سوق إدارة الأساطيل في كندا مجزأ، ويضم العديد من الشركات العالمية. تقدم هذه الشركات أسعارًا تنافسية وحلولاً متنوعة ومنتجات مبتكرة وخدمات في جميع أنحاء العالم. ونظرًا لوجود هذه الشركات على المستويين الإقليمي والدولي، يقدم الموردون والمصنعون منتجات وخدمات بحلول وميزات متنوعة تناسب جميع الميزانيات. ويساهم الطلب المتزايد على الخدمات اللوجستية نتيجةً لقطاع التجارة الإلكترونية، بالإضافة إلى تزايد الطلب على تحسين خدمات العملاء، في دفع نمو السوق بشكل كبير. علاوةً على ذلك، فإن التبني السريع لأنظمة إدارة الوقود في الأساطيل، وزيادة الطلب على التأجير الشامل، يُعززان نمو السوق. ومع ذلك، من المتوقع أن يُعيق انخفاض كفاءة الاتصال والتوجيه غير السليم لتمكين المسار نمو السوق. علاوةً على ذلك، من المتوقع أن يُشكل ارتفاع التهديدات الإلكترونية تحديًا لنمو السوق. ومع ذلك، من المتوقع أن تُوفر زيادة النماذج القائمة على البيانات في مجال التنقل فرصًا مربحة لنمو السوق.

يمكنك الوصول إلى التقرير الكامل على https://www.databridgemarketresearch.com/reports/canada-fleet-management-market

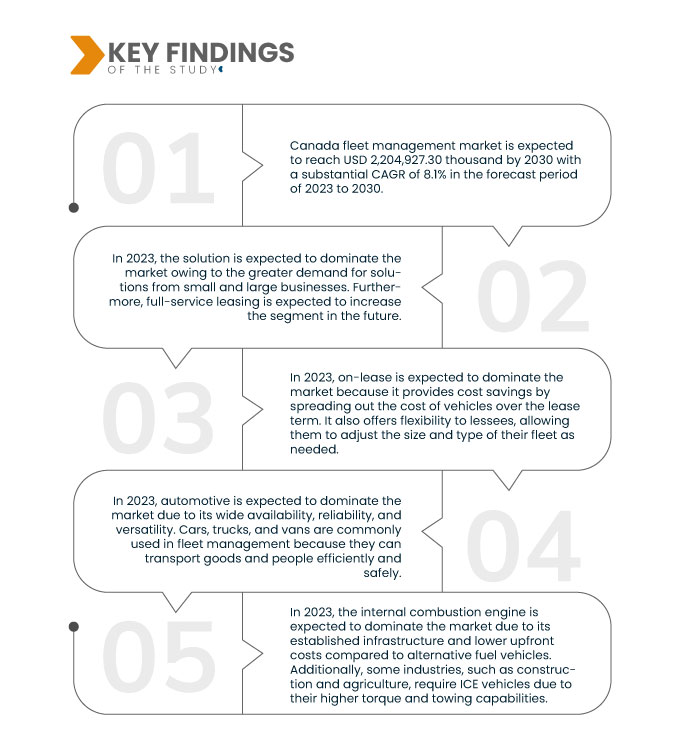

تشير تحليلات Data Bridge Market Research إلى أن سوق إدارة الأسطول الكندي من المتوقع أن يصل إلى 2،204،927.30 ألف دولار أمريكي بحلول عام 2030 من 1،189،531.99 ألف دولار أمريكي في عام 2022، بنمو قدره 8.1٪ في الفترة المتوقعة من 2023 إلى 2030.

النتائج الرئيسية للدراسة

ارتفاع الطلب على تحسين خدمات العملاء

أصبح العملاء اليوم أكثر ذكاءً وتوقعاتهم أعلى من أي وقت مضى. يُعدّ رضا العملاء وسعادتهم من أهم الاعتبارات لأي شركة. بغض النظر عن قطاع الأعمال، لن يبقى العملاء غير الراضين عملاءً للشركة لفترة طويلة، لذا من المهم الحفاظ على رضاهم ومنحهم شعورًا بالتقدير. وينطبق هذا على الخدمات اللوجستية وإدارة الأساطيل، حيث يُعدّ الحفاظ على العملاء مفتاح النجاح على المدى الطويل.

يُعدّ تحسين خدمات العملاء ورضاهم من خلال تحسين أداء إدارة الأساطيل عاملاً رئيسياً يُتوقع أن يُعزز نمو السوق. في ظلّ المنافسة الشديدة اليوم، تُدرك الشركات أهمية رضا العملاء، وتستخدم التقنيات المتقدمة في حلول إدارة الأساطيل لتحسين عملياتها وتحسين تجارب عملائها.

نطاق التقرير وتقسيم السوق

مقياس التقرير

|

تفاصيل

|

فترة التنبؤ

|

2023 - 2030

|

سنة الأساس

|

2022

|

السنوات التاريخية

|

2021 (قابلة للتخصيص حتى 2015 – 2020)

|

الوحدات الكمية

|

الإيرادات بالألف دولار أمريكي

|

القطاعات المغطاة

|

العرض (الحلول والخدمات)، نوع الإيجار (بالإيجار وبدون إيجار)، وسيلة النقل (السيارات والبحرية والمركبات المتحركة والطائرات)، نوع المركبة (محرك الاحتراق الداخلي والمركبة الكهربائية)، الأجهزة (أجهزة تتبع نظام تحديد المواقع العالمي (GPS)، كاميرات لوحة القيادة، علامات تتبع البلوتوث، مسجلات البيانات، وغيرها)، حجم الأسطول (أساطيل صغيرة (1-5 مركبات)، أساطيل متوسطة (5-20 مركبة) وأساطيل كبيرة وكبيرة (20-50+ مركبة)، نطاق الاتصالات (اتصالات قصيرة المدى واتصالات طويلة المدى)، نموذج النشر (محلي، سحابي، وهجين)، التكنولوجيا (GNSS، الأنظمة الخلوية، التبادل الإلكتروني للبيانات (EDI)، الاستشعار عن بعد، الطريقة الحسابية واتخاذ القرار، RFID، وغيرها)، الوظائف (مراقبة سلوك السائق، استهلاك الوقود، إدارة الأصول، شكوى ELD، إدارة الطريق، تحديثات صيانة المركبة، جدول التسليم، الوقاية من الحوادث، موقع المركبة في الوقت الفعلي، تطبيقات الهاتف المحمول وغيرها، والعمليات (الخاصة والتجارية)، ونوع العمل (الأعمال الصغيرة والكبيرة)، والمستخدم النهائي (السيارات، والنقل والخدمات اللوجستية، وتجارة التجزئة، والتصنيع، والأغذية والمشروبات، والطاقة والمرافق، والتعدين، والحكومة، والرعاية الصحية، والزراعة، والبناء، وغيرها)

|

البلد المغطى

|

كندا

|

الجهات الفاعلة في السوق المغطاة

|

Element Fleet Management Corp. (الولايات المتحدة)، Verizon. (الولايات المتحدة)، Geotab Inc. (كندا)، Motive Technologies, Inc. (الولايات المتحدة)، Jim Pattison Lease (كندا)، Holman, Inc. (الولايات المتحدة)، Cisco Systems, Inc. (الولايات المتحدة)، Donlen (الولايات المتحدة)، Omnitracs (جزء من Solera) (الولايات المتحدة)، Wheels Inc. (الولايات المتحدة)، DENSO CORPORATION (اليابان)، AT&T (الولايات المتحدة)، Continental AG (ألمانيا)، ORBCOMM (الولايات المتحدة)، Summit Fleet Leasing and Management (كندا)، Siemens (ألمانيا)، ADDISON LEASING OF CANADA LTD (كندا)، Robert Bosch GmbH (ألمانيا)، RAM Tracking (المملكة المتحدة)، TRANSFLO (الولايات المتحدة)، Foss National Leasing Ltd. (كندا)، Samsara Inc. (الولايات المتحدة)، Sierra Wireless. (الولايات المتحدة)، Mendix Technology BV (هولندا)، ALD Automotive (فرنسا)، IBM (الولايات المتحدة)، ADDISON LEASING OF CANADA LTD (كندا)، Robert Bosch GmbH (ألمانيا)، RAM Tracking (المملكة المتحدة)، وTRANSFLO (الولايات المتحدة)، من بين شركات أخرى

|

نقاط البيانات التي يغطيها التقرير

|

بالإضافة إلى الرؤى حول سيناريوهات السوق مثل القيمة السوقية ومعدل النمو والتجزئة والتغطية الجغرافية واللاعبين الرئيسيين، تتضمن تقارير السوق التي تم تنظيمها بواسطة Data Bridge Market Research أيضًا تحليلًا متعمقًا من الخبراء والإنتاج والقدرة التمثيلية الجغرافية للشركة وتخطيطات الشبكة للموزعين والشركاء وتحليل اتجاهات الأسعار التفصيلية والمحدثة وتحليل العجز في سلسلة التوريد والطلب.

|

تحليل القطاعات

يتم تقسيم سوق إدارة الأسطول في كندا إلى ثلاثة عشر قطاعًا بارزًا بناءً على العرض ونوع الإيجار ووسيلة النقل ونوع السيارة والأجهزة وحجم الأسطول ونطاق الاتصالات ونموذج النشر والتكنولوجيا والوظائف والعمليات ونوع العمل والمستخدم النهائي.

- على أساس العرض، يتم تقسيم السوق إلى حلول وخدمات.

في عام 2023، من المتوقع أن يهيمن قطاع الحلول على السوق

ومن المتوقع أن تهيمن الحلول على السوق في عام 2023 بحصة سوقية تبلغ 65.49% بسبب الطلب الأكبر على الحلول من الشركات الصغيرة والكبيرة.

- بناءً على نوع التأجير، يُقسّم السوق إلى إيجارات مُؤجّرة وغير مُؤجّرة. وفي عام ٢٠٢٣، من المتوقع أن يُهيمن قطاع التأجير المُؤجّر على السوق بحصة سوقية تبلغ ٧٠.٠٥٪.

- بناءً على الأجهزة، يُقسّم السوق إلى أجهزة تتبع نظام تحديد المواقع العالمي (GPS)، وكاميرات DASH، وعلامات تتبع بلوتوث، وأجهزة تسجيل البيانات، وغيرها. في عام 2023، من المتوقع أن تهيمن أجهزة تتبع نظام تحديد المواقع العالمي (GPS) على السوق بحصة سوقية تبلغ 38.37%.

- على أساس حجم الأسطول، يتم تقسيم السوق إلى أساطيل صغيرة (1-5 مركبات)، وأساطيل متوسطة (5-20 مركبة)، وأساطيل كبيرة ومؤسسية (20-50+ مركبة).

في عام 2023، من المتوقع أن تهيمن شريحة الأساطيل الصغيرة (1-5 مركبات) على السوق

من المتوقع أن تهيمن الأساطيل الصغيرة (1-5 مركبات) على السوق في عام 2023 بحصة سوقية تبلغ 48.31٪ حيث يتم استخدامها بشكل رئيسي من قبل الشركات الصغيرة وهي فعالة من حيث التكلفة بالنسبة لهم.

- بناءً على مدى الاتصالات، يُقسّم السوق إلى اتصالات قصيرة المدى واتصالات طويلة المدى. وفي عام ٢٠٢٣، من المتوقع أن يهيمن قطاع الاتصالات قصيرة المدى على السوق بحصة سوقية تبلغ ٥٧.٧٠٪.

- بناءً على نموذج النشر، يُقسّم السوق إلى حلول محلية، وحلول سحابية، وحلول هجينة. ومن المتوقع أن يهيمن قطاع الحلول المحلية على السوق في عام 2023 بحصة سوقية تبلغ 62.50%.

- بناءً على التكنولوجيا، يُقسّم السوق إلى أنظمة الملاحة العالمية عبر الأقمار الصناعية (GNSS)، والأنظمة الخلوية، وتبادل البيانات الإلكتروني (EDI)، والاستشعار عن بُعد، والأساليب الحسابية واتخاذ القرارات، وتقنية تحديد الهوية بموجات الراديو (RFID)، وغيرها. ومن المتوقع أن يهيمن قطاع أنظمة الملاحة العالمية عبر الأقمار الصناعية (GNSS) على السوق بحصة سوقية تبلغ 45.93% في عام 2023.

- بناءً على الوظيفة، يُقسّم السوق إلى: مراقبة سلوك السائق، واستهلاك الوقود، وإدارة الأصول، والامتثال لأجهزة تسجيل البيانات الإلكترونية (ELD)، وإدارة المسارات، وتحديثات صيانة المركبات، وجداول التسليم، والوقاية من الحوادث، وتحديد موقع المركبة في الوقت الفعلي، وتطبيقات الجوال، وغيرها. في عام 2023، من المتوقع أن يهيمن قطاع إدارة الأصول على السوق بحصة سوقية تبلغ 27.13%.

- بناءً على العمليات، يُقسّم السوق إلى قطاع خاص وقطاع تجاري. وفي عام ٢٠٢٣، من المتوقع أن يُهيمن القطاع التجاري على السوق بحصة سوقية تبلغ ٦٨.٣٧٪.

- بناءً على نوع العمل، يُقسّم السوق إلى شركات صغيرة وكبيرة. وفي عام ٢٠٢٣، من المتوقع أن تهيمن الشركات الكبيرة على السوق بحصة سوقية تبلغ ٦٥.١٣٪.

- بناءً على نوع المركبة، يُقسّم السوق إلى محرك احتراق داخلي (ICE) وسيارة كهربائية. وفي عام 2023، من المتوقع أن يهيمن قطاع محركات الاحتراق الداخلي (ICE) على السوق بحصة سوقية تبلغ 78.87%.

- بناءً على وسيلة النقل، يُقسّم السوق إلى سيارات، وسفن، وعربات، وطائرات. ومن المتوقع أن يهيمن قطاع السيارات على السوق بحصة سوقية تبلغ 67.51% في عام 2023.

- بناءً على المستخدم النهائي، يُقسّم السوق إلى قطاعات السيارات، والنقل والخدمات اللوجستية، وتجارة التجزئة، والتصنيع، والأغذية والمشروبات، والطاقة والمرافق، والتعدين، والحكومة، والرعاية الصحية، والزراعة، والبناء، وغيرها. ومن المتوقع أن يهيمن قطاع السيارات على السوق بحصة سوقية تبلغ 29.95% في عام 2023.

اللاعبون الرئيسيون

تعترف شركة Data Bridge Market Research بالشركات التالية باعتبارها اللاعبين الرئيسيين في سوق إدارة الأسطول في كندا وهي Element Fleet Management Corp. (الولايات المتحدة)، وVerizon. (الولايات المتحدة)، وGeotab Inc. (كندا)، وMotive Technologies, Inc. (الولايات المتحدة)، وJim Pattison Lease (كندا)، وHolman, Inc. (الولايات المتحدة)، وغيرها.

تطوير السوق

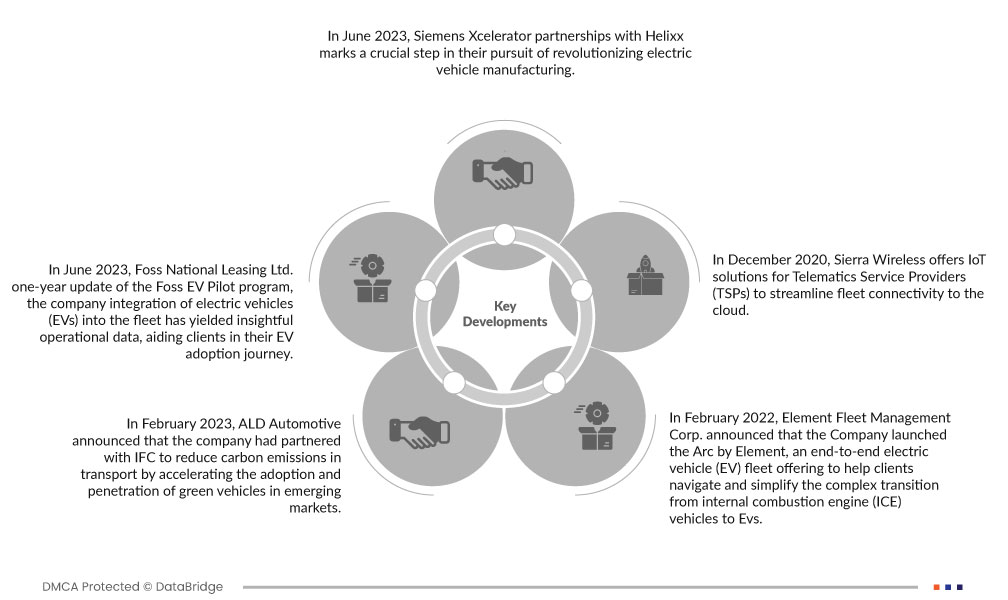

- في يونيو 2023، تُمثل شراكة سيمنز إكسيليريتور مع هيليكس خطوةً حاسمةً في سعيهما لإحداث ثورة في تصنيع المركبات الكهربائية. من خلال دمج برامج وخدمات سيمنز الصناعية، تهدف هيليكس إلى نشر نظامها المبتكر لتصنيع المركبات الكهربائية بسرعة في جميع أنحاء العالم، مما يعزز النمو الاقتصادي المستدام من خلال حلول تنقل حضري سهلة المنال وخالية من الانبعاثات. يُبرز هذا التعاون مفهوم هيليكس الرائد "مراكز هيليكس للتنقل"، والذي سيُمكّن المصانع المرخصة عالميًا من إنتاج مجموعة متنوعة من المركبات الكهربائية، مما يُعزز تأثيرها بشكل كبير يتجاوز توقعات الإنتاج الأولية.

- في يونيو 2023، أصدرت شركة فوس ناشيونال ليسينج المحدودة تحديثًا سنويًا لبرنامج فوس التجريبي للسيارات الكهربائية، والذي أثمر عن بيانات تشغيلية قيّمة، ساعدت العملاء في رحلة تبنيهم للسيارات الكهربائية. يساهم هذا البرنامج بفعالية في تسهيل الانتقال إلى حلول إدارة أساطيل مستدامة من خلال معالجة جوانب عدم اليقين. وفي الختام، تُبرز جهود الشركة المستمرة الدور المحوري للبرنامج في تسهيل اتخاذ قرارات مدروسة من أجل مستقبل أكثر استدامة وكفاءة.

- في فبراير 2023، أعلنت شركة ALD Automotive عن شراكتها مع مؤسسة التمويل الدولية (IFC) للحد من انبعاثات الكربون في قطاع النقل من خلال تسريع اعتماد المركبات الصديقة للبيئة وانتشارها في الأسواق الناشئة. وقد استثمرت مؤسسة التمويل الدولية 400 مليون دولار أمريكي من خلال هذه الشراكة في الشركة، ومن المتوقع أن تُسهم في تنمية أسطولها الصديق للبيئة، الذي يضم مزيجًا من المركبات الهجينة، والهجينة القابلة للشحن، والمركبات الكهربائية التي تعمل بالبطاريات. ومن المتوقع أن تُعزز هذه الشراكة قدرة الشركة على الوصول إلى السوق، وتعزز هيمنتها على سوق إدارة الأساطيل في كندا.

- في فبراير 2022، أعلنت شركة إليمنت لإدارة الأسطول عن إطلاقها خدمة Arc by Element، وهي خدمة شاملة لأسطول المركبات الكهربائية، تهدف إلى مساعدة العملاء على اجتياز وتبسيط عملية الانتقال المعقدة من مركبات محرك الاحتراق الداخلي إلى المركبات الكهربائية. ومن خلال هذه الخدمة، ساعدت الشركة عملاءها على تقييم هذه التقنية الجديدة وتبنيها لتحقيق أهدافهم المستدامة والاستراتيجية والاقتصادية، وعززت حضورها في سوق إدارة الأساطيل في كندا.

- في ديسمبر 2020، قدمت سييرا وايرلس حلول إنترنت الأشياء لمقدمي خدمات الاتصالات عن بُعد (TSPs) لتبسيط اتصال أساطيل المركبات بالسحابة. يمكن لمقدمي خدمات الاتصالات الاستفادة من تقنية إنترنت الأشياء لجمع البيانات الفورية من أساطيل المركبات، مما يُمكّن من تحسين الصيانة، وكفاءة استهلاك الوقود، وخدمة العملاء، والأمان. يُسهّل حل أوكتاف المتكامل من الحافة إلى السحابة استخراج البيانات وتنظيمها ودمجها بشكل آمن في الأنظمة السحابية، مما يُعزز في نهاية المطاف تطوير أنظمة الاتصالات عن بُعد للأساطيل وتوليد القيمة في الاقتصاد المتصل.

لمزيد من المعلومات التفصيلية حول تقرير سوق إدارة الأسطول في كندا، انقر هنا - https://www.databridgemarketresearch.com/reports/canada-fleet-management-market