Europe Down Syndrome Market

Market Size in USD Million

USD

432.65 Million

USD

1,215.27 Million

2024

2032

USD

432.65 Million

USD

1,215.27 Million

2024

2032

| 2025 - 2032 | |

| USD 432.65 Million | |

| USD 1,215.27 Million | |

| % | |

|

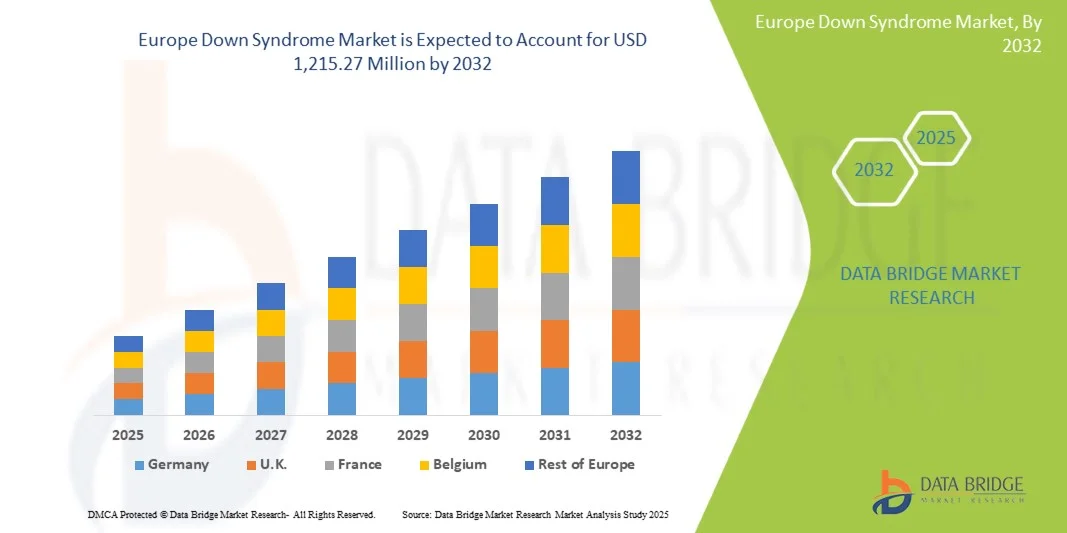

Europe Down Syndrome Market Size

- The Europe Down Syndrome market size was valued at USD 432.65 million in 2024 and is expected to reach USD 1,215.27 million by 2032, at a CAGR of 13.78% during the forecast period

- The market growth is largely driven by increasing awareness, early diagnosis, and advancements in medical care and therapeutic interventions for individuals with Down Syndrome across the region

- Furthermore, rising demand for specialized healthcare services, supportive therapies, and government initiatives promoting inclusive healthcare and education for Down Syndrome patients are enhancing the quality of life and care. These converging factors are accelerating the adoption of innovative treatments and services, thereby significantly boosting the market's growth

Europe Down Syndrome Market Analysis

- Down Syndrome care and management, encompassing early diagnosis, therapeutic interventions, and supportive healthcare services, are increasingly vital components of pediatric and adult healthcare systems in both residential and clinical settings due to their impact on quality of life, cognitive development, and social inclusion

- The escalating demand for Down Syndrome treatments and supportive therapies is primarily fueled by increasing awareness, advancements in medical technology, and growing government and non-government initiatives promoting inclusive healthcare and early intervention programs

- Germany dominated the Europe Down Syndrome market with the largest revenue share of 38.2% in 2024, characterized by well-established healthcare infrastructure, advanced diagnostic facilities, and strong government support for patient care programs, with substantial growth in specialized clinics, early intervention services, and innovative therapeutic solutions for Down Syndrome

- Poland is expected to be the fastest growing country in the Europe Down Syndrome market during the forecast period due to increasing healthcare investments, rising awareness, and expansion of genetic screening and supportive care programs

- Diagnosis segment dominated the Europe Down Syndrome market with a market share of 46.7% in 2024, driven by rising demand for early detection through advanced prenatal and postnatal screening techniques, enabling timely therapeutic interventions and improved patient outcomes

Report Scope and Europe Down Syndrome Market Segmentation

|

Attributes |

Europe Down Syndrome Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Europe Down Syndrome Market Trends

“Integration of Advanced Diagnostic and Genetic Screening Tools”

- A significant and accelerating trend in the Europe Down Syndrome market is the increasing adoption of advanced prenatal and postnatal diagnostic technologies, including non-invasive prenatal testing (NIPT) and genetic screening panels, enabling earlier and more accurate detection of Down Syndrome

- For instance, the Harmony® NIPT test is widely used across Germany, France, and the U.K., allowing early risk assessment and facilitating timely counseling for expectant parents

- Integration of high-throughput sequencing and AI-based analytics is enhancing diagnostic precision and supporting personalized therapeutic planning, which helps healthcare providers optimize interventions for each patient

- These technologies also enable centralized tracking and monitoring of patient outcomes across clinics and hospitals, improving coordination of care and resource allocation

- The trend toward more precise, non-invasive, and integrated diagnostic approaches is reshaping clinical standards for Down Syndrome care, prompting healthcare providers and companies to invest in next-generation screening solutions

- The demand for innovative diagnostic tools is growing rapidly across hospitals, clinics, and specialized centers, as early detection is increasingly linked to improved developmental and therapeutic outcomes

Europe Down Syndrome Market Dynamics

Driver

“Rising Awareness and Supportive Government Initiatives”

- The increasing awareness about Down Syndrome, coupled with supportive government policies and healthcare programs, is a key driver for the Europe Down Syndrome market

- For instance, Germany’s National Plan for People with Disabilities emphasizes early diagnosis and inclusive healthcare services, driving the adoption of specialized therapies and medical interventions

- Growing advocacy and public education campaigns are increasing parental knowledge about available treatments, early intervention programs, and therapy options, encouraging timely healthcare engagement

- Rising investments in specialized clinics, therapy centers, and homecare services are expanding access to care, enhancing patient quality of life, and fostering market growth

- The development of integrated care pathways for Down Syndrome patients, including multidisciplinary therapy and medical management, is further strengthening market adoption

- Increasing collaboration between healthcare providers, NGOs, and government agencies is improving accessibility and availability of diagnostic and therapeutic services across Europe

Restraint/Challenge

“Limited Access to Specialized Care and High Treatment Costs”

- Challenges in accessing specialized therapy centers, advanced diagnostics, and trained healthcare professionals limit broader adoption of Down Syndrome care solutions across Europe

- For instance, rural regions in Poland and Eastern Europe often have fewer specialized clinics and limited availability of early intervention programs, restricting timely patient care

- The high cost of diagnostic tests, genetic screening, and ongoing therapies can be a barrier for families, particularly where public healthcare coverage is limited or partial

- Variability in reimbursement policies across European countries adds complexity for both providers and patients seeking consistent and affordable care

- Addressing these barriers through expansion of therapy centers, improved insurance coverage, and subsidized diagnostic programs is essential for sustained market growth

- While awareness and initiatives are improving, disparities in infrastructure, cost, and accessibility continue to challenge equitable access to Down Syndrome care

Europe Down Syndrome Market Scope

The market is segmented on the basis of disease type, treatment, end user, and distribution channel.

- By Disease Type

On the basis of disease type, the Europe Down Syndrome market is segmented into Trisomy 21, Translocation Down Syndrome, and Mosaic Down Syndrome. The Trisomy 21 segment dominated the market with the largest revenue share of 72% in 2024, driven by its high prevalence among Down Syndrome cases. Trisomy 21 is widely recognized in clinical diagnostics and receives the most attention in terms of screening programs, awareness campaigns, and therapeutic interventions. Hospitals and specialized clinics prioritize early detection and personalized therapy for Trisomy 21 patients, contributing to higher adoption of diagnostic tools and therapy services. Public health initiatives across Germany, France, and the U.K. have also focused on Trisomy 21 awareness, increasing accessibility of care. Research and development efforts, including non-invasive prenatal testing (NIPT) and targeted therapy options, further strengthen this segment. The high incidence rate and established clinical protocols make Trisomy 21 the primary focus of the Down Syndrome market in Europe.

The Mosaic Down Syndrome segment is anticipated to witness the fastest growth from 2025 to 2032 due to increasing awareness and improved diagnostic accuracy in detecting mosaic cases, which are often underdiagnosed. Advances in genetic testing and AI-based analysis allow earlier and more precise identification of mosaic cases, enabling timely therapeutic intervention. Rising interest in personalized care programs for patients with variable phenotypes is further driving growth. Hospitals and therapy centers are increasingly adopting tailored intervention strategies, including speech, physical, and occupational therapy for mosaic patients. Awareness campaigns and NGO support are expanding in Eastern Europe, where previously diagnostic limitations restricted early detection. The growing recognition of mosaic Down Syndrome’s unique needs is fueling investment in research, diagnostics, and treatment solutions.

- By Treatment

On the basis of treatment, the Europe Down Syndrome market is segmented into Diagnosis and Therapy. The Diagnosis segment dominated the market with a share of 46.7% in 2024, primarily due to rising demand for early detection through prenatal and postnatal screening programs. Hospitals, clinics, and specialized diagnostic centers offer non-invasive prenatal testing, karyotyping, and advanced genetic screening to detect Down Syndrome at the earliest stages. Early diagnosis allows healthcare providers to plan therapies and interventions tailored to the patient’s needs, improving long-term developmental outcomes. Government and NGO initiatives supporting widespread screening also contribute to the dominance of this segment. Increased awareness among parents and healthcare providers about the benefits of timely diagnosis further drives adoption. Diagnostic innovations and integration of AI in genetic analysis are strengthening this segment.

The Therapy segment is expected to witness the fastest growth from 2025 to 2032, driven by rising demand for multidisciplinary therapeutic interventions including physical, occupational, and speech therapy. Therapy centers and homecare services are increasingly providing personalized treatment programs, improving quality of life and developmental progress for patients. Public and private healthcare investment in therapy services is expanding, especially in Poland and Eastern Europe. Teletherapy and remote monitoring solutions are further accelerating growth in this segment. Increasing parental awareness and focus on inclusive education programs also contribute to the rising adoption of therapy services.

- By End User

On the basis of end user, the Europe Down Syndrome market is segmented into hospital, clinics, homecare setting, therapy centers, and others. The Hospitals segment dominated the market with the largest revenue share of 50.4% in 2024, owing to their comprehensive infrastructure and availability of advanced diagnostic and therapeutic services. Hospitals provide multidisciplinary teams including pediatricians, geneticists, and therapists, ensuring early diagnosis and ongoing care. National healthcare programs and insurance coverage in Germany, France, and the U.K. often prioritize hospital-based interventions. High patient trust in hospital services and the ability to access specialized equipment drive segment dominance. Hospitals also lead in implementing advanced screening technologies and pilot therapeutic programs. Collaborative initiatives between hospitals and research institutions further strengthen their market position.

The Homecare Setting segment is expected to witness the fastest growth from 2025 to 2032, fueled by rising demand for personalized, convenient, and continuous care at home. Remote monitoring, teletherapy, and mobile healthcare services allow patients to receive regular interventions without frequent hospital visits. Parents and caregivers increasingly prefer home-based programs for flexibility and comfort. The adoption of digital health solutions and wearable devices further supports this trend. Growing government and NGO support for home-based care in Eastern Europe is accelerating segment expansion. Cost-effectiveness and enhanced quality of life make homecare an attractive option for long-term management of Down Syndrome.

- By Distribution Channel

On the basis of distribution channel, the Europe Down Syndrome market is segmented into Direct Tender, Retail Sales, and Others. The Direct Tender segment dominated the market with the largest revenue share of 61% in 2024, driven by procurement of diagnostic kits, therapy equipment, and medical supplies by hospitals and government healthcare programs. Large-scale purchasing agreements and tenders ensure cost-efficiency and widespread availability of necessary products. Hospitals and clinics prefer direct procurement from manufacturers to guarantee authenticity, compliance, and timely delivery. Government initiatives in Germany, France, and the U.K. also rely on direct tender for distributing diagnostic and therapy equipment to multiple care centers. Direct tender ensures scalability, standardization, and streamlined logistics, reinforcing its dominance in the market.

The Retail Sales segment is expected to witness the fastest growth from 2025 to 2032, owing to increasing availability of home-based diagnostic kits, therapy tools, and supportive care products through pharmacies and online platforms. Parents and caregivers increasingly purchase diagnostic or monitoring tools for home use. E-commerce platforms facilitate access to specialized equipment, particularly in countries with limited local clinic access. Rising awareness of early intervention and homecare programs fuels adoption through retail channels. The convenience and growing trust in online healthcare products contribute to rapid growth in this segment.

Europe Down Syndrome Market Regional Analysis

- Germany dominated the Europe Down Syndrome market with the largest revenue share of 38.2% in 2024, characterized by well-established healthcare infrastructure, advanced diagnostic facilities, and strong government support for patient care programs, with substantial growth in specialized clinics, early intervention services, and innovative therapeutic solutions for Down Syndrome

- Healthcare providers and parents in the region highly value the accessibility of specialized therapies, comprehensive hospital services, and early diagnosis programs, which improve developmental outcomes and quality of life for patients

- This widespread adoption is further supported by high public and private healthcare investments, advanced research initiatives, and growing awareness campaigns, establishing Germany as a key hub for Down Syndrome diagnosis, therapy, and supportive care across Europe

U.K. Down Syndrome Market Insight

The U.K. Down Syndrome market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing awareness, early diagnosis, and supportive government programs. Growing parental preference for early intervention and therapy services is boosting adoption across hospitals, clinics, and homecare settings. The U.K.’s well-developed healthcare system, coupled with strong advocacy by Down Syndrome organizations, promotes access to genetic screening, counseling, and multidisciplinary therapeutic programs. In addition, teletherapy and digital health initiatives are expanding care delivery in both urban and semi-urban areas. Rising demand for personalized therapy plans and inclusive education programs further strengthens market growth. The country’s focus on improving patient outcomes and enhancing quality of life continues to stimulate market adoption.

France Down Syndrome Market Insight

The France Down Syndrome market is projected to witness steady growth during the forecast period, fueled by robust healthcare infrastructure and government-supported early intervention initiatives. Increasing public awareness and widespread access to diagnostic tools, including non-invasive prenatal testing, are driving adoption. Hospitals and specialized therapy centers are expanding their services, providing multidisciplinary care encompassing medical, therapeutic, and educational support. The country’s emphasis on inclusive healthcare and rehabilitation programs promotes comprehensive patient management. Growing collaboration between healthcare providers, NGOs, and research institutions supports innovation and accessibility of services. Overall, France continues to be a key contributor to Europe’s Down Syndrome market due to its proactive healthcare policies and advanced care programs.

Poland Down Syndrome Market Insight

The Poland Down Syndrome market is expected to witness the fastest growth at a notable CAGR during the forecast period, driven by increasing awareness, expanding healthcare infrastructure, and rising access to early diagnosis and therapeutic interventions. Hospitals, clinics, and therapy centers are increasingly adopting non-invasive prenatal testing, genetic screening, and multidisciplinary therapy programs, improving patient outcomes. Government initiatives and NGO support are enhancing access to specialized care and inclusive education programs across urban and semi-urban areas. Home-based care services and teletherapy solutions are gaining traction, providing flexible and continuous support for patients. Rising parental awareness and advocacy for early intervention are further boosting market adoption. Overall, Poland is emerging as a high-growth market in Europe due to its improving healthcare ecosystem and growing emphasis on comprehensive Down Syndrome care.

Europe Down Syndrome Market Share

The Europe Down Syndrome industry is primarily led by well-established companies, including:

- AC Immune SA (Switzerland)

- Aelis Farma (France)

- Annovis Bio, Inc. (U.S.)

- Alzheon, (U.S.)

- Perha Pharmaceuticals (U.S.)

- Aphios Corporation (U.S.)

- Eisai Co., Ltd. (Japan)

- SERVIER LABORATORIES (France)

- Biogen Inc. (U.S.)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Illumina, Inc. (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- Myriad Genetics, Inc. (U.S.)

- Demeditec Diagnostics GmbH (Germany)

- ManRos Therapeutics (Switzerland)

- NeuroNascent, Inc. (U.S.)

- Natera, Inc. (U.S.)

- Abnova Corporation (Taiwan)

What are the Recent Developments in Europe Down Syndrome Market?

- In November 2024, Poland's Ministry of Health updated the country's newborn screening program to include tests for additional rare genetic disorders, such as Down syndrome. This expansion aims to facilitate early diagnosis and intervention, enhancing long-term health outcomes for affected children

- In September 2024, the Polish government adopted the Rare Disease Plan for 2024–2025, which includes the establishment of new specialist centers by December 2025. These centers aim to improve access to diagnostic and therapeutic services for individuals with rare diseases, including Down syndrome

- In April 2024, Management Solutions supported the Down syndrome community in Poland by participating in the "Colorful Socks" virtual race organized by the Coś Dobrego Foundation. This event aimed to raise awareness and promote inclusion for individuals with Down syndrome

- In January 2023, the first café in Poland employing people with Down syndrome opened in Kraków. This initiative aims to promote social inclusion and provide employment opportunities for adults with Down syndrome, fostering greater independence and community integration

- In May 2021, Poland's government introduced full support for families with disabled children under the Family 500+ program. This initiative provides financial assistance to families, ensuring that all disabled children up to 18 years of age receive support, thereby alleviating some of the financial burdens associated with raising a child with Down syndrome

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.