Asia Pacific Nuclear Imaging Devices Market

Market Size in USD Billion

USD

1.63 Billion

USD

2.45 Billion

2025

2033

USD

1.63 Billion

USD

2.45 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.63 Billion | |

| USD 2.45 Billion | |

| % | |

|

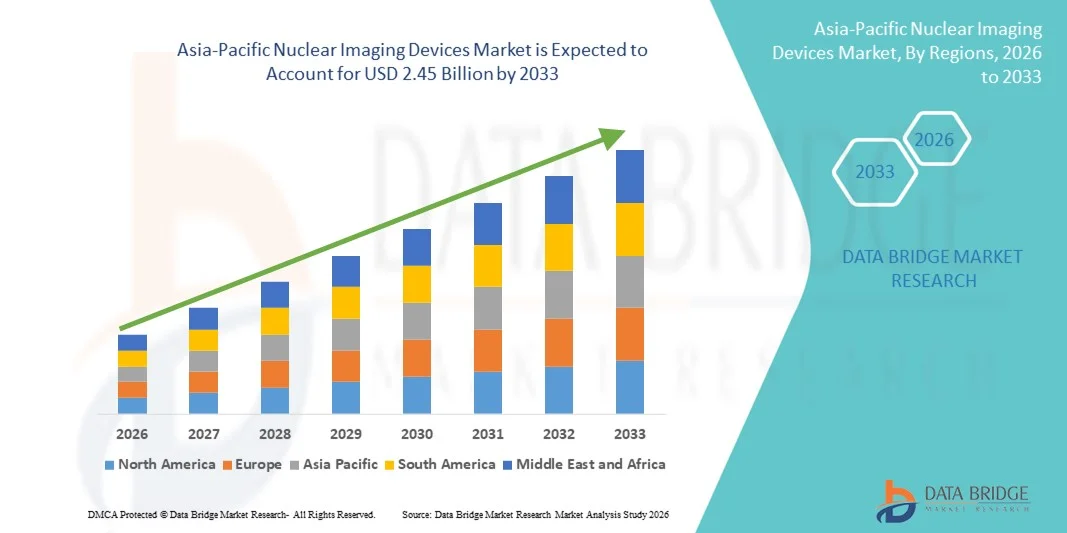

Asia-Pacific Nuclear Imaging Devices Market Size

- The Asia-Pacific nuclear imaging devices market size was valued at USD 1.63 billion in 2025 and is expected to reach USD 2.45 billion by 2033, at a CAGR of 5.25% during the forecast period

- The market growth is largely fueled by rising healthcare infrastructure investments, increasing prevalence of chronic diseases such as cancer and cardiovascular disorders, and technological advancements in imaging modalities which are enhancing diagnostic precision across clinical applications

- Furthermore, expanding diagnostic capabilities in hospitals and imaging centers, growing demand for early disease detection, and supportive government initiatives for healthcare modernization are driving adoption of nuclear imaging solutions in the region. These converging factors are accelerating uptake of advanced nuclear imaging devices, thereby significantly boosting the industry’s growth

Asia-Pacific Nuclear Imaging Devices Market Analysis

- Nuclear imaging devices, including Single Photon-Emission Computed Tomography (SPECT), Hybrid PET, and Planar Scintigraphy systems, are increasingly vital components of modern diagnostic workflows in hospitals and imaging centers across the Asia-Pacific due to their ability to provide highly accurate functional and molecular imaging for early disease detection and treatment planning

- The escalating demand for nuclear imaging devices is primarily fueled by rising prevalence of chronic and lifestyle diseases such as cancer and cardiovascular disorders, growing healthcare infrastructure investments, and increasing adoption of advanced imaging modalities for precise diagnostics across clinical applications

- China dominated the Asia-Pacific nuclear imaging devices market with the largest revenue share of 38.5% in 2025, characterized by well-established healthcare infrastructure, government support for modern diagnostic technologies, and a growing number of hospitals and imaging centers equipped with hybrid PET and SPECT systems

- India is expected to be the fastest growing country during the forecast period due to expanding healthcare access, increasing diagnostic centers, and rising healthcare expenditure fueled by urbanization and improving disposable incomes

- Single Photon-Emission Computed Tomography (SPECT) segment dominated the Asia-Pacific nuclear imaging devices market with a share of 41.2% in 2025, driven by its broad clinical applications in oncology, cardiology, and neurology, as well as cost-effectiveness and wide availability in hospitals and imaging centers across the countries

Report Scope and Asia-Pacific Nuclear Imaging Devices Market Segmentation

|

Attributes |

Asia-Pacific Nuclear Imaging Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Asia-Pacific Nuclear Imaging Devices Market Trends

Integration of Hybrid Imaging and AI-Driven Diagnostics

- A significant and accelerating trend in the Asia-Pacific nuclear imaging devices market is the increasing integration of hybrid PET/SPECT systems with AI-powered diagnostic software, enhancing imaging accuracy and clinical workflow efficiency

- For instance, the Siemens Biograph Vision PET/CT system incorporates AI-based image reconstruction to reduce scan time while improving lesion detectability, enabling faster and more precise diagnostics

- AI integration in nuclear imaging devices allows features such as automated image analysis, predictive diagnostics, and pattern recognition in oncology and cardiology, improving clinical decision-making. For instance, GE Discovery MI utilizes AI algorithms to optimize PET image clarity and quantify tracer uptake for accurate tumor assessment

- The seamless integration of hybrid imaging systems with hospital PACS and radiology information systems facilitates centralized data management and streamlined reporting, enabling radiologists to monitor and analyze patient data more efficiently

- This trend towards more intelligent, precise, and interconnected imaging solutions is reshaping clinical expectations in diagnostic radiology. For instance, Philips Vereos Digital PET/CT leverages AI-assisted reconstruction to enhance patient throughput while maintaining high diagnostic quality

- The adoption of hybrid PET/SPECT systems with AI-driven analytics is rapidly growing across oncology and cardiology departments, as hospitals prioritize diagnostic accuracy, workflow efficiency, and early disease detection

- Increasing interest in theranostics, combining diagnostics and targeted therapy monitoring using nuclear imaging devices, is emerging as a transformative trend across oncology departments in Asia-Pacific hospitals

Asia-Pacific Nuclear Imaging Devices Market Dynamics

Driver

Rising Healthcare Investments and Growing Prevalence of Chronic Diseases

- The increasing prevalence of cancer, cardiovascular, and neurological disorders, coupled with expanding healthcare infrastructure in Asia-Pacific, is a key driver for nuclear imaging device adoption

- For instance, in March 2025, GE Healthcare announced deployment of advanced PET/CT systems across multiple hospitals in India to support oncology diagnostics and therapy planning

- As patient volumes grow and early diagnosis becomes critical, nuclear imaging devices offer highly accurate functional imaging, improved detection rates, and better treatment monitoring, supporting clinician decision-making

- Furthermore, government initiatives and private hospital investments in advanced diagnostic equipment are making nuclear imaging a standard component of modern healthcare facilities

- The increasing availability of hospital-based imaging centers, rising patient awareness, and demand for minimally invasive diagnostics are key factors propelling adoption. For instance, several multi-specialty hospitals in China have upgraded to hybrid PET/SPECT systems to meet rising oncology and cardiology diagnostic needs

- For instance, collaborations between device manufacturers and hospital networks are enabling faster installation and maintenance of advanced imaging systems, reducing deployment delays

- Rising insurance coverage and reimbursement policies for advanced nuclear imaging procedures in countries such as Japan and South Korea are encouraging more hospitals to adopt these devices

Restraint/Challenge

High Cost and Regulatory Compliance Barriers

- The high acquisition and maintenance cost of nuclear imaging devices pose a significant challenge for adoption in smaller hospitals and developing countries, limiting market penetration

- For instance, procurement of hybrid PET/SPECT systems in emerging markets such as Vietnam is often delayed due to budgetary constraints and high upfront investment requirements

- Strict regulatory approvals, licensing, and safety compliance for radioactive tracers and imaging devices create hurdles for rapid deployment in new facilities. For instance, regulatory clearance for novel PET tracers in India can take several months, delaying clinical adoption

- While large hospitals in countries such as Japan and China can invest in cutting-edge imaging systems, cost-sensitive markets and smaller clinics may rely on older equipment, slowing growth

- Overcoming these challenges through cost-effective models, leasing options, and simplified regulatory processes, as well as educating clinicians on device utilization, will be vital for sustained market growth. For instance, some companies now offer service contracts and training programs to reduce operational burden on hospitals

- For instance, concerns over radiation exposure and safety protocols in nuclear imaging procedures can limit adoption in smaller imaging centers lacking specialized staff

- Limited local manufacturing and dependence on imported devices in countries such as India and Indonesia can increase costs and supply chain delays, hindering market growth

Asia-Pacific Nuclear Imaging Devices Market Scope

The market is segmented on the basis of product, application, and end user.

- By Product

On the basis of product, the Asia-Pacific nuclear imaging devices market is segmented into Single Photon-Emission Computed Tomography (SPECT), Hybrid PET, and Planar Scintigraphy. The SPECT segment dominated the market with the largest market revenue share of 41.2% in 2025, driven by its broad clinical applications in oncology, cardiology, and neurology. SPECT systems are widely adopted in hospitals and imaging centers due to their cost-effectiveness, availability of tracers, and established use in functional imaging. Clinicians often prefer SPECT for routine diagnostic procedures, and it is supported by a large installed base across Asia-Pacific countries. The segment also benefits from ongoing technological enhancements such as improved gamma cameras and software for image reconstruction, increasing diagnostic accuracy. In addition, SPECT systems integrate well with hospital PACS and reporting systems, facilitating efficient workflow and centralized patient data management.

The Hybrid PET segment is anticipated to witness the fastest growth at a CAGR of 8.3% from 2026 to 2033, fueled by increasing adoption in oncology and cardiology departments. Hybrid PET systems, such as PET/CT and PET/MRI, offer high-resolution imaging and precise molecular visualization, enabling early disease detection and therapy monitoring. Hospitals and specialty centers are increasingly investing in hybrid systems due to their ability to combine anatomical and functional imaging, reducing the need for multiple scans. The growing prevalence of cancer in countries such as China, India, and Japan, along with supportive government healthcare initiatives, is driving PET system adoption. Moreover, integration with AI-based diagnostic tools and cloud-based image processing platforms is enhancing clinical workflow efficiency. The segment’s growth is also supported by rising demand from research and academic institutions for advanced imaging in clinical trials and experimental therapeutics.

- By Application

On the basis of application, the market is segmented into oncology, cardiology, neurology, and other. The Oncology segment dominated the market with a revenue share of 45.5% in 2025, driven by the increasing incidence of cancer in Asia-Pacific countries and the crucial role of nuclear imaging in tumor detection, staging, and therapy monitoring. Hospitals and specialized cancer centers widely use PET and SPECT systems to guide targeted treatments, improve patient outcomes, and monitor treatment response. The segment benefits from continuous technological advancements, including hybrid imaging and AI-assisted diagnostic software, which enhance accuracy and reduce scan time. Governments in countries such as China, Japan, and South Korea are also investing in cancer care infrastructure, expanding access to nuclear imaging. Patient awareness campaigns and insurance coverage for advanced diagnostic procedures further support growth.

The Cardiology segment is expected to witness the fastest growth at a CAGR of 7.8% from 2026 to 2033, fueled by rising prevalence of cardiovascular diseases and increased adoption of nuclear imaging for myocardial perfusion and heart function analysis. Advanced SPECT and PET systems enable non-invasive assessment of cardiac conditions, reducing diagnostic errors and improving treatment planning. Hospitals and diagnostic centers are increasingly integrating cardiology-specific imaging protocols into hybrid systems. Government healthcare initiatives promoting early detection of heart disease, particularly in India and Southeast Asia, are also supporting rapid adoption. The segment’s growth is further boosted by clinicians’ preference for accurate, functional imaging in high-risk patients, alongside research studies on novel cardiac tracers.

- By End User

On the basis of end user, the market is segmented into hospitals, imaging centers, academic and research centers, and other. The Hospitals segment dominated the market with a share of 52.3% in 2025, driven by the widespread installation of nuclear imaging devices for oncology, cardiology, and neurology diagnostics. Hospitals benefit from advanced hybrid systems that allow centralized patient care, reduced scan duplication, and streamlined workflow. Large hospitals in China, Japan, and India are increasingly upgrading to hybrid PET/SPECT systems for improved imaging accuracy and patient throughput. Hospitals also leverage AI-assisted imaging platforms and cloud-based data management for better diagnostics. Furthermore, hospital adoption is supported by reimbursement policies, training programs for radiologists, and government initiatives for early disease detection.

The Imaging Centers segment is expected to witness the fastest growth at a CAGR of 8.5% from 2026 to 2033, fueled by the expansion of private diagnostic centers and outpatient facilities across Asia-Pacific. Imaging centers are increasingly investing in SPECT and hybrid PET systems to cater to rising outpatient demand, provide specialized diagnostic services, and reduce patient waiting times. Advanced imaging solutions integrated with cloud analytics allow centers to offer remote consultations and second-opinion services. Countries such as India, Vietnam, and Thailand are witnessing rapid growth in private imaging centers due to increasing healthcare awareness and affordability. The segment is also supported by collaborations with hospitals and research institutions for clinical trials and early disease screening programs.

Asia-Pacific Nuclear Imaging Devices Market Regional Analysis

- China dominated the Asia-Pacific nuclear imaging devices market with the largest revenue share of 38.5% in 2025, characterized by well-established healthcare infrastructure, government support for modern diagnostic technologies, and a growing number of hospitals and imaging centers equipped with hybrid PET and SPECT systems

- Hospitals and diagnostic centers in the country prioritize nuclear imaging devices for early detection of cancer, cardiovascular, and neurological disorders, with hybrid PET and SPECT systems widely adopted for accurate diagnosis and treatment planning

- This widespread adoption is further supported by government initiatives promoting modern healthcare facilities, high patient volumes in urban hospitals, and a growing number of private diagnostic centers, establishing nuclear imaging devices as the preferred choice for both public and private healthcare providers

The China Nuclear Imaging Devices Market Insight

The China nuclear imaging devices market captured the largest revenue share of 38.5% in 2025, fueled by significant investments in healthcare infrastructure and a growing incidence of chronic diseases such as cancer and cardiovascular disorders. Hospitals and diagnostic centers are increasingly prioritizing hybrid PET and SPECT systems for early disease detection, accurate treatment planning, and patient monitoring. The adoption of AI-based imaging analytics, coupled with government initiatives promoting advanced diagnostic facilities, is further driving market expansion. Moreover, rising patient awareness and increasing private hospital investments are supporting the growth of nuclear imaging solutions across both urban and semi-urban areas.

Japan Nuclear Imaging Devices Market Insight

The Japan nuclear imaging devices market is gaining momentum due to the country’s advanced healthcare infrastructure, high adoption of technology, and demand for precision diagnostics. Hospitals extensively use PET, SPECT, and hybrid systems for oncology, cardiology, and neurology applications, integrating imaging with AI-driven analysis for enhanced diagnostic accuracy and workflow efficiency. Furthermore, government support for modern healthcare solutions and growing patient volumes are encouraging continuous upgrades in imaging facilities. Japan’s focus on early disease detection and research-oriented applications in academic institutions is also fueling demand for advanced nuclear imaging devices.

India Nuclear Imaging Devices Market Insight

The India nuclear imaging devices market accounted for the largest market revenue share in Asia-Pacific after China in 2025, attributed to the rapidly expanding middle class, urbanization, and increasing healthcare expenditure. Hospitals and imaging centers are investing in SPECT and hybrid PET systems to cater to rising patient volumes, particularly for oncology and cardiology diagnostics. Government initiatives promoting smart healthcare facilities, alongside affordable nuclear imaging devices from domestic and international manufacturers, are accelerating market adoption. The push towards smart hospitals and increased awareness about early diagnosis are key factors driving the growth of nuclear imaging devices in India.

South Korea Nuclear Imaging Devices Market Insight

The South Korea nuclear imaging devices market is experiencing steady growth due to the country’s highly developed healthcare system and increasing adoption of hybrid imaging technologies. Hospitals and specialized centers leverage PET/CT and SPECT systems for oncology and cardiology diagnostics, with integration into AI-assisted imaging platforms enhancing efficiency and accuracy. Government reimbursement policies and initiatives for early disease detection further support market expansion. In addition, research institutions and academic hospitals are increasingly investing in advanced nuclear imaging systems for clinical studies, contributing to long-term growth.

Asia-Pacific Nuclear Imaging Devices Market Share

The Asia-Pacific Nuclear Imaging Devices industry is primarily led by well-established companies, including:

- GE HealthCare (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Siemens Healthineers AG (Germany)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- Digirad Corporation (U.S.)

- CMR Naviscan Corporation (U.S.)

- Neusoft Medical Systems Co., Ltd. (China)

- Shimadzu Corporation (Japan)

- Hitachi, Ltd. (Japan)

- FUJIFILM Holdings Corporation (Japan)

- Bracco Imaging S.p.A. (Italy)

- Cardinal Health, Inc. (U.S.)

- Alliar Medicina Diagnóstica S.A. (Brazil)

- DASA Brazil)

- NTP Radioisotopes SOC Ltd. (South Africa)

- Absolute Imaging, Inc. (U.S.)

- Alliar Medicos a Frente (Brazil)

- SurgicEye GmbH (Germany)

- Shanghai United Imaging Healthcare Co., Ltd. (China)

- Mediso Ltd. (Hungary)

What are the Recent Developments in Asia-Pacific Nuclear Imaging Devices Market?

- In October 2025, the National University Hospital (NUH) and the National University of Singapore (NUS) launched a new Molecular Imaging and Theranostics Centre that features Singapore’s first total‑body PET/CT system, aimed at transforming diagnostics, treatment and research in cancer and other diseases with faster, safer and more precise imaging

- In October 2025, Singapore’s Molecular Imaging and Theranostics Centre was widely reported for its game‑changing total‑body PET/CT system that significantly increases detection sensitivity and reduces scan time, advancing personalized medicine and research

- In October 2025, the All India Institute of Medical Sciences (AIIMS), Raipur became the only government hospital in Chhattisgarh equipped with advanced nuclear medicine infrastructure by installing an automated radio synthesizer and Gallium generator to produce next‑generation PET radiotracers in‑house, improving early diagnosis and personalized treatment capacity

- In June 2025, the All India Institute of Medical Sciences (AIIMS), Raipur installed an automated radio synthesizer and Gallium generator to begin in‑house production of next‑generation PET radiotracers, enabling advanced PET imaging services and personalized cancer diagnostics and therapy

- In June 2023, Penang Adventist Hospital in Malaysia was recognized as the Nuclear Medicine Service Provider of the Year 2023 by GlobalHealth Asia‑Pacific after installing its first digital PET/CT scanner to enhance diagnostic accuracy and track patient therapy responses, marking a significant upgrade in nuclear imaging capabilities for the region

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.