Europe Contrast Injector Market

Market Size in USD Million

USD

397.42 Million

USD

582.71 Million

2025

2033

USD

397.42 Million

USD

582.71 Million

2025

2033

| 2026 - 2033 | |

| USD 397.42 Million | |

| USD 582.71 Million | |

| % | |

|

Europe Contrast Injector Market Size

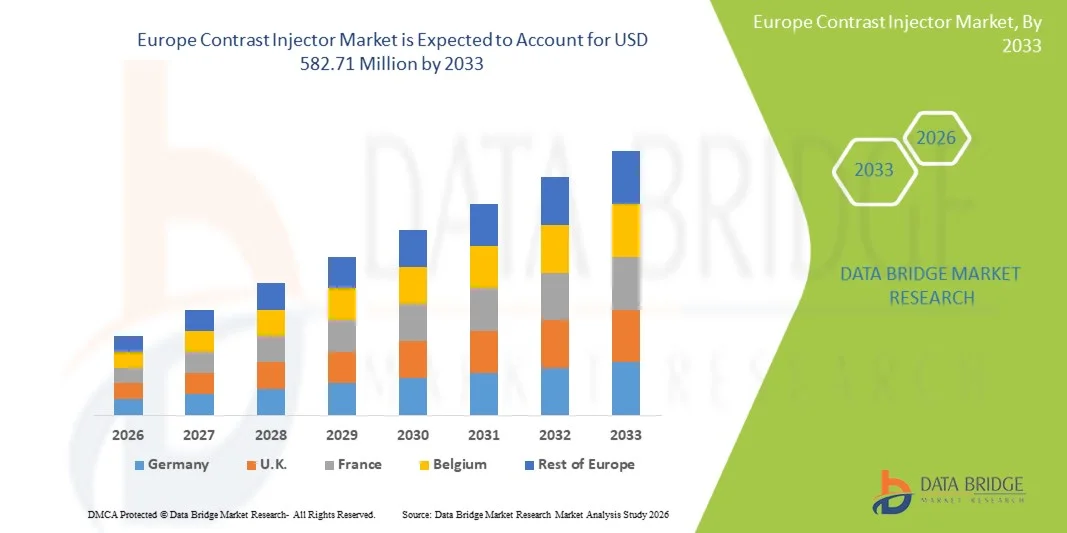

- The Europe contrast injector market size was valued at USD 397.42 million in 2025 and is expected to reach USD 582.71 million by 2033, at a CAGR of 4.90% during the forecast period

- The market growth is largely driven by the rising volume of diagnostic imaging procedures, along with continuous technological advancements in contrast delivery systems, particularly across CT and MRI applications in hospitals and diagnostic centers

- Furthermore, increasing emphasis on patient safety, precise dosing, workflow efficiency, and the growing prevalence of chronic diseases are positioning contrast injectors as an essential component of modern medical imaging infrastructure, thereby significantly accelerating market growth across Europe

Europe Contrast Injector Market Analysis

- Contrast injectors, enabling the controlled and automated delivery of contrast media during diagnostic imaging procedures, are increasingly critical components of modern radiology workflows across hospitals and diagnostic imaging centers in Europe due to their ability to enhance image quality, improve dosing accuracy, and support efficient clinical operations

- The growing demand for contrast injectors is primarily driven by the rising volume of CT and MRI scans, increasing prevalence of chronic diseases such as cardiovascular and neurological disorders, and the expanding elderly population requiring advanced diagnostic imaging

- Germany dominated the Europe contrast injector market with the largest revenue share of 28.4% in 2025, supported by its advanced healthcare infrastructure, high diagnostic imaging penetration, strong reimbursement framework, and the presence of leading medical device manufacturers, with widespread adoption across tertiary hospitals and specialized imaging centers

- Poland is expected to be the fastest-growing country in the Europe contrast injector market during the forecast period driven by increasing healthcare investments, modernization of diagnostic facilities, and rising access to advanced imaging technologies across public and private healthcare sectors

- Dual-head segment dominated the Europe contrast injector market with a market share of 46.8% in 2025, driven by their capability to support complex imaging protocols, improve workflow efficiency, and meet the growing demand for high-precision diagnostic procedures across European healthcare facilities

Report Scope and Europe Contrast Injector Market Segmentation

|

Attributes |

Europe Contrast Injector Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Europe Contrast Injector Market Trends

“Integration of AI-Driven Dose Optimization and Workflow Automation”

- A significant and accelerating trend in the Europe contrast injector market is the integration of artificial intelligence (AI) and automation technologies to optimize contrast dosing, reduce human error, and enhance imaging workflow efficiency across CT and MRI procedures

- For instance, Bayer’s MEDRAD Centargo CT Injection System incorporates automation features that streamline contrast delivery and reduce setup steps, enabling radiology departments to improve productivity while maintaining dosing accuracy

- AI-enabled contrast injectors support real-time monitoring of injection parameters, adaptive flow control, and protocol standardization, helping clinicians achieve consistent image quality while minimizing contrast media waste and patient risk

- The increasing adoption of AI-assisted imaging platforms allows contrast injectors to seamlessly integrate with scanners, electronic medical records, and radiology information systems, enabling synchronized and data-driven diagnostic workflows

- This growing focus on intelligent, connected injector systems is reshaping expectations within European radiology departments, where efficiency, patient safety, and regulatory compliance are becoming critical purchasing criteria

- Consequently, companies such as Bracco and Guerbet are advancing smart injector platforms with enhanced connectivity, automated protocols, and data analytics capabilities to meet evolving clinical and operational demands

- The increasing preference for compact, mobile injector designs is also influencing product development, particularly for outpatient imaging centers and space-constrained hospital environments

Europe Contrast Injector Market Dynamics

Driver

“Rising Diagnostic Imaging Volumes and Emphasis on Patient Safety”

- The increasing volume of diagnostic imaging procedures across Europe, driven by the rising prevalence of chronic diseases and an aging population, is a major driver fueling demand for advanced contrast injector systems

- For instance, in March 2024, Guerbet announced the expansion of its injector and consumables portfolio in Europe to support growing CT and MRI procedure volumes while enhancing patient safety and workflow efficiency

- As healthcare providers focus on reducing contrast-induced complications, modern injectors offer precise dosing, pressure monitoring, and automated delivery, positioning them as a preferred upgrade over manual injection methods

- Furthermore, strict European regulatory standards and hospital quality benchmarks are encouraging the adoption of advanced injector technologies that ensure traceability, consistency, and compliance in imaging procedures

- The increasing investment in hospital modernization and diagnostic infrastructure across major European countries is further accelerating the adoption of contrast injectors in both public and private healthcare facilities

- Growing demand for early disease detection and preventive diagnostics is also driving higher utilization of contrast-enhanced imaging across oncology, cardiology, and neurology applications

- The expansion of private diagnostic imaging chains across Europe is creating sustained demand for standardized, high-throughput contrast injector systems

Restraint/Challenge

“High Equipment Costs and Complex Regulatory Compliance”

- The high initial cost of advanced contrast injector systems, coupled with ongoing maintenance and consumable expenses, poses a significant challenge to market adoption, particularly for smaller hospitals and imaging centers

- For instance, budget-constrained healthcare facilities in parts of Southern and Eastern Europe often delay injector upgrades due to competing capital expenditure priorities

- In addition, stringent European medical device regulations and lengthy approval processes can slow product launches and increase compliance costs for manufacturers

- These regulatory and financial barriers may discourage rapid technology adoption, especially among price-sensitive buyers who continue to rely on older or refurbished injector systems

- Overcoming these challenges through cost-effective product offerings, simplified compliance strategies, and value-based procurement models will be critical for sustaining long-term growth in the Europe contrast injector market

- Limited availability of trained radiology staff in some countries further complicates the adoption of advanced injector technologies requiring specialized operation

- Variability in reimbursement policies for contrast-enhanced imaging across European countries can also restrict purchasing decisions and delay equipment replacement cycles

Europe Contrast Injector Market Scope

The market is segmented on the basis of product, application, modality, design, end user, and distribution channel.

- By Product

On the basis of product, the Europe contrast injector market is segmented into injector systems, consumables, and accessories. The injector systems segment dominated the market in 2025, driven by their critical role in delivering precise and automated contrast media during CT and MRI procedures. These systems account for the highest capital expenditure among product categories, significantly contributing to overall market revenue. European hospitals prioritize advanced injector systems to ensure dosing accuracy, patient safety, and compliance with stringent EU medical device regulations. The integration of automation, connectivity, and workflow optimization features further strengthens demand for injector systems. In addition, replacement of legacy injectors across Western Europe supports sustained dominance. Long service lifecycles and bundled maintenance contracts further reinforce this segment’s leading position.

The consumables segment is expected to be the fastest growing during the forecast period due to its recurring usage in every contrast-enhanced imaging procedure. Each scan requires disposable components such as syringes, tubing, and connectors, ensuring continuous demand. Rising CT and MRI procedure volumes across oncology, cardiology, and neurology are directly increasing consumables consumption. Strict infection control and hygiene standards across European healthcare facilities further support frequent replacement. The growing adoption of multi-patient and syringeless injector systems is also expanding consumables usage. Moreover, long-term supply agreements with hospitals are accelerating segment growth.

- By Application

On the basis of application, the market is segmented into radiology, interventional radiology, and interventional cardiology. The radiology segment dominated the market in 2025 due to the high volume of routine contrast-enhanced CT and MRI scans performed across Europe. Radiology remains the primary diagnostic discipline for cancer detection, neurological disorders, and abdominal imaging. Nearly all hospitals and diagnostic centers are equipped with radiology departments, ensuring widespread injector utilization. Demand is further driven by the need for consistent image quality and standardized imaging protocols. Increasing outpatient diagnostic imaging volumes continue to support dominance. Ongoing upgrades of CT and MRI scanners also reinforce injector demand in radiology.

The interventional radiology segment is anticipated to be the fastest growing during the forecast period, driven by the rapid adoption of minimally invasive, image-guided procedures. These procedures require highly precise and controlled contrast delivery, boosting injector usage. Growth is supported by advancements in injector pressure control and real-time monitoring technologies. Increasing preference for catheter-based treatments over open surgery is accelerating procedure volumes. Expansion of dedicated interventional suites across Europe further supports growth. Improved patient outcomes and shorter recovery times are also contributing to rising adoption.

- By Modality

On the basis of modality, the market is segmented into dual-head, single-head, and syringeless injectors. The dual-head injector segment dominated the market in 2025 with a market share of 46.8% due to its ability to sequentially deliver contrast media and saline within a single procedure. This capability is essential for advanced multi-phase CT imaging protocols. Dual-head injectors help improve image clarity while reducing overall contrast volume administered to patients. European hospitals prefer these systems for enhanced workflow efficiency and procedural flexibility. Compatibility with high-end CT scanners further supports widespread adoption. Strong usage in tertiary and teaching hospitals sustains this segment’s dominance.

The syringeless injector segment is expected to grow at the fastest rate during the forecast period, driven by increasing focus on infection prevention and operational efficiency. Syringeless systems reduce manual handling of contrast media, lowering contamination risks. These systems also minimize consumable waste, aligning with sustainability goals across European healthcare systems. High-volume imaging centers favor faster setup and reduced downtime. Standardized workflows and reduced preparation steps enhance productivity. Regulatory emphasis on patient safety is further accelerating adoption.

- By Design

On the basis of design, the market is segmented into pedestal mounted, ceiling mounted, and standalone injectors. The pedestal-mounted segment dominated the market in 2025 due to its flexibility and ease of integration into existing imaging environments. These injectors require minimal infrastructure modification, making them suitable for retrofit projects. Hospitals favor pedestal-mounted designs due to their lower installation costs compared to ceiling-mounted systems. Their mobility allows usage across multiple imaging rooms when required. Compatibility with various scanner configurations supports widespread adoption. Strong presence in both public and private hospitals reinforces dominance.

The ceiling-mounted segment is projected to be the fastest growing during the forecast period, driven by increasing construction of new and upgraded imaging suites across Europe. Ceiling-mounted designs optimize floor space and reduce equipment clutter. Improved ergonomics enhance staff comfort and procedural efficiency. Demand is particularly strong in modern diagnostic centers and flagship hospitals. Adoption aligns with contemporary hospital design standards. Long-term workflow and space-efficiency benefits are accelerating investment.

- By End User

On the basis of end user, the market is segmented into hospitals, diagnostic imaging centers, ambulatory surgical centers, and others. The hospital segment dominated the market in 2025 due to high patient volumes and broad diagnostic and interventional service offerings. Hospitals perform the majority of contrast-enhanced imaging procedures across Europe. Availability of capital budgets supports procurement of advanced injector systems. Teaching and tertiary hospitals often adopt high-end injector technologies. Integration with hospital information and imaging systems strengthens demand. Public healthcare funding further sustains dominance.

The diagnostic imaging centers segment is expected to witness the fastest growth during the forecast period, driven by the rapid expansion of private imaging networks. These centers focus on high-throughput outpatient diagnostics, increasing injector utilization. Demand for efficient and standardized injector systems is high. Hospitals increasingly outsource imaging services to specialized centers. Rising private healthcare expenditure supports technology upgrades. Operational efficiency requirements are accelerating growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender and third-party distributors. The direct tender segment dominated the market in 2025 due to centralized procurement practices across public healthcare systems in Europe. Large hospitals and healthcare networks rely on tender-based purchasing for compliance and transparency. This channel favors established manufacturers with proven clinical performance. Long-term contracts provide stable revenue streams. Bulk purchasing helps reduce unit costs. Strong public sector presence sustains dominance.

The third-party distributors segment is expected to grow the fastest during the forecast period, driven by the rising demand from private hospitals and imaging centers. Distributors provide localized sales, installation, and technical support. Flexible purchasing options appeal to smaller facilities. Faster access to consumables improves operational continuity. The growth is particularly strong in the emerging European markets. The expansion of private diagnostics is increasing distributor relevance.

Europe Contrast Injector Market Regional Analysis

- Germany dominated the Europe contrast injector market with the largest revenue share of 28.4% in 2025, supported by its advanced healthcare infrastructure, high diagnostic imaging penetration, strong reimbursement framework, and the presence of leading medical device manufacturers, with widespread adoption across tertiary hospitals and specialized imaging centers

- Healthcare providers in Germany place a high priority on patient safety, precise contrast dosing, and workflow efficiency, supporting widespread adoption of automated and technologically advanced contrast injector systems across hospitals and diagnostic imaging centers

- This dominance is further reinforced by favorable reimbursement policies, strong public healthcare funding, and the presence of leading medical device manufacturers, establishing Germany as a key hub for contrast injector adoption and innovation within Europe

The Germany Contrast Injector Market Insight

The Germany contrast injector market dominated Europe in 2025, supported by its advanced healthcare infrastructure and high penetration of CT and MRI scanners. German hospitals emphasize precision diagnostics, patient safety, and workflow efficiency, driving strong adoption of automated contrast injector systems. Favorable reimbursement policies and strong public healthcare funding further support market growth. The presence of leading medical device manufacturers and innovation-focused hospitals reinforces Germany’s leadership. Continuous replacement of legacy imaging equipment sustains long-term demand.

U.K. Contrast Injector Market Insight

The U.K. contrast injector market is projected to grow at a notable CAGR during the forecast period, driven by increasing diagnostic imaging demand within the NHS. Ongoing investments in imaging capacity expansion and modernization programs are supporting injector adoption. Strong focus on early cancer detection and chronic disease diagnosis is increasing contrast-enhanced procedures. Regulatory emphasis on patient safety and standardized imaging protocols further boosts demand. Growth is also supported by rising outpatient diagnostic services.

France Contrast Injector Market Insight

The France contrast injector market is experiencing steady growth, driven by a well-developed public healthcare system and rising imaging procedure volumes. French hospitals increasingly adopt advanced injector systems to improve workflow efficiency and reduce contrast-related risks. Government support for healthcare digitization and modernization is strengthening equipment upgrades. Growing emphasis on oncology and cardiovascular diagnostics is increasing demand for contrast-enhanced imaging. Adoption is strong across both public and private healthcare facilities.

Poland Contrast Injector Market Insight

The Poland contrast injector market is emerging as one of the fastest-growing markets in Europe, driven by increasing healthcare investments and modernization of diagnostic infrastructure. Expansion of CT and MRI installations across public hospitals is supporting rising demand for contrast injectors. Growing access to advanced imaging services is improving early disease detection rates. EU-funded healthcare development programs are accelerating equipment upgrades. Increasing participation of private diagnostic centers is further boosting market growth.

Europe Contrast Injector Market Share

The Europe Contrast Injector industry is primarily led by well-established companies, including:

- Bracco S.p.A. (Italy)

- Bayer AG (Germany)

- Guerbet Group (France)

- Medtron AG (Germany)

- GE HealthCare (U.S.)

- Siemens Healthineers AG (Germany)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- Nemoto Kyorindo Co., Ltd. (Japan)

- AngioDynamics, Inc. (U.S.)

- Imaxeon Pty Ltd. (Australia)

- APOLLO RT Co., Ltd. (Japan)

- Cook (U.S.)

- RI.MOS. S.r.l. (Italy)

- CS Diagnostics GmbH (Germany)

- Sino Medical-Device Technology Co., Ltd. (China)

- Shenzhen Anke High-Tech Co., Ltd. (China)

- Shenzhen Seacrown Electromechanical Co., Ltd. (China)

- HONG KONG MEDI CO LIMITED (Hong Kong)

- B. Braun SE (Germany)

What are the Recent Developments in Europe Contrast Injector Market?

- In March 2025, ulrich medical reported 15 consecutive years of growth, with its CT and MRI contrast media injector product lines cited as key revenue drivers in Europe and additional production capacity being added to support expanding adoption

- In September 2024, ulrich medical reported above-average sales growth of its contrast media injectors in Europe, with an 18% year-on-year increase and particularly strong uptake in France driven by syringe-free injector systems that improve workflow and patient throughput. This growth reflects real-world adoption increases of newer injector models across European imaging departments

- In July 2024, Ulrich Medical announced extraordinary growth in Europe’s contrast media injector sector with significant expansion in France’s market share, driven by multi-patient compliant injectors and broader distribution, highlighting adoption trends and operational flexibility in clinical settings

- In April 2024, Elucirem™ (Gadopiclenol), following its European regulatory approval, was administered to patients undergoing MRI scans in Europe, demonstrating real-world clinical use of this new contrast agent that works closely with injector technology in imaging protocols

- In December 2023, the European Commission granted marketing authorisation approval for Guerbet’s Elucirem™ (Gadopiclenol), a high-relaxivity MRI contrast agent that enables MRI scans with half the conventional gadolinium dose, representing a significant step in contrast agent innovation tied to injector usage

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.