Asia Pacific Dairy Alternative Market

Market Size in USD Billion

USD

10.84 Billion

USD

17.45 Billion

2024

2032

USD

10.84 Billion

USD

17.45 Billion

2024

2032

| 2025 - 2032 | |

| USD 10.84 Billion | |

| USD 17.45 Billion | |

| % | |

|

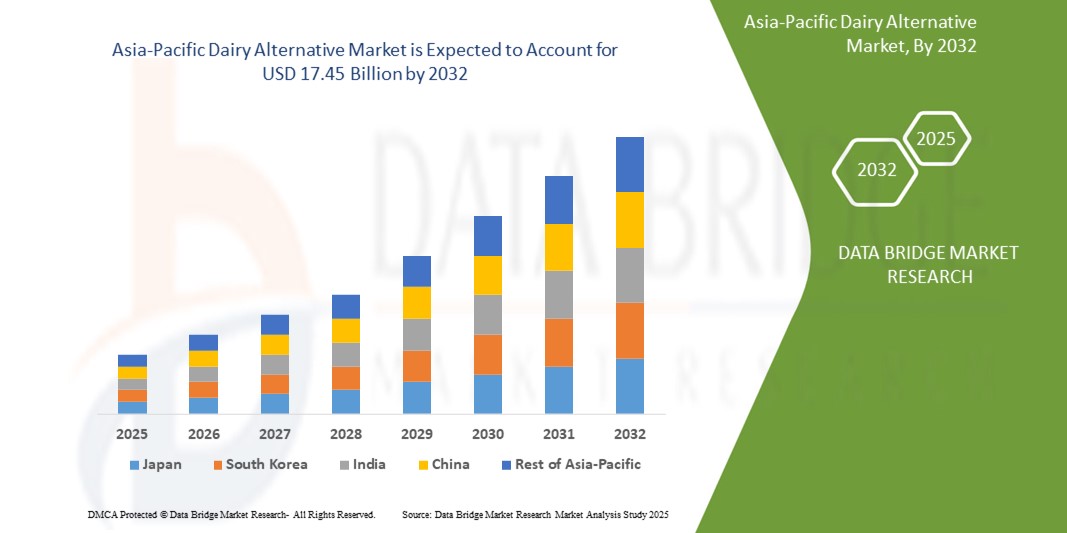

Asia-Pacific Dairy Alternative Market Size

- The Global Asia-Pacific Dairy Alternative Market size was valued at USD 10.84 billion in 2024 and is expected to reach USD 17.45 billion by 2032, at a CAGR of 8.32 % during the forecast period

- This growth is primarily driven by increasing health consciousness, rising cases of lactose intolerance, and a growing vegan population in countries like China, India, and Japan. The demand for plant-based milk alternatives such as soy, almond, and oat milk is surging due to their perceived health benefits and environmental sustainability

- Furthermore, government initiatives promoting plant-based diets, coupled with advancements in product formulations and expanding distribution channels, are significantly contributing to the market's expansion. The integration of dairy alternatives into mainstream food and beverage products is also enhancing their accessibility and appeal to a broader consumer base

Asia-Pacific Dairy Alternative Market Analysis

- Dairy alternatives, encompassing plant-based substitutes for traditional dairy products, are gaining significant traction in the Asia-Pacific region. This surge is attributed to increasing health consciousness, rising lactose intolerance, and a growing vegan population. Consumers are seeking nutritious, sustainable, and ethical food options, leading to a heightened demand for plant-based milk, yogurt, cheese, and other dairy alternatives

- The market's growth is propelled by several factors, including the prevalence of lactose intolerance in the region, environmental concerns associated with dairy farming, and the expanding availability of dairy alternative products through various distribution channels. Additionally, the influence of Western dietary trends and the rise of flexitarian diets are contributing to the market's expansion

- China currently dominates the Asia-Pacific dairy alternatives market, accounting for a significant revenue share. This dominance is due to the country's large population, increasing disposable incomes, and a growing awareness of health and wellness. The Chinese market is witnessing a rapid adoption of plant-based dairy products, with soy milk being particularly popular

- India is projected to be the fastest-growing market for dairy alternatives in the Asia-Pacific region during the forecast period. Factors such as a high prevalence of lactose intolerance, a large vegetarian population, and increasing health consciousness are driving the demand for plant-based dairy products in the country. The market is further supported by the availability of a wide range of dairy alternative products catering to diverse consumer preferences

- Soy-based products currently lead the Asia-Pacific dairy alternatives market, holding the largest market share. This dominance is attributed to soy's high protein content, affordability, and widespread availability. However, almond-based dairy alternatives are experiencing rapid growth due to their perceived health benefits, including being low in calories and rich in vitamins and minerals

Report Scope and Asia-Pacific Dairy Alternative Market Segmentation

|

Attributes |

Smart Lock Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Asia-Pacific Dairy Alternative Market Trends

“Personalization and Functional Innovation in Dairy Alternatives”

- A significant and accelerating trend in the Asia-Pacific dairy alternatives market is the shift towards personalized and functional plant-based products. Consumers are increasingly seeking dairy alternatives that cater to specific health needs, such as lactose intolerance, cholesterol management, and dietary preferences. This demand is driving innovation in product formulations, including the addition of probiotics, vitamins, and minerals to plant-based milks and yogurts

- For instance, companies like Oatly have expanded their product lines in the region, introducing oat-based beverages fortified with calcium and vitamin D to appeal to health-conscious consumers. Similarly, Vitasoy has launched soy and almond milk variants enriched with nutrients to support immune health

- The integration of technology is also playing a role in this trend. Brands are utilizing AI and machine learning to analyze consumer preferences and health data, enabling them to offer personalized product recommendations and develop new formulations that align with consumer health goals

- This focus on personalization and functional benefits is reshaping consumer expectations in the dairy alternatives market. As a result, companies are investing in research and development to create products that not only serve as substitutes for traditional dairy but also offer added health benefits, thereby enhancing their appeal to a broader consumer base

- The demand for personalized and functionally enriched dairy alternatives is growing rapidly across the Asia-Pacific region, particularly in urban areas where consumers are more health-conscious and open to adopting new dietary trends. This trend is expected to continue driving innovation and growth in the dairy alternatives market

Asia-Pacific Dairy Alternative Market Dynamics

Driver

“Rising Health Awareness and Lactose Intolerance Fueling Demand”

- The Asia-Pacific dairy alternatives market is experiencing significant growth, primarily driven by increasing health consciousness and the high prevalence of lactose intolerance among the population. Studies indicate that over 90% of adults in East Asia experience some degree of lactose malabsorption, leading consumers to seek plant-based alternatives such as soy, almond, and oat milk

- Health-conscious consumers are turning to dairy alternatives perceived as healthier options, often lower in calories and cholesterol, and free from lactose. The rising incidence of chronic diseases related to animal fats, such as cardiovascular conditions, further underscores the shift towards plant-based dairy

- The expanding vegan population in countries like Australia and India is also contributing to the increased demand for dairy alternatives. Cultural and ethical considerations, along with environmental concerns associated with dairy farming, are prompting consumers to opt for plant-based options

- Manufacturers are responding to this demand by introducing a wide range of fortified and functional products targeting various consumer segments. Innovations include plant-based beverages enriched with essential nutrients like calcium and vitamin D, catering to health-conscious consumers

Restraint/Challenge

“High Costs and Limited Accessibility in Rural Areas”

- Despite the growing demand, the higher cost of dairy alternatives compared to traditional dairy products remains a significant barrier. In countries like India, plant-based alternatives such as almond or soy milk can cost nearly twice as much as cow's milk, making them less accessible to the price-sensitive population

- The elevated prices are attributed to factors such as the cost of raw materials, processing complexities, and packaging requirements. Additionally, the lack of economies of scale and government subsidies that benefit the traditional dairy industry further exacerbate the pricing challenge for plant-based alternatives

- Access to dairy alternatives is still limited in rural parts of the Asia-Pacific region. While urban centers have a growing variety of plant-based options, rural areas face limited availability due to underdeveloped supply chains and distribution challenges. This limits market penetration in less developed regions with significant potential consumer bases

- Taste and texture differences between plant-based alternatives and traditional dairy products also pose challenges. Some consumers find plant-based milks lacking in creaminess or having distinct flavors that are unfamiliar or unappealing, impacting adoption rates

- Overcoming these challenges requires efforts to reduce production costs, improve distribution networks, and enhance product formulations to better match consumer expectations. Additionally, increasing consumer education and awareness about the benefits and availability of dairy alternatives can help drive broader adoption

Asia-Pacific Dairy Alternative Market Scope

The Asia-Pacific dairy alternative market is segmented on the basis of product type, type, formulation, application, nutritive, and distribution channel.

- By Product Type

On the basis of product type, the Asia-Pacific dairy alternative market is segmented into Soy Milk, Almond Milk, Coconut Milk, Cashew Milk, Oat Milk, and Rice Milk. The Soy Milk segment held the largest market revenue share in 2024, attributed to its long-standing presence, affordability, and high protein content, especially in countries like China and Japan where soy-based diets are traditional

The Almond Milk segment is anticipated to witness the fastest growth rate from 2025 to 2032. This growth is driven by increasing consumer awareness of its health benefits, such as lower blood sugar levels, cholesterol, and blood pressure, along with its increasing adoption by those seeking lactose-free and low-calorie options

- By Type

On the basis of type, the Asia-Pacific dairy alternative market is segmented into Inorganic and Organic. The Inorganic (Conventional) segment accounted for the largest market revenue share in 2024, primarily due to its widespread availability and relatively lower price points compared to organic alternatives, making it more accessible to a broader consumer base

The Organic segment is expected to witness the fastest CAGR from 2025 to 2032. This growth is fueled by increasing consumer awareness regarding health and environmental concerns, leading to a rising preference for natural, chemical-free, and sustainably sourced organic dairy alternative products

- By Formulation

On the basis of formulation, the Asia-Pacific dairy alternative market is segmented into Plain and Sweetened, Flavored and Unsweetened, Flavored and Sweetened, and Plain and Unsweetened. The Plain and Unsweetened segment is expected to hold a significant market share as consumers increasingly opt for healthier options with no added sugars.

The Flavored and Sweetened segment is anticipated to witness substantial growth, particularly among consumers seeking taste and variety in their dairy alternatives, with Asian-inspired flavors gaining traction.

- By Application

On the basis of application, the Asia-Pacific dairy alternative market is segmented into Food and Beverages. The Beverages segment accounted for the largest market revenue share in 2024, driven by the strong demand for dairy alternative milks (soy, almond, oat, etc.) for direct consumption, as well as in coffee, tea, and other drinks.

The Food segment is expected to witness the fastest CAGR from 2025 to 2032, propelled by the growing use of dairy alternatives in various food applications such as yogurts, ice creams, cheeses, and other culinary uses, catering to the rising demand for plant-based food products.

- By Nutritive

On the basis of nutritive, the Asia-Pacific dairy alternative market is segmented into Protein, Vitamins, and Carbohydrates. The Protein segment is expected to hold a significant market share, driven by consumers seeking high-protein plant-based options for muscle growth, satiety, and overall health.

The Vitamins segment is anticipated to witness strong growth, as manufacturers fortify dairy alternative products with essential vitamins (like Vitamin D and B12) to match the nutritional profile of traditional dairy and cater to health-conscious consumers.

- By Distribution Channel

On the basis of distribution channel, the Asia-Pacific dairy alternative market is segmented into Supermarkets/Hypermarkets, Online, and Specialized Stores. The Supermarkets/Hypermarkets segment held the largest market revenue share in 2024, due to their wide product availability, consumer convenience, and established presence in both urban and semi-urban areas.

The Online segment is expected to witness the fastest CAGR from 2025 to 2032. This growth is driven by increasing internet and smartphone penetration, the convenience of home delivery, and the rising popularity of e-commerce platforms for grocery shopping, especially among younger demographics.

- By Brands

Key brands operating in the Asia-Pacific dairy alternative market include Silk, Blue Diamond, So Delicious, Califia Farms, Dream, Oatly, Vitasoy International Holdings Ltd., SunOpta Inc., Danone S.A., and others. These brands are continually innovating with new product launches and expanded distribution to cater to the evolving consumer preferences in the region.

Asia-Pacific Dairy Alternative Market Regional Analysis

The Asia-Pacific dairy alternative market is a rapidly expanding sector, driven by a confluence of health, ethical, and environmental factors. The region's diverse consumer base and varying levels of economic development contribute to distinct market dynamics across its key countries

- China Dairy Alternative Market Insight

The China dairy alternative market accounted for the largest market revenue share in Asia Pacific in 2024, attributed to the country's expanding middle class, rapid urbanization, and high rates of technological adoption. China stands as one of the largest markets for plant-based food and beverages, and dairy alternatives are becoming increasingly popular in residential and food service sectors. The push towards healthier lifestyles, a growing understanding of lactose intolerance, and the availability of diverse and affordable dairy alternative options, alongside strong domestic manufacturers, are key factors propelling the market in China

- India Dairy Alternative Market Insight

The India dairy alternative market is projected to witness significant growth throughout the forecast period. This surge is primarily driven by India's vast vegetarian population, increasing awareness of health benefits associated with plant-based diets, and a rising prevalence of lactose intolerance. Government initiatives promoting plant-based foods, coupled with a growing number of domestic and international brands entering the market, are also contributing to its expansion. The increasing availability of dairy alternatives through various distribution channels, including online platforms, further fuels this growth

- Japan Dairy Alternative Market Insight

The Japan dairy alternative market is gaining momentum due to the country’s high-tech culture, growing health consciousness, and demand for innovative and convenient food options. While traditional dairy products have a strong foothold, the Japanese market is increasingly open to plant-based alternatives driven by concerns for health, environmental impact, and animal welfare. The integration of dairy alternatives into traditional Japanese cuisine and the emphasis on premium, high-quality, and organic products are fueling growth. Japan's aging population also contributes to the demand for healthier and easily digestible alternatives

- Australia & New Zealand Dairy Alternative Market Insight

The Australia and New Zealand dairy alternative market is characterized by high consumer awareness regarding health and sustainability. These developed economies boast high disposable incomes and a strong focus on ethical food choices. Oat milk and other alternative milks are popular choices, and plant-based yogurt and ice cream are gaining momentum. The market is also driven by robust retail infrastructure and a strong trend towards flexitarian diets

- Southeast Asia Dairy Alternative Market Insight

The Southeast Asian dairy alternative market is experiencing rapid growth, primarily driven by rising disposable incomes, increasing urbanization, and a growing middle class. High rates of lactose intolerance in many Southeast Asian populations make dairy alternatives a natural choice. The region's diverse culinary traditions also provide opportunities for innovation, with local ingredients like coconut milk being widely used. The expansion of modern retail and e-commerce platforms further boosts accessibility and consumption of dairy alternatives

Asia-Pacific Dairy Alternative Market Share

The Asia-Pacific Dairy Alternative industry is primarily led by well-established companies, including:

- The WhiteWave Foods Company (U.S)

- Kite Hill (U.S)

- Oatly (Sweden)

- Blue Diamond Growers (U.S)

- Earth’s Own Food Company Inc. (Canada)

- SunOpta (Canada)

- Pureharvest (Australia)

- Pacific Foods of Oregon, Inc. (U.S)

- Sanitarium Health and Wellbeing Company (Australia)

- The Hain Celestial Group, Inc. (U.S)

Latest Developments in Global Smart Lock Market

- In March 2024, Kerry Dairy launched a new range of oat and dairy-blended products, combining the nutritional benefits of both ingredients. This innovative product line aims to provide a more sustainable and inclusive option for consumers seeking plant-based alternatives without compromising on taste or texture. This launch reflects Kerry Dairy's commitment to sustainability and catering to evolving consumer demands.

- In February 2024, Fonterra Co-operative Group Ltd. announced imminent plans to merge its dairy businesses in Australia and New Zealand (Fonterra Australia and Fonterra Brands New Zealand). While primarily a dairy company, this strategic integration initiative is expected to further strengthen the company's position in this region, potentially impacting its foray into dairy alternatives as well.

- In February 2023, Silk, a leading global plant-based milk brand, unveiled an advertising campaign called 'Got Milk?' in the US, highlighting the growing celebrity endorsement and mainstream acceptance of dairy alternatives, which resonates with the evolving consumer preferences in the Asia-Pacific region.

- In 2023, Café Coffee Day, India's largest coffee chain, expanded its beverage offerings to include milk alternatives across its extensive network of over 900 outlets. This demonstrates the foodservice industry's increasing commitment to meeting evolving consumer preferences for plant-based options in the region.

- In September 2022, Hershey India launched Sofit Plus, a plant protein-fortified drink. The product was developed as part of its 'Nourishing Minds' social initiative in collaboration with IIT-Bombay and Sion Hospital, aiming to meet the nutritional needs of underprivileged children.

- In September 2022, Vitasoy International Holdings Ltd. introduced its new Vitasoy Plant+ product line in Singapore, featuring almond milk and oat milk varieties that are high in calcium, low in sugar, and have zero cholesterol. This launch underscored Vitasoy's focus on expanding its dairy alternative portfolio and catering to health-conscious consumers in the region.

- In September 2022, Sanitarium launched a new master brand campaign for its plant-based milk brand, 'So Good,' demonstrating ongoing efforts by established brands to strengthen their market presence and awareness in the dairy alternative segment.

- In October 2022, Vitasoy International Holdings Ltd. announced plans to expand its dairy alternative business by acquiring shares from its joint venture Bega Cheese subsidiary, National Food Holdings Ltd. This strategic move signifies a consolidation and expansion trend within the market.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Asia Pacific Dairy Alternative Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Asia Pacific Dairy Alternative Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Asia Pacific Dairy Alternative Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.