Asia Pacific Spinal Implants And Spinal Devices Market

Market Size in USD Billion

USD

3.31 Billion

USD

4.92 Billion

2024

2032

USD

3.31 Billion

USD

4.92 Billion

2024

2032

| 2025 - 2032 | |

| USD 3.31 Billion | |

| USD 4.92 Billion | |

| % | |

|

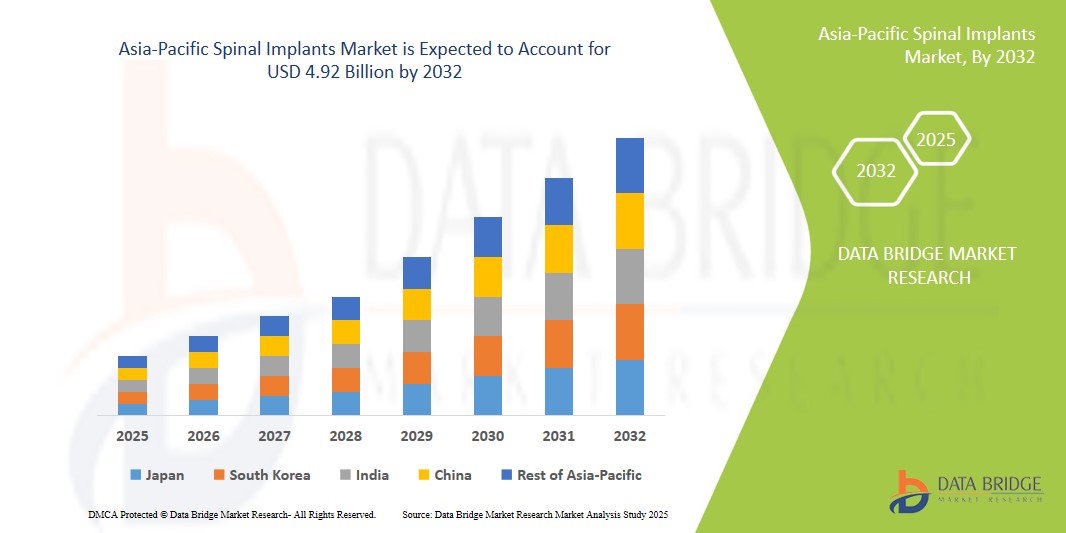

Spinal Implants Market Size

- The Asia-Pacific spinal implants market size was valued at USD 3.31 billion in 2024 and is expected to reach USD 4.92 billion by 2032, at a CAGR of 5.10% during the forecast period

- This growth is driven by factors such as the increasing prevalence of spinal disorders, advancements in minimally invasive surgical techniques, the rising aging population, and technological innovations in spinal implant materials and designs

Spinal Implants Market Analysis

- Spinal implants, crucial in spinal surgeries, enhance fusion, stability, and correct deformities.

- Constructed from metals such as stainless steel or titanium, they offer varied sizes and types including hooks, cages, screws, plates, and rods. Ongoing research aims to refine implant efficacy, advancing treatment outcomes in spinal interventions.

- China is expected to dominate the spinal implants market with 17.9% due to substantial geriatric population and rapid technological advancements in healthcare

- India is expected to be the fastest growing region in the spinal implants market during the forecast period due to increasing healthcare investments and technological advancements

- The fusion devices segment is expected to dominate the market with a market share with 57.9% due to adoption of spinal fusion surgeries, which are commonly performed to treat conditions such as degenerative disc disease and spinal instability

Report Scope and Spinal Implants Market Segmentation

|

Attributes |

Spinal Implants Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Spinal Implants Market Trends

“Integration of Artificial Intelligence (AI) in Minimally Invasive Spine Surgery”

- The Asia-Pacific region is witnessing a significant shift towards minimally invasive spine surgeries, driven by advancements in AI technologies

- AI is being utilized to enhance surgical precision, predict patient outcomes, and personalize treatment plans, thereby improving the overall effectiveness of spinal procedures

- Countries such as Japan, China, and India are leading the adoption of AI in spine surgery, with healthcare providers investing in AI-driven surgical systems and training programs for medical professionals

- The integration of AI is also facilitating the development of robotic-assisted surgeries, enabling surgeons to perform complex spinal procedures with greater accuracy and reduced risk of complications

- This technological advancement is reshaping the landscape of spinal interventions in the region

Spinal Implants Market Dynamics

Driver

“Increasing Prevalence of Spinal Disorders”

- The Asia-Pacific region is experiencing a rise in spinal disorders due to factors such as aging populations, sedentary lifestyles, and increasing obesity rates

- Conditions such as degenerative disc disease, scoliosis, and spinal injuries are becoming more prevalent, leading to a higher demand for spinal implants and surgical interventions

- Countries such as India and China are witnessing a surge in spinal disorder cases, prompting healthcare systems to enhance their capabilities in spinal care

- This includes expanding access to spinal implants and improving surgical facilities to meet the growing demand

- The increasing incidence of spinal disorders is also influencing healthcare policies, with governments allocating more resources towards spinal healthcare services and infrastructure development

Opportunity

“Growth of Medical Tourism in Spinal Treatments”

- Asia-Pacific countries, particularly India and Thailand, are becoming popular destinations for medical tourism, offering high-quality spinal treatments at competitive prices

- This trend is attracting patients from developed countries seeking affordable and effective spinal care

- The availability of advanced spinal surgical procedures, coupled with state-of-the-art medical facilities and experienced healthcare professionals, is enhancing the region's appeal as a medical tourism hub.

- Governments are supporting this growth by implementing policies that promote medical tourism, such as streamlining visa processes and accrediting healthcare institutions to international standards

Restraint/Challenge

“High Cost of Advanced Spinal Implants”

- The adoption of advanced spinal implants, including those made from materials such as titanium and PEEK, is hindered by their high costs

- These expenses can limit access to cutting-edge treatments, especially in lower-income regions within the Asia-Pacific area

- Insurance coverage for spinal implant procedures varies across countries, with some patients facing out-of-pocket expenses that make treatments unaffordable

- The high cost of implants also affects healthcare providers, particularly in developing nations, as they may struggle to procure and maintain advanced spinal devices, impacting the overall quality of care

- Efforts are being made to address this challenge through the development of cost-effective implant alternatives and the implementation of government subsidies to make spinal treatments more accessible

Spinal Implants Market Scope

The market is segmented on the basis of product, materials, application, indication, technology, surgery type, end user, and distribution channel.

|

Segmentation |

Sub-Segmentation |

|

By Product |

|

|

By Material |

|

|

By Application |

|

|

By Indication |

|

|

By Technology |

|

|

By Surgery Type |

|

|

By End User |

|

|

By Distribution Channel |

|

In 2025, the fusion devices is projected to dominate the market with a largest share in product segment

The fusion devices segment is expected to dominate the spinal implants market with the largest share with 58.9% in 2025 due to adoption of spinal fusion surgeries, which are commonly performed to treat conditions such as degenerative disc disease and spinal instability. The development of innovative fusion technologies, such as 3D-printed interbody cages and biologically active implants, has enhanced the effectiveness and safety of spinal fusion procedures.

The Vertebral Compression Fracture (VCF) Treatment Devices is expected to account for the largest share during the forecast period in technology market

In 2025, the Vertebral Compression Fracture (VCF) Treatment Devices segment is expected to dominate the market with the largest market share due increasing incidence of osteoporosis-related fractures and the preference for minimally invasive treatment options. The development of more precise and user-friendly instruments, have improved treatment outcomes and patient satisfaction, further driving market growth

Spinal Implants Market Regional Analysis

“China Holds the Largest Share in the Spinal Implants Market”

- China holds the largest market share in the Asia-Pacific spinal implants sector with 19.9%, driven by its substantial geriatric population and rapid technological advancements in healthcare

- The country boasts a vast network of medical facilities, including over 2,000 hospitals offering spinal surgeries, with at least 500 specializing in complex procedures such as microscopic spine surgery

- China's government has been actively investing in healthcare infrastructure, aiming to enhance the accessibility and quality of spinal care services across the nation

- The integration of advanced medical technologies and the adoption of minimally invasive surgical techniques have further strengthened China's position in the spinal implants market

- With ongoing developments and investments, China is expected to maintain its dominance in the Asia-Pacific spinal implants market in the foreseeable future

“India is Projected to Register the Highest CAGR in the Spinal Implants Market”

- India is experiencing the highest growth rate in the Asia-Pacific spinal implants market,

- The rising prevalence of spinal disorders and deformities is driving the demand for spinal implants and devices in the country

- Significant investments in healthcare infrastructure and the establishment of new manufacturing facilities are contributing to the market's growth

- The adoption of advanced spinal implant technologies and the presence of world-class medical professionals are enhancing treatment outcomes

- India's reputation as a hub for medical tourism, offering high-quality spinal treatments at competitive prices, is attracting patients from across the globe

Spinal Implants Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, Asia-Pacific presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Medtronic (U.S.)

- Canwell Medical Co., Ltd. (China)

- NuVasive, Inc. (U.S.)

- SeaSpine (U.S.)

- Globus Medical (U.S.)

- RTI Surgical (U.S.)

- MW Industries (U.S.)

- Captiva Spine, Inc. (U.S.)

- XTANT MEDICAL (U.S.)

- SINTX Technologies, Inc. (U.S.)

- Orthofix Medical, Inc. (U.S.)

- Alphatec Spine, Inc. (U.S.)

- Wenzel Spine (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Tecomet, Inc. (U.S.)

- Stryker (U.S.)

- Zimmer Biomet (U.S.)

Latest Developments in Asia-Pacific Spinal Implants Market

- In January 2024, Accelus, a medical technology firm headquartered in the U.S., launched the Linesider Modular-Cortical System, a solution for spinal implant operations designed to improve the accuracy and effectiveness of spinal implant surgeries. It allows for the early insertion of screw shanks during the surgical process and provides the flexibility to tailor the surgical construct with modular tulips and rods. The system is adaptable to various surgical techniques in both cortical and open modular configurations.

- In April 2024, Proprio introduced a multi-phase partnership with the Biedermann Group, a distinguished innovator in cutting-edge spinal procedural solutions and implant systems. The partnership aims to combine Biedermann’s innovative spinal implants with Proprio’s Paradigm system, which utilizes artificial intelligence, computer vision, and augmented reality to offer exceptional real-time visualization and guidance during surgical procedures.

- In October 2023, Johnson & Johnson MedTech announced that DePuy Synthes, a division of Johnson & Johnson specializing in orthopedic products, has obtained 510(k) clearances from the U.S. FDA for both the TriALTIS Spine System and the TriALTIS Navigation Enabled Instruments. The TriALTIS Spine System is an advanced system of pedicle screws designed for the posterior thoracolumbar region, offering a wide array of implant choices and sophisticated instrumentation.

- In September 2023, Silony Medical International AG acquired Centinel Spine’s Global Fusion Business. This strategic move combined Silony’s existing posterior screw & rod fusion systems with Centinel Spine’s Fusion Products, including cervical stand-alone cages, lateral stand-alone cages, anterior cervical plates, and ALIF devices. The acquisition improved Silony’s technological capabilities and geographic footprint, enabling the company to offer a comprehensive range of spinal fusion solutions for both open and minimally invasive procedures.

- In January 2023, Companion Spine acquired Backbone SAS. With the addition of Backbone's primary medical device, the LISA implant, the acquisition expanded companies offering medical implant solutions. Due to this acquisition, Companion Spine can provide a full range of therapy options for spine diseases, including lumbar stenosis and degenerative disc disease, by matching implants to the disease's severity.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.