يتميز سوق أجهزة علاج الصدمات بميزات أساسية، مثل مجموعة متنوعة من الأدوات المتخصصة لتثبيت العظام، وإغلاق الجروح ، وإصلاح الأنسجة. ومن بين هذه الأجهزة، تُعدّ أجهزة علاج الصدمات العظمية القطاع الرئيسي، بما في ذلك غرسات تثبيت الكسور وحلول إعادة بناء المفاصل. تُعد هذه الأجهزة أساسية في علاج إصابات العظام وأمراض العظام. ويعود نمو السوق إلى شيخوخة السكان، وارتفاع حالات الإصابات الناجمة عن الحوادث، والتقدم التكنولوجي في مواد الزرع، مما عزز مكانة أجهزة علاج الصدمات العظمية كقطاع سوقي بارز.

يمكنك الوصول إلى التقرير الكامل على https://www.databridgemarketresearch.com/press-release/global-taxane-market

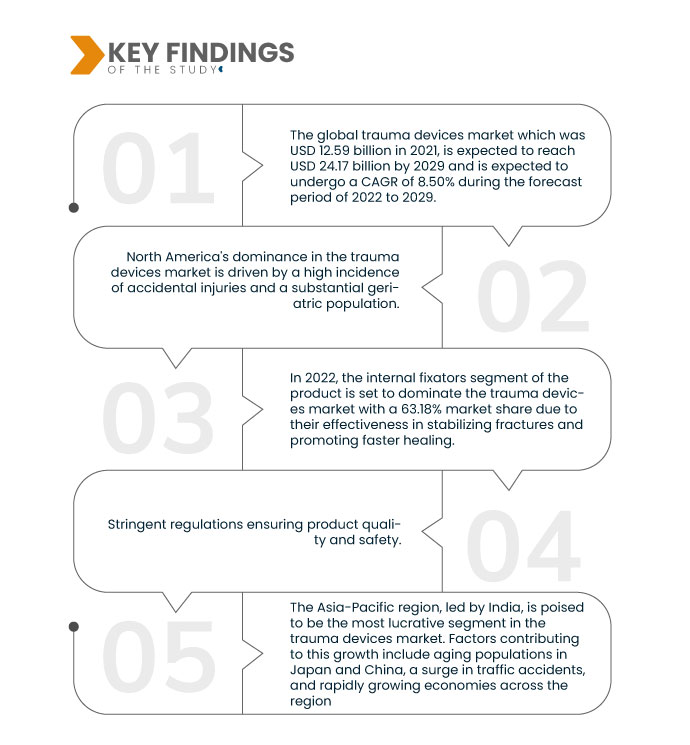

تُحلل شركة داتا بريدج لأبحاث السوق أن سوق أجهزة الصدمات العالمي ، الذي بلغ 12.59 مليار دولار أمريكي في عام 2021، من المتوقع أن يصل إلى 24.17 مليار دولار أمريكي بحلول عام 2029، وأن يشهد معدل نمو سنوي مركب بنسبة 8.50% خلال الفترة المتوقعة من 2022 إلى 2029. ويُعدّ تزايد عدد كبار السن، المعرضين للكسور ومشاكل العظام، عاملاً رئيسياً في نمو سوق أجهزة الصدمات. ومع تزايد إصابات العظام ومشاكل المفاصل المرتبطة بالعمر، يتزايد الطلب على أجهزة الصدمات العظمية، بما في ذلك الغرسات واستبدال المفاصل، لتلبية الاحتياجات الصحية الفريدة لهذه الفئة السكانية.

النتائج الرئيسية للدراسة

ومن المتوقع أن يؤدي الوعي والتثقيف إلى دفع معدل نمو السوق

يلعب الوعي المتزايد برعاية الإصابات والأجهزة المتاحة دورًا محوريًا في سوق أجهزة علاج الإصابات. يتزايد وعي المرضى ومقدمي الرعاية الصحية بخيارات إدارة الإصابات المتقدمة، مما يؤدي إلى علاجات أسرع وأكثر فعالية. يشجع هذا الوعي المتزايد على اعتماد أجهزة علاج إصابات مبتكرة، مما يؤدي إلى تحسين نتائج المرضى وخفض معدلات الوفيات. بالإضافة إلى ذلك، يعزز هذا الوعي التعاون بين الكوادر الطبية ومصنّعي الأجهزة، مما يدفع عجلة التقدم المستمر في تقنيات رعاية الإصابات.

نطاق التقرير وتقسيم السوق

مقياس التقرير

|

تفاصيل

|

فترة التنبؤ

|

من 2022 إلى 2029

|

سنة الأساس

|

2021

|

السنوات التاريخية

|

2020 (قابلة للتخصيص حتى 2014-2019)

|

الوحدات الكمية

|

الإيرادات بالمليارات من الدولارات الأمريكية، والحجم بالوحدات، والتسعير بالدولار الأمريكي

|

القطاعات المغطاة

|

المنتج (أجهزة التثبيت الداخلية، أجهزة التثبيت الخارجية وغيرها)، موقع الجراحة (الأطراف السفلية والعلوية)، نوع الأنسجة (الأنسجة الصلبة والأنسجة الرخوة)، نوع المادة (غير قابلة للامتصاص وقابلة للامتصاص الحيوي)، عمر المريض (بالغون وأطفال)، المستخدم النهائي (المستشفيات ومراكز الصدمات ومراكز الجراحة الخارجية وغيرها)، قناة التوزيع (العطاء المباشر ومبيعات التجزئة)

|

الدول المغطاة

|

الولايات المتحدة وكندا والمكسيك في أمريكا الشمالية، ألمانيا، فرنسا، المملكة المتحدة، هولندا، سويسرا، بلجيكا، روسيا، إيطاليا، إسبانيا، تركيا، بقية أوروبا في أوروبا، الصين، اليابان، الهند، كوريا الجنوبية، سنغافورة، ماليزيا، أستراليا، تايلاند، إندونيسيا، الفلبين، بقية دول آسيا والمحيط الهادئ (APAC) في منطقة آسيا والمحيط الهادئ (APAC)، المملكة العربية السعودية، الإمارات العربية المتحدة، جنوب أفريقيا، مصر، إسرائيل، بقية دول الشرق الأوسط وأفريقيا (MEA) كجزء من الشرق الأوسط وأفريقيا (MEA)، البرازيل والأرجنتين وبقية دول أمريكا الجنوبية كجزء من أمريكا الجنوبية.

|

الجهات الفاعلة في السوق المغطاة

|

شركة شنغهاي كينيتيك الطبية المحدودة (الصين)، مجموعة ويغاو (الصين)، شركة مايكروبورت العلمية (الصين)، شركة أورثوفيكس يو إس إل إل سي (الولايات المتحدة)، شركة كونميد (الولايات المتحدة)، مجموعة رايت الطبية إن في (الولايات المتحدة)، شركة نوفاسيف (الولايات المتحدة)، مجموعة كورين (الولايات المتحدة)، إينوفيس (الولايات المتحدة)، أوستيوميد (الولايات المتحدة)، إنفيبيو المحدودة (الولايات المتحدة)، جي بي سي ميديكال (الولايات المتحدة)، ميدترونيك (أيرلندا)، سميث+نيفيو (الولايات المتحدة)، إنتيغرا لايف ساينسز (الولايات المتحدة)، بي براون إس إي (ألمانيا)، سترايكر (الولايات المتحدة)

|

نقاط البيانات التي يغطيها التقرير

|

بالإضافة إلى الرؤى حول سيناريوهات السوق مثل القيمة السوقية ومعدل النمو والتجزئة والتغطية الجغرافية واللاعبين الرئيسيين، فإن تقارير السوق التي تم تنظيمها بواسطة Data Bridge Market Research تتضمن أيضًا تحليلًا متعمقًا من الخبراء وعلم الأوبئة للمرضى وتحليل خطوط الأنابيب وتحليل التسعير والإطار التنظيمي.

|

تحليل القطاعات:

يتم تقسيم سوق أجهزة الصدمات العالمية على أساس المنتج وموقع الجراحة ونوع الأنسجة ونوع المادة وعمر المريض والمستخدم النهائي.

- بناءً على المنتج، يُقسّم سوق أجهزة الصدمات العالمية إلى أجهزة تثبيت داخلية، وأجهزة تثبيت خارجية، وغيرها. في عام 2022، من المتوقع أن تهيمن أجهزة التثبيت الداخلية على سوق أجهزة الصدمات بحصة سوقية تبلغ 63.18%، نظرًا لفعاليتها في تثبيت الكسور وتسريع عملية الشفاء.

في عام 2022، من المتوقع أن تهيمن شريحة المثبتات الداخلية لقطاع المنتجات على سوق أجهزة الصدمات

في عام ٢٠٢٢، من المتوقع أن تهيمن المثبتات الداخلية على سوق أجهزة علاج الإصابات بحصة سوقية تبلغ ٦٣.١٨٪، وذلك بفضل فعاليتها في تثبيت الكسور وتسريع عملية الشفاء. توفر هذه الأجهزة، بما في ذلك الصفائح والبراغي والمسامير، دعمًا داخليًا للعظام المكسورة، مما يُخفف الألم ويُعزز القدرة على الحركة. ومع تزايد الطلب على حلول علاج الإصابات العظمية، تظل المثبتات الداخلية عنصرًا أساسيًا في إدارة الإصابات الرضحية، مما يعزز هيمنتها على السوق.

- بناءً على موقع الجراحة، يُقسّم سوق أجهزة الصدمات العالمي إلى قسمين: قسم للأطراف السفلية وقسم للأطراف العلوية. في عام 2022، من المتوقع أن يهيمن قطاع الأطراف السفلية على سوق أجهزة الصدمات بحصة سوقية تبلغ 78.60%، نظرًا لأهميته في علاج مجموعة واسعة من إصابات الأطراف السفلية، بما في ذلك الكسور وإصابات المفاصل.

في عام 2022، من المتوقع أن يهيمن قطاع الأطراف السفلية من قطاع موقع الجراحة على سوق أجهزة الصدمات

في عام ٢٠٢٢، من المتوقع أن يهيمن قطاع الأطراف السفلية على سوق أجهزة الصدمات بحصة سوقية تبلغ ٧٨.٦٠٪، نظرًا لأهميته في علاج مجموعة واسعة من إصابات الأطراف السفلية، بما في ذلك الكسور وإصابات المفاصل. ونظرًا لأهمية الحركة، لا يزال الطلب على أجهزة مثل غرسات الورك والركبة، والمسامير النخاعية، وأنظمة تثبيت الكاحل مرتفعًا، مما يعزز مكانة هذا القطاع.

- بناءً على نوع الأنسجة، يُقسّم سوق أجهزة الصدمات العالمي إلى أنسجة صلبة وأنسجة رخوة. في عام ٢٠٢٢، تُعزى هيمنة قطاع الأنسجة الصلبة في سوق أجهزة الصدمات، بحصة سوقية بلغت ٨٥.٦٥٪، إلى تركيزه على معالجة إصابات وكسور العظام الشائعة والتي تتطلب أجهزة متخصصة لعلاجها والتعافي منها بفعالية.

- بناءً على نوع المادة، يُقسّم سوق أجهزة الصدمات العالمية إلى أجهزة غير قابلة للامتصاص وأجهزة قابلة للامتصاص بيولوجيًا. في عام 2022، من المتوقع أن يتصدر قطاع الأجهزة غير القابلة للامتصاص سوق أجهزة الصدمات بحصة سوقية تبلغ 68.59% بفضل متانته وثباته في علاج الكسور والإصابات، مما يجعله الخيار الأمثل للدعم والتثبيت طويل الأمد.

- بناءً على عمر المريض، يُقسّم سوق أجهزة الصدمات العالمية إلى قسمين: للبالغين والأطفال. في عام 2022، من المتوقع أن يهيمن قطاع البالغين على سوق أجهزة الصدمات بحصة سوقية تبلغ 77.26%، نظرًا لأن غالبية الإصابات والكسور تحدث لدى البالغين، مما يستلزم زيادة الطلب على أجهزة الصدمات المصممة خصيصًا لاحتياجاتهم وخصائصهم الديموغرافية.

- بناءً على المستخدم النهائي، يُقسّم سوق أجهزة الصدمات العالمي إلى مستشفيات، ومراكز صدمات، ومراكز جراحية متنقلة، وغيرها. في عام 2022، من المتوقع أن تُهيمن المستشفيات على سوق أجهزة الصدمات بحصة سوقية تبلغ 51.22%، حيث تُعدّ مراكز علاج رئيسية للحالات المتعلقة بالصدمات، وتتطلب مجموعة واسعة من الأجهزة المتخصصة للعمليات الجراحية، والكسور، وإدارة الإصابات، مما يُحفّز الطلب.

- بناءً على قنوات التوزيع، يُقسّم سوق أجهزة الصدمات العالمي إلى مناقصة مباشرة ومبيعات بالتجزئة. في عام 2022، من المرجح أن يتصدر قطاع المناقصة المباشرة سوق أجهزة الصدمات بحصة سوقية تبلغ 86.99%، إذ يتضمن الشراء المباشر من الشركات المصنعة، مما يُتيح توريدًا وتخصيصًا فعالين من حيث التكلفة، مما يجذب مؤسسات الرعاية الصحية التي تبحث عن منتجات عالية الجودة ومزايا سعرية.

اللاعبون الرئيسيون

تعترف شركة Data Bridge Market Research بالشركات التالية باعتبارها لاعبين عالميين في سوق أجهزة الصدمات في سوق أجهزة الصدمات العالمية وهي Shanghai Kinetic Medical Co. Ltd (الصين)، ومجموعة Weigao (الصين)، وشركة MicroPort Scientific Corporation (الصين)، وOrthofix US LLC (الولايات المتحدة)، وشركة CONMED Corporation (الولايات المتحدة)، ومجموعة Wright Medical Group NV (الولايات المتحدة)، وNuVasive، Inc (الولايات المتحدة).

تطورات السوق

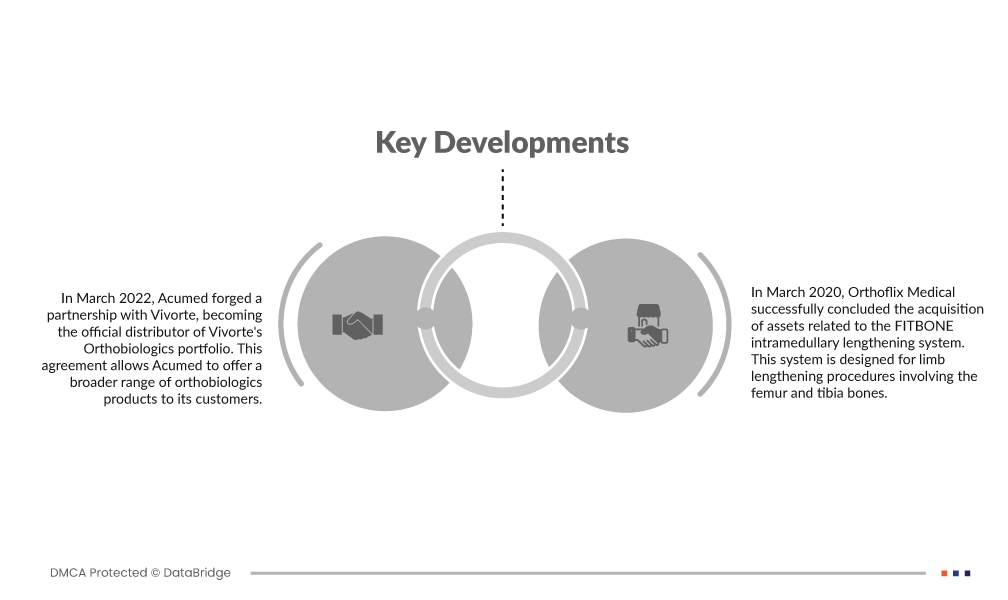

- في مارس 2022، أبرمت أكوميد شراكة مع فيفورت، لتصبح الموزع الرسمي لمجموعة منتجاتها من المنتجات الحيوية التقويمية. تتيح هذه الاتفاقية لأكوميد تقديم مجموعة أوسع من منتجاتها الحيوية التقويمية لعملائها. تلعب هذه المنتجات دورًا محوريًا في الطب التجديدي، حيث تعزز عمليات الشفاء الطبيعية. من خلال توزيع منتجات فيفورت، تهدف أكوميد إلى تعزيز خدماتها في مجال رعاية العظام والإصابات، مما يعود بالنفع على المرضى في نهاية المطاف من خلال توفير حلول متطورة لإصلاح العظام والأنسجة.

- في مارس 2020، استحوذت شركة أورثوفليكس ميديكال بنجاح على أصول تتعلق بنظام FITBONE لإطالة النخاع. صُمم هذا النظام لإجراءات إطالة الأطراف التي تشمل عظمي الفخذ والساق. عزز هذا الاستحواذ محفظة أورثوفليكس ميديكال من حلول تقويم العظام، لا سيما في مجال إطالة الأطراف، ومكّن الشركة من تقديم خدمة أفضل للمرضى والعاملين في مجال الرعاية الصحية الذين يحتاجون إلى تقنيات متقدمة لتصحيح اختلافات طول الأطراف والحالات المرتبطة بها.

التحليل الإقليمي

جغرافيًا، البلدان التي يغطيها تقرير سوق أجهزة الصدمات العالمية هي الولايات المتحدة وكندا والمكسيك في أمريكا الشمالية وألمانيا وفرنسا والمملكة المتحدة وهولندا وسويسرا وبلجيكا وروسيا وإيطاليا وإسبانيا وتركيا وبقية أوروبا في أوروبا والصين واليابان والهند وكوريا الجنوبية وسنغافورة وماليزيا وأستراليا وتايلاند وإندونيسيا والفلبين وبقية دول آسيا والمحيط الهادئ (APAC) في منطقة آسيا والمحيط الهادئ (APAC) والمملكة العربية السعودية والإمارات العربية المتحدة وجنوب إفريقيا ومصر وإسرائيل وبقية دول الشرق الأوسط وأفريقيا (MEA) كجزء من الشرق الأوسط وأفريقيا (MEA) والبرازيل والأرجنتين وبقية دول أمريكا الجنوبية كجزء من أمريكا الجنوبية.

وفقًا لتحليل Data Bridge Market Research:

أمريكا الشمالية هي المنطقة المهيمنة في سوق أجهزة الصدمات العالمية خلال الفترة المتوقعة 2022 - 2029

تُعزى هيمنة أمريكا الشمالية على سوق أجهزة علاج الصدمات إلى ارتفاع معدل الإصابات العرضية ووجود عدد كبير من كبار السن. وتستفيد المنطقة من مستشفيات متخصصة في علاج الصدمات مجهزة للتعامل مع حالات الطوارئ، مما يخلق سوقًا واضح المعالم لأجهزة علاج الصدمات. ويشهد الطلب على المعدات والأجهزة الطبية المتطورة في مجال رعاية الصدمات ارتفاعًا مستمرًا، مما يضمن حضورًا قويًا في السوق وفرص نمو للشركات المتخصصة في الأجهزة والحلول الطبية المتعلقة بالصدمات.

من المتوقع أن تهيمن منطقة آسيا والمحيط الهادئ على سوق أجهزة الصدمات العالمية في الفترة المتوقعة 2022 - 2029

من المتوقع أن تصبح منطقة آسيا والمحيط الهادئ، بقيادة الهند، أكثر القطاعات ربحية في سوق أجهزة علاج الصدمات. ومن العوامل المساهمة في هذا النمو شيخوخة السكان في اليابان والصين، وارتفاع حوادث المرور، والنمو الاقتصادي السريع في جميع أنحاء المنطقة. إضافةً إلى ذلك، يُسهم نمو السياحة العلاجية لإجراءات مثل جراحات السمنة والجراحات طفيفة التوغل في زيادة الطلب على الدبابيس الجراحية، مما يُعزز توسع السوق في منطقة آسيا والمحيط الهادئ.

لمزيد من المعلومات التفصيلية حول تقرير سوق أجهزة الصدمات العالمية، انقر هنا - https://www.databridgemarketresearch.com/reports/global-trauma-devices-market