Asia Pacific Q Pcr And D Pcr Devices Market

Market Size in USD Million

USD

938.50 Million

USD

1,673.79 Million

2025

2033

USD

938.50 Million

USD

1,673.79 Million

2025

2033

| 2026 - 2033 | |

| USD 938.50 Million | |

| USD 1,673.79 Million | |

| % | |

|

Asia-Pacific q-PCR and d-PCR Devices Market Size

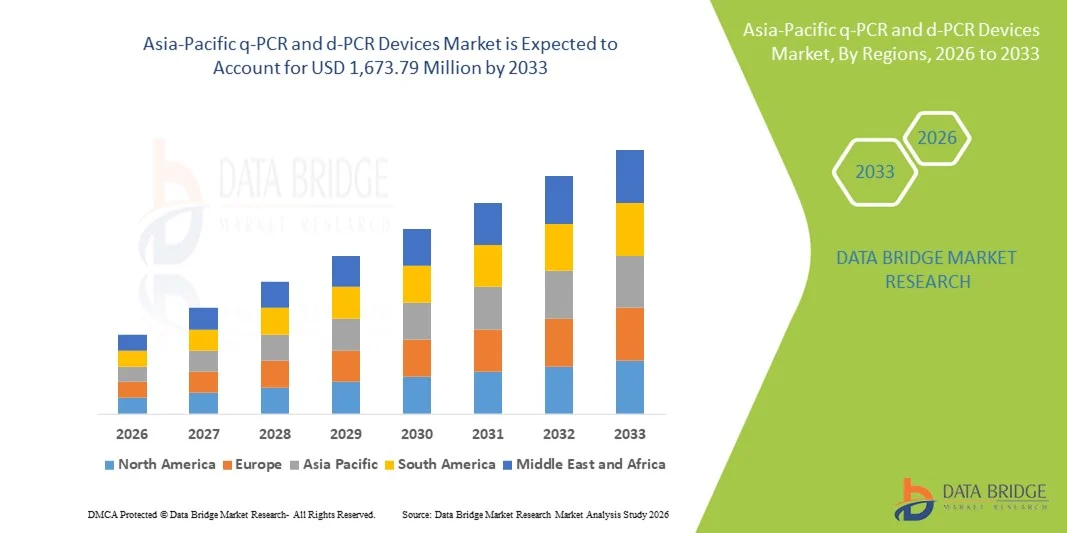

- The Asia-Pacific q-PCR and d-PCR devices market size was valued at USD 938.50 million in 2025 and is expected to reach USD 1,673.79 million by 2033, at a CAGR of 7.50% during the forecast period

- The market growth is largely driven by increased adoption of advanced molecular diagnostic technologies, rising demand for accurate and rapid pathogen detection, and expanding research activities in genomics and personalized medicine across the Asia‑Pacific region

- Furthermore, growing investments in healthcare infrastructure, rising prevalence of infectious diseases and genetic disorders, and technological advancements in q‑PCR and d‑PCR platforms are bolstering demand for these devices across clinical, research, and pharmaceutical sectors. These converging factors are facilitating broader market uptake, thereby significantly supporting industry growth

Asia-Pacific q-PCR and d-PCR Devices Market Analysis

- q‑PCR and d‑PCR devices, offering highly precise nucleic acid quantification for diagnostics, research, and forensic applications, are increasingly critical in modern molecular diagnostics and genomics research across both healthcare and pharmaceutical sectors due to their accuracy, rapid results, and adaptability to diverse laboratory workflows

- The rising demand for q‑PCR and d‑PCR devices is primarily fueled by the growing prevalence of infectious diseases and genetic disorders, increased investment in molecular diagnostics, and an expanding focus on personalized medicine and genomic research initiatives across the region

- China dominated the Asia‑Pacific q‑PCR and d‑PCR devices market with the largest revenue share of 38.5% in 2025, characterized by advanced healthcare infrastructure, strong government support for biotech research, and the presence of leading industry players, with substantial adoption in clinical laboratories, research institutes, and pharmaceutical R&D, driven by innovations in high-throughput and automated PCR platforms

- India is expected to be the fastest growing country in the market during the forecast period, due to increasing healthcare expenditure, rising awareness of molecular diagnostics, and adoption of cutting-edge PCR technologies in clinical, research, and diagnostic laboratories

- Quantitative PCR segment dominated the market with a 52.3% share in 2025, driven by its widespread use in clinical diagnostics, research applications, and compatibility with automated laboratory systems for high-throughput testing

Report Scope and Asia-Pacific q-PCR and d-PCR Devices Market Segmentation

|

Attributes |

Asia-Pacific q-PCR and d-PCR Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Asia-Pacific q-PCR and d-PCR Devices Market Trends

Integration with Automated and High-Throughput Systems

- A significant and accelerating trend in the Asia‑Pacific q‑PCR and d‑PCR devices market is the growing integration of PCR platforms with automated and high-throughput laboratory systems, enhancing workflow efficiency, reproducibility, and throughput in both clinical and research laboratories

- For instance, Thermo Fisher Scientific’s QuantStudio™ 12K Flex Real-Time PCR System integrates seamlessly with robotic liquid handlers, allowing automated sample preparation and processing for large-scale genomic studies

- Automation integration enables features such as reduced hands-on time, minimized human error, and faster processing of multiple samples, while advanced software can provide real-time data analysis and reporting. For instance, Bio-Rad’s CFX384 Touch Real-Time PCR System offers software-enabled multi-plate data analysis and automated quality control for research and diagnostic applications

- The seamless incorporation of PCR devices into laboratory information management systems (LIMS) facilitates centralized monitoring of experiments, data logging, and integration with other lab equipment, creating a unified and automated laboratory workflow

- This trend toward highly automated, interconnected, and software-enhanced PCR systems is fundamentally reshaping laboratory workflows and researcher expectations. For instance, Qiagen’s QIAcuity Digital PCR System enables fully automated workflows with minimal manual intervention, improving efficiency and reproducibility

- The demand for q‑PCR and d‑PCR devices with enhanced automation and high-throughput capabilities is growing rapidly across clinical, research, and pharmaceutical sectors, as laboratories prioritize efficiency, accuracy, and scalability

- Emerging applications in infectious disease surveillance, including pandemic preparedness, are driving investment in multi-sample high-throughput PCR systems capable of rapid large-scale testing. For instance, digital PCR platforms were deployed in select Asia-Pacific public health labs during COVID-19 for mass viral detection

Asia-Pacific q-PCR and d-PCR Devices Market Dynamics

Driver

Rising Demand Due to Increased Genomic Research and Diagnostics

- The increasing prevalence of genetic disorders, infectious diseases, and oncology research, coupled with rising investments in molecular diagnostics, is a significant driver for the heightened demand for q‑PCR and d‑PCR devices

- For instance, in March 2025, Bio-Rad Laboratories announced the expansion of its digital PCR solutions for oncology research, integrating high-throughput workflows to support precision medicine initiatives

- As healthcare providers and research institutions seek rapid and accurate nucleic acid quantification, q‑PCR and d‑PCR devices provide features such as absolute quantification, multiplexing, and high sensitivity, offering a compelling upgrade over conventional PCR methods

- Furthermore, the growing adoption of personalized medicine and large-scale genomic projects is making q‑PCR and d‑PCR devices integral components of modern laboratories, offering compatibility with advanced data analysis and laboratory automation platforms

- The ability to perform precise diagnostics, monitor disease progression, and conduct genomic research with minimal sample volumes is a key factor propelling the adoption of PCR devices in clinical, research, and pharmaceutical laboratories. The trend toward integrating PCR workflows with lab automation and digital analysis further contributes to market growth

- Increasing collaborations between pharmaceutical companies and academic research institutions to accelerate drug discovery and biomarker development is driving PCR device adoption. For instance, several oncology-focused projects in Japan and South Korea utilize high-throughput q‑PCR for biomarker validation

- Government initiatives promoting molecular diagnostics, infectious disease testing, and genomic research are supporting market growth in the region. For instance, India’s Department of Biotechnology funded multiple programs in 2025 that included advanced q‑PCR infrastructure for disease surveillance

Restraint/Challenge

High Cost and Technical Complexity

- The relatively high acquisition and maintenance costs of advanced q‑PCR and d‑PCR systems pose a significant challenge to broader market penetration, particularly in small or budget-constrained laboratories

- For instance, some cutting-edge digital PCR platforms from Thermo Fisher and Bio-Rad require substantial capital investment, making adoption slower in emerging economies despite growing demand

- Addressing these cost and technical barriers through user training, modular platforms, and lower-cost consumables is crucial for wider adoption. For instance, Qiagen and Bio-Rad offer scalable kits and consumables to reduce overall operational costs

- In addition, the complexity of operating sophisticated PCR devices, coupled with the need for skilled personnel and adherence to strict laboratory protocols, can hinder adoption in smaller clinical and research settings

- While efforts are being made to simplify workflows and reduce operational costs, the combination of high initial investment and technical requirements continues to challenge market growth. For instance, some laboratories adopt simpler q‑PCR setups before transitioning to high-throughput digital PCR systems to manage costs and technical learning curves

- Limited availability of trained molecular diagnostics personnel in certain Asia-Pacific countries further restrains market growth. For instance, small diagnostic labs in Southeast Asia face challenges in hiring staff skilled in digital PCR workflows

- Regulatory hurdles related to clinical validation and device approval for diagnostic applications can slow market entry for new PCR platforms. For instance, delays in local regulatory approvals in countries such as India and Indonesia have postponed adoption of some advanced digital PCR systems

Asia-Pacific q-PCR and d-PCR Devices Market Scope

The market is segmented on the basis of technology, product type, application, and end-user.

- By Technology

On the basis of technology, the Asia-Pacific q‑PCR and d‑PCR devices market is segmented into Quantitative PCR (q‑PCR) and Digital PCR (d‑PCR). The Quantitative PCR (q‑PCR) segment dominated the market with the largest revenue share of 52.3% in 2025, driven by its widespread adoption in clinical diagnostics, research applications, and high-throughput laboratories. q‑PCR offers real-time monitoring of nucleic acid amplification, making it ideal for applications such as pathogen detection, gene expression analysis, and genetic disorder screening. Researchers and clinical laboratories often prioritize q‑PCR systems for their robustness, reproducibility, and compatibility with automated workflows. The segment benefits from the extensive availability of reagents, consumables, and software tailored for q‑PCR systems, further reinforcing its dominance. Integration with laboratory information management systems (LIMS) and high-throughput platforms also enhances operational efficiency and reliability. Strong regional adoption in countries such as China and Japan contributes significantly to market share.

The Digital PCR (d‑PCR) segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by its ability to detect rare mutations and quantify low-abundance nucleic acids with higher sensitivity than conventional q‑PCR. d‑PCR is increasingly adopted in oncology, virology, and precision medicine applications, where absolute quantification is critical for accurate diagnostics and research. The growth is supported by technological advancements such as partitioning systems, automated workflows, and integration with high-throughput instruments. Rising awareness of d‑PCR’s precision and adoption in genomic research initiatives in countries such as India and South Korea are driving this growth. Moreover, d‑PCR’s expanding use in regulatory-approved clinical diagnostics is further propelling demand. The segment’s capability to reduce experimental variability and enhance reproducibility is a key factor for its rapid adoption.

- By Product Type

On the basis of product type, the market is segmented into instruments, reagents, consumables, and software. The Instruments segment dominated the market with a 45.8% share in 2025, owing to high demand for advanced q‑PCR and d‑PCR platforms in clinical laboratories, research institutions, and pharmaceutical R&D. Instruments form the backbone of molecular diagnostics workflows, providing the hardware for amplification, detection, and analysis. Established PCR systems from Thermo Fisher, Bio-Rad, and Qiagen are widely preferred due to their reliability, automation compatibility, and throughput capabilities. Laboratories often invest in high-performance instruments for long-term efficiency and accuracy, justifying their larger market share. The availability of instrument packages bundled with reagents and software further reinforces market dominance. Strong adoption in countries such as China and Japan, driven by well-established research and healthcare infrastructure, contributes significantly to revenue.

The Consumables segment is expected to witness the fastest growth from 2026 to 2033, driven by recurring demand for sample preparation kits, plates, tubes, and reagents required for PCR workflows. Consumables are critical for reproducible results, and increasing adoption of both q‑PCR and d‑PCR devices is expanding the consumables market. Emerging research labs, diagnostic centers, and home healthcare testing setups in India, South Korea, and Southeast Asia are boosting demand. The segment’s growth is further supported by rising genomic research initiatives, infectious disease testing programs, and the increasing need for reliable, high-quality consumables compatible with automated systems. Consumables also benefit from frequent replacement cycles, contributing to recurring revenue streams for suppliers. Technological advancements, such as low-volume consumables for high-throughput PCR, are further enhancing adoption rates.

- By Application

On the basis of application, the market is segmented into clinical applications, research applications, forensic applications, and others. The Clinical Applications segment dominated the market with a 49.6% share in 2025, due to the widespread use of PCR devices for pathogen detection, disease diagnostics, genetic disorder screening, and monitoring treatment responses. Hospitals, diagnostic centers, and laboratories rely on PCR technologies for rapid and accurate nucleic acid quantification. Clinical adoption is reinforced by government initiatives supporting molecular diagnostics, especially in countries such as China, Japan, and Australia. Increasing prevalence of infectious diseases and genetic disorders drives continuous demand for PCR-based clinical testing. Compatibility with high-throughput and automated instruments enhances efficiency, reproducibility, and reliability. Integration with laboratory software and data management systems further supports the segment’s dominance.

The Research Applications segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing genomics, oncology, and personalized medicine research in academic and pharmaceutical labs. d‑PCR and q‑PCR are critical tools for gene expression studies, biomarker discovery, and drug development research. Emerging economies such as India, South Korea, and Singapore are investing heavily in molecular biology research infrastructure, contributing to rapid adoption. The segment benefits from integration with automation and high-throughput platforms, which reduce experimental errors and accelerate research timelines. Expanding collaborations between universities, biotech firms, and pharmaceutical companies are fueling the research applications market. Technological innovations, such as multiplexed PCR assays and advanced software analysis, further drive segment growth.

- By End-User

On the basis of end-user, the market is segmented into hospitals, diagnostic centers, ambulatory centres, home healthcare, clinics, and community healthcare. The Hospitals segment dominated the market with a 41.6% share in 2025, due to high-volume testing requirements, advanced laboratory infrastructure, and the availability of skilled personnel to operate PCR devices. Hospitals extensively use PCR for disease diagnostics, infectious disease screening, and genetic testing. Large hospitals in countries such as China, Japan, and Australia have well-established molecular diagnostics departments, reinforcing instrument adoption. Integration with laboratory automation, data management, and high-throughput platforms further enhances efficiency. Hospitals also benefit from consistent supply of reagents and consumables, supporting sustained PCR usage. Government initiatives promoting hospital-based molecular diagnostics further strengthen the segment’s dominance.

The Diagnostic Centers segment is expected to witness the fastest growth from 2026 to 2033, driven by the expansion of private diagnostic laboratories, increasing outsourcing of molecular testing, and rising demand for accessible testing in urban and semi-urban areas. Centers in India, Southeast Asia, and South Korea are rapidly adopting PCR technologies for infectious disease testing, oncology screening, and prenatal diagnostics. The growth is further fueled by partnerships with hospitals and research institutes, as well as increasing government support for diagnostic testing programs. Smaller centers prefer modular q‑PCR and d‑PCR platforms that offer scalability and cost-efficiency. Rising awareness of molecular diagnostics among patients and clinicians is driving adoption in these decentralized testing facilities.

Asia-Pacific q-PCR and d-PCR Devices Market Regional Analysis

- China dominated the Asia‑Pacific q‑PCR and d‑PCR devices market with the largest revenue share of 38.5% in 2025, characterized by advanced healthcare infrastructure, strong government support for biotech research, and the presence of leading industry players

- Laboratories and hospitals in the region highly value the accuracy, rapid results, and high-throughput capabilities offered by q‑PCR and d‑PCR devices, which support clinical diagnostics, infectious disease testing, and research applications

- This widespread adoption is further supported by advanced laboratory automation, availability of skilled personnel, and collaborations between hospitals, research institutions, and pharmaceutical companies, establishing PCR technologies as a preferred choice across both clinical and research settings

The China q‑PCR and d‑PCR Devices Market Insight

The China q‑PCR and d‑PCR devices market captured the largest revenue share of 38.5% in 2025, driven by strong government initiatives in molecular diagnostics, robust healthcare infrastructure, and substantial investment in genomics and biotechnology research. Clinical laboratories and hospitals are rapidly adopting high-throughput PCR platforms for infectious disease testing, oncology screening, and genetic disorder analysis. The growing integration of automated PCR workflows with laboratory information management systems enhances operational efficiency and accuracy. Furthermore, China’s emphasis on precision medicine and public health surveillance fuels demand for both q‑PCR and d‑PCR technologies. Domestic manufacturers and research institutes are also contributing to market growth by developing cost-effective solutions. The increasing focus on pandemic preparedness and rapid testing capabilities continues to expand the market.

Japan q‑PCR and d‑PCR Devices Market Insight

The Japan q‑PCR and d‑PCR devices market is gaining momentum, supported by advanced healthcare infrastructure, a technologically inclined population, and high adoption of molecular diagnostics in both clinical and research settings. Japanese laboratories emphasize accuracy, reproducibility, and rapid turnaround times for diagnostics, driving demand for automated and high-throughput PCR systems. Integration of PCR platforms with other laboratory technologies, including next-generation sequencing workflows, enhances research productivity. The country’s aging population and focus on personalized medicine further support the adoption of advanced PCR technologies. In addition, strong government funding for genomics research and infectious disease monitoring contributes to market expansion. Laboratories in Japan increasingly rely on PCR devices for both routine diagnostics and specialized research applications.

India q‑PCR and d‑PCR Devices Market Insight

The India q‑PCR and d‑PCR devices market accounted for the largest growth potential in Asia‑Pacific in 2025, driven by increasing healthcare expenditure, rising awareness of molecular diagnostics, and the expansion of research and diagnostic laboratories. Rapid urbanization, growing infectious disease testing programs, and the establishment of smart laboratory infrastructure are key growth factors. India’s emphasis on genomic research, clinical trials, and precision medicine supports the adoption of high-throughput q‑PCR and digital PCR platforms. The availability of affordable devices and reagents from domestic and international suppliers further propels market expansion. Government initiatives promoting biotechnology and molecular diagnostics enhance market penetration. Increasing collaborations between hospitals, diagnostic centers, and academic institutions also drive adoption across multiple applications.

South Korea q‑PCR and d‑PCR Devices Market Insight

The South Korea q‑PCR and d‑PCR devices market is expected to grow at a substantial CAGR, driven by advanced healthcare infrastructure, widespread adoption of molecular diagnostics, and strong investments in genomics and biotech research. Korean laboratories prioritize high-throughput PCR technologies for oncology, infectious disease testing, and precision medicine research. Integration with automated workflows and digital data management systems enhances efficiency and reproducibility. The country’s focus on innovative diagnostic solutions and regulatory support for molecular testing further supports market expansion. In addition, private research institutes and pharmaceutical companies are increasingly adopting q‑PCR and d‑PCR platforms for biomarker discovery and drug development. Rising demand for rapid, accurate testing in both clinical and research settings is driving continued growth

Asia-Pacific q-PCR and d-PCR Devices Market Share

The Asia-Pacific q-PCR and d-PCR Devices industry is primarily led by well-established companies, including:

- Thermo Fisher Scientific Inc., (U.S.)

- Bio Rad Laboratories, Inc., (U.S.)

- QIAGEN (Netherlands)

- Takara Bio Inc., (Japan)

- Agilent Technologies, Inc., (U.S.)

- F. Hoffmann La Roche Ltd., (Switzerland)

- Abbott (U.S.)

- Danaher (U.S.)

- Merck KGaA, (Germany)

- BD (U.S.)

- Promega Corporation, (U.S.)

- Analytik Jena GmbH+Co. KG, (Germany)

- Standard BioTools Inc., (U.S.)

- Genome Diagnostics Pvt Ltd, (India)

- Lepu Medical Technology Beijing Co Ltd, (China)

- Fluidigm Corporation (U.S.)

- PerkinElmer Inc., (U.S.)

- Seegene, Inc., (South Korea)

- Illumina, Inc., (U.S.)

- BIONEER CORPORATION (South Korea)

What are the Recent Developments in Asia-Pacific q-PCR and d-PCR Devices Market?

- In November 2024, Takara Bio’s SmartChip ND Real‑Time PCR System was further highlighted publicly at scientific and industry events as an innovation advancing clinical research and AMR monitoring, reinforcing its strategic role in polymerase chain reaction workflows across Asia‑Pacific labs

- In September 2024, Takara Bio USA, Inc., a subsidiary of Japan‑based Takara Bio, announced the launch of the SmartChip ND Real‑Time PCR System, a high‑throughput qPCR platform that supports broad surveillance of antimicrobial resistance with up to 5,184 reactions per chip and reduced reagent costs

- In May 2023, Thermo Fisher Scientific announced the launch of the Applied Biosystems™ QuantStudio™ Absolute Q™ AutoRun dPCR Suite, an automated digital PCR solution designed to simplify high‑throughput nucleic acid quantification and enable up to 72‑hour hands‑free operation suited for molecular research and diagnostics

- In March 2023, Thermo Fisher Scientific’s Applied Biosystems™ QuantStudio™ Absolute Q™ AutoRun dPCR Suite was also widely reported as a leading digital PCR automation solution that combines microfluidic dPCR with intelligent lab automation to enhance productivity for pharma and molecular biology researchers

- In January 2021, QIAGEN announced the launch of next‑generation digital PCR technology globally, with integration of advanced dPCR capabilities acquired through the FORMULATRIX platform, aimed at expanding its PCR product offerings and strengthening automated assay workflows used in research and clinical labs across the Asia‑Pacific region

- https://www.labx.com/resources/launch-of-the-applied-biosystems-quantstudio-absolute-q-autorun-dpcr-suite/3956

- https://www.takarabio.com/about/in-the-news/takara-bio-launches-high-throughput-cost-effective-qpcr-system-to-advance-clinical-research%3Fsrsltid%3DAfmBOoo-acES7pFf0V2ZaYHpEyFTJ7ALXWMsCim_Jj9sZyar3_1bGAyO

- https://healthcareasiamagazine.com/healthcare/news/heres-whats-driving-japans-pcr-systems-market

- https://www.technologynetworks.com/analysis/product-news/thermo-fisher-scientific-launches-new-digital-pcr-automation-solution-370708

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.