Asia Pacific Transplant Diagnostics Market

Market Size in USD Billion

USD

1.43 Billion

USD

2.66 Billion

2025

2033

USD

1.43 Billion

USD

2.66 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.43 Billion | |

| USD 2.66 Billion | |

| % | |

|

Asia-Pacific Transplant Diagnostics Market Size

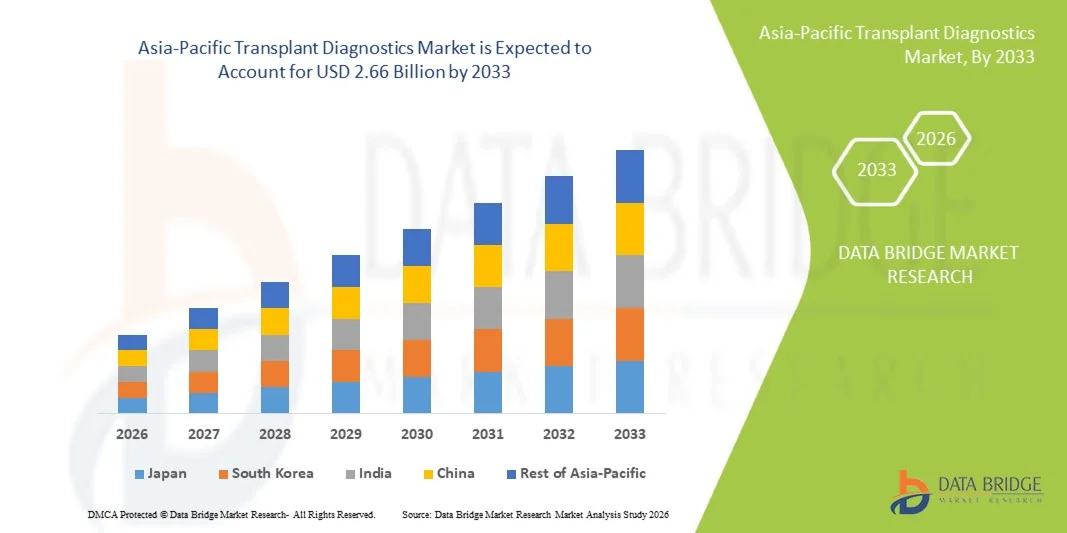

- The Asia-Pacific transplant diagnostics market size was valued at USD 1.43 billion in 2025 and is expected to reach USD 2.66 billion by 2033, at a CAGR of 8.1% during the forecast period

- The market growth is largely fueled by the increasing number of organ transplant procedures across the region, coupled with the rising prevalence of chronic diseases such as kidney failure, liver disorders, and cardiovascular conditions, which is driving demand for accurate donor–recipient compatibility testing

- Furthermore, expanding healthcare infrastructure, growing investments in advanced molecular diagnostics technologies, and increasing awareness regarding organ donation and transplantation are enhancing the adoption of transplant diagnostics solutions in both developed and emerging Asia-Pacific economies, thereby significantly supporting the industry's growth

Asia-Pacific Transplant Diagnostics Market Analysis

- Transplant diagnostics, encompassing molecular and immunological testing methods for donor–recipient compatibility assessment, are increasingly critical in modern healthcare due to their role in improving transplant success rates, reducing rejection risks, and supporting personalized medicine approaches in organ transplantation procedures

- The escalating demand for transplant diagnostics is primarily fueled by the rising incidence of chronic diseases leading to organ failure, growing organ transplant volumes, and increasing awareness among healthcare providers regarding advanced compatibility testing techniques such as HLA typing and crossmatching

- China dominated the transplant diagnostics market with the largest revenue share of 35.7% in 2025, supported by a high volume of transplant procedures, strong investments in healthcare modernization, and the presence of advanced laboratory networks

- India is expected to witness the fastest growth in the transplant diagnostics market during the forecast period driven by expanding healthcare infrastructure, increasing government initiatives to promote organ donation, and rising adoption of advanced diagnostic technologies across major urban healthcare centers

- The PCR-Based Molecular Assays segment dominated the transplant diagnostics market with a significant market share of 52.3% in 2025, driven by its high accuracy, ability to provide detailed genetic compatibility insights, and increasing integration of next-generation sequencing (NGS) technologies in transplant compatibility testing workflows

Report Scope and Asia-Pacific Transplant Diagnostics Market Segmentation

|

Attributes |

Asia-Pacific Transplant Diagnostics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Asia-Pacific Transplant Diagnostics Market Trends

“Advancements in Molecular Testing and Precision Diagnostics”

- A significant and accelerating trend in the Asia-Pacific transplant diagnostics market is the increasing adoption of advanced molecular testing technologies such as next-generation sequencing (NGS), PCR-based assays, and high-resolution HLA typing, which are enhancing accuracy and efficiency in donor–recipient compatibility assessment

- For instance, Illumina platforms and Thermo Fisher Scientific solutions are widely utilized in advanced laboratories across countries such as China and India to support high-throughput genomic analysis for transplant compatibility testing

- Integration of digital pathology and laboratory automation is enabling faster turnaround times and improved workflow efficiency in transplant laboratories, while AI-assisted data interpretation tools are helping clinicians make more precise compatibility and risk assessments

- The growing integration of transplant diagnostics with centralized laboratory networks and hospital information systems is facilitating seamless data sharing, enabling better coordination between transplant centers and diagnostic labs across urban healthcare ecosystems

- This trend toward more precise, technology-driven, and data-integrated diagnostic solutions is reshaping clinical expectations in transplantation, with companies such as Qiagen and Bio-Rad expanding their molecular diagnostic portfolios to support transplant applications in the region

- The demand for advanced transplant diagnostics leveraging molecular platforms is growing rapidly across both public and private healthcare sectors, as increasing transplant volumes and clinical demand for accurate compatibility testing continue to drive adoption

- In addition, the rising adoption of cloud-based laboratory information systems (LIS) is improving data management, interoperability, and remote access to diagnostic results, thereby enhancing efficiency in transplant workflows across multi-center healthcare networks

Asia-Pacific Transplant Diagnostics Market Dynamics

Driver

“Rising Transplant Procedures and Expanding Healthcare Infrastructure”

- The increasing prevalence of end-stage organ diseases, coupled with a growing number of organ transplant procedures across Asia-Pacific, is a significant driver for the heightened demand for transplant diagnostics

- For instance, in 2024, the National Organ and Tissue Transplant Organization (NOTTO) in India reported continued growth in organ transplant registrations and procedures, reflecting rising awareness and system development in transplant care

- As healthcare systems modernize and expand, transplant centers are increasingly adopting advanced diagnostic tools such as HLA typing, crossmatching, and molecular assays to improve transplant success rates and reduce rejection risks

- Furthermore, government initiatives promoting organ donation awareness and improving transplant infrastructure are encouraging hospitals and diagnostic laboratories to invest in advanced transplant diagnostic technologies

- The growing accessibility of specialized diagnostic services, combined with increasing collaboration between hospitals and diagnostic companies, is driving the integration of transplant diagnostics into routine clinical workflows in both developed and emerging economies

- The rising need for accurate, timely, and reliable compatibility testing in complex transplant procedures is a key factor propelling the adoption of transplant diagnostics across the region

- Increasing investments by public and private healthcare providers in expanding transplant centers and upgrading laboratory capabilities are further strengthening the diagnostic ecosystem

- In addition, the growing involvement of international diagnostic firms and research collaborations is enhancing technology transfer and improving access to advanced transplant testing solutions across the region

Restraint/Challenge

“High Cost of Advanced Diagnostics and Limited Awareness”

- Concerns surrounding the high cost of advanced transplant diagnostic technologies and limited reimbursement coverage in certain countries pose a significant challenge to broader market penetration

- For instance, in several developing economies across Asia-Pacific, the cost of molecular assays such as next-generation sequencing and high-resolution HLA typing can limit accessibility for smaller hospitals and price-sensitive patients

- Addressing affordability challenges through cost-effective diagnostic solutions and localized manufacturing is crucial for improving adoption, while leading companies such as Roche and Thermo Fisher Scientific emphasize scalable platforms to support broader access

- In addition, limited awareness among patients and healthcare providers in certain regions regarding the importance of advanced compatibility testing can delay diagnosis and restrict the uptake of transplant diagnostics

- While awareness is gradually improving through government programs and healthcare initiatives, disparities in infrastructure and expertise between urban and rural areas continue to impact market growth

- Overcoming these challenges through increased healthcare investment, awareness programs, and development of affordable diagnostic technologies will be vital for sustained growth of the transplant diagnostics market in Asia-Pacific

- Limited availability of skilled professionals trained in advanced molecular and immunological testing techniques further constrains the efficient adoption of transplant diagnostics in some countries

- Moreover, variability in regulatory frameworks across different Asia-Pacific countries can slow down the approval and standardization of advanced diagnostic technologies, creating additional barriers for market expansion

Asia-Pacific Transplant Diagnostics Market Scope

The market is segmented on the basis of product type, technology, transplant type, application, end user, and distribution channel.

- By Product Type

On the basis of product type, the transplant diagnostics market is segmented into transplant diagnostic instruments, transplant diagnostic software, and transplant diagnostic reagents. The transplant diagnostic reagents segment dominated the market with the largest revenue share in 2025, driven by their extensive use in routine compatibility testing procedures such as HLA typing, crossmatching, and molecular assays. Reagents are essential consumables in every transplant diagnostic workflow, ensuring recurring demand across laboratories and hospitals. Their widespread adoption is supported by the increasing number of transplant procedures and the need for consistent and accurate test results. In addition, continuous product innovation and availability of standardized reagent kits from major players further strengthen this segment’s dominance.

The transplant diagnostic software segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the increasing digitalization of laboratories and the adoption of advanced data analytics in transplant diagnostics. Software solutions enable efficient data management, result interpretation, and integration with laboratory information systems, improving workflow efficiency. The growing use of AI-driven platforms for HLA data analysis and donor-recipient matching is further accelerating demand. Rising investments in healthcare IT infrastructure across Asia-Pacific countries are also contributing to the rapid expansion of this segment.

- By Technology

On the basis of technology, the transplant diagnostics market is segmented into PCR-based molecular assays and sequencing-based molecular assays. The PCR-based molecular assays segment dominated the market with the largest revenue share of 52.3% in 2025, attributed to their cost-effectiveness, high reliability, and widespread adoption in clinical laboratories. PCR technologies are extensively used for HLA typing and pathogen detection due to their proven accuracy and relatively shorter turnaround time. Their established presence in both developed and emerging healthcare systems makes them a preferred choice for routine transplant compatibility testing.

The sequencing-based molecular assays segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing adoption of next-generation sequencing (NGS) technologies for high-resolution genetic analysis. Sequencing-based methods provide deeper insights into genetic compatibility, improving transplant outcomes and reducing rejection risks. Growing demand for precision medicine and advancements in sequencing platforms are further supporting segment growth. Increasing investments in genomic research and expanding use of NGS in transplant centers across major Asia-Pacific countries are accelerating adoption.

- By Transplant Type

On the basis of transplant type, the market is segmented into solid organ transplantation, stem cell transplantation, soft tissue transplantation, bone marrow transplantation, and others. The solid organ transplantation segment dominated the market with the largest revenue share in 2025, driven by the high volume of kidney, liver, and heart transplant procedures across the region. Rising prevalence of chronic diseases such as kidney failure and liver disorders is significantly contributing to the demand for transplant diagnostics in this segment. Solid organ transplants require stringent compatibility testing, increasing reliance on advanced diagnostic techniques.

The stem cell transplantation segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing use of stem cell therapies in treating hematological disorders and cancers. Advances in regenerative medicine and expanding clinical applications of stem cell transplantation are driving demand for compatibility testing. Growing research activities and clinical trials in countries such as China, Japan, and India are further supporting segment expansion. Improved awareness and adoption of minimally invasive transplant procedures are also contributing to the growth of this segment.

- By Application

On the basis of application, the transplant diagnostics market is segmented into diagnostic applications and research applications. The diagnostic applications segment dominated the market with the largest revenue share in 2025, driven by the critical role of transplant diagnostics in pre-transplant compatibility testing and post-transplant monitoring. Hospitals and transplant centers heavily rely on diagnostic testing to ensure successful transplantation outcomes and minimize rejection risks. Increasing transplant volumes and growing demand for accurate and timely diagnostic results are further strengthening this segment.

The research applications segment is expected to witness the fastest growth rate from 2026 to 2033, supported by increasing investments in transplant-related research and advancements in molecular biology. Academic institutions and research laboratories are increasingly utilizing transplant diagnostics tools to study genetic compatibility, immune response, and transplant rejection mechanisms. Expanding government funding for biomedical research and growing collaboration between research institutes and diagnostic companies are accelerating innovation. The rising focus on developing personalized transplant solutions is also contributing to segment growth.

- By End User

On the basis of end user, the market is segmented into research laboratories and academic institutes, hospital and transplant centers, commercial service providers, and others. The hospital and transplant centers segment dominated the market with the largest revenue share in 2025, driven by the high concentration of transplant procedures performed in these facilities. These centers require advanced diagnostic solutions for pre- and post-transplant testing, making them the primary consumers of transplant diagnostics products. Increasing investments in hospital infrastructure and expansion of specialized transplant units are further supporting segment dominance.

The commercial service providers segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the outsourcing of diagnostic services to specialized laboratories. These providers offer cost-effective, high-quality testing services to hospitals and clinics lacking in-house diagnostic capabilities. The growing trend of centralized testing facilities and increasing demand for specialized molecular diagnostics are driving this segment. Expansion of private diagnostic chains and partnerships with healthcare providers are also contributing to rapid growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, retail sales, and others. The direct tender segment dominated the market with the largest revenue share in 2025, driven by bulk procurement of transplant diagnostic products by hospitals, government healthcare systems, and large transplant centers. Direct tenders ensure cost efficiency, standardized supply, and long-term contracts with suppliers, making them the preferred procurement method in institutional settings. Increasing government involvement in healthcare procurement across Asia-Pacific further supports this segment.

The retail sales segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing availability of diagnostic kits and reagents through distributors, online platforms, and specialty suppliers. Smaller laboratories and private clinics often rely on retail channels for flexible and timely procurement. Growing penetration of e-commerce platforms and expansion of distribution networks by key manufacturers are further accelerating segment growth. Rising demand for quick access to diagnostic products in emerging markets is also contributing to this trend.

Asia-Pacific Transplant Diagnostics Market Regional Analysis

- China dominated the transplant diagnostics market with the largest revenue share of 35.7% in 2025, supported by a high volume of transplant procedures, strong investments in healthcare modernization, and the presence of advanced laboratory networks

- Healthcare providers in the country are increasingly adopting advanced transplant diagnostic technologies such as HLA typing, crossmatching, and next-generation sequencing to improve transplant compatibility and clinical outcomes

- This widespread adoption is further supported by expanding laboratory infrastructure, increasing investments in molecular diagnostics, and growing awareness of organ donation and transplant procedures, establishing transplant diagnostics as a key component of the country’s healthcare system

The China Transplant Diagnostics Market Insight

China dominated the Asia-Pacific transplant diagnostics market with the largest revenue share in 2025, driven by a high volume of organ transplant procedures and strong investments in healthcare modernization. The country’s expanding network of advanced hospitals and diagnostic laboratories is accelerating the adoption of transplant compatibility testing solutions. Increasing use of technologies such as HLA typing, crossmatching, and next-generation sequencing is improving transplant success rates. Government initiatives supporting organ donation awareness and infrastructure development are further strengthening market growth. In addition, the presence of established domestic and international diagnostic companies is enhancing accessibility to advanced transplant diagnostics across the country.

Japan Transplant Diagnostics Market Insight

The Japan transplant diagnostics market is experiencing steady growth, supported by the country’s advanced healthcare system and strong focus on precision medicine. High standards of clinical care and widespread adoption of molecular diagnostic technologies are driving demand for accurate compatibility testing. The aging population and increasing incidence of organ failure are contributing to the need for transplant procedures and associated diagnostics. Integration of automated laboratory systems and advanced sequencing platforms is improving efficiency and turnaround times. Furthermore, continuous research and development activities in transplant immunology are supporting innovation in diagnostic solutions across clinical and academic settings.

India Transplant Diagnostics Market Insight

The India transplant diagnostics market accounted for a significant revenue share in Asia Pacific in 2025, driven by rapid urbanization, a growing patient population, and increasing awareness of organ transplantation. The expansion of healthcare infrastructure and rising number of transplant centers are supporting the adoption of advanced diagnostic technologies. Increasing prevalence of chronic diseases such as kidney and liver disorders is fueling demand for compatibility testing. Government initiatives promoting organ donation and transplant programs are further contributing to market growth. In addition, the availability of cost-effective diagnostic solutions and growing participation of private healthcare providers are enhancing access to transplant diagnostics across the country.

South Korea Transplant Diagnostics Market Insight

The South Korea transplant diagnostics market is witnessing steady growth, supported by a well-developed healthcare system and increasing adoption of advanced medical technologies. The country’s strong emphasis on precision diagnostics and digital healthcare integration is driving the use of molecular transplant testing solutions. Rising cases of chronic diseases and increasing transplant procedures are contributing to the demand for compatibility testing. Advanced laboratory infrastructure and high penetration of next-generation sequencing technologies are improving diagnostic accuracy and efficiency. Furthermore, continuous government support for healthcare innovation and research is fostering advancements in transplant diagnostics across hospitals and specialized diagnostic centers.

Asia-Pacific Transplant Diagnostics Market Share

The Asia-Pacific Transplant Diagnostics industry is primarily led by well-established companies, including:

- QIAGEN (Netherlands)

- Thermo Fisher Scientific Inc. (U.S.)

- BIOMÉRIEUX (France)

- CareDx, Inc. (U.S.)

- Luminex Corporation (U.S.)

- BD (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- Illumina, Inc. (U.S.)

- Abbott Laboratories (U.S.)

- Immucor Transplant Diagnostics, Inc. (U.S.)

- GenDx (Netherlands)

- Siemens Healthineers AG (Germany)

- Danaher (U.S.)

- Sysmex Corporation (Japan)

- Hologic, Inc. (U.S.)

- Bruker Corporation (U.S.)

- Werfen Group (Spain)

- Diasorin S.p.A. (Italy)

- Seegene, Inc. (South Korea)

What are the Recent Developments in Asia-Pacific Transplant Diagnostics Market?

- In March 2026, Insight Molecular Diagnostics Inc. submitted its GraftAssureDx™ transplant rejection diagnostic test for FDA review, marking a key regulatory milestone toward clinical availability in the U.S. This submission follows favorable head-to-head data and aims to expand decentralized molecular testing for kidney transplant rejection while targeting additional regulatory clearances in the U.K. and EU

- In March 2026, a second study affirmed the superiority of Insight Molecular Diagnostics’ GraftAssure assay’s proprietary dd-cfDNA combination model score, supporting commercialization efforts with robust clinical evidence from a multi-center study involving biopsy-matched patients, advancing non-invasive transplant rejection diagnostics

- In March 2026, Insight Molecular Diagnostics also completed major clinical and quality milestones for its GraftAssureDx test kit, including a reproducibility study across three major transplant centers and ISO 13485 certification, enabling planned regulatory submissions in the U.S., U.K., and Europe

- In January 2026, CareDx, Inc. announced a collaboration with 10x Genomics to launch ImmuneScape™, a multi-omics research platform designed to decode transplant rejection mechanisms and drug response, aiming to accelerate discovery and precision diagnostics in transplant care globally

- In October 2025, Thermo Fisher Scientific introduced a new molecular diagnostic system designed to aid evaluation of lung transplant rejection in post-transplant biopsies, reflecting ongoing innovation in transplant diagnostics technology for clinical pathology labs

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.