Asia Pacific Infertility Testing Market

Market Size in USD Billion

CAGR :

%

USD

2.92 Billion

USD

5.38 Billion

2025

2033

USD

2.92 Billion

USD

5.38 Billion

2025

2033

| 2026 –2033 | |

| USD 2.92 Billion | |

| USD 5.38 Billion | |

| % | |

|

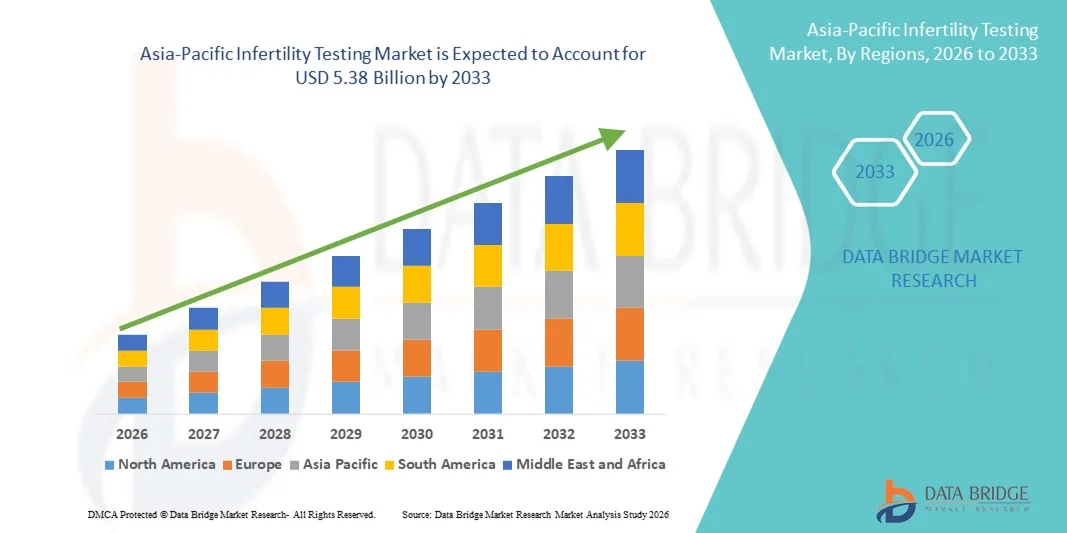

Asia-Pacific Infertility Testing Market Size

- The Asia-Pacific infertility testing market size was valued at USD 2.92 billion in 2025 and is expected to reach USD 5.38 billion by 2033, at a CAGR of 7.95% during the forecast period

- The market growth is largely fueled by growing public awareness of reproductive health, technological advances in diagnostic tools, and increased access to fertility evaluation services across both clinical and home settings. These trends are encouraging early screening and personalized health management, which are essential components of infertility testing

- Furthermore, rising consumer demand for accessible, precise, and user‑friendly fertility testing solutions, alongside expanding fertility care infrastructure in countries such as China and India, is positioning infertility testing as a critical component in reproductive healthcare. These converging factors are accelerating the uptake of advanced diagnostic technologies, thereby significantly boosting the region’s infertility testing market growth

Asia-Pacific Infertility Testing Market Analysis

- Infertility testing, including both female and male diagnostic solutions, is increasingly vital in the Asia‑Pacific region due to rising awareness of reproductive health, technological advances in hormone and ovulation test kits, and growing adoption of fertility evaluation services in both clinical and home-based settings

- The escalating demand for infertility testing is primarily fueled by the increasing public awareness of reproductive health issues, technological progress in diagnostic test kits, and the rising preference for accessible, user-friendly, and self-monitoring fertility solutions that enable early detection and personalized care

- China dominated the Asia‑Pacific infertility testing market in 2025 with a revenue share of 38.1%, driven by its population size, expanding healthcare infrastructure, and a strong presence of fertility clinics and diagnostic laboratories

- India is expected to be the fastest-growing country in the infertility testing market during the forecast period fueled by rising urbanization, increasing disposable incomes, and growing government and private investment in reproductive healthcare services

- Female infertility testing segment dominated the Asia‑Pacific market in 2025 with a 62.4% share, driven by high prevalence of reproductive health issues among women, increasing awareness about fertility management, widespread adoption of diagnostic test kits

Report Scope and Asia-Pacific Infertility Testing Market Segmentation

|

Attributes |

Asia-Pacific Infertility Testing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Asia-Pacific Infertility Testing Market Trends

Advancements in AI-Enabled and Home-Based Fertility Testing

- A significant and accelerating trend in the Asia‑Pacific infertility testing market is the integration of AI-driven diagnostics and home-based fertility testing kits, which are enhancing user convenience, accuracy, and personalized monitoring of reproductive health

- For instance, modern FSH and LH urine test kits now feature AI-assisted interpretation of hormone levels, allowing women to track ovulation cycles and fertility windows more accurately without frequent clinical visits

- AI integration in infertility testing enables predictive insights, such as suggesting optimal testing times or flagging irregular hormone patterns, while home-based digital kits provide real-time notifications, reducing the need for multiple clinic appointments

- The seamless integration of diagnostic test kits with mobile apps and telehealth platforms facilitates centralized management of reproductive health, allowing users to store results, schedule consultations, and track treatment plans through a single interface

- This trend towards more intelligent, user-friendly, and connected fertility testing solutions is fundamentally reshaping patient expectations for reproductive healthcare. Consequently, companies such as Ava and Mira are developing AI-enabled fertility monitors with features such as predictive ovulation alerts and app-based cycle management

- The demand for AI-driven, home-based infertility testing kits is growing rapidly across urban and semi-urban populations, as consumers increasingly prioritize convenience, privacy, and continuous fertility monitoring

- Rising digital literacy and smartphone penetration in APAC countries are enabling more users to adopt mobile-connected fertility solutions, fueling faster growth of home-based and AI-assisted testing

Asia-Pacific Infertility Testing Market Dynamics

Driver

Rising Awareness and Adoption of Fertility Diagnostics

- The increasing awareness of reproductive health issues, coupled with the expanding availability of fertility clinics and diagnostic solutions, is a significant driver for the heightened demand for infertility testing

- For instance, in March 2025, Mira Labs introduced AI-assisted ovulation test kits in India, designed for at-home use, which significantly increased consumer adoption of home-based fertility monitoring solutions

- As couples and individuals become more aware of infertility risks and the importance of early detection, testing kits offer insights such as hormone profiling, ovulation tracking, and fertility assessments, providing a compelling reason to adopt diagnostic solutions

- Furthermore, growing investments in reproductive healthcare services and telemedicine platforms are making fertility testing more accessible, encouraging adoption in both urban and semi-urban areas

- The convenience of home-based testing, AI-assisted interpretations, and app-based tracking tools are key factors propelling the uptake of infertility testing across Asia-Pacific, particularly among working couples seeking privacy and efficiency

- Government initiatives and awareness campaigns promoting reproductive health are helping to educate the public and increase adoption of infertility testing, particularly in emerging markets such as India and Southeast Asia

- Rising collaborations between diagnostic companies and hospitals or clinics are expanding the availability of advanced infertility testing services, increasing market penetration and credibility of home-based and clinical solutions

Restraint/Challenge

High Cost and Regulatory Compliance Hurdles

- The relatively high cost of advanced fertility test kits and diagnostic services poses a significant challenge to broader market penetration, particularly in price-sensitive segments of the population

- For instance, premium AI-assisted fertility monitors with integrated app tracking are priced higher than conventional hormone test kits, limiting adoption among lower-income groups

- Regulatory hurdles, such as approvals for diagnostic test kits and clinical validation requirements, can delay product launches and restrict availability in certain countries, impacting overall market growth

- While some affordable alternatives exist, the perception of higher costs for AI-enabled or home-based diagnostic kits can deter consumers who may not immediately recognize the value of advanced features

- Overcoming these challenges through pricing strategies, robust regulatory compliance, and awareness campaigns highlighting the benefits of early infertility testing will be crucial for sustained growth in the Asia-Pacific market

- Limited access to fertility testing in rural and remote areas continues to restrain market growth, as logistics and lack of trained personnel hinder adoption outside urban centers

- Data privacy and cybersecurity concerns related to app-based fertility tracking may slow adoption among tech-savvy but cautious consumers, requiring robust encryption and secure handling of sensitive reproductive health information

Asia-Pacific Infertility Testing Market Scope

The market is segmented on the basis of type, test kits, prescription mode, distribution channel, and end user.

- By Type

On the basis of type, the Asia-Pacific infertility testing market is segmented into female infertility testing and male infertility testing. The female infertility testing segment dominated the market with the largest revenue share of 62.4% in 2025, driven by the higher prevalence of reproductive health issues among women, widespread use of hormone and ovulation test kits, and strong demand for early fertility assessment in clinical and home-based settings. Female testing includes comprehensive evaluations such as Follicular Stimulating Hormone (FSH), Luteinizing Hormone (LH), and Human Chorionic Gonadotropin (HCG) monitoring, enabling personalized fertility management. Clinics and fertility centers often prioritize female testing due to its critical role in treatment planning and monitoring assisted reproductive technologies (ART). The segment also benefits from growing awareness campaigns and government initiatives promoting reproductive health. In addition, the availability of home-based AI-assisted testing kits further reinforces the dominance of female infertility testing.

The male infertility testing segment is anticipated to witness the fastest growth rate of 15.8% from 2026 to 2033, fueled by increasing recognition of male reproductive health issues, rising adoption of semen analysis, sperm count testing, and hormone profiling. The growth is supported by technological advances in AI-enabled diagnostic tools, increasing male participation in fertility planning, and greater awareness of male infertility as a treatable condition. Urban fertility clinics and telehealth platforms are expanding male testing services, offering home-based sample collection and remote consultation. Male testing adoption is also being driven by rising lifestyle-related fertility challenges, such as stress, obesity, and environmental factors.

- By Test Kits

On the basis of test kits, the market is segmented into FSH urine test kits, LH urine test kits, HCG hormone blood test kits, and others. The FSH urine test kits segment dominated the market in 2025 with a 28% share, driven by their established role in assessing ovarian reserve, ease of home use, and integration into fertility monitoring apps. FSH kits are widely recommended by gynecologists and fertility specialists for baseline evaluation before ART procedures. The segment’s dominance is further supported by strong patient awareness, availability in both prescription-based and OTC formats, and compatibility with mobile health platforms. FSH kits also benefit from standardized protocols that ensure accuracy and reliability in both clinical and home settings. The increasing prevalence of female reproductive health awareness campaigns also reinforces adoption.

The LH urine test kits segment is expected to witness the fastest CAGR of 17.2% from 2026 to 2033, driven by their critical role in ovulation tracking and fertility planning. LH kits are increasingly preferred by home users due to convenience, real-time feedback, and integration with fertility apps. Rising adoption of AI-assisted cycle prediction and telehealth-based fertility guidance further accelerates growth. Urban populations in China, India, and Southeast Asia are particularly adopting LH kits to support natural conception strategies. Moreover, rising partnerships between test kit manufacturers and online pharmacies are expanding distribution channels, making LH kits more accessible.

- By Prescription Mode

On the basis of prescription mode, the market is segmented into prescription-based and over-the-counter (OTC) based test kits. The prescription-based segment dominated the market in 2025 with a 70% share, due to the reliance on healthcare providers for accurate diagnosis, validated testing protocols, and professional interpretation of hormone and fertility markers. Prescription-based kits are widely used in fertility clinics, hospitals, and research institutes, ensuring clinical reliability and integration with assisted reproductive treatments. The segment’s dominance is reinforced by regulatory approvals, insurance coverage, and patient trust in healthcare professionals. In addition, clinical oversight helps ensure test accuracy and appropriate follow-up care. Telehealth platforms increasingly support prescription-based kits by enabling remote ordering and consultation.

The OTC-based segment is expected to witness the fastest growth rate of 18.5% from 2026 to 2033, fueled by growing consumer demand for privacy, convenience, and at-home fertility monitoring. OTC kits allow individuals to self-assess ovulation and hormone levels without visiting clinics, supporting early fertility awareness and planning. Rapid urbanization, rising digital literacy, and smartphone-based integration of test kits with mobile apps are accelerating adoption. OTC growth is also supported by partnerships with e-commerce and online pharmacy platforms, increasing accessibility across semi-urban and tier-2 cities.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospitals pharmacies, online pharmacies, and pharmacies and drug stores. The hospitals pharmacies segment dominated the market in 2025 with a 55% share, driven by the high adoption of clinically validated kits and professional consultation services. Hospitals and fertility centers prefer purchasing through their pharmacy networks to ensure reliability and integration with patient treatment protocols. Hospitals pharmacies also facilitate access to prescription-based kits and support follow-up testing, reinforcing their dominance. The segment benefits from trust, convenience, and bundled services in fertility assessment packages. Established healthcare institutions in China, India, and Japan contribute substantially to revenue.

The online pharmacies segment is expected to witness the fastest CAGR of 20.3% from 2026 to 2033, fueled by increasing e-commerce adoption, privacy concerns, and demand for home delivery of test kits. Consumers in urban and semi-urban areas are increasingly leveraging online platforms to purchase FSH, LH, and HCG test kits conveniently. Integration of AI-assisted guidance and mobile apps with online ordering further enhances user experience and adoption. Marketing initiatives by test kit manufacturers on online platforms are also boosting awareness and penetration in emerging APAC markets.

- By End User

On the basis of end user, the market is segmented into fertility centers, hospitals and clinics, research institutes, and cryobanks. The fertility centers segment dominated the market in 2025 with a 48% share, driven by the high demand for advanced diagnostic testing in assisted reproductive technologies (ART) and personalized treatment plans. Fertility centers often use multiple test kits for comprehensive evaluation, including FSH, LH, and HCG monitoring, ensuring accurate diagnosis and treatment optimization. The dominance is reinforced by the increasing number of ART clinics, expansion of IVF services, and growing patient awareness. Fertility centers also provide integrated care with counseling and AI-assisted fertility monitoring.

The research institutes segment is expected to witness the fastest CAGR of 19.1% from 2026 to 2033, fueled by rising investments in reproductive health studies, fertility technology innovation, and hormone research. Research institutes are adopting advanced diagnostic kits for clinical trials, biomarker validation, and longitudinal studies on reproductive health. Collaborations with hospitals and fertility centers further accelerate adoption. Growing government funding and private sector R&D initiatives are supporting segment growth, particularly in countries such as China, Japan, and India.

Asia-Pacific Infertility Testing Market Regional Analysis

- China dominated the Asia‑Pacific infertility testing market in 2025 with a revenue share of 38.1%, driven by its population size, expanding healthcare infrastructure, and a strong presence of fertility clinics and diagnostic laboratories

- Consumers and patients in the region increasingly value convenient, accurate, and home-based fertility testing solutions, along with integration of AI-assisted diagnostic tools that enable early detection and personalized reproductive healthcare management

- This widespread adoption is further supported by rising disposable incomes, urbanization, increasing digital literacy, and government initiatives promoting reproductive health, establishing infertility testing as a preferred solution for couples seeking fertility evaluation and management across clinical and home settings

The China Infertility Testing Market Insight

The China infertility testing market dominated APAC with the largest revenue share of 38.1% in 2025, fueled by the country’s large population, growing awareness of reproductive health, and rapid expansion of fertility clinics and diagnostic laboratories. Consumers are increasingly adopting both prescription-based and OTC test kits, supported by AI-enabled ovulation and hormone monitoring tools. Urban centers such as Beijing, Shanghai, and Guangzhou are driving adoption due to higher disposable incomes, digital literacy, and access to specialized fertility care. Government initiatives promoting fertility awareness, particularly in response to declining birth rates, further reinforce market growth. The integration of home-based testing kits with mobile apps also allows users to track hormone levels and ovulation cycles conveniently, increasing the adoption rate across urban households.

India Infertility Testing Market Insight

The India infertility testing market is expected to grow at the fastest CAGR during the forecast period, driven by rising urbanization, increasing disposable incomes, and growing reproductive healthcare infrastructure. Urban hubs such as Delhi, Mumbai, and Bangalore are witnessing the highest adoption of clinical and home-based fertility testing solutions. The availability of affordable OTC kits, growing digital literacy, and telehealth platforms supporting remote consultation are key factors accelerating market growth. In addition, rising awareness campaigns and collaborations between diagnostic companies and hospitals are enhancing access to fertility diagnostics, making early detection and monitoring increasingly convenient for working couples. The trend towards personalized fertility care and AI-assisted predictive testing further supports adoption.

Japan Infertility Testing Market Insight

The Japan infertility testing market is gaining momentum, driven by the country’s high awareness of reproductive health, the growing prevalence of age-related fertility issues, and the adoption of home-based AI-assisted test kits. Fertility clinics and hospitals in Tokyo, Osaka, and Yokohama are leveraging advanced diagnostic solutions for hormone tracking, ovulation monitoring, and assisted reproductive technology (ART) planning. Home-based fertility testing adoption is increasing due to convenience, privacy, and integration with mobile apps that provide cycle prediction and treatment guidance. Furthermore, Japan’s aging population and rising infertility rates are spurring demand for accessible, accurate, and continuous monitoring solutions, particularly among working couples.

South Korea Infertility Testing Market Insight

The South Korea infertility testing market is expanding steadily, driven by increasing infertility awareness, government support for reproductive health, and adoption of advanced diagnostic tools. Urban centers such as Seoul, Busan, and Incheon are leading growth due to a concentration of fertility clinics, hospitals, and research institutes offering both prescription-based and home-based fertility kits. Consumers increasingly prefer AI-assisted ovulation and hormone monitoring tools integrated with mobile apps, enabling personalized fertility tracking and remote consultations. Rising government initiatives to address low birth rates, combined with high smartphone penetration and digital literacy, are accelerating the adoption of fertility testing solutions. In addition, partnerships between diagnostic companies and online pharmacies are improving accessibility, affordability, and convenience for tech-savvy urban consumers.

Asia-Pacific Infertility Testing Market Share

The Asia-Pacific Infertility Testing industry is primarily led by well-established companies, including:

- F. Hoffmann La Roche Ltd. (Switzerland)

- Abbott (U.S.)

- Quidel Corporation (U.S.)

- BIOMÉRIEUX (France)

- Procter & Gamble (U.S.)

- Halotech DNA (India)

- Andrology Solutions (U.K.)

- SA Scientific (U.S.)

- Atlas Medical UK (U.K.)

- Babystart Ltd. (U.K.)

- Wondfo Biotech Co., Ltd (China)

- Fairhaven Health, LLC (U.S.)

- SPD Swiss Precision Diagnostics GmbH (Switzerland)

- Equinox Biotech Co., Ltd (China)

- Pregmate (China)

- Premom (U.S.)

- Cook (U.S.)

- Vitrolife AB (Sweden)

- FUJIFILM Irvine Scientific (U.S.)

- Esco Micro Pte Ltd. (Singapore)

What are the Recent Developments in Asia-Pacific Infertility Testing Market?

- In November 2025, GENPRIME expanded its fertility services with new flagship fertility centres in Singapore and Manila to address growing reproductive health needs in Asia‑Pacific, enhancing access to fertility diagnostics, personalised treatment plans, assisted reproductive technologies (ART), and ongoing care for couples seeking parenthood

- In May 2025, ASPIRE (a fertility advocacy body) launched a regional fertility health awareness drive under its new leadership to educate and engage policymakers and the public across Asia‑Pacific on declining birth rates, infertility challenges, and the importance of reproductive health services

- In May 2025, a policy paper titled “Improving Access to Fertility Treatment in Asia Pacific” was published, urging coordinated government action across 13 Asia‑Pacific countries to address fertility care barriers, expand access to ART and egg freezing, and recognize infertility as a disease requiring public health support

- In September 2024, PacBio announced the formation of the “HiFi Solves Sub‑fertility Consortium” in Singapore, a research collaboration across Asia‑Pacific aiming to harness high‑fidelity long‑read sequencing to improve diagnosis and treatment of subfertility and recurrent pregnancy loss through advanced genomic techniques

- In December 2023, Indian health‑tech firm Arva Health launched a new at‑home infertility diagnostic tool tailored for Indian women with reproductive health concerns such as PCOS and thyroid issues, providing comprehensive hormone insights including AMH and ovarian reserve testing to improve fertility awareness and testing accessibility

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.