The rising demand for advanced driver training and safety education is a significant driver of the global driving simulator market. With the increasing number of vehicles on roads worldwide and the growing incidence of traffic accidents, governments, driving schools, and transportation authorities are placing greater emphasis on improving driver competence and road safety. Driving simulators provide a safe and controlled environment where trainees can practice various driving scenarios, including hazardous road conditions, emergency situations, and complex traffic environments, without risking real-life accidents. This capability makes simulators highly valuable for both beginner drivers and professional operators, such as commercial vehicle drivers and military personnel.

Access Full Report @ https://www.databridgemarketresearch.com/reports/global-driving-simulator-market

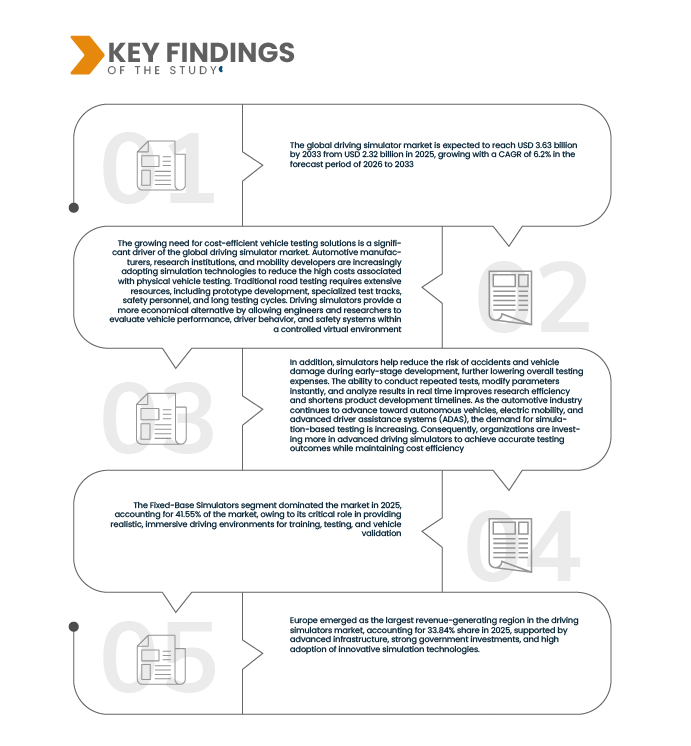

Data Bridge Market Research analyses that the Global Driving Simulator Market is expected to reach USD 3.63 billion by 2033 from USD 2.32 billion in 2025, growing with a CAGR of 6.2% in the forecast period of 2026 to 2033.

Key Findings of the Study

Growing Need for Cost-Efficient Vehicle Testing Solutions

The growing need for cost-efficient vehicle testing solutions is a significant driver of the global driving simulator market. Automotive manufacturers, research institutions, and mobility developers are increasingly adopting simulation technologies to reduce the high costs associated with physical vehicle testing. Traditional road testing requires extensive resources, including prototype development, specialized test tracks, safety personnel, and long testing cycles. Driving simulators provide a more economical alternative by allowing engineers and researchers to evaluate vehicle performance, driver behavior, and safety systems within a controlled virtual environment. These systems enable the testing of various road conditions, weather scenarios, and traffic situations without the financial and logistical burden of real-world trials.

In addition, simulators help reduce the risk of accidents and vehicle damage during early-stage development, further lowering overall testing expenses. The ability to conduct repeated tests, modify parameters instantly, and analyze results in real time improves research efficiency and shortens product development timelines. As the automotive industry continues to advance toward autonomous vehicles, electric mobility, and advanced driver assistance systems (ADAS), the demand for simulation-based testing is increasing. Consequently, organizations are investing more in advanced driving simulators to achieve accurate testing outcomes while maintaining cost efficiency.

Report Scope and Market Segmentation

|

Report Metric

|

Details

|

|

Forecast Period

|

2026 to 2033

|

|

Base Year

|

2025

|

|

Historic Years

|

2024 (Customizable from 2018-2023)

|

|

Quantitative Units

|

Revenue in USD Billion

|

|

Segments Covered

|

By simulation type (fixed-base simulators, motion-based simulators, VR/AR enabled simulators, and full-vehicle simulators), Vehicle type (passenger vehicles, heavy commercial vehicles, specialty vehicles, and two-wheelers), Training application (driver training & education, corporate & fleet training, research & testing, military & defense, and rehabilitation & accessibility training), End user (automotive OEMs, driving schools & training centers, government & regulatory bodies, military & defense organizations, research institutions & universities, and simulation & software service providers), Hardware components (visual display systems, motion platform systems, computing & processors, control interface systems, and sensory & environmental devices), Software component (simulation software, virtual environment tools, analytics & reporting tools, AI & machine learning modules, and connectivity & integration), Training mode (fixed scenario mode, dynamic scenario mode, and multiplayer & networked mode), Integration & connectivity (third-party system integration, real-time telemetry integration, API & SDK support), Deployment (on-premise and cloud-based), and Support & services (maintenance & upgrades, installation & commissioning, training & certification, and consulting services)

|

|

Countries Covered

|

U.S., Canada, Mexico, Germany, U.K., France, Italy, Spain, Russia, Turkey, Netherlands, Norway, Finland, Denmark, Sweden, Poland, Switzerland, Belgium, Rest of Europe, China, Japan, India, South Korea, Australia, Indonesia, Thailand, Malaysia, Singapore, Philippines, Rest of Asia-Pacific, Brazil, Argentina, rest of South America. U.A.E., Saudi Arabia, South Africa, Egypt, Israel, and the rest of Middle East and Africa

|

|

Market Players Covered

|

Moog Inc. (U.S.), Dallara (Italy), Exail (France), IPG Automotive GmbH (Germany), aiMotive (Hungary), VI‑grade GmbH (Germany), Cruden B.V. (Netherlands), Dynisma Ltd. (U.K.), Applied Intuition Inc. (U.S.), rFpro (rFpro Limited) (England), Siemens AG (Germany), Dassault Systèmes SE (France), MTS Systems Corporation (U.S.), CAE Inc. (Canada), NVIDIA Corporation (U.S.), AB Dynamics PLC (U.K.), Forum8 (Japan), Mitsubishi Precision Co., Ltd. (Japan), FAAC Incorporated (U.S.), DriveSafety (U.S.), Simtec Simulation Technology GmbH (Germany), MB Dynamics Inc. (U.S.), Sanlab Simulation (India), SimCraft (U.S.), CXC Simulations (U.S.), XPI Simulation (U.K.), Tecknotrove Simulator Systems Pvt. Ltd. (India), Zhejiang Kechi Intelligent Technology Co., Ltd. (China), Shenzhen Zhongzhi Simulation (China), Hindustan Simulators (India), DriveSimSolutions (U.S.), Teksim Technologies (India), iMVR Inc. (U.S.), and SimXperience (U.S.)

|

|

Data Points Covered in the Report

|

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand.

|

Segment Analysis

The global driving simulator market is segmented into ten notable segments based on the simulation type, vehicle type, training application, end user, hardware components, software components, training mode, integration & connectivity, deployment, and support & services.

- On the basis of simulation type, the global driving simulator market is segmented into fixed-base simulators, motion-based simulators, VR/AR-enabled simulators, and full-vehicle simulators.

In 2025, the fixed-base simulators is expected to dominate the global driving simulator market

The fixed-base simulators segment dominated the market in 2025, with a 41.55% market share, owing to its widespread adoption by automotive OEMs, training institutions, and research centers; the increasing demand for cost-effective, high-fidelity simulation solutions; and the growing emphasis on driver safety, skill development, and vehicle system validation.

- On the basis of vehicle type, the global driving simulator market is segmented into passenger vehicles, heavy commercial vehicles, specialty vehicles, and two-wheelers

In 2025, the passenger vehicles segment is expected to dominate the global driving simulator market

The passenger vehicles segment dominated the market with in 2025, with a 41.71% market share due to its extensive use in automotive R&D, driver training, and autonomous/ADAS vehicle testing, increasing adoption of simulators by automotive OEMs and training institutes, and strong commercial investment from leading vehicle manufacturers and technology providers. Additionally, the ability of simulators to deliver cost-effective, safe, and high-fidelity testing environments for diverse vehicle types continues to drive widespread adoption across the global market.

- On the basis of training application, the global driving simulator market is segmented into driver training & education, corporate & fleet training, research & testing, military & defense, and rehabilitation & accessibility training. The driver training & education segment dominated the market in 2025 with a share of 36.06% due to its widespread adoption by driver schools, automotive OEMs, and corporate training centers, increasing demand for safe and controlled training environments, and growing integration with advanced simulation technologies such as VR/AR, motion platforms, and AI-driven analytics.

- On the basis of end user, the global driving simulator market is segmented into automotive OEMs, driving schools & training centers, government & regulatory bodies, military & defense organizations, research institutions & universities, and simulation & software service providers. The automotive OEMs segment dominated the market in 2025, with a share of 32.54% due to its critical role in vehicle design, testing, and validation of advanced driver-assistance systems (ADAS) and autonomous vehicles

- On the basis of hardware components, the global driving simulator market is segmented into visual display systems, motion platform systems, computing & processors, control interface systems, and sensory & environmental devices. The visual display systems segment dominated the market in 2025, accounting for 29.98% of the market, owing to its critical role in providing realistic, immersive driving environments for training, testing, and vehicle validation. High adoption is driven by the increasing need for high-fidelity visual feedback, integration with VR/AR platforms, and enhanced simulation accuracy

- On the basis of software components, the global driving simulator market is segmented into simulation software, virtual environment tools, analytics & reporting tools, AI & machine learning modules, and connectivity & integration. The simulation software segment dominated the market in 2025, with a share of 34.67% due to its widespread use in driver training, vehicle system testing, autonomous vehicle validation, and research applications

- On the basis of training mode, the global driving simulator market is segmented into fixed scenario mode, dynamic scenario mode, and multiplayer & networked mode. The fixed scenario mode segment dominated the market with a share of 49.54% due to its widespread adoption in driver training programs, automotive R&D, and fleet safety training.

- On the basis of integration & connectivity, the global driving simulator market is segmented into third-party system integration, real-time telemetry integration, and API & SDK support. The third-party system integration segment dominated the market in 2025, with a share of 38.42% due to its critical role in enabling seamless integration of simulators with vehicle systems, ADAS sensors, telematics, and ECU modules, which is essential for automotive OEMs, fleet operators, and research institutions.

- On the basis of deployment, the global driving simulator market is segmented into on-premise and cloud-based. The on-premise segment dominated the market in 2025 with a share of 59.68% due to its preference among automotive OEMs, driver training centers, corporate fleets, and research institutions that require high control, data security, and low-latency performance for simulation operations.

- On the basis of support & services, the global driving simulator market is segmented into maintenance & upgrades, installation & commissioning, training & certification, and consulting services. The maintenance & upgrades segment dominated the market in 2025, with a share of 34.21% due to its critical role in ensuring continuous, high-performance operation of driving simulators across automotive OEMs, training institutes, corporate fleets, and research organizations

Major Players

Data Bridge Market Research analyzes some of the major market players operating in the market are NVIDIA Corporation (U.S.), AB Dynamics PLC (U,K.), Forum8 (Japan), Mitsubishi Precision Co., Ltd. (Japan), FAAC Incorporated (U.S.), DriveSafety (U.S.), and Simtec Simulation Technology GmbH (Germany).

Market Developments

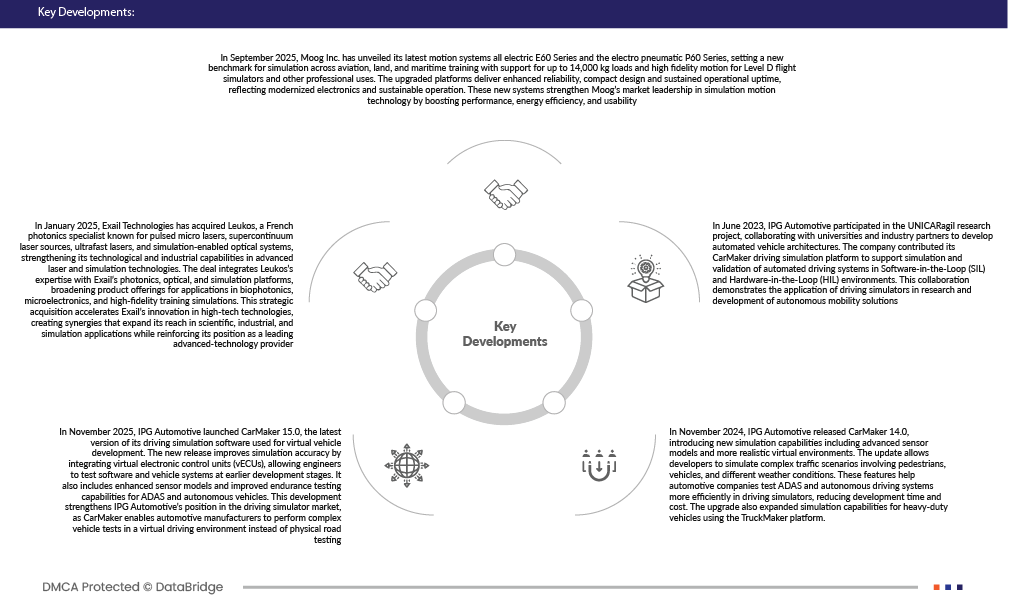

- In September 2025, Moog Inc. has unveiled its latest motion systems all electric E60 Series and the electro pneumatic P60 Series, setting a new benchmark for simulation across aviation, land, and maritime training with support for up to 14,000 kg loads and high fidelity motion for Level D flight simulators and other professional uses. The upgraded platforms deliver enhanced reliability, compact design and sustained operational uptime, reflecting modernized electronics and sustainable operation. These new systems strengthen Moog’s market leadership in simulation motion technology by boosting performance, energy efficiency, and usability

- In January 2025, Exail Technologies has acquired Leukos, a French photonics specialist known for pulsed micro lasers, supercontinuum laser sources, ultrafast lasers, and simulation-enabled optical systems, strengthening its technological and industrial capabilities in advanced laser and simulation technologies. The deal integrates Leukos’s expertise with Exail’s photonics, optical, and simulation platforms, broadening product offerings for applications in biophotonics, microelectronics, and high-fidelity training simulations. This strategic acquisition accelerates Exail’s innovation in high-tech technologies, creating synergies that expand its reach in scientific, industrial, and simulation applications while reinforcing its position as a leading advanced-technology provider

- In November 2025, IPG Automotive launched CarMaker 15.0, the latest version of its driving simulation software used for virtual vehicle development. The new release improves simulation accuracy by integrating virtual electronic control units (vECUs), allowing engineers to test software and vehicle systems at earlier development stages. It also includes enhanced sensor models and improved endurance testing capabilities for ADAS and autonomous vehicles. This development strengthens IPG Automotive’s position in the driving simulator market, as CarMaker enables automotive manufacturers to perform complex vehicle tests in a virtual driving environment instead of physical road testing.

- In November 2024, IPG Automotive released CarMaker 14.0, introducing new simulation capabilities including advanced sensor models and more realistic virtual environments. The update allows developers to simulate complex traffic scenarios involving pedestrians, vehicles, and different weather conditions. These features help automotive companies test ADAS and autonomous driving systems more efficiently in driving simulators, reducing development time and cost. The upgrade also expanded simulation capabilities for heavy-duty vehicles using the TruckMaker platform.

- In June 2023, IPG Automotive participated in the UNICARagil research project, collaborating with universities and industry partners to develop automated vehicle architectures. The company contributed its CarMaker driving simulation platform to support simulation and validation of automated driving systems in Software-in-the-Loop (SIL) and Hardware-in-the-Loop (HIL) environments. This collaboration demonstrates the application of driving simulators in research and development of autonomous mobility solutions

Regional Analysis

Geographically, the country covered in the global driving simulator market report is U.S., Canada, Mexico, Germany, U.K., France, Italy, Spain, Russia, Turkey, Netherlands, Norway, Finland, Denmark, Sweden, Poland, Switzerland, Belgium, Rest of Europe, China, Japan, India, South Korea, Australia, Indonesia, Thailand, Malaysia, Singapore, Philippines, Rest of Asia-Pacific, Brazil, Argentina, rest of South America. U.A.E., Saudi Arabia, South Africa, Egypt, Israel, and the rest of Middle East and Africa.

As per Data Bridge Market Research analysis:

Europe is the dominant region in the global driving simulator market

Europe emerged as the largest revenue-generating region in the driving simulators market, accounting for 33.84% share in 2025, supported by advanced infrastructure, strong government investments, and high adoption of innovative simulation technologies.

Asia Pacific is estimated to be the fastest-growing region in the global driving simulator market

Asia-Pacific is expected to be the fastest-growing region during the forecast period, driven by rising urbanization, increasing investments in training infrastructure, and growing adoption of advanced driving simulation solutions in countries such as China, India, and Japan.

For more detailed information about global driving simulator market click here – https://www.databridgemarketresearch.com/reports/global-driving-simulator-market