The increasing demand for corrosion-resistant solutions is a key driver accelerating the growth of the global non-metallic enclosure market. In industries such as chemical processing, wastewater treatment, marine, and oil & gas, equipment is frequently exposed to moisture, salts, and aggressive chemicals that cause rapid degradation of traditional metallic enclosures. Corrosion not only reduces the lifespan of enclosures but also leads to equipment failure, safety risks, and significant maintenance costs. As a result, industries are increasingly prioritizing materials that can withstand such harsh conditions while ensuring long-term operational reliability.

Non-metallic enclosures, particularly those made from fiberglass-reinforced polymers and polycarbonate, offer inherent resistance to corrosion, chemicals, and environmental stressors. These materials are immune to rust and provide superior performance in corrosive environments such as coastal areas and industrial plants. Their ability to maintain structural integrity and reduce maintenance frequency makes them a cost-effective alternative to metal enclosures, especially in applications where durability and lifecycle performance are critical.

Access Full Report @ https://www.databridgemarketresearch.com/reports/global-non-metallic-enclosure-market

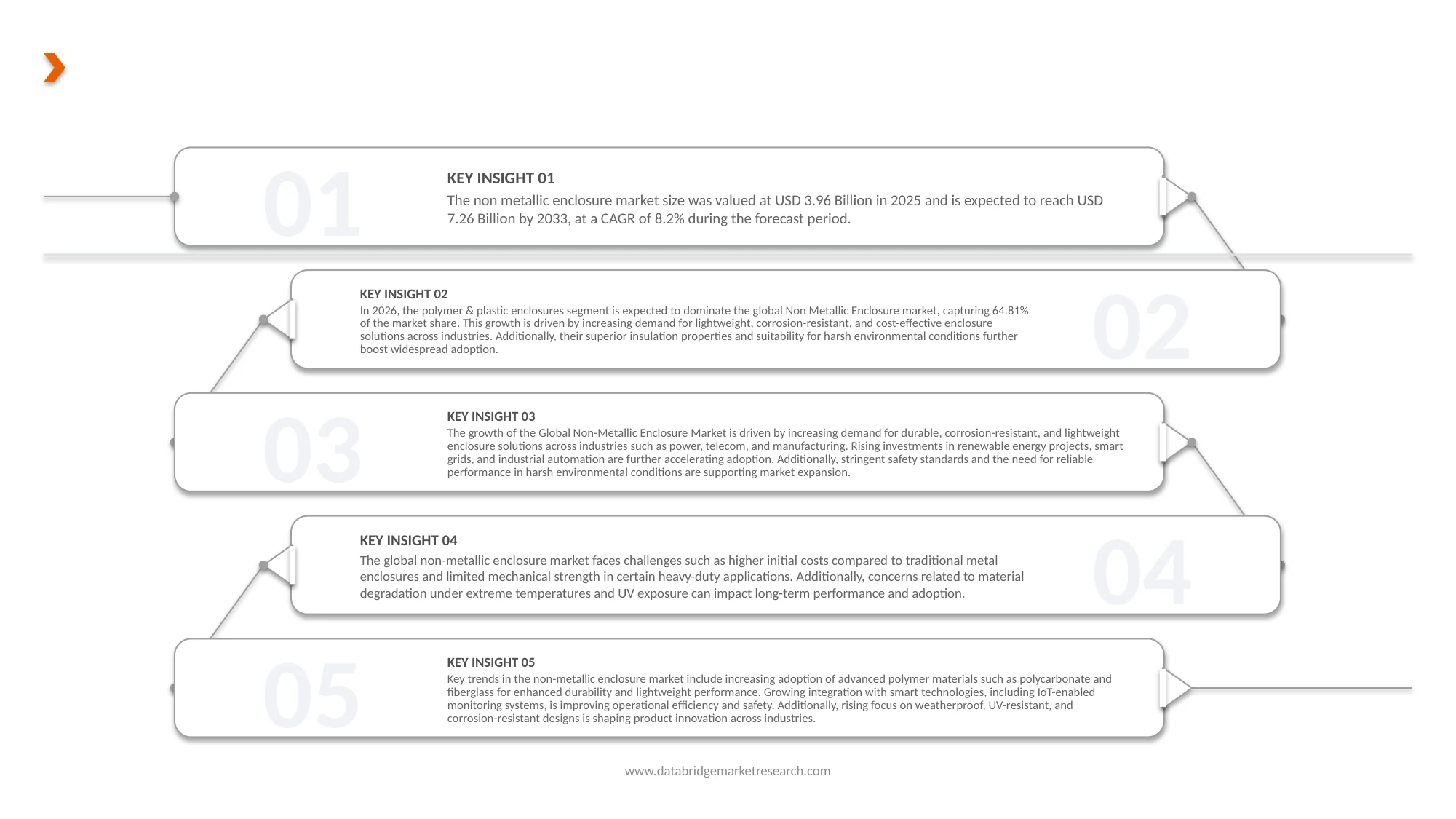

Data Bridge market research analyzes that the Global Meal Replacement Products Market is expected to reach USD 7.26 billion by 2033 from USD 3.96 billion In 2025, growing with a substantial CAGR of 8.2% in the forecast period of 2026 to 2033.

Key Findings of the Study

Expansion of Electrical, Telecommunications, and Electronics Sectors

The expansion of electrical, telecommunications, and electronics sectors is significantly driving demand for protective enclosure solutions, including non‑metallic variants. As digital transformation accelerates globally, investments in electrical grid infrastructure, telecom networks (especially 5G), data centers, and connected devices are surging. These systems require reliable protection for sensitive components like control panels, distribution nodes, power converters, and network hardware against environmental, electrical, and physical risks.

In the electrical sector, increasing electricity demand fueled by digital growth and electrification initiatives such as smart grids and data center expansion necessitates robust enclosure solutions to support complex power distribution and control systems. In telecommunications, the rapid deployment of 5G and supporting infrastructure increases the volume and diversity of network equipment installed outdoors and in challenging conditions. Non‑metallic enclosures, with benefits such as corrosion resistance, electrical insulation, and weight reduction, are well‑suited to meet these requirements and are being increasingly specified for modern infrastructure deployments. The electronics market’s proliferation spanning industrial automation, IoT, and edge computing adds further impetus to protective enclosure demand.

Report Scope and Market Segmentation

|

Report Metric

|

Details

|

|

Forecast Period

|

2026 to 2033

|

|

Base Year

|

2025

|

|

Historic Years

|

2024 (Customizable to 2018-2023)

|

|

Quantitative Units

|

Revenue in USD million

|

|

Segments Covered

|

By Product Type (Polymer & Plastic Enclosures, Composite Enclosures, Thermoplastic Elastomer Enclosures, Other Specialty Polymers), By Applications (Electrical & Electronics, Industrial Automation, Energy & Utilities, Telecommunications, Transportation, Consumer Electronics, Medical & Healthcare, Defense & Aerospace), By Form Factor (Box Enclosures, Cabinet & Rack-Mount, DIN-Rail Enclosures, Custom & Modular Enclosures, Hinged Cover Enclosures, Sealed / Gasketed Enclosures), By Material Type (Thermoplastics, Thermoset Composites, Elastomers, Others), By Distribution Channel (OEM Direct Sales, Distributors / Value-Added Resellers, System Integrators & Panel Builders, Online Industrial Marketplaces, Retail)

|

|

Countries Covered

|

U.S., Canada, Mexico, Germany, France, Italy, U.K., Russia, Spain, Turkey, Sweden, Netherlands, Switzerland, Finland, Norway, Belgium, Denmark, Rest of Europe, China, India, Japan, South Korea, Taiwan, Australia, Thailand, Indonesia, Malaysia, Philippines, Singapore, Hong Kong, New Zealand, Rest of Asia-Pacific, Brazil, Argentina, Colombia, Peru, Chile, Venezuela, Ecuador, Bolivia, Uruguay, Paraguay, Rest of South America, Saudi Arabia, South Africa, United Arab Emirates, Egypt, Israel, Kuwait, Oman, Qatar, Bahrain, Rest of Middle East and Africa

|

|

Market Players Covered

|

|

|

Data Points Covered in the Report

|

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand.

|

Segment Analysis

the global non-metallic enclosure market is segmented into five notable segments based on product type, application, form factor, material type, and distribution channel.

- on the basis of product type, the global non-metallic enclosure market is segmented into polymer & plastic enclosures, composite enclosures, thermoplastic elastomer enclosures, and other specialty polymers.

in 2026, the polymer & plastic enclosures segment is anticipated to dominate the market

in 2026, the polymer & plastic enclosures segment is expected to dominate the market with share of 64.81% share due to their widespread usage across electrical, industrial, and telecommunications applications. these enclosures offer advantages such as lightweight structure, corrosion resistance, cost-effectiveness, and ease of manufacturing, making them highly suitable for indoor and outdoor installations. composite enclosures, particularly fiberglass-reinforced materials, are gaining traction in harsh industrial and utility environments due to their superior strength, chemical resistance, and durability.

- on the basis of application, the global non-metallic enclosure market is segmented into electrical & electronics, industrial automation, energy & utilities, telecommunications, transportation, consumer electronics, medical & healthcare, and defense & aerospace.

in 2026, the electrical & electronics is expected to dominate the market

in 2026, the electrical & electronics segment is anticipated to dominate the market with share of 29.42% due to increasing demand for protective enclosures in power distribution systems, control panels, and circuit protection applications. industrial automation and energy & utilities are also key contributors, driven by increasing deployment of control systems, renewable energy infrastructure, and smart grid technologies. telecommunications is witnessing strong growth due to rising demand for outdoor network enclosures and fiber infrastructure protection.

- on the basis of form factor, the global non-metallic enclosure market is segmented into box enclosures, cabinet & rack-mount, din-rail enclosures, custom & modular enclosures, hinged cover enclosures, and sealed / gasketed enclosures.

in 2026, box enclosures segment is expected to dominate the market

in 2026, box enclosures are expected to dominate the market with share of 40.64% due to their extensive use in small-scale electrical installations, junction boxes, and instrumentation protection. sealed / gasketed enclosures are witnessing increasing demand in outdoor and harsh environments where protection against dust, moisture, and contaminants is critical. custom & modular enclosures are also gaining popularity due to growing demand for application-specific designs.

- on the basis of material type, the global non-metallic enclosure market is segmented into thermoplastics, thermoset composites, elastomers, and others.

in 2026, the thermoplastics segment is expected to dominate the market

in 2026, the thermoplastics segment is expected to dominate the market with share of 67.44% owing to their versatility, cost efficiency, and ease of processing. materials such as polycarbonate and abs are widely used due to their impact resistance, UV stability, and electrical insulation properties. thermoset composites, including fiberglass-reinforced polyester, are preferred in demanding industrial and outdoor environments due to their superior mechanical strength and resistance to heat and chemicals.

- on the basis of distribution channel, the global non-metallic enclosure market is segmented into OEM direct sales, distributors / value-added resellers, system integrators & panel builders, online industrial marketplaces, and retail.

in 2026, OEM direct sales segment is expected to dominate the market

in 2026, OEM direct sales are expected to dominate the market with share of 32.20% as manufacturers directly supply enclosures to industrial OEMs, utilities, and infrastructure projects, ensuring customization, bulk procurement, and long-term contracts. distributors and value-added resellers play a critical role in expanding market reach, particularly for small and medium enterprises. meanwhile, online industrial marketplaces are emerging as a growing channel due to increasing digital procurement and ease of product comparison.

Major Players

Schneider Electric (France), ABB Ltd. (Switzerland), Eaton Corporation (Ireland), Rittal GmbH & Co. KG (Germany), Legrand SA (France)

Regional Analysis

Geographically, the country covered in the Global Non-Metallic Enclosure market report is U.S., Canada, Mexico, Germany, U.K., France, Italy, Spain, Russia, Turkey, Netherlands, Norway, Finland, Denmark, Sweden, Poland, Switzerland, Belgium, Rest of Europe, China, Japan, India, South Korea, Australia, Indonesia, Thailand, Malaysia, Singapore, Philippines, Rest of Asia-Pacific, Brazil, Argentina, rest of South America. U.A.E., Saudi.

As per Data Bridge Market Research analysis:

North America is the dominant region in the global Non-Metallic Enclosure market

North America leads the global non-metallic enclosure market due to the strong presence of advanced electrical infrastructure, increasing industrial automation, and rising investments in renewable energy and smart grid projects across the region. The growing adoption of non-metallic enclosures in sectors such as power distribution, telecommunications, oil & gas, water treatment, and manufacturing is significantly supporting market growth. In addition, strict safety regulations and standards related to electrical protection and corrosion resistance are encouraging industries to prefer durable non-metallic enclosures over traditional metallic alternatives. The region also benefits from rapid technological advancements, high demand for lightweight and weather-resistant enclosure systems, and the presence of major market players continuously investing in product innovation. Furthermore, expanding data centers, increasing construction activities, and rising deployment of EV charging infrastructure are contributing to the strong demand for non-metallic enclosures across the United States and Canada.

Asia-Pacific is estimated to be the fastest-growing region in the global Non-Metallic Enclosure market

Asia-Pacific is expected to be the fastest-growing region in the global non-metallic enclosure market from 2026 to 2033, driven by rapid industrialization, urban infrastructure development, and expanding power distribution networks across countries such as China, India, Japan, and South Korea. Rising investments in renewable energy projects, smart manufacturing facilities, telecommunications infrastructure, and electric vehicle charging systems are significantly increasing demand for durable and corrosion-resistant enclosure solutions.

Market Developments

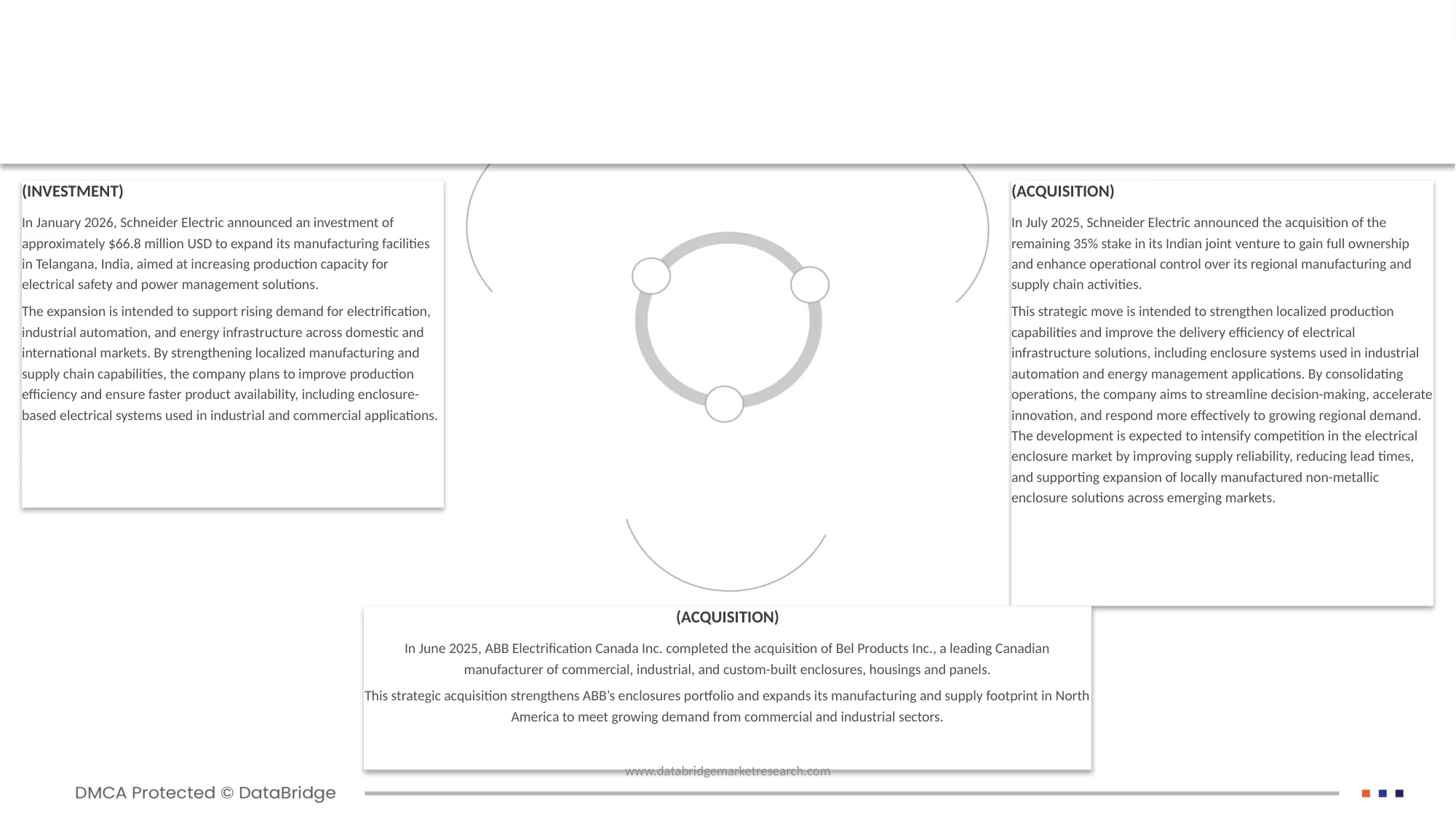

- In January 2026, Schneider Electric announced an investment of approximately $66.8 million USD to expand its manufacturing facilities in Telangana, India, aimed at increasing production capacity for electrical safety and power management solutions. The expansion is intended to support rising demand for electrification, industrial automation, and energy infrastructure across domestic and international markets. By strengthening localized manufacturing and supply chain capabilities, the company plans to improve production efficiency and ensure faster product availability, including enclosure-based electrical systems used in industrial and commercial applications.

- In June 2025, ABB Electrification Canada Inc. completed the acquisition of Bel Products Inc., a leading Canadian manufacturer of commercial, industrial, and custom‑built enclosures, housings and panels. This strategic acquisition strengthens ABB’s enclosures portfolio and expands its manufacturing and supply footprint in North America to meet growing demand from commercial and industrial sectors.

- In May 2025, Lenze and Rittal signed a technology partnership to work together to shape the future of power distribution and drive technology. The combination of RiLineX, as the new standard platform for busbar systems, and Lenze’s market-leading compact inverters provides the basis.

- In November 2025, Eaton announced an agreement to acquire the Boyd Thermal business to strengthen its engineered solutions portfolio supporting data centers and industrial infrastructure. The acquisition is aimed at enhancing Eaton’s capabilities in thermal management technologies, which play an important role in maintaining temperature control and operational efficiency in electrical systems. By integrating Boyd’s advanced cooling and thermal solutions, Eaton expands its ability to deliver more efficient and reliable power distribution systems, including enclosure-based electrical applications. The acquisition strengthens Eaton’s integrated electrical solutions portfolio, improves enclosure system performance through enhanced thermal management, and increases competitiveness in rapidly growing data center and industrial electrification markets.

- In November 2025, Legrand continued its targeted acquisition strategy to expand its portfolio in high‑growth segments tied to the energy and digital transition. The Group completed seven acquisitions during the year including companies in datacenter solutions and building automation adding approximately €500 million in annualized sales and strengthening its position in complementary infrastructure technologies.

As per Data Bridge Market Research analysis:

For more detailed information about the global non-metallic enclosure market report, click here – https://www.databridgemarketresearch.com/reports/global-non-metallic-enclosure-market