Europe Biodegradable Paper Plastic Packaging Market

Market Size in USD Billion

USD

1.93 Billion

USD

3.51 Billion

2025

2033

USD

1.93 Billion

USD

3.51 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.93 Billion | |

| USD 3.51 Billion | |

| % | |

|

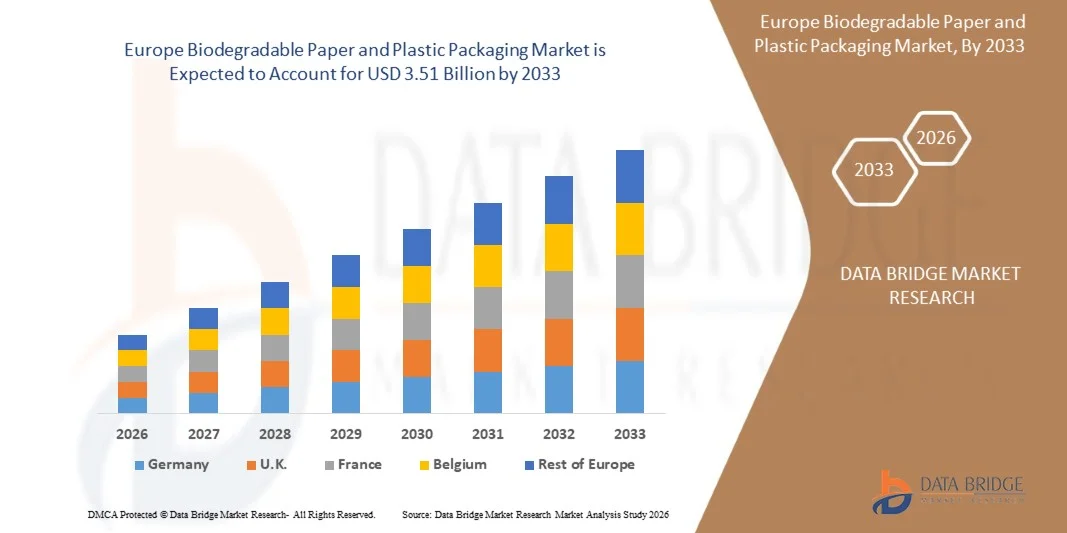

Europe Biodegradable Paper and Plastic Packaging Market Size

- The Europe Biodegradable Paper and Plastic Packaging Market size was valued at USD 1.93 billion in 2025 and is expected to reach USD 3.51 billion by 2033, at a CAGR of 7.8% during the forecast period

- The market growth is largely fueled by the increasing global shift toward sustainable packaging solutions driven by strict environmental regulations on single-use plastics and rising corporate commitments to carbon neutrality

- Furthermore, rising consumer awareness regarding environmental pollution and growing preference for eco-friendly and compostable packaging materials are encouraging brands to transition toward bio-based packaging formats

Europe Biodegradable Paper and Plastic Packaging Market Analysis

- Biodegradable paper and plastic packaging refers to packaging materials derived from renewable sources such as plant fibers, starch, and biopolymers that can naturally decompose under composting or environmental conditions without leaving harmful residues. These materials are widely used in food packaging, retail bags, e-commerce packaging, and disposable product applications due to their eco-friendly properties and regulatory compliance benefits

- The escalating demand for biodegradable packaging is primarily fueled by the rapid expansion of the e-commerce sector, increasing adoption of circular economy practices, and strong investments in bio-based material innovation. Growing focus on reducing landfill waste and plastic pollution is further strengthening the shift toward sustainable packaging alternatives across global supply chains

- Germany dominated the Europe Biodegradable Paper and Plastic Packaging Market in 2025, due to its strong packaging manufacturing base, strict environmental regulations, and early adoption of circular economy practices across industrial and consumer sectors

- K. is expected to be the fastest growing country in the Europe Biodegradable Paper and Plastic Packaging Market during the forecast period due to rapid growth in e-commerce, strong retail sustainability commitments, and increasing consumer preference for eco-friendly packaging solutions

- Plastic segment dominated the market with a market share of 65.28% in 2025, due to its cost efficiency, durability, and wide applicability across multiple packaging requirements in food service and retail sectors. Manufacturers continue to prefer biodegradable plastic variants due to their flexibility, moisture resistance, and scalability in mass production

Report Scope and Europe Biodegradable Paper and Plastic Packaging Market Segmentation

|

Attributes |

Biodegradable Paper and Plastic Packaging Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe |

|

Key Market Players |

· Smurfit Kappa (Ireland) · DS Smith (U.K.) · Tetra Pak (Switzerland) · Mondi (U.K.) · International Paper (U.S.) · VPK Group (Belgium) · Sonoco Products Company (U.S.) · STOROPACK HANS REICHENECKER GMBH (Germany) · WestRock Company (U.S.) · Stora Enso (Finland) · Novamont S.p.A. (Italy) · OSQ (Poland) · BIO-LUTIONS International AG (Germany) · TIPA LTD (Israel) · BioApply (U.S.) · CPS Paper Products (India) · The Biodegradable Bag Company Ltd. (U.K.) |

|

Market Opportunities |

· Expansion of Sustainable E-commerce Packaging Demand Across Global Retail · Technological Advancements in Cost-Effective Biopolymer and Fiber-Based Packaging Solutions |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Europe Biodegradable Paper and Plastic Packaging Market Trends

“Rising Shift Toward Compostable and Bio-Based Packaging Materials”

- A significant trend in the Europe Biodegradable Paper and Plastic Packaging Market is the increasing transition toward compostable and bio-based materials, driven by the need to replace conventional petroleum-based plastics with sustainable alternatives across food, beverage, and consumer goods industries. This shift is strengthening the adoption of materials derived from renewable sources such as corn starch, sugarcane, and cellulose in packaging applications

- For instance, NatureWorks and Novamont are supplying bio-based polymers such as PLA and Mater-Bi that are widely used in compostable packaging formats adopted by global food service and retail brands. These materials are enabling companies to reduce environmental impact while maintaining packaging performance standards in terms of durability and usability

- The demand for sustainable packaging is expanding rapidly across global retail and quick-service restaurant chains as they increasingly replace single-use plastic packaging with biodegradable alternatives. This transformation is reinforcing circular economy practices and encouraging innovation in recyclable and compostable packaging formats

- The beverage industry is also integrating biodegradable paper-based cartons and molded fiber packaging solutions to reduce plastic dependency and improve recyclability. Companies such as Tetra Pak are actively advancing fiber-based packaging innovations to support lower carbon footprint packaging systems across global markets

- Manufacturers are investing in material science innovations to enhance barrier properties, moisture resistance, and shelf-life performance of biodegradable packaging solutions. This ongoing innovation is enabling broader adoption across industries that require both sustainability and functional packaging efficiency

Europe Biodegradable Paper and Plastic Packaging Market Dynamics

Driver

“Increasing Regulatory Restrictions on Single-Use Plastics Globally”

- The growing implementation of strict environmental regulations restricting single-use plastics is driving the demand for biodegradable paper and plastic packaging solutions across multiple industries. Governments are enforcing bans and usage limitations to reduce plastic pollution and accelerate the shift toward sustainable packaging alternatives

- For instance, the European Union Single-Use Plastics Directive and regulations under India’s Plastic Waste Management Rules are pushing companies such as Unilever to adopt compostable and recyclable packaging formats across their product portfolios. These regulatory frameworks are compelling manufacturers and brands to redesign packaging strategies in alignment with sustainability targets

- The food and beverage industry is rapidly adopting biodegradable packaging to comply with evolving regulatory standards while meeting consumer expectations for environmentally responsible products. This compliance-driven transition is accelerating the replacement of plastic packaging with paper-based and bio-derived alternatives

- Retail and e-commerce sectors are also increasing the use of biodegradable packaging materials to align with extended producer responsibility policies and waste reduction mandates. This is encouraging large-scale adoption of recyclable corrugated packaging and compostable mailers

- Many global corporations are committing to sustainability goals that include eliminating or significantly reducing virgin plastic usage in packaging systems. This strategic shift is reinforcing long-term demand for biodegradable packaging materials across global supply chains

Restraint/Challenge

“High Production Cost and Limited Scalability of Biodegradable Packaging Solutions”

- The Europe Biodegradable Paper and Plastic Packaging Market faces challenges due to higher production costs compared to conventional plastic packaging, primarily driven by expensive raw materials and specialized manufacturing processes. These cost pressures limit widespread adoption, particularly among price-sensitive markets and small-scale manufacturers

- For instance, Amcor and Mondi have invested heavily in sustainable packaging development, yet the transition toward large-scale biodegradable production continues to face cost-related constraints due to complex material sourcing and processing requirements. These challenges impact the ability to achieve price parity with traditional plastic packaging

- The limited availability of industrial composting infrastructure further restricts the scalability of biodegradable packaging solutions, reducing their effectiveness in certain regions. This infrastructure gap affects disposal efficiency and slows down widespread implementation of compostable packaging systems

- Manufacturing biodegradable packaging requires advanced technologies and controlled production environments to ensure material performance, durability, and compliance with environmental standards. These technical requirements increase operational complexity and production expenses

- The market continues to face difficulties in balancing cost efficiency with performance requirements, especially in high-volume applications such as FMCG and food delivery packaging. These constraints collectively limit rapid scaling and create barriers to full market penetration despite strong sustainability demand

Europe Biodegradable Paper and Plastic Packaging Market Scope

The market is segmented on the basis of packaging type, product, usage, distribution channel, application, packaging layer, and end-user.

- By Packaging Type

On the basis of packaging type, the Europe Biodegradable Paper and Plastic Packaging Market is segmented into plastic and paper. The plastic segment dominated the largest market revenue share of 65.28% in 2025, driven by its cost efficiency, durability, and wide applicability across multiple packaging requirements in food service and retail sectors. Manufacturers continue to prefer biodegradable plastic variants due to their flexibility, moisture resistance, and scalability in mass production. Existing processing infrastructure also supports faster adoption of plastic-based biodegradable solutions compared to alternatives. Strong compatibility with diverse product formats further reinforces its leading position in the market.

The paper segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rising environmental awareness and regulatory push toward reducing plastic dependency. Paper-based biodegradable packaging is gaining traction due to its recyclability, compostability, and improved consumer perception in sustainable branding. Innovations in coated and molded fiber paper solutions are expanding its use in food and consumer goods packaging. Increasing adoption by food delivery and retail brands is accelerating demand. Sustainability commitments by global companies are further supporting this growth trajectory.

- By Product

On the basis of product, the market is segmented into bags, baking sheets, paper plates, clamshell sandwich containers, portion cups, trays, cutlery, bowls, pouches and sachets, lidded containers, and others. The bags segment dominated the largest revenue share in 2025, driven by widespread usage in grocery retail, food delivery, and takeaway services. Their lightweight structure, cost-effectiveness, and adaptability to biodegradable materials make them highly preferred across multiple end-use industries. Retailers and food chains increasingly adopt eco-friendly bags to meet regulatory compliance and consumer sustainability expectations. High production scalability further strengthens their market leadership.

The clamshell sandwich containers segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising demand in quick-service restaurants and food delivery platforms. These containers offer strong structural integrity, food safety, and convenience for on-the-go consumption. Increasing preference for sustainable takeaway packaging solutions is accelerating their adoption. Innovation in molded fiber and compostable material technologies is improving performance and cost efficiency. Expanding urban food delivery ecosystems are further supporting segment growth.

- By Usage

On the basis of usage, the market is segmented into single-use and reusable packaging. The single-use segment dominated the largest market revenue share in 2025, driven by high consumption in food delivery, quick-service restaurants, and retail packaging applications. Its convenience, hygiene benefits, and low-cost production make it the preferred choice for large-scale packaging operations. Biodegradable innovations are increasingly replacing conventional plastics in single-use applications. Strong demand from urban consumption patterns continues to reinforce this dominance. Regulatory pressure on disposable plastics is also reshaping material choices within this segment.

The reusable segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by increasing sustainability initiatives and circular economy adoption. Businesses are investing in durable biodegradable materials designed for multiple-use cycles in logistics and retail systems. Growing consumer preference for eco-conscious packaging alternatives is further supporting adoption. Technological advancements in bio-based polymers are enhancing durability and lifecycle performance. Corporate sustainability commitments are accelerating the shift toward reusable packaging models.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into e-commerce, supermarkets/hypermarkets, convenience stores, specialty stores, and others. The supermarkets/hypermarkets segment dominated the largest revenue share in 2025, driven by high product availability, strong supplier networks, and bulk purchasing patterns. These retail formats provide extensive visibility for biodegradable packaging products across food and household categories. Established procurement systems and large-scale distribution efficiency further support their dominance. Consumer exposure to sustainable packaging options is also highest in these outlets.

The e-commerce segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by rapid expansion of online retail and food delivery services. Increasing digital purchasing behavior is driving demand for sustainable packaging solutions optimized for shipping and handling. E-commerce platforms are actively integrating eco-friendly packaging policies to meet sustainability goals. Growth in direct-to-consumer brands is further boosting adoption. Rising logistics efficiency and packaging innovation are accelerating segment expansion.

- By Application

On the basis of application, the market is segmented into food packaging, beverage packaging, pharmaceuticals packaging, personal & home care packaging, electronic appliance packaging, and others. The food packaging segment dominated the largest market revenue share in 2025, driven by high consumption across restaurants, retail, and delivery services. Increasing demand for sustainable packaging solutions in ready-to-eat and processed food categories is strengthening its position. Regulatory focus on reducing plastic waste in food contact materials is further supporting adoption. Strong consumer preference for eco-friendly food packaging is accelerating market penetration.

The pharmaceuticals packaging segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by rising demand for sustainable and compliant packaging solutions. Increasing environmental regulations in healthcare packaging are encouraging adoption of biodegradable alternatives. Growth in global pharmaceutical distribution networks is expanding application scope. Advanced material innovations are ensuring safety, sterility, and durability requirements. Healthcare sustainability initiatives are further boosting segment growth.

- By Packaging Layer

On the basis of packaging layer, the market is segmented into primary packaging, secondary packaging, and tertiary packaging. The primary packaging segment dominated the largest revenue share in 2025, driven by its direct contact with products and high demand in food and consumer goods industries. It plays a critical role in product protection, safety, and shelf appeal, making it essential across retail and food service sectors. Biodegradable materials are increasingly being used in primary formats to meet sustainability standards. Strong regulatory emphasis on reducing direct plastic usage is reinforcing this segment’s dominance.

The tertiary packaging segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising focus on sustainable logistics and bulk transportation solutions. Companies are adopting biodegradable alternatives to reduce environmental impact in supply chain operations. Increasing global trade and e-commerce shipments are expanding demand for eco-friendly protective packaging. Innovations in fiber-based and molded packaging solutions are improving strength and efficiency. Corporate sustainability targets are further accelerating adoption.

- By End-User

On the basis of end-user, the market is segmented into restaurants, hotels, tea and coffee shops, sweets & snacks stores, cafeteria, and others. The restaurants segment dominated the largest market revenue share in 2025, driven by high usage of disposable packaging in dine-in, takeaway, and delivery services. Increasing consumer preference for sustainable dining experiences is encouraging adoption of biodegradable packaging solutions. Regulatory restrictions on single-use plastics are further reinforcing this dominance. Large-scale food service operations continue to generate consistent demand for eco-friendly packaging.

The tea and coffee shops segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by rapid expansion of café culture and urban consumption trends. Growing awareness of environmental sustainability among younger consumers is increasing demand for biodegradable cups, lids, and packaging. Expansion of branded café chains is further accelerating adoption. Convenience-driven consumption patterns are boosting packaging demand in this segment. Strong emphasis on brand sustainability positioning is supporting long-term growth.

Europe Biodegradable Paper and Plastic Packaging Market Regional Analysis

- Germany dominated the Europe Biodegradable Paper and Plastic Packaging Market with the largest revenue share in 2025, driven by its strong packaging manufacturing base, strict environmental regulations, and early adoption of circular economy practices across industrial and consumer sectors

- The presence of leading packaging and material solution providers such as Tetra Pak, Mondi Group, and Amcor strengthens the demand for advanced biodegradable and compostable packaging formats across food, beverage, and retail applications

- Increasing innovation in bio-based polymers, expansion of compostable paper packaging solutions, and strong alignment with European Union sustainability directives further reinforce Germany’s dominant position in the Europe biodegradable packaging market

U.K. Europe Biodegradable Paper and Plastic Packaging Market Insight

The U.K. is projected to register the fastest CAGR in the Europe Biodegradable Paper and Plastic Packaging Market during the forecast period, supported by rapid growth in e-commerce, strong retail sustainability commitments, and increasing consumer preference for eco-friendly packaging solutions. The country’s shift toward reducing single-use plastics is accelerating demand for paper-based and compostable packaging alternatives. Leading packaging players such as DS Smith and Mondi are expanding their sustainable packaging portfolios with lightweight, recyclable, and fiber-based solutions for retail and industrial applications. Growing investments by major retailers such as Tesco and Sainsbury’s in sustainable packaging systems, combined with government-led plastic reduction initiatives, are positioning the U.K. as the fastest-growing market in Europe.

France Europe Biodegradable Paper and Plastic Packaging Market Insight

France is expected to witness steady growth in the Europe Biodegradable Paper and Plastic Packaging Market during the forecast period, driven by rising adoption of sustainable packaging in food, beverage, and personal care industries along with strong regulatory emphasis on plastic reduction. The country’s packaging landscape is increasingly shifting toward recyclable and compostable materials supported by national environmental policies and circular economy goals. Leading companies such as Danone, Carrefour, and Lactalis are actively integrating biodegradable paper and plastic packaging formats across their product lines to reduce environmental impact and meet consumer demand for sustainable solutions. Expanding retail sustainability programs, growth in organic food consumption, and continuous innovation in bio-based packaging materials are reinforcing France’s position as a stable and steadily growing market in Europe.

Europe Biodegradable Paper and Plastic Packaging Market Share

The biodegradable paper and plastic packaging industry is primarily led by well-established companies, including:

- Smurfit Kappa (Ireland)

- DS Smith (U.K.)

- Tetra Pak (Switzerland)

- Mondi (U.K.)

- International Paper (U.S.)

- VPK Group (Belgium)

- Sonoco Products Company (U.S.)

- STOROPACK HANS REICHENECKER GMBH (Germany)

- WestRock Company (U.S.)

- Stora Enso (Finland)

- Novamont S.p.A. (Italy)

- OSQ (Poland)

- BIO-LUTIONS International AG (Germany)

- TIPA LTD (Israel)

- BioApply (U.S.)

- CPS Paper Products (India)

- The Biodegradable Bag Company Ltd. (U.K.)

Latest Developments in Europe Biodegradable Paper and Plastic Packaging Market

- In October 2024, Avantium’s commissioning of its flagship PEF production plant in the Netherlands marked a major step in scaling bio-based polymer supply for high-performance packaging applications, particularly in premium beverage packaging. The facility enabled greater commercial availability of PEF, a recyclable and plant-based polymer that offers superior barrier properties compared to conventional plastics, thereby supporting brand owners in transitioning toward more sustainable packaging solutions while maintaining product shelf life and quality standards

- In September 2024, Paques Biomaterials secured EUR 14 million in funding to advance its 6,000-tonne PHA production facility, strengthening the development of marine-biodegradable bioplastics for packaging applications. This investment enhanced the commercialization pathway for PHA-based materials, which decompose in natural environments without leaving microplastic residues, thereby increasing adoption potential in foodservice packaging, agricultural films, and hygiene products across European sustainability-driven markets

- In August 2024, Futerro’s large-scale PLA biorefinery in Normandy reaching full production capacity significantly boosted Europe’s internal supply of polylactic acid, a widely used compostable bioplastic in packaging applications. This expansion reduced reliance on imports, improved cost efficiency, and supported broader adoption of PLA-based packaging formats such as containers, trays, and flexible films used in food and retail sectors, thereby strengthening the regional biodegradable packaging supply chain

- In July 2024, HolyGrail 2.0 watermark technology trials in Germany achieved high detection efficiency for compostable packaging materials, improving automated sorting accuracy in recycling facilities. This advancement enhanced the ability to separate biodegradable and compostable packaging from conventional waste streams, thereby increasing recycling efficiency and supporting the circular economy framework for sustainable packaging systems across Europe

- In March 2024, Xampla expanded its plant-protein-based packaging technology across European markets, advancing the commercialization of fully plastic-free films and coatings designed for food delivery and retail applications. This development strengthened innovation in natural polymer-based packaging materials, reducing dependency on fossil fuel-derived plastics and supporting the transition toward fully biodegradable and sustainable packaging alternatives in high-volume consumer markets

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Europe Biodegradable Paper Plastic Packaging Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Europe Biodegradable Paper Plastic Packaging Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Europe Biodegradable Paper Plastic Packaging Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.