世界の医療画像管理市場の規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

5.97 Billion

USD

8.96 Billion

2024

2032

USD

5.97 Billion

USD

8.96 Billion

2024

2032

| 2025 –2032 | |

| USD 5.97 Billion | |

| USD 8.96 Billion | |

| % | |

|

世界の医療画像管理市場のセグメンテーション、製品別(画像アーカイブおよび通信システム(PACS)、ベンダーニュートラルアーカイブ(VNA)、アプリケーション非依存臨床アーカイブ(AICA)、エンタープライズビューア/ユニバーサルビューア)、配信モデル別(ハイブリッド、Web/クラウドベース、オンプレミス)、専門分野別(外科、腫瘍学、歯科、その他)、エンドユーザー別(病院、放射線科チェーン/センター、外来手術センター、その他)、流通チャネル別(直接入札、サードパーティ管理者、その他) - 2032年までの業界動向と予測

医療画像管理市場規模

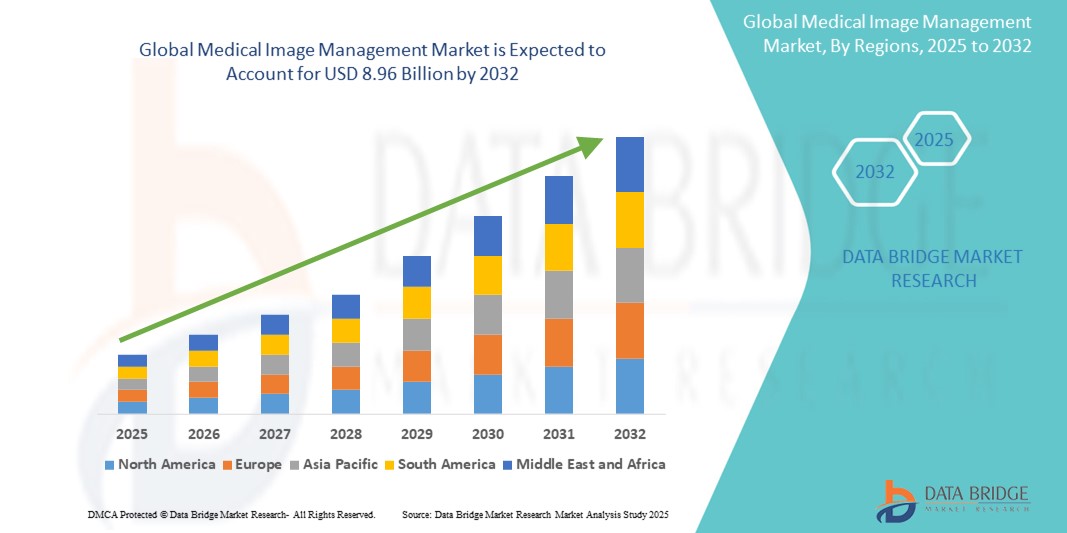

- 世界の医療画像管理市場規模は2024年に59億7000万米ドルと評価され、予測期間中に5.20%のCAGRで成長し、2032年には89億6000万米ドル に達すると予想されています 。

- 市場の成長は、AIとクラウドベースのプラットフォームの統合を含む診断画像モダリティと画像管理ソフトウェアの技術的進歩と相まって、増加する複雑な画像データを処理するための効率的で統合されたソリューションに対する需要の高まりによって主に推進されています。

- さらに、病気の早期発見に対する消費者の需要の高まり、慢性疾患の蔓延の増加、電子医療記録の導入を促進する政府の取り組みにより、医療画像管理システムは現代の医療提供に不可欠なツールとして確立され、業界の成長を大幅に促進しています。

医療画像管理市場分析

- 画像アーカイブおよび通信システム(PACS)やベンダー中立アーカイブ(VNA)などのソリューションを網羅する医療画像管理システムは、画像データの量と複雑さの増加、効率的な保管と検索の必要性、電子医療記録とのシームレスな統合により、現代の医療においてますます重要になっています。

- 医療画像管理ソリューションの需要の高まりは、主に診断画像診断法の急速な技術進歩、頻繁な画像診断を必要とする慢性疾患の増加、医療におけるデジタルヘルスインフラとITへの投資の増加によって促進されています。

- 北米は、2024年に41.5%という最大の収益シェアで医療画像管理市場を支配しており、その特徴は、この地域の洗練された医療システム、高度な画像技術の早期かつ広範な導入、そしてデジタル化とEHRの実装を促進する政府の重要な取り組みである。

- アジア太平洋地域は、医療費の増加、患者数の急速な拡大、病気の早期発見に対する意識の高まり、新興国における医療インフラの継続的な改善により、予測期間中に医療画像管理市場で最も急速に成長する地域になると予想されています。

- 画像アーカイブおよび通信システム(PACS)セグメントは、特に画像検査の大部分が処理される放射線科部門において、医療画像の管理と保管における広範な使用と重要な機能により、2024年には50.5%の市場シェアで医療画像管理市場を支配します。

レポートの範囲と医療画像管理市場のセグメンテーション

|

属性 |

医療画像管理の主要市場インサイト |

|

対象セグメント |

|

|

対象国 |

北米

ヨーロッパ

アジア太平洋

中東およびアフリカ

南アメリカ

|

|

主要な市場プレーヤー |

|

|

市場機会 |

|

|

付加価値データ情報セット |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Medical Image Management Market Trends

“Enhanced Diagnostics and Workflow Optimization Through AI and Deep Learning”

- A significant and accelerating trend in the global medical image management market is the deepening integration of Artificial Intelligence (AI) and its subset, deep learning, across various stages of the imaging workflow. This fusion of technologies is fundamentally transforming diagnostic capabilities, improving workflow efficiency, and enhancing patient care

- For instance, AI algorithms are now being used to analyze vast datasets of medical images (X-rays, CTs, MRIs, ultrasounds) with remarkable speed and precision, aiding in the early detection of subtle abnormalities, such as cancerous lesions, that might be missed by the human eye. Companies such as Qure.ai and Niramai are developing AI-based diagnostic tools for specific conditions, while major players such as GE HealthCare and Siemens Healthineers are embedding AI into their imaging systems and management platforms

- AI integration in medical image management enables features such as automated image segmentation and reconstruction, improved image quality through noise reduction, and intelligent triage systems that prioritize critical cases for radiologists, significantly reducing their workload. Natural Language Processing (NLP) is also being utilized to extract relevant information from unstructured clinical notes and radiology reports, further streamlining data management and decision support

- The seamless integration of AI-powered tools with Picture archiving and communication systems (PACS) and vendor neutral archives (VNA) facilitates a more centralized and intelligent approach to managing complex imaging data. This creates a unified and automated environment for image acquisition, analysis, storage, and reporting, leading to faster turnaround times and more consistent diagnoses

- This trend towards more intelligent, intuitive, and interconnected medical imaging systems is fundamentally reshaping expectations for diagnostic accuracy and efficiency in healthcare. Consequently, companies are focusing on developing AI-enabled solutions that offer enhanced diagnostic support, automated tasks, and predictive analytics capabilities

- The demand for medical image management solutions that offer seamless AI and deep learning integration is growing rapidly across hospitals, diagnostic centers, and research institutions, as healthcare providers increasingly prioritize improved patient outcomes, reduced costs, and optimized operational workflows

Medical Image Management Market Dynamics

Driver

“Increasing Volume of Medical Images and Rising Prevalence of Chronic Diseases”

- The escalating volume of medical images generated from advanced diagnostic modalities, coupled with the rising global prevalence of chronic diseases, is a significant driver for the heightened demand for medical image management solutions

- For instance, the continuous innovation in imaging technologies such as MRI, CT scans, and PET scans, alongside the growing use of 3D and 4D imaging, results in massive datasets that require sophisticated systems for efficient storage, retrieval, and analysis. This surge in data necessitates robust image management systems to ensure data integrity and accessibility

- As the global population ages, there's a corresponding increase in the incidence of chronic conditions such as cancer, cardiovascular diseases, and neurological disorders, all of which heavily rely on diagnostic imaging for early detection, diagnosis, and ongoing monitoring. This demographic shift directly translates to a greater demand for imaging procedures and, consequently, for comprehensive medical image management solutions

- Furthermore, government initiatives promoting the adoption of electronic medical records (EMRs) and the digitalization of healthcare data worldwide are making medical image management systems an indispensable part of modern healthcare infrastructure. These systems facilitate seamless integration with EMRs, improving patient care coordination and streamlining clinical workflows

- The critical need for accurate and timely diagnoses, coupled with the desire for efficient workflows and improved patient outcomes, are key factors propelling the adoption of medical image management solutions in hospitals, diagnostic centers, and other healthcare facilities. The growing awareness among healthcare providers about the benefits of centralized and accessible imaging data further contributes to market growth

Restraint/Challenge

“Data Security & Privacy Concerns and High Implementation & Interoperability Costs”

- Concerns surrounding the cybersecurity vulnerabilities of healthcare IT systems, including medical image management solutions, pose a significant challenge to broader market penetration. As these systems rely on network connectivity and software to manage sensitive patient data, they are susceptible to hacking attempts and data breaches, raising anxieties among healthcare providers and patients about the security and privacy of their information

- For instance, high-profile reports of ransomware attacks and data breaches targeting healthcare organizations have made some providers hesitant to invest in or fully integrate advanced digital image management solutions. The potential for disruption to patient care and the severe financial and legal repercussions associated with such incidents further amplify these concerns

- ·Addressing these cybersecurity concerns through robust encryption, secure authentication protocols, regular software updates, and adherence to stringent regulatory frameworks is crucial for building trust among healthcare institutions. Companies in the medical image management space, such such as Sectra and Philips, emphasize their advanced security features and compliance certifications in their offerings to reassure potential buyers. In addition, the relatively high initial cost of some comprehensive medical image management systems, compared to maintaining older, disparate systems, can be a barrier to adoption for budget-sensitive healthcare providers, particularly in developing regions or for smaller clinics

- While prices are gradually decreasing due to technological advancements and competitive pressure, the perceived premium for advanced medical image management technology can still hinder widespread adoption, especially for those who do not immediately see the compelling return on investment or the necessity for the full suite of advanced features offered

- Overcoming these challenges through enhanced cybersecurity measures, clear demonstrations of ROI, comprehensive training on data security best practices, and the development of more scalable and affordable medical image management options will be vital for sustained market growth

Medical Image Management Market Scope

The market is segmented on the basis of product, delivery model, specialty, end user, and distribution channel

- By Product

On the basis of product, the medical image management market is segmented into Picture Archiving & Communication system (PACS), vendor neutral archives (VNA), application-independent clinical archive (AICA), and enterprise viewers/universal viewers. The picture archiving & communication system (PACS) segment dominates the largest market revenue share of 50.5% in 2024, driven by its long-standing adoption and critical role in storing, retrieving, and distributing medical images, especially within radiology departments. PACS remains foundational for efficient image workflow and diagnostic reporting in healthcare facilities globally.

The vendor neutral archives (VNA) segment is anticipated to witness the fastest growth rate from 2025 to 2032, fueled by the increasing need for centralized, vendor-agnostic storage solutions that address interoperability challenges and reduce data silos. VNAs offer healthcare organizations greater flexibility, easier data migration, and a unified view of patient imaging data across multiple specialties and departments, contributing to enhanced data governance and long-term cost savings

- By Delivery Mode

On the basis of delivery model, the medical image management market is segmented into hybrid, web/cloud based, and on premises. The on-premises segment held the largest market revenue share in 2024, driven by the traditional preference of large hospitals and healthcare systems for maintaining direct control over their data security and infrastructure. On-premise solutions offer maximum customization and data sovereignty, appealing to organizations with stringent security policies and significant IT resources.

The web/cloud based segment is expected to witness the fastest CAGR from 2025 to 2032, driven by its benefits of scalability, lower upfront costs, remote accessibility, and reduced IT maintenance burden. Cloud-based solutions facilitate teleradiology, enable easier data sharing across geographically dispersed facilities, and support the growing trend of remote work for healthcare professionals, making them increasingly attractive to a wide range of providers.

- By Specialty

On the basis of specialty, the medical image management market is segmented into surgery, oncology, dental, and others. The oncology segment held a significant market share in 2024, largely due to the high incidence and increasing prevalence of cancer worldwide, which necessitates extensive diagnostic imaging for screening, diagnosis, staging, and treatment monitoring. The complex nature of cancer care often requires multi-modal imaging and long-term image archiving, driving the demand for specialized management solutions

The orthopedics segment is anticipated to witness substantial growth. This is due to the high demand for imaging in diagnosing musculoskeletal conditions, such fractures, arthritis, and joint replacements, often requiring detailed image analysis and longitudinal tracking for treatment and recovery.

- By End User

On the basis of end user, the medical image management market is segmented into hospitals, radiology chains/centers, ambulatory surgery center, and others. The hospitals segment dominates the largest market revenue share in 2024, accounting for 58% of the revenue. This dominance stems from their comprehensive range of imaging modalities, large patient volumes, and the critical need for integrated systems to manage vast amounts of medical data generated from diverse departments. Hospitals serve as primary centers for a wide array of diagnostic imaging procedures.

放射線科チェーン/センターセグメントは、診断画像サービスへの特化、開業医からの患者紹介の増加、そして最適化された画像管理ワークフローによる効率性と費用対効果への注力により、予測期間中に大幅な成長が見込まれています。これらのセンターは、高度な画像管理システムを活用して高スループットに対応し、迅速な診断レポートを提供しています。

- 流通チャネル別

流通チャネルに基づいて、医療画像管理市場は、直接入札、サードパーティ管理者、その他に分類されます。2024年には、直接入札セグメントが大きな市場シェアを占めました。これは、大規模な病院や統合医療ネットワークが、包括的なソリューション、長期的なサポート、既存のITインフラとのカスタマイズされた統合を確保するために、入札を通じて主要ベンダーから直接調達することを好む傾向があるためです。

サードパーティの管理者セグメントは、2025年から2032年にかけて最も高い成長率を示すと予想されています。この成長は、マネージドサービス、IT運用のアウトソーシング、そして社内インフラの負担なしにデータ管理とサイバーセキュリティに関する専門知識を求める需要の増加によって促進されています。サードパーティの管理者は、拡張性と費用対効果に優れたソリューションを提供しており、特に中小規模の医療施設にとって魅力的です。

医療画像管理市場の地域分析

- 北米は、同地域の洗練された医療システム、先進的な画像技術の早期かつ広範な導入、デジタル化とEHRの実装を促進する政府の重要な取り組みにより、2024年には医療画像管理市場において最大の収益シェア41.5%を占め、市場を支配しています。

- この地域の消費者と医療提供者は、複雑な画像データを効率的かつ安全に管理するための統合ソリューションを高く評価しています。

- この広範な導入は、有利な償還ポリシー、患者の転帰改善への強い重点、そして多数の主要な業界プレーヤーの存在によってさらに支えられており、高度な医療画像管理システムは、この地域の医療提供の重要な要素として確立されています。

米国医療画像管理市場の洞察

米国の医療画像管理市場は、デジタル医療記録と高度な画像技術の急速な導入に牽引され、2024年には北米市場において最大の収益シェア(76.6%)を占めると予測されています。医療機関は、医療画像の増加と複雑化に対応するため、画像アーカイブ・コミュニケーションシステム(PACS)とベンダーニュートラル・アーカイブ(VNA)の統合をますます重視しています。AIを活用した分析とクラウドベースのプラットフォームへの旺盛な需要に加え、政府および民間による医療ITへの多額の投資も、市場をさらに牽引しています。

欧州医療画像管理市場の洞察

欧州の医療画像管理市場は、医療費の増加、高齢化率の上昇、そして早期疾患発見への意識の高まりを主な要因として、予測期間を通じて大幅なCAGRで拡大すると予測されています。データのプライバシーとセキュリティに関する厳格な規制枠組みも、高度な画像管理ソリューションの導入を後押ししています。この地域では、AIを画像診断ワークフローに統合し、病院や診療所全体の診断効率向上を目指した相互運用性の高いシステムへの移行が急速に進んでいます。

英国の医療画像管理市場に関する洞察

英国の医療画像管理市場は、国民保健サービス(NHS)による継続的なデジタル化の取り組みと、患者ケアパスの改善への重点的な取り組みに牽引され、予測期間中に注目すべきCAGRで成長すると予想されています。効率的な画像共有への需要の高まり、放射線科向けAIへの多額の投資、そして電子医療記録(EHR)の導入は、医療提供者による高度な画像管理ソリューションの導入を促進しています。英国は技術革新と医療プロセスの合理化に重点を置いており、今後も市場の成長を刺激すると予想されます。

ドイツ医療画像管理市場インサイト

ドイツの医療画像管理市場は、デジタルヘルスソリューションへの認知度の高まり、堅牢な医療インフラ、そして技術革新への注力に支えられ、予測期間中に大幅なCAGRで拡大すると予想されています。ドイツの充実した医療システムは、質の高い患者ケアと高度な診断能力への重点と相まって、高度な画像管理システムの導入を促進しています。また、医療画像ワークフローにおけるAIとクラウドコンピューティングの統合もますます普及しており、安全で効率的な医療ITを求める現地の傾向と一致しています。

アジア太平洋地域の医療画像管理市場に関する洞察

アジア太平洋地域の医療画像管理市場は、医療費の増加、医療インフラの急速な拡大、そして中国、日本、インドなどの国々における技術進歩に牽引され、予測期間中に最も高いCAGRで成長する見込みです。デジタル化と医療へのアクセスを促進する政府の取り組みに支えられ、この地域ではデジタルヘルスケアへの関心が高まっており、医療画像管理ソリューションの導入が促進されています。さらに、慢性疾患の罹患率の上昇と患者数の増加も、アジア太平洋地域全体の市場拡大を加速させています。

日本医療画像管理市場インサイト

日本の医療画像管理市場は、ハイテク文化、急速な高齢化、そして高度な診断能力に対する需要の高まりにより、急速に成長しています。日本市場では医療診断の精度が重視されており、複雑な画像データの効率的な処理に対するニーズの高まりが医療画像管理の導入を牽引しています。医療提供者が診断精度とワークフロー効率の向上を目指す中、医療画像分野へのAIの統合と政府によるデジタルヘルス変革の推進が成長を牽引しています。

インドの医療画像管理市場の洞察

インドの医療画像管理市場は、2024年にアジア太平洋地域において大きな市場収益シェアを占めました。これは、同国の医療セクターの拡大、急速なデジタル化、そして慢性疾患による患者負担の増加によるものです。インドでは、医療インフラへの投資の増加と電子カルテの導入拡大により、公立病院と私立病院の両方で高度な画像管理ソリューションがますます普及しています。政府によるデジタルヘルスへの取り組みの推進と、国内外の企業による費用対効果の高いソリューションの提供が、インド市場の成長を牽引する主要な要因となっています。

医療画像管理市場シェア

医療画像管理業界は、主に次のような定評のある企業によって主導されています。

- GEヘルスケア(米国)

- Koninklijke Philips NV (オランダ)

- シーメンス・ヘルシニアーズAG(ドイツ)

- 富士フイルムホールディングス株式会社(日本)

- キヤノンメディカルシステムズ株式会社(日本)

- アグファ・ゲバルトグループ(ベルギー)

- ケアストリームヘルス(米国)

- Sectra AB(スウェーデン)

- コニカミノルタ株式会社(日本)

- メラティブ(米国)

- インフィニットヘルスケア株式会社(韓国)

- チェンジ・ヘルスケア(米国)

- Mach7 Technologies(オーストラリア)

- インテルラッド(カナダ)

- アンブラヘルス(米国)

- テラリコン(米国)

- Visage Imaging, Inc.(米国)

- ノバラッド(米国)

- RamSoft, Inc.(カナダ)

- デル社(米国)

世界の医療画像管理市場の最新動向

- 2024年11月、GEヘルスケアとラドネットは、画像システムの変革と医用画像における人工知能(AI)の導入の加速を目的とした戦略的提携を発表した。特に乳がん検診の強化に重点を置く。

- 2024年1月、ロイヤル フィリップスは、インド放射線画像協会(IRIA)2024の第76回年次会議で、次世代の超音波、MRI、CTシステムを含むAI主導のエンタープライズ画像ポートフォリオの包括的なスイートを展示しました。

- In January 2024, FUJIFILM Diosynth Biotechnologies and SHL Medical announced a strategic partnership aimed at addressing the increasing market demand for auto-injector medicines. This collaboration, integrated into SHL’s Alliance Management Program, seeks to optimize processes and enhance efficiency for pharmaceutical and biotech firms offering finished self-injection device services, primarily leveraging SHL’s leading auto-injector platform, Molly

- In January 2024, Royal Philips, a global leader in health technology, showcased its robust portfolio of AI-driven enterprise imaging solutions at the 76th Annual Conference of the Indian Radiological and Imaging Association (IRIA) 2024. During this event in Vijayawada, Philips highlighted its next-generation Ultrasound, MRI, and CT systems, and also introduced its new state-of-the-art Compact Ultrasound System 5000 series, emphasizing performance and portability derived from its premium ultrasound capabilities. This demonstrates Philips' commitment to advancing diagnostic imaging through integrated AI

- In June 2024, Apollo released enhanced multidisciplinary medical image management capabilities of its arcc platform at SIIM24

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。