Global Influenza Drug Market Size, Share, and Trends Analysis Report

Market Size in USD Billion

CAGR :

%

USD

981.68 Billion

USD

1,168.36 Billion

2024

2032

USD

981.68 Billion

USD

1,168.36 Billion

2024

2032

| 2025 –2032 | |

| USD 981.68 Billion | |

| USD 1,168.36 Billion | |

| % | |

|

Global Influenza Drug Market Segmentation, By Type (Influenza A, Influenza B, and Influenza C), Treatment (Vaccines and Drugs), Route of Administration (Oral, Intramuscular, Intradermal, Intranasal, and Intravenous), Age (Pediatrics and Adults), End User (Hospitals, and Home Care), Distribution Channel (Direct Tenders and Retail Sales) - Industry Trends and Forecast to 2032

Influenza Drug Market Size

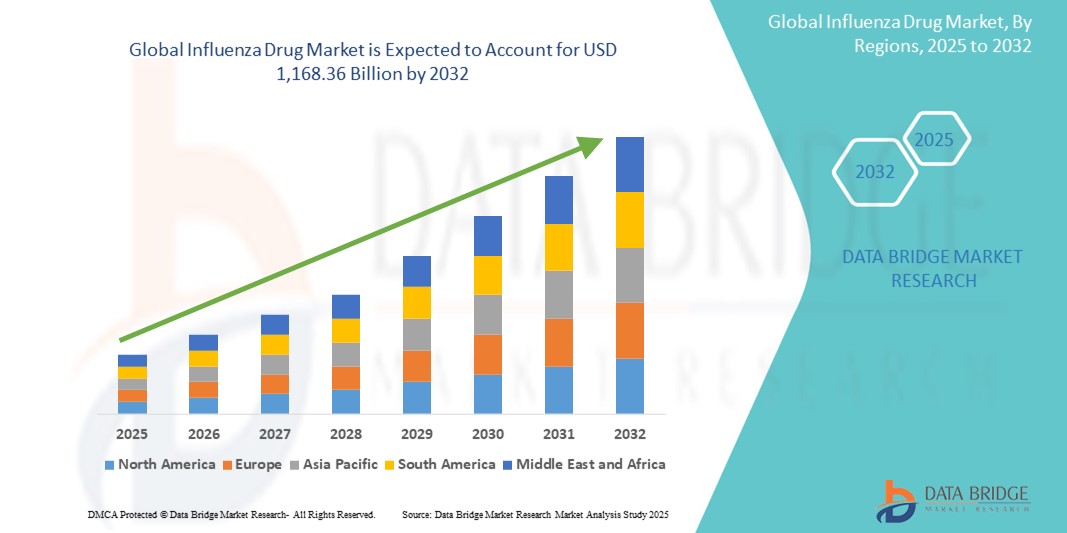

- The global influenza drug market size was valued at USD 981.68 billion in 2024 and is expected to reach USD 1,168.36 billion by 2032, at a CAGR of 2.20% during the forecast period

- The market growth is largely fueled by the growing incidence of seasonal flu and other contagious respiratory illnesses, along with an increasing patient population at risk of developing flu-related complications

- Furthermore, rising investments in research and development activities by pharmaceutical companies and research institutions to develop advanced and improved medications, including novel antiviral drugs and recombinant vaccines, are accelerating the uptake of influenza drug solutions, thereby significantly boosting the industry's growth

Influenza Drug Market Analysis

- The global influenza drug market encompasses a range of antiviral medications and vaccines designed to prevent, treat, and alleviate the symptoms of influenza infections, which pose a significant public health challenge due to their recurrent and seasonal nature, constant viral mutations, and potential for pandemics

- The escalating demand for influenza drugs is primarily fueled by the consistent global prevalence of influenza infections, increasing awareness about the benefits of vaccination, and continuous advancements in pharmaceutical research leading to more effective antiviral therapies and next-generation vaccines

- North America dominates the influenza drug market with the largest revenue share of 60.5% in 2024, characterized by robust healthcare infrastructure, high vaccination coverage rates, and the presence of major pharmaceutical companies. The U.S. experiences strong market growth driven by extensive public health campaigns, government initiatives for pandemic preparedness, and ongoing R&D in novel influenza treatments and vaccines

- Asia-Pacific is expected to be the fastest growing region in the influenza drug market during the forecast period due to increasing awareness about influenza, rising healthcare expenditure, growing urbanization, and a large patient pool susceptible to infections in densely populated countries

- インフルエンザA型は、変異率の高さ、宿主域の広さ、パンデミックの可能性の高さ、病気の重症度の高さにより、より複雑なワクチン戦略と治療の頻繁な更新が必要となることから、2024年にはインフルエンザ薬市場を47.78%のシェアで支配するでしょう。

レポートの範囲とインフルエンザ薬市場のセグメンテーション

|

属性 |

インフルエンザ治療薬の主要市場分析 |

|

対象セグメント |

|

|

対象国 |

北米

ヨーロッパ

アジア太平洋

中東およびアフリカ

南アメリカ

|

|

主要な市場プレーヤー |

|

|

市場機会 |

|

|

付加価値データ情報セット |

データブリッジマーケットリサーチがまとめた市場レポートには、市場価値、成長率、セグメンテーション、地理的範囲、主要プレーヤーなどの市場シナリオに関する洞察に加えて、専門家による詳細な分析、価格設定分析、ブランドシェア分析、消費者調査、人口統計分析、サプライチェーン分析、バリューチェーン分析、原材料/消耗品の概要、ベンダー選択基準、PESTLE分析、ポーター分析、規制の枠組みも含まれています。 |

インフルエンザ治療薬市場の動向

「遠隔医療とデジタルヘルスツールの導入増加」

- インフルエンザ薬市場における重要な加速トレンドとして、インフルエンザの管理、診断、処方のための遠隔医療とデジタルヘルスツールの統合が進んでいます。こうした技術の融合により、特にインフルエンザ患者にとって、医療サービスへのアクセスが大幅に向上しています。

- For instance, virtual consultations allow individuals with flu-like symptoms to connect with healthcare professionals from the comfort of their homes, reducing the risk of viral transmission in clinics and hospitals. Telemedicine platforms can facilitate rapid diagnosis based on symptom assessment and guide patients on appropriate self-care or prescription of antiviral medications such as oseltamivir or baloxavir. Approximately 33% of health systems integrate influenza treatment into telemedicine services, enhancing accessibility in rural regions

- Digital health tools, including mobile apps and wearable devices, enable continuous monitoring of physiological parameters that can indicate the onset or progression of influenza. Some smart thermometers, such as those from KINSA, can track aggregate temperature data to identify potential flu hotspots. These technologies can provide early alerts, prompting individuals to seek medical advice sooner, which is crucial for the efficacy of antiviral treatments

- The seamless integration of digital health tools with healthcare systems also supports broader public health surveillance efforts. Data from wearable devices can contribute to real-time influenza surveillance, helping health authorities track outbreaks and allocate resources more effectively. This enhanced surveillance can inform targeted vaccination campaigns and timely distribution of antiviral drugs

- This trend towards more accessible, proactive, and data-driven influenza management is fundamentally reshaping patient engagement and healthcare delivery. Consequently, pharmaceutical companies and healthcare providers are exploring partnerships and developing platforms that leverage these digital capabilities to improve patient outcomes and medication adherence

- The demand for influenza drugs is indirectly boosted by these trends, as telemedicine makes it easier for patients to receive timely prescriptions, and digital monitoring can lead to earlier diagnosis and intervention, maximizing the effectiveness of available treatments

Influenza Drug Market Dynamics

Driver

“Growing Need Due to Consistent Global Prevalence of Influenza and Public Health Initiatives”

- The increasing and consistent global prevalence of seasonal influenza epidemics, coupled with the ongoing threat of pandemic strains and robust public health initiatives, is a significant driver for the heightened demand for influenza drugs and vaccines

- For instance, governments worldwide, including the U.S. and those in Europe and Asia, continually launch extensive vaccination campaigns and invest in national immunization programs to mitigate the impact of annual flu seasons and prepare for potential pandemics. These initiatives, along with increased surveillance and rapid diagnostic advancements, lead to a greater push for vaccination and early treatment with antiviral drugs

- As awareness among the general population and healthcare providers grows regarding the severity of influenza and its potential complications, there's a heightened demand for both preventive and therapeutic solutions. This is particularly true for high-risk populations such as the elderly, young children, and individuals with underlying health conditions

- Furthermore, continuous research and development efforts by pharmaceutical companies to create more effective and broader-spectrum antiviral drugs, as well as next-generation vaccines, are expanding the available treatment landscape and improving the efficacy of existing interventions, thereby propelling market growth

- The necessity for updated vaccine formulations each year due to the constantly evolving nature of influenza viruses ensures a sustained and recurring demand for novel products. This continuous cycle of development, production, and distribution is a key factor propelling the influenza drug market in both developed and emerging economies

Restraint/Challenge

“Challenges of Viral Mutability and Drug Resistance, and High Development Costs”

- A significant challenge to the global influenza drug market is the inherent mutability of influenza viruses, which constantly undergo antigenic drift and shift. This rapid evolution can render existing vaccines less effective and lead to the emergence of antiviral drug resistance, posing a continuous threat to public health

- For instance, the frequent need to update vaccine strains annually necessitates a continuous cycle of research, development, and production, which is both time-consuming and costly. Furthermore, the emergence of drug-resistant strains, such as those resistant to older antivirals such as amantadine or, more recently, some H1N1 viruses showing resistance to oseltamivir (Tamiflu), limits treatment options and complicates clinical management

- Addressing these biological challenges requires significant and sustained investment in R&D for novel antiviral agents with new mechanisms of action and broader-spectrum activity, as well as universal influenza vaccines that can offer long-lasting protection against multiple strains. However, vaccine and drug development is an exceptionally lengthy and expensive process, often taking 10-15 years and costing hundreds of millions to over a billion USD, with a high failure rate

- In addition, logistical challenges, particularly maintaining the "cold chain" for vaccine distribution from manufacturing sites to remote areas, can lead to wastage and reduced efficacy. Factors such as inadequate infrastructure, human error, and power outages in lower-income countries pose significant barriers

- The high initial cost of developing and bringing new influenza drugs and vaccines to market, combined with stringent regulatory approval processes, creates significant hurdles for manufacturers. This often translates to higher prices for advanced treatments, potentially limiting access in price-sensitive markets or for underinsured populations

- Overcoming these challenges through international collaborations, increased public and private funding for R&D, streamlined regulatory pathways, and investment in robust global distribution infrastructures will be vital for sustained market growth and effective pandemic preparedness

Influenza Drug Market Scope

The market is segmented on the basis of type, treatment, route of administration, age, end user, and distribution channel.

- By Type

On the basis of type, the influenza drug market is segmented into influenza A, influenza B, and influenza C. The influenza A segment dominates the market with a market share of 47.78% in 2024, driven by its higher mutation rate, wider host range, significant pandemic potential, and increased severity of illness, necessitating more complex vaccination strategies to control outbreaks. The consistent threat of Influenza A strains such as H1N1 and H3N2 ensures a sustained demand for related drugs and vaccines

Influenza B is expected to witness highest CAGR in market due to its inclusion in quadrivalent vaccines, which offer broader protection against both A and B strains. The increasing awareness of Influenza B's role in seasonal epidemics and the growing emphasis on comprehensive flu prevention strategies are driving demand for more effective vaccines that cover these strains, particularly in vulnerable populations

- By Treatment

On the basis of treatment, the influenza drug market is segmented into vaccines and drugs. The vaccines segment dominates the market with a market share of 87.23% in 2024, due to its pivotal role in preventing illness, reducing transmission, and addressing public health concerns associated with seasonal outbreaks and potential pandemics. Continuous advancements in vaccine technology, including the development of quadrivalent vaccines offering broader protection, further solidify their market leadership

The drugs segment, including antivirals such as oseltamivir and baloxavir, plays a crucial role in treating established infections, with baloxavir marboxil (Xofluza) noted as the fastest-growing drug type due to its single-dose administration and efficacy

- By Route of Administration

On the basis of route of administration, the influenza drug market is segmented into oral, intramuscular, intradermal, intranasal, and intravenous. The oral segment is expected to dominate the market with a market share of 45.04% in 2024, primarily driven by its convenience, ease of self-administration, and widespread accessibility for patients in both outpatient and home care settings. Oral antiviral medications are often the first line of treatment for influenza

The intranasal segment is expected to be the fastest-growing route of administration during the forecast period. This is attributed to its non-invasive, needle-free administration, which improves patient compliance, especially in pediatric populations, and its ability to induce both systemic and mucosal immunity

- By Age

On the basis of age, the influenza drug market is segmented into pediatrics and adults. The adult segment is the largest in the influenza market, with a 66.7% share in 2024, propelled by elevated vaccination rates among seniors and individuals with chronic illnesses, who are at higher risk of severe flu complications

The pediatrics segment is poised to grow at a notable CAGR, as young children, particularly those under 5 years, are at higher risk of severe influenza complications, accelerating the market scope for child-friendly formulations and vaccination efforts.

- By End Use

On the basis of end user, the influenza drug market is segmented into hospitals, and home care. The hospitals segment dominates the global influenza drug market with a market share of 72.62% in 2024, largely due to their role in managing severe influenza cases requiring intensive monitoring, intravenous antivirals, and critical care for high-risk patients. Hospitals also serve as key points for vaccination drives

The home care segment is expected to witness the fastest compound annual growth rate (CAGR) from 2025 to 2032 in the global influenza drug market, driven by the increasing preference for at-home treatment options, advancements in telemedicine, and the growing adoption of home healthcare services. These factors enable patients to manage influenza symptoms effectively within the comfort of their homes, reducing the need for hospitalization and minimizing exposure to healthcare facilities.

- By Distribution Channel

On the basis of distribution channel, the global influenza drug market is segmented into direct tenders and retail sales. The direct tenders segment is projected to dominate the global influenza drug market with the largest market share of 56.34% in 2024, primarily driven by large-scale procurement of vaccines and antiviral drugs by governments and public health organizations for national immunization programs and strategic stockpiling. This channel ensures bulk purchasing and efficient distribution for mass vaccination campaigns.

The retail sales segment is also a dominant channel, acting as key access points for both vaccines and over-the-counter and prescription treatments for the general public, and is expected to see significant growth, particularly through online pharmacies due to convenience and accessibility.

Influenza Drug Market Regional Analysis

- North America dominates the influenza drug market with the largest revenue share of 60.5% in 2024, driven by robust healthcare infrastructure, high vaccination coverage rates, and the presence of major pharmaceutical companies

- Consumers in the region highly prioritize preventive healthcare and readily access vaccines and antiviral treatments

- This widespread adoption is further supported by favorable reimbursement policies, a technologically advanced population, and the growing emphasis on public health initiatives, establishing influenza drugs as a crucial component of seasonal disease management

U.S. Influenza Drug Market Insight

The U.S. influenza drug market captured the largest revenue share of 56.2% in 2024 within North America, reflecting the nation's advanced healthcare system and proactive public health strategies. The U.S. is a major driver of the influenza market due to its substantial burden of seasonal flu, robust vaccination programs, and continuous investment in R&D for new treatments and vaccines. Consumers increasingly prioritize preventive measures and readily access influenza medications. The strong integration of public health recommendations, widespread availability of both vaccines and antiviral drugs, and a significant patient population contribute to the sustained demand.

Europe Influenza Drug Market Insight

The Europe influenza drug market is projected to expand at a CAGR of 2.5% throughout the forecast period, primarily driven by established government initiatives for influenza vaccination and treatment, stringent public health guidelines, and a high incidence of seasonal flu. The region's focus on preventive healthcare, coupled with advanced healthcare infrastructure and increasing awareness about flu complications, is fostering the adoption of influenza drugs. European countries are experiencing consistent demand for both vaccines and antiviral therapies in response to annual outbreaks.

U.K. Influenza Drug Market Insight

The U.K. influenza drug market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by robust government vaccination programs, an increasing focus on public health, and a desire for enhanced protection against seasonal flu. The U.K.'s well-established healthcare system and strong recommendations for annual flu shots are encouraging high uptake of both vaccines and antiviral treatments among the population. The country's commitment to public health initiatives further stimulates market growth.

Germany Influenza Drug Market Insight

The Germany influenza drug market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of public health security, a strong emphasis on preventive medicine, and demand for technologically advanced solutions. Germany's well-developed healthcare infrastructure, combined with its focus on high vaccination rates and efficient disease management, promotes the adoption of influenza drugs, particularly in both general practice and hospital settings. The integration of advanced diagnostics and a preference for evidence-based treatments align with local consumer and medical expectations.

アジア太平洋地域のインフルエンザ薬市場に関する洞察

アジア太平洋地域のインフルエンザ治療薬市場は、予測期間中に最も高いCAGRで成長する見込みです。これは、中国、日本、インドなどの国々における都市化の進展、可処分所得の増加、そして医療技術の進歩に牽引されています。この地域の人口は大きく、増加傾向にあり、インフルエンザの流行に対して非常に脆弱であるため、効果的な治療法やワクチンに対する認識と需要が高まっています。さらに、アジア太平洋地域では医療インフラが整備され、政府の取り組みによって必須医薬品へのアクセスが促進されているため、インフルエンザ治療薬の手頃な価格と入手しやすさは、より幅広い消費者層に広がっています。

日本インフルエンザ治療薬市場インサイト

日本におけるインフルエンザ治療薬市場は、季節性インフルエンザの発生率の高さ、急速な都市化、そして効果的な治療選択肢への強い需要により、抗ウイルス薬の需要が高まっています。日本市場は公衆衛生とワクチン接種率を重視しており、特に高齢化社会における合併症への意識の高まりがインフルエンザ治療薬の採用を牽引しています。日本がインフルエンザの負担軽減を最優先に考える中、先進的な抗ウイルス薬の導入と継続的な研究開発努力が成長を牽引しています。

インドのインフルエンザ薬市場の洞察

インドのインフルエンザ薬市場は、2024年にはアジア太平洋地域において大きなシェアを占めると予測されています。これは、同国における中流階級の拡大、急速な都市化、そして医療へのアクセス向上によるものです。インドは感染症の負担が大きい大規模市場であり、インフルエンザ薬は公衆衛生プログラムと民間医療の両方においてますます重要になっています。医療インフラの改善に向けた取り組みと、国産および輸入のインフルエンザ薬の入手しやすさが、インド市場の成長を牽引する主要な要因となっており、年平均成長率(CAGR)は2.6%と予測されています。

インフルエンザ薬の市場シェア

インフルエンザ薬業界は、主に、次のような老舗企業によって牽引されています。

- アッヴィ社(米国)

- アストラゼネカ(英国)

- BioNTech SE(ドイツ)

- ブリストル・マイヤーズ スクイブ社(米国)

- シプラ(インド)

- コクリスタルファーマ社(米国)

- CSL(英国)

- 第一三共株式会社(日本)

- ドクター・レディーズ・ラボラトリーズ社(インド)

- F. ホフマン・ラ・ロッシュ AG (スイス)

- ギリアド・サイエンシズ(米国)

- GSK plc.(英国)

- ジョンソン・エンド・ジョンソン・サービス社(米国)

- メルク社(米国)

- モデナ社(米国)

- ノバルティスAG(スイス)

- ノババックス(米国)

- オシヴァックス(フランス)

- サノフィSA(フランス)

世界のインフルエンザ薬市場の最新動向

- 2024年9月、アストラゼネカのフルミストが米国で自己接種の承認を取得しました。これは、医療従事者による接種を必要としない初のインフルエンザワクチンであり、インフルエンザ予防を求める人々のアクセスと利便性を向上させるという大きな進歩です。フルミストは、米国食品医薬品局(FDA)により、49歳までの成人による自己接種、または2歳から17歳までの親/介護者による接種が承認されています。

- 2024年8月、ハーバード大学医学部の科学者たちは、病原体捕捉・中和スプレー(PCANS)、略してProfiと呼ばれる鼻腔スプレーを開発しました。このスプレーは、鼻腔内にバリアを形成し、ウイルスや細菌を捕捉・中和することで、インフルエンザ、風邪、COVID-19を99.99%以上の効果で予防すると謳っています。

- 2024年5月、サノフィとノババックス社は、ノババックス社が現在販売している単独型アジュバント添加COVID-19ワクチンを全世界で共同販売するとともに、新たなインフルエンザ-COVID-19ワクチンの配合ワクチンを開発する共同独占ライセンス契約を締結したことを発表しました。この提携は、混合ワクチンの開発を加速させ、患者にとって利便性と保護効果を高めることを目的としています。

- 2023年4月、シノバック・バイオテック株式会社は、北京に新たなインフルエンザワクチン製造施設を開設したことを発表しました。この拡張により、インフルエンザワクチンの世界的な生産能力が向上し、より広範な供給と入手性の向上に貢献します。

- 2023年3月、FDAのワクチンおよび関連生物学的製剤諮問委員会(VRBPAC)は、2023~2024年の米国インフルエンザシーズンにおけるワクチンの成分を決定するために招集されました。この年次プロセスは、流行しているインフルエンザウイルス株に対するワクチンの有効性を確保するために非常に重要です。

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。