Asia Pacific Bladder Cancer Diagnostics Market

Market Size in USD Million

USD

360.00 Million

USD

646.84 Million

2024

2032

USD

360.00 Million

USD

646.84 Million

2024

2032

| 2025 - 2032 | |

| USD 360.00 Million | |

| USD 646.84 Million | |

| % | |

|

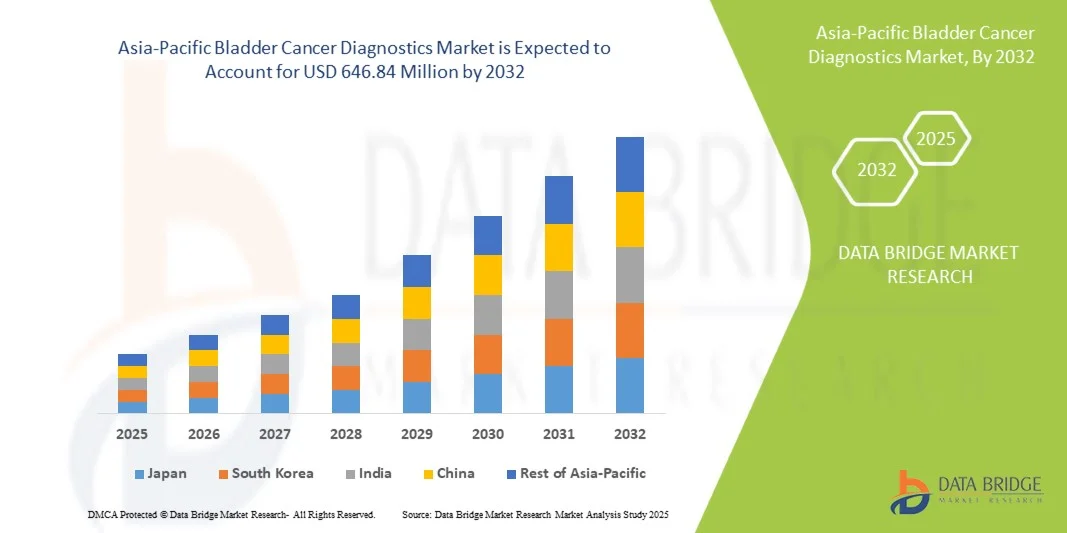

Asia-Pacific Bladder Cancer Diagnostics Market Size

- The Asia-Pacific bladder cancer diagnostics market size was valued at USD 360.00 million in 2024 and is expected to reach USD 646.84 million by 2032, at a CAGR of 7.6% during the forecast period

- The market growth is largely fueled by the increasing incidence of bladder cancer in the region, advancements in diagnostic technologies, and a heightened focus on early detection and personalized treatment, leading to improved patient outcomes in both clinical and research settings

- Furthermore, countries such as Japan and China, with their sophisticated healthcare infrastructure and expanding healthcare access, are driving the adoption of advanced diagnostic solutions, establishing bladder cancer diagnostics as a critical component of regional healthcare strategies. These converging factors are accelerating the uptake of diagnostic tools, thereby significantly boosting the industry's growth

Asia-Pacific Bladder Cancer Diagnostics Market Analysis

- Bladder cancer diagnostics, encompassing tests such as cystoscopy, urine lab tests, biopsy, and imaging tests, are becoming essential tools in the early detection and management of bladder cancer in both clinical and research settings due to their ability to improve diagnostic accuracy, enable personalized treatment, and support ongoing patient monitoring

- The rising demand for bladder cancer diagnostics is primarily driven by increasing bladder cancer prevalence in the Asia-Pacific region, growing awareness of early detection benefits, and technological advancements in non-invasive and molecular diagnostic tools

- Japan dominated the Asia-Pacific bladder cancer diagnostics market with the largest revenue share of 29.9% in 2024, supported by sophisticated healthcare infrastructure, increasing healthcare expenditure, and the presence of key diagnostic companies focusing on high-precision technologies

- India is expected to be the fastest growing market during the forecast period due to rising healthcare awareness, improving diagnostic facilities, and increasing government initiatives for cancer screening programs

- Cystoscopy segment dominated the Asia-Pacific bladder cancer diagnostics market with a market share of 42.6% in 2024, driven by its high diagnostic accuracy, widespread clinical adoption, and ability to detect early-stage bladder cancer effectively

Report Scope and Asia-Pacific Bladder Cancer Diagnostics Market Segmentation

|

Attributes |

Asia-Pacific Bladder Cancer Diagnostics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Asia-Pacific Bladder Cancer Diagnostics Market Trends

Advancements in Non-Invasive and Molecular Diagnostic Technologies

- A significant and accelerating trend in the Asia-Pacific bladder cancer diagnostics market is the growing adoption of non-invasive urine-based assays and molecular diagnostic tools, enhancing early detection and improving patient comfort

- For instance, the UroVysion FISH test allows detection of chromosomal abnormalities in urine samples, reducing reliance on invasive cystoscopy procedures

- Molecular assays enable precise identification of cancer subtypes, guide personalized treatment plans, and facilitate real-time monitoring of disease progression

- Integration of these advanced diagnostics with hospital information systems allows clinicians to track patient data efficiently and support decision-making for treatment strategies

- This trend towards more accurate, patient-friendly, and technologically advanced diagnostic solutions is reshaping clinical expectations and driving demand for early detection tools

- The demand for non-invasive and molecular diagnostic tests is growing rapidly across hospitals, diagnostic imaging centers, and independent laboratories, as healthcare providers prioritize efficiency and patient compliance

Asia-Pacific Bladder Cancer Diagnostics Market Dynamics

Driver

Rising Prevalence of Bladder Cancer and Focus on Early Detection

- The increasing incidence of bladder cancer in Asia-Pacific countries, coupled with heightened awareness of early detection benefits, is a major driver for market growth

- For instance, Japan has implemented nationwide screening programs to detect bladder cancer at early stages, promoting adoption of advanced diagnostic tests

- Early detection enables timely treatment interventions, reduces treatment costs, and improves patient survival rates. Growing healthcare expenditure, expansion of diagnostic infrastructure, and improved access to healthcare in emerging countries are increasing the uptake of diagnostic tools

- Hospitals and diagnostic centers are increasingly adopting advanced technologies such as cystoscopy, urine-based assays, and imaging tests to meet rising demand and enhance patient care

- Rising investments by private healthcare providers and diagnostic companies in the Asia-Pacific region are accelerating the availability of advanced diagnostic platforms

- Increased collaborations between research institutes and healthcare providers are driving innovation in early detection methods and personalized diagnostics. Public awareness campaigns and educational programs are contributing to higher patient participation in screening programs, further boosting market growth

Restraint/Challenge

High Cost of Advanced Diagnostics and Limited Awareness in Emerging Regions

- The relatively high cost of advanced diagnostic tests, such as molecular assays and imaging-based diagnostics, poses a significant barrier to adoption in price-sensitive markets

- For instance, sophisticated FISH-based urine assays may not be affordable for smaller clinics or patients in low-income regions, limiting market penetration

- Lack of awareness regarding early bladder cancer detection and the importance of regular screening in rural or semi-urban areas can restrict the uptake of diagnostic solutions

- Inconsistent regulatory frameworks across Asia-Pacific countries can delay product approvals and hinder the timely introduction of new diagnostic technologies. Limited availability of trained personnel to perform advanced diagnostic tests in smaller hospitals or laboratories may constrain market growth

- Challenges in integrating new diagnostic technologies into existing healthcare workflows can slow adoption and affect operational efficiency. Socioeconomic disparities and unequal healthcare access in certain regions create variability in diagnostic adoption rates

- Addressing these challenges through government subsidies, training programs, and cost-effective diagnostic solutions will be crucial for sustained market growth

Asia-Pacific Bladder Cancer Diagnostics Market Scope

The market is segmented on the basis of test type, stages, cancer type, end user, and distribution channel.

- By Test Type

On the basis of test type, the Asia-Pacific bladder cancer diagnostics market is segmented into cystoscopy, urine lab test, biopsy, imaging test, and others. The cystoscopy segment dominated the market with the largest revenue share of 42.6% in 2024, owing to its high diagnostic accuracy and widespread clinical adoption. Cystoscopy allows direct visualization of the bladder interior, enabling early detection of tumors and precise biopsy collection. Hospitals and specialized diagnostic centers prefer cystoscopy due to its reliability and established clinical protocols. The segment benefits from continuous technological improvements such as high-definition imaging and flexible scopes, which enhance patient comfort and procedure efficiency. Increasing clinician trust and patient awareness also drive the adoption of cystoscopy as a primary diagnostic tool. Moreover, reimbursement policies in countries such as Japan support its widespread use, strengthening its dominance.

The urine lab test segment is anticipated to witness the fastest growth during the forecast period, driven by the rising demand for non-invasive, cost-effective diagnostic solutions. Urine-based assays offer ease of sample collection, repeatability for monitoring, and suitability for early detection programs. Technological advancements, such as biomarker panels and molecular assays, are increasing the sensitivity and specificity of these tests. This segment is particularly gaining traction in emerging countries where access to advanced hospital facilities is limited. The non-invasive nature encourages patient compliance and supports large-scale screening initiatives.

- By Stages

On the basis of disease stage, the market is segmented into Stage I, Stage II, Stage III, and Stage IV. The Stage I segment dominated the market with a share of 36.5% in 2024, as early-stage detection is crucial for better prognosis and survival rates. Advanced diagnostics, including cystoscopy and urine lab tests, are primarily focused on identifying Stage I tumors to enable prompt treatment interventions. Clinicians prioritize Stage I detection as it allows minimally invasive treatments and reduces long-term healthcare costs. Early-stage diagnostics are increasingly integrated with hospital information systems for patient tracking and personalized care. Awareness campaigns and government-supported screening programs also contribute to Stage I testing growth. Improved accessibility and clinician confidence reinforce its dominant position.

The Stage II segment is expected to register the fastest growth during the forecast period, fueled by better diagnostic infrastructure and increasing adoption of molecular and imaging tests for mid-stage disease detection. Stage II detection enables timely intervention, often preventing progression to advanced stages. Investments in hospital laboratories and private diagnostic centers are enhancing Stage II diagnostic capabilities. The rising prevalence of bladder cancer in countries such as India and China drives the demand for Stage II-focused diagnostics.

- By Cancer Type

On the basis of cancer type, the market is segmented into transitional cell bladder cancer, squamous cell bladder cancer, and other cancer types. The transitional cell bladder cancer segment dominated the market with a share of 68.2% in 2024, as it represents the most common type of bladder cancer in the Asia-Pacific region. Diagnostics tailored for transitional cell carcinoma, including cystoscopy and urine cytology, are widely available and integrated into standard clinical protocols. High prevalence rates and established treatment pathways support the sustained adoption of these diagnostic methods. The segment benefits from ongoing technological improvements and clinician familiarity. Awareness campaigns targeting transitional cell carcinoma further reinforce its dominance.

The squamous cell bladder cancer segment is anticipated to witness the fastest growth during the forecast period due to increasing detection rates and technological advancements in molecular diagnostics. Although less common, squamous cell carcinoma requires specialized testing for early detection and effective treatment planning. Improved laboratory infrastructure and emerging biomarker research are driving growth in this segment. Countries with rising schistosomiasis prevalence also contribute to increased focus on squamous cell carcinoma diagnostics.

- By End User

On the basis of end user, the market is segmented into hospitals, diagnostic imaging centers, cancer research institutes, independent diagnostic laboratories, and associated labs. The hospital segment dominated the market with a share of 51.4% in 2024, as hospitals are equipped with advanced diagnostic tools, skilled clinicians, and integrated patient care systems. Hospitals often conduct cystoscopy, imaging, and biopsy tests in-house, providing comprehensive diagnostic solutions. Increasing healthcare expenditure and patient preference for hospital-based diagnostics contribute to this dominance. Hospitals also serve as primary referral centers, further consolidating their market share. The adoption of hospital information systems and electronic medical records facilitates better workflow management and patient tracking.

The independent diagnostic laboratories segment is expected to register the fastest growth during the forecast period, driven by expanding access to affordable and specialized diagnostic services. These labs cater to semi-urban and rural populations, offering urine-based and molecular tests with shorter turnaround times. Collaborations with hospitals and government screening programs boost their market presence. Rising health awareness and increased patient preference for convenient testing locations fuel segment growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender and retail sales. The direct tender segment dominated the market with a share of 59.6% in 2024, supported by bulk procurement by hospitals, government initiatives, and large diagnostic centers. Direct tender agreements ensure reliable supply of diagnostic kits and equipment at negotiated costs. This channel is preferred for large-scale cancer screening programs and high-volume diagnostic facilities. Institutional adoption ensures consistent demand, strengthening the segment’s market position. Favorable procurement policies and long-term contracts contribute to its dominance.

The retail sales segment is anticipated to witness the fastest growth during the forecast period, driven by increasing demand for home-based urine tests and point-of-care diagnostics. Growing awareness of self-screening and preventive healthcare encourages retail adoption. Convenience, ease of access, and rising online distribution channels are facilitating segment growth. Emerging markets with expanding middle-class populations provide additional opportunities for retail sales expansion.

Asia-Pacific Bladder Cancer Diagnostics Market Regional Analysis

- Japan dominated the Asia-Pacific bladder cancer diagnostics market with the largest revenue share of 29.9% in 2024, supported by sophisticated healthcare infrastructure, increasing healthcare expenditure, and the presence of key diagnostic companies focusing on high-precision technologies

- Patients and healthcare providers in Japan increasingly prioritize early detection, accurate diagnostics, and personalized treatment plans, fueling demand for cystoscopy, urine-based assays, biopsy, and imaging tests

- This widespread adoption is further supported by government-led cancer screening programs, strong clinician awareness, and technological innovations in diagnostic platforms, establishing Japan as the leading market for bladder cancer diagnostics in the region

The Japan Bladder Cancer Diagnostics Market Insight

The Japan bladder cancer diagnostics market is the largest in Asia-Pacific, capturing a significant revenue share of 29.9% in 2024, driven by advanced healthcare infrastructure, high healthcare expenditure, and a focus on early cancer detection. Adoption of advanced diagnostic tools such as cystoscopy, urine-based assays, biopsy, and imaging tests is widespread in hospitals and specialized diagnostic centers. Nationwide screening programs and government initiatives promote routine testing, increasing patient participation and early detection rates. Integration of diagnostics with hospital information systems and personalized treatment protocols enhances clinical efficiency and patient outcomes. Technological advancements, including high-definition imaging and molecular assays, support accurate and timely diagnosis. In addition, clinician awareness and preference for precision diagnostics further reinforce Japan’s market dominance.

India Bladder Cancer Diagnostics Market Insight

The India bladder cancer diagnostics market is the fastest growing in Asia-Pacific, fueled by rapid urbanization, increasing bladder cancer awareness, and expanding healthcare infrastructure. Rising middle-class population and growing healthcare affordability drive demand for early detection and accurate diagnostics. Hospitals, independent diagnostic laboratories, and imaging centers are increasingly adopting cystoscopy, urine-based assays, biopsy, and imaging tests to meet patient demand. Government initiatives promoting cancer screening and digital health programs are improving access to diagnostics in urban and semi-urban areas. Affordable diagnostic solutions and the presence of private healthcare providers accelerate market penetration. Furthermore, increased patient awareness and rising prevalence of bladder cancer are encouraging timely diagnosis and treatment.

China Bladder Cancer Diagnostics Market Insight

The China bladder cancer diagnostics market is witnessing strong growth, driven by increasing prevalence of bladder cancer, expanding healthcare infrastructure, and rising government initiatives for early cancer detection. Hospitals and diagnostic centers in urban regions are rapidly adopting advanced tools such as cystoscopy, urine lab tests, imaging tests, and molecular assays. Integration of diagnostics with electronic health records and hospital information systems enhances workflow efficiency and patient care. Awareness campaigns and health education programs are encouraging early testing and monitoring. Technological advancements, including AI-assisted imaging and non-invasive urine-based assays, are improving diagnostic accuracy. Moreover, increasing investments from private diagnostic companies and research institutes are further propelling market expansion.

Australia Bladder Cancer Diagnostics Market Insight

The Australia bladder cancer diagnostics market is growing steadily due to a high standard of healthcare, increasing government support for cancer screening programs, and rising patient awareness of early detection benefits. Hospitals, cancer research institutes, and independent laboratories are the primary adopters of cystoscopy, urine lab tests, biopsy, and imaging diagnostics. Government initiatives promoting routine screening, along with collaborations with private healthcare providers, enhance accessibility and adoption rates. Advanced diagnostic technologies, such as molecular assays and imaging systems, are increasingly being integrated into clinical practice. Rising incidence of bladder cancer among older populations is driving demand for regular testing. In addition, strong reimbursement frameworks and high healthcare expenditure support market growth.

Asia-Pacific Bladder Cancer Diagnostics Market Share

The Asia-Pacific Bladder Cancer Diagnostics industry is primarily led by well-established companies, including:

- Astellas Pharma Inc. (Japan)

- Sysmex Corporation (Japan)

- FUJIFILM Corporation (Japan)

- Abbott (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- GE HealthCare (U.S.)

- Siemens Healthineers AG (Germany)

- Koninklijke Philips N.V., (Netherlands)

- Medtronic (Ireland)

- Thermo Fisher Scientific Inc. (U.S.)

- Illumina, Inc. (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- PerkinElmer (U.S.)

- Agilent Technologies, Inc. (U.S.)

- QIAGEN (Germany)

- bioMérieux (France)

- Hologic, Inc. (U.S.)

- BD (U.S.)

- AbbVie Inc. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

What are the Recent Developments in Asia-Pacific Bladder Cancer Diagnostics Market?

- In July 2025, Safdarjung Hospital in New Delhi announced significant upgrades to its urology services, including the installation of advanced medical equipment such as India's first video urodynamic machine with near-infrared spectroscopy. These enhancements aim to improve diagnostic and treatment capabilities for bladder cancer patients, particularly benefiting economically disadvantaged individuals

- In June 2025, the ANZUP 1301 trial commenced in Australia, marking the largest randomized study in the bladder cancer field in the past decade. This trial involves 501 patients across 17 sites and aims to evaluate the efficacy of a new combination treatment for high-risk, non-muscle-invasive bladder cancer, potentially reducing the need for bladder removal or intensive therapies

- In April 2025, Craif, a Japanese startup spun off from Nagoya University, launched the miSignal test—a non-invasive urine-based diagnostic tool capable of detecting up to seven types of cancer, including bladder cancer. The test utilizes microRNA biomarkers and aims to enhance early detection, potentially reducing the need for invasive procedures such as cystoscopy

- In March 2025, the state of Telangana, India, launched a pilot program integrating artificial intelligence into cancer screening processes, focusing on early detection with improved accuracy. The initiative aims to enhance diagnostic capabilities and overcome challenges such as the shortage of radiologists, with plans to expand AI tools across state medical colleges and establish district-level screening centers

- In February 2025, a new urine-based diagnostic kit was introduced in Australia, offering a non-invasive method for the early detection of bladder cancer. This kit aims to improve early diagnosis, reduce unnecessary cystoscopies, and enhance patient quality of life by enabling at-home testing

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.