitating better access to diagnostic services and advanced treatment options. Furthermore, government initiatives to improve chronic disease management and expand healthcare infrastructure are driving adoption. The emergence of local pharmaceutical manufacturing and affordable therapies is also increasing treatment accessibility across the region.

Japan Diabetic Gastroparesis Treatment Market Insight

The Japan diabetic gastroparesis treatment market is gaining momentum due to the country’s high prevalence of diabetes, technologically advanced healthcare infrastructure, and rising demand for patient-centric care. Japanese patients increasingly prefer minimally invasive treatments and effective pharmacological therapies for long-term management. Integration of digital health monitoring and telemedicine supports adherence and symptom tracking, boosting therapy adoption. In addition, an aging population is such asly to increase demand for convenient and safe treatment options in both outpatient and homecare settings.

India Diabetic Gastroparesis Treatment Market Insight

The India diabetic gastroparesis treatment market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to the country’s growing diabetes population, rapid urbanization, and expanding healthcare access. India has witnessed increasing awareness among patients and healthcare providers about diabetic gastroparesis management, leading to higher adoption of pharmacological therapies. Government initiatives to improve chronic disease management and the availability of affordable therapies further contribute to market growth. The presence of domestic pharmaceutical companies and the expansion of specialty clinics also play a significant role in driving the Indian market.

Diabetic Gastroparesis Treatment Market Share

糖尿病性胃不全麻痺の治療業界は、主に、以下を含む定評のある企業によって主導されています。

- Evoke Pharma, Inc.(米国)

- アボット(米国)

- アッヴィ社(米国)

- Salix Pharmaceuticals, Inc.(米国)

- セラヴァンス・バイオファーマ社(米国)

- メドトロニック(アイルランド)

- バウシュ・ヘルス・カンパニーズ(カナダ)

- ファイザー社(米国)

- テバ製薬工業株式会社(イスラエル)

- 武田薬品工業株式会社(日本)

- カディラ・ファーマシューティカルズ社(インド)

- エーザイ株式会社(日本)

- GSK plc(英国)

- Ipca Laboratories Ltd.(インド)

- ジョンソン・エンド・ジョンソン社(米国)

- リズム・ファーマシューティカルズ社(米国)

- ヴァンダ・ファーマシューティカルズ社(米国)

- プロセサ・ファーマシューティカルズ社(米国)

- Neurogastrx, Inc.(米国)

- ヴァンダ・ファーマシューティカルズ社(米国)

世界の糖尿病性胃不全麻痺治療市場の最近の動向は何ですか?

- エンテラ・メディカルは2025年6月、胃不全麻痺患者の慢性的な吐き気・嘔吐症状のコントロールにおける胃電気刺激(GES)療法の有効性を評価するNAVIGATE臨床試験を開始しました。この試験は、薬剤抵抗性の胃不全麻痺患者にとってGESが有効な治療選択肢であることを裏付けるさらなるエビデンスを提供することを目的としています。

- 2023年10月、エンテラ・メディカル社は、同社のエンテラIIシステムが米国食品医薬品局(FDA)より条件付きMRI承認を取得したと発表しました。この承認により、エンテラIIシステムを装着した患者は、特定の条件下で頭部または上肢・下肢の磁気共鳴画像(MRI)検査を安全に受けられるようになります。

- 2024年3月、胃電気刺激装置であるEnterra IIシステムが、磁気共鳴(MR)検査の条件付き使用についてFDAの承認を取得しました。この進歩により、胃不全麻痺の患者は装置を外すことなくMRI検査を受けることができ、治療の柔軟性が向上します。Enterra® IIシステムは、胃の筋肉に弱い電気パルスを照射することで、胃不全麻痺に伴う慢性的な吐き気や嘔吐を軽減します。

- 2023年5月、アイアンウッド・ファーマシューティカルズは、希少消化器疾患を専門とする臨床段階のバイオテクノロジー企業であるベクティヴバイオの買収を発表しました。この買収額は約10億米ドルで、アイアンウッドはベクティヴバイオの主力治験薬であるアプラグルチド(短腸症候群などの疾患治療薬として開発中)へのアクセスを獲得します。

- 2021年10月、プロセサ・ファーマシューティカルズは、胃不全麻痺の治療薬として新規セロトニン5-HT4受容体作動薬であるPCS12852の第2a相臨床試験の実施をFDAから承認されました。この試験は、中等度から重度の胃不全麻痺患者における胃排出速度の改善における同薬の安全性と有効性を評価することを目的としていました。

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。