مواد الفضاء والدفاع قطاع متخصص ضمن صناعة المواد، يُعنى بتوفير مواد مصممة لتطبيقات الفضاء والدفاع. يجب أن تستوفي هذه المواد، بما في ذلك المعادن والمركبات والسيراميك والبوليمرات والمكونات الإلكترونية، متطلبات صارمة للأداء والسلامة. وهي ضرورية لبناء وصيانة وتشغيل الطائرات والمركبات الفضائية والمركبات العسكرية والأسلحة والأنظمة المرتبطة بها. كما أنها تلعب دورًا محوريًا في تمكين تطوير أنظمة فضاء ودفاع عالية الأداء وموثوقة.

يمكنك الوصول إلى التقرير الكامل على https://www.databridgemarketresearch.com/reports/global-aerospace-and-defense-materials-market

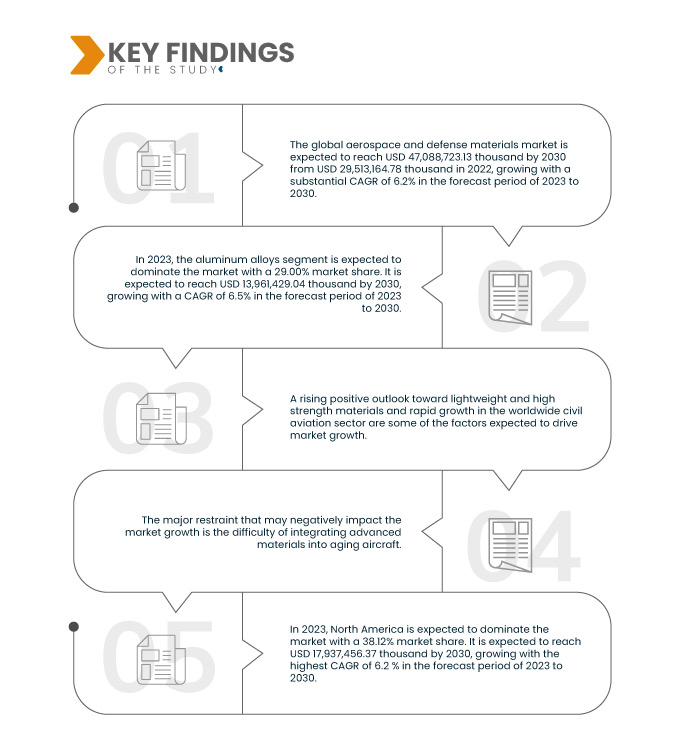

تحلل شركة Data Bridge Market Research سوق المواد الجوية والدفاعية العالمية ومن المتوقع أن يصل إلى 47،088،723.13 ألف دولار أمريكي بحلول عام 2030 من 29،513،164.78 ألف دولار أمريكي في عام 2022، بنمو بمعدل نمو سنوي مركب كبير يبلغ 6.2٪ في الفترة المتوقعة من 2023 إلى 2030. إن التوقعات الإيجابية المتزايدة تجاه المواد خفيفة الوزن وعالية القوة ستدفع نمو السوق.

النتائج الرئيسية للدراسة

تخصيصات حكومية متزايدة لتمويل الدفاع

تُحفّز ميزانيات الدفاع المتزايدة الاستثمارات في التقنيات المتقدمة، مما يؤدي إلى زيادة الطلب على مواد متخصصة مثل المواد المركبة والسبائك والمواد خفيفة الوزن والطلاءات لتعزيز أداء المعدات العسكرية ومتانتها. وتتيح ميزانيات الدفاع الموسعة للحكومات والمقاولين الاستثمار في الجيل القادم من الطائرات والسفن البحرية والمركبات البرية والأسلحة المتطورة، مما يتطلب مواد خفيفة الوزن ومتينة مثل المواد المركبة الكربونية والبوليمرات المتقدمة للبناء والصيانة. إضافةً إلى ذلك، يُحفّز التمويل الدفاعي المتزايد الابتكارات التكنولوجية والتعاون داخل القطاع. وتتعاون الحكومات مع الشركات الخاصة ومؤسسات البحث والجامعات لتطبيق ابتكارات في علوم وتكنولوجيا المواد. ويؤدي هذا النهج التعاوني إلى تطوير مواد متطورة مُصمّمة خصيصًا لتلبية احتياجات الدفاع المُحدّدة. وقد دفع الطلب على تقنية التخفي إلى تطورات كبيرة في المواد المُمتصة للرادار.

نطاق التقرير وتقسيم السوق

مقياس التقرير

|

تفاصيل

|

فترة التنبؤ

|

من 2023 إلى 2030

|

سنة الأساس

|

2022

|

السنوات التاريخية

|

2021 (قابلة للتخصيص حتى 2020 - 2015)

|

الوحدات الكمية

|

الإيرادات بالألف دولار أمريكي

|

القطاعات المغطاة

|

المنتج (سبائك الألومنيوم، والمركبات، والسبائك المقاومة للحرارة، والبلاستيك والبوليمرات، والسبائك الفائقة، والسيراميك، والصلب، والمركبات النانوية ، والجرافين وغيرها)، والتطبيق (هياكل الطائرات/الهياكل الجوية، وأنظمة الدفع، والمكونات، وتصميمات المقصورة الداخلية، والأقمار الصناعية، ومكونات البناء والعزل وغيرها)، والاستخدام النهائي (الطيران التجاري والعسكري والأعمال والطيران العام وغيرها)

|

الدول المغطاة

|

الولايات المتحدة الأمريكية، كندا، المكسيك، فرنسا، ألمانيا، المملكة المتحدة، إسبانيا، إيطاليا، روسيا، سويسرا، هولندا، تركيا، بلجيكا وبقية أوروبا، الصين، الهند، اليابان، كوريا الجنوبية، سنغافورة، أستراليا ونيوزيلندا، ماليزيا، الفلبين، تايلاند، إندونيسيا وبقية دول آسيا والمحيط الهادئ، البرازيل، الأرجنتين وبقية دول أمريكا الجنوبية، المملكة العربية السعودية، الإمارات العربية المتحدة، جنوب أفريقيا، إسرائيل، مصر وبقية دول الشرق الأوسط وأفريقيا

|

الجهات الفاعلة في السوق المغطاة

|

شركة هندالكو للصناعات المحدودة (الهند)، شركة تاتا للأنظمة المتقدمة المحدودة (شركة تابعة لشركة تاتا سونز الخاصة المحدودة) (الهند)، شركة ماتيريون (الولايات المتحدة)، شركة بارك إيروسبيس (الولايات المتحدة)، شركة تيجين المحدودة (اليابان)، شركة توراي للصناعات (اليابان)، شركة 3 إم (الولايات المتحدة)، شركة هانتسمان الدولية (الولايات المتحدة)، شركة سافران (فرنسا)، شركة أركيما (فرنسا)، شركة سولفاي (بلجيكا)، شركة روجرز (الولايات المتحدة)، شركة ألكوا (الولايات المتحدة)، شركة أركونيك (الولايات المتحدة)، شركة هيكسل (الولايات المتحدة)، شركة كونستيليوم (فرنسا)، إيه إم جي (الولايات المتحدة)، شركة إس جي إل كاربون (ألمانيا)، شركة دوبونت (الولايات المتحدة)، شركة سابك (المملكة العربية السعودية) وغيرها.

|

نقاط البيانات التي يغطيها التقرير

|

بالإضافة إلى الرؤى حول سيناريوهات السوق مثل القيمة السوقية ومعدل النمو والتجزئة والتغطية الجغرافية واللاعبين الرئيسيين، تتضمن تقارير السوق التي تم تنظيمها بواسطة Data Bridge Market Research أيضًا تحليلًا متعمقًا من الخبراء والإنتاج والقدرة التمثيلية الجغرافية للشركة وتخطيطات الشبكة للموزعين والشركاء وتحليل اتجاهات الأسعار التفصيلية والمحدثة وتحليل العجز في سلسلة التوريد والطلب.

|

تحليل القطاعات:

يتم تقسيم سوق المواد الجوية والدفاعية العالمية إلى ثلاثة قطاعات بارزة على أساس المنتج والتطبيق والاستخدام النهائي.

- على أساس المنتج، يتم تقسيم السوق إلى سبائك الألومنيوم، والمركبات، والسبائك المقاومة للحرارة، والبلاستيك والبوليمرات، والسبائك الفائقة، والسيراميك، والصلب، والمركبات النانوية، والجرافين، وغيرها.

في عام 2023، من المتوقع أن يهيمن قطاع سبائك الألومنيوم على سوق المواد الفضائية والدفاعية العالمية

ومن المتوقع أن تهيمن سبائك الألومنيوم على السوق في عام 2023 بسبب خفة وزنها وقوتها العالية ومقاومتها للتآكل وفعاليتها من حيث التكلفة، وهو أمر بالغ الأهمية في مجال الطيران والدفاع من أجل كفاءة الوقود والسلامة الهيكلية والقدرة على تحمل التكاليف، مع أعلى حصة سوقية تبلغ 29.00٪.

- على أساس التطبيق، يتم تقسيم السوق إلى الهياكل الهيكلية للطائرات/الهياكل الجوية، وأنظمة الدفع، والمكونات، والتصميمات الداخلية للمقصورة، والأقمار الصناعية، ومكونات البناء والعزل، وغيرها.

في عام 2023، من المتوقع أن يهيمن قطاع الهياكل الهيكلية للطائرات/الهياكل الجوية على سوق المواد الفضائية والدفاعية العالمية

في عام ٢٠٢٣، من المتوقع أن تهيمن الهياكل الهيكلية للطائرات على السوق نظرًا لمتطلباتها المادية الواسعة لهياكل الطائرات وهياكلها ومكوناتها الهيكلية الأساسية الأخرى. يجب أن تكون هذه المواد خفيفة الوزن ومتينة وقادرة على تحمل مختلف الضغوط والظروف البيئية، مما يجعلها جزءًا أساسيًا من تصميم وتصنيع الطائرات، ومن المتوقع أن تسيطر على السوق بحصة سوقية تبلغ ٣٩.٣١٪.

- بناءً على الاستخدام النهائي، يُقسّم السوق إلى طيران تجاري، وعسكري، ورجال أعمال، وعام، وغيرها. وفي عام ٢٠٢٣، من المتوقع أن يهيمن القطاع التجاري على السوق بحصة سوقية تبلغ ٤٨.٩٥٪.

اللاعبون الرئيسيون

تقوم شركة Data Bridge Market Research بتحليل شركة Alcoa Corporation (الولايات المتحدة)، وSafran (فرنسا)، وArconic (الولايات المتحدة)، وHexcel Corporation (الولايات المتحدة)، وTEIJIN LIMITED (اليابان) باعتبارها اللاعبين الرئيسيين في السوق.

تطوير السوق

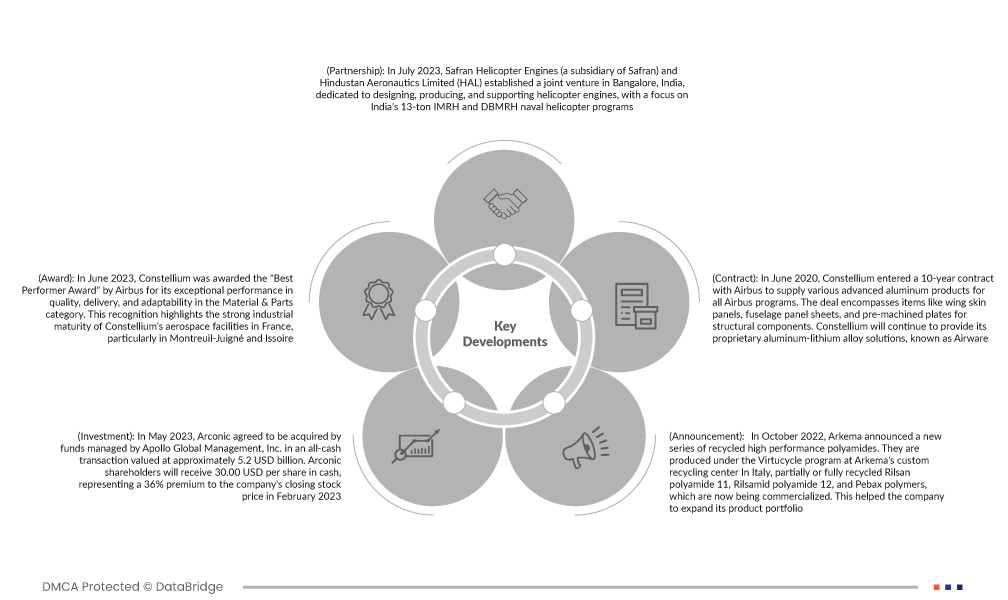

- في يوليو 2023، أسست شركة سافران لمحركات المروحيات (التابعة لسافران) وشركة هندوستان للملاحة الجوية المحدودة (HAL) مشروعًا مشتركًا في بنغالور، الهند، مُخصصًا لتصميم وإنتاج ودعم محركات المروحيات، مع التركيز على برامج المروحيات البحرية الهندية IMRH وDBMRH التي يبلغ وزنها 13 طنًا. تُمثل هذه المبادرة أول مبادرة هندية لتصميم وتصنيع المحركات داخليًا. يدعم هذا التعاون خارطة الطريق الاستراتيجية في مجال الطيران بين الهند وفرنسا، بما يتماشى مع رؤية "Aanirbhar Bharat" للاعتماد على الذات في تكنولوجيا الدفاع. تستند هذه الشراكة إلى العلاقة طويلة الأمد بين الشركتين، مستفيدةً من خبرة HAL في التصنيع وخبرة سافران لمحركات المروحيات في تصميم محركات التوربينات العمودية. بالإضافة إلى تاريخهما الناجح، سيستكشف المشروع المشترك فرصًا تجارية جديدة في مجال الطيران.

- في يونيو 2023، حصلت شركة كونستيليوم على جائزة "أفضل أداء" من إيرباص لأدائها الاستثنائي في الجودة والتسليم والقدرة على التكيف ضمن فئة المواد والقطع. يُبرز هذا التكريم النضج الصناعي القوي لمرافق كونستيليوم في قطاع الطيران في فرنسا، وخاصةً في مونتروي-جويني وإسوار. تُزود الشركة إيرباص بمجموعة واسعة من منتجات الألمنيوم المتطورة، بما في ذلك سبيكة إيروير الخاصة بها. أعربت إنغريد يورغ، رئيسة قسم الطيران والنقل في كونستيليوم، عن امتنانها لهذا التكريم، وأكدت التزامها بالحفاظ على أدائها المتميز. كما أشادت إيرباص بجهود كونستيليوم المتواصلة لتحسين الجودة وأداء سلسلة التوريد من خلال مشاريع SQIP.

- في مايو 2023، وافقت شركة أركونيك على الاستحواذ عليها من قِبل صناديق تُديرها شركة أبولو جلوبال مانجمنت، في صفقة نقدية بالكامل تُقدر قيمتها بحوالي 5.2 مليار دولار أمريكي. سيحصل مساهمو أركونيك على 30 دولارًا أمريكيًا للسهم نقدًا، وهو ما يُمثل علاوة سعرية بنسبة 36% على سعر إغلاق سهم الشركة في فبراير 2023. بعد إتمام الصفقة، ستصبح أركونيك شركة خاصة، ولن تُتداول أسهمها في بورصة نيويورك. تُخطط أبولو لاستثمارات استراتيجية، تشمل تطوير قدرات الإنتاج والتكنولوجيا والمبادرات البيئية، لدعم نمو أركونيك في أسواق الألمنيوم المُستدام حول العالم. يهدف هذا الاستحواذ إلى تعزيز مكانة أركونيك وأهدافها طويلة المدى بدعم من خبرة أبولو.

- في أكتوبر 2022، أعلنت أركيما عن سلسلة جديدة من البولي أميدات عالية الأداء المعاد تدويرها. تُنتج هذه البوليمرات ضمن برنامج "فيرتوسايكيل" في مركز أركيما لإعادة التدوير المُخصص. في إيطاليا، تُعاد تدوير بوليمرات ريلسمان بولي أميد 11، وريلسميد بولي أميد 12، وبيباكس جزئيًا أو كليًا، وهي الآن قيد التسويق. وقد ساعد هذا الشركة على توسيع محفظة منتجاتها.

- في يونيو 2020، أبرمت شركة كونستيليوم عقدًا لمدة عشر سنوات مع إيرباص لتوريد منتجات ألمنيوم متطورة متنوعة لجميع برامج إيرباص. تشمل الصفقة ألواح أجنحة الطائرات، وألواح هيكل الطائرة، وصفائح مُجهزة مسبقًا للمكونات الهيكلية. ستواصل كونستيليوم توفير حلول سبائك الألومنيوم والليثيوم الخاصة بها، والمعروفة باسم إيروير. تُعزز هذه الاتفاقية الشراكة الراسخة بين كونستيليوم وإيرباص، مُبرزةً ريادة كونستيليوم في مجال حلول الألمنيوم المتقدمة. وقد حظيت الشركة بتقدير من إيرباص لجودة منتجاتها وأدائها التشغيلي في الماضي. سيتم الحصول على المنتجات من منشآت كونستيليوم في فرنسا والولايات المتحدة.

التحليل الإقليمي

على أساس البلد، يتم تقسيم السوق إلى الولايات المتحدة وكندا والمكسيك وفرنسا وألمانيا والمملكة المتحدة وإسبانيا وإيطاليا وروسيا وسويسرا وهولندا وتركيا وبلجيكا وبقية أوروبا والصين والهند واليابان وكوريا الجنوبية وسنغافورة وأستراليا ونيوزيلندا وماليزيا والفلبين وتايلاند وإندونيسيا وبقية دول آسيا والمحيط الهادئ والبرازيل والأرجنتين وبقية دول أمريكا الجنوبية والمملكة العربية السعودية والإمارات العربية المتحدة وجنوب إفريقيا وإسرائيل ومصر وبقية دول الشرق الأوسط وأفريقيا.

وفقًا لتحليل Data Bridge Market Research :

من المتوقع أن تهيمن أمريكا الشمالية على سوق المواد الفضائية والدفاعية العالمية

ومن المتوقع أن تهيمن أمريكا الشمالية على السوق بسبب تركيز شركات الطيران والدفاع الكبرى، والاستثمارات الحكومية الكبيرة، والبحث والتطوير، وقطاع الطيران التجاري القوي، مما يساهم في قيادة السوق.

من المتوقع أن تكون منطقة آسيا والمحيط الهادئ أسرع المناطق نموًا في سوق المواد الفضائية والدفاعية العالمية

ومن المتوقع أن تصبح منطقة آسيا والمحيط الهادئ أسرع المناطق نمواً بسبب الطلب المتزايد من الأسواق الناشئة والتوسع.

لمزيد من المعلومات التفصيلية حول تقرير سوق إمدادات التجارب السريرية في أوروبا، انقر هنا - https://www.databridgemarketresearch.com/reports/global-aerospace-and-defense-materials-market