Europe Ear Nasal Packing Market

Market Size in USD Million

USD

80.00 Million

USD

133.39 Million

2025

2033

USD

80.00 Million

USD

133.39 Million

2025

2033

| 2026 - 2033 | |

| USD 80.00 Million | |

| USD 133.39 Million | |

| % | |

|

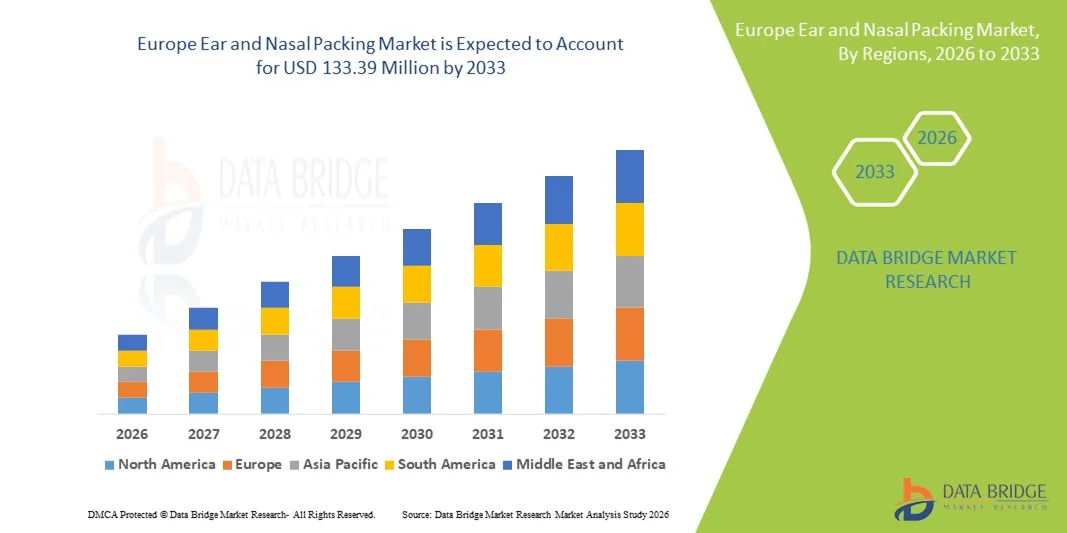

Europe Ear and Nasal Packing Market Size

- The Europe ear and nasal packing market size was valued at USD 80.00 million in 2025 and is expected to reach USD 133.39 million by 2033, at a CAGR of 6.6% during the forecast period

- The market growth is largely fueled by the increasing prevalence of ENT (ear, nose, and throat) disorders, rising surgical procedures, and enhanced awareness regarding postoperative care and infection prevention across Europe

- Furthermore, technological innovations in absorbable and non-absorbable packing materials, coupled with rising demand from hospitals and clinics for efficient and patient-friendly nasal and ear packing solutions, are driving market adoption. These factors are accelerating the uptake of advanced ear and nasal packing products, thereby significantly boosting the industry's growth

Europe Ear and Nasal Packing Market Analysis

- Ear and nasal packing products, designed to control bleeding, support tissue healing, and prevent infections after ENT surgeries or trauma, are increasingly vital components of hospital and outpatient ENT care due to their effectiveness, ease of use, and patient safety benefits

- The escalating demand for ear and nasal packing is primarily fueled by the rising prevalence of ENT disorders, growing awareness of postoperative care, and increasing numbers of ENT surgical procedures across Europe

- Germany dominated the Europe ear and nasal packing market with the largest revenue share of 28.4% in 2025, characterized by advanced healthcare infrastructure, high adoption of innovative ENT devices, and a strong presence of key industry players, with hospitals and clinics increasingly using both absorbable and non-absorbable packing materials

- France is expected to be the fastest-growing countries during the forecast period due to high patient awareness, increasing ENT surgeries, technological adoption in hospitals, and growing investments in modern ENT treatment facilities.

- Nasal segment dominated the Europe ear and nasal packing market with a market share of 55.7% in 2025, driven by its widespread use in controlling epistaxis, compatibility with both absorbable and non-absorbable materials, and established effectiveness in surgical and trauma-related ENT procedures

Report Scope and Europe Ear and Nasal Packing Market Segmentation

|

Attributes |

Europe Ear and Nasal Packing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Europe Ear and Nasal Packing Market Trends

Advancements in Absorbable and Patient-Friendly Materials

- A significant and accelerating trend in the Europe ear and nasal packing market is the development of absorbable materials and patient-friendly designs that reduce discomfort and improve postoperative recovery outcomes

- For instance, Floseal Nasal Pack utilizes a gelatin-thrombin matrix that dissolves naturally, eliminating the need for manual removal and reducing patient pain during postoperative care

- Enhanced material innovations allow packing products to conform better to nasal and ear cavities, reducing trauma, controlling bleeding more effectively, and providing antimicrobial protection. For instance, Merocel® packs feature highly absorbent foam that adapts to cavity shape and minimizes irritation

- Hospitals and clinics increasingly adopt these advanced packs to optimize surgical outcomes and minimize follow-up procedures, enabling better workflow and patient satisfaction

- This trend towards more comfortable, effective, and clinically efficient packing solutions is fundamentally reshaping expectations for postoperative ENT care. Consequently, companies such as Medtronic and Stryker are developing bioresorbable and antimicrobial packing options that reduce patient discomfort and enhance healing

- The demand for patient-friendly and technologically improved ear and nasal packing products is growing rapidly across hospitals and outpatient clinics, as healthcare providers prioritize safety, recovery efficiency, and patient comfort

- Increasing collaboration between device manufacturers and hospitals to develop customized packing solutions tailored to specific ENT procedures is also shaping market innovation and adoption patterns

Europe Ear and Nasal Packing Market Dynamics

Driver

Rising ENT Procedures and Increasing Patient Awareness

- The increasing prevalence of ENT disorders and growing numbers of surgical procedures is a significant driver for heightened demand for ear and nasal packing products across Europe

- For instance, in March 2025, Smith & Nephew reported increased adoption of their absorbable nasal packs in German hospitals to manage postoperative epistaxis, highlighting market growth driven by surgical demand

- As awareness of postoperative care, infection prevention, and patient comfort rises, healthcare providers increasingly prefer advanced packing materials that ensure effective hemostasis and reduce complications

- Furthermore, the rising focus on minimally invasive ENT surgeries and outpatient procedures is driving hospitals to adopt patient-friendly and easy-to-use packing solutions for efficient treatment

- The growing emphasis on reducing recovery time, improving surgical outcomes, and enhancing patient experience is propelling the adoption of both absorbable and non-absorbable packs in hospitals and ENT clinics across Europe

- Technological advancements in antimicrobial and hemostatic materials, along with strong clinical support and evidence, are further encouraging hospital procurement of innovative packing solutions

- Government initiatives and healthcare programs promoting standardized postoperative care in ENT surgeries are also boosting product adoption and market growth across key European countries

Restraint/Challenge

Material Sensitivity and Regulatory Compliance Hurdles

- Concerns surrounding allergic reactions, irritation, or improper absorption of certain packing materials pose a significant challenge to broader market adoption. Healthcare providers must carefully select products suitable for sensitive patients

- For instance, high-profile reports of adverse reactions to certain nasal packing foams have made some surgeons hesitant to adopt newer or unfamiliar products, slowing penetration

- Addressing these clinical safety concerns through rigorous testing, compliance with EU medical device regulations, and clear product labeling is crucial for building trust among hospitals and ENT specialists. For instance, companies such as Medtronic and Stryker emphasize CE marking, biocompatibility, and clinical trial data in marketing to reassure buyers

- In addition, the relatively higher cost of advanced absorbable or antimicrobial packing compared to standard gauze can be a barrier for budget-conscious hospitals or outpatient clinics, particularly in smaller European markets

- While prices are gradually decreasing, the perceived premium for innovative ENT packing solutions can still hinder adoption, especially for facilities that do not perform high volumes of ENT procedures. Overcoming these challenges through clinical validation, regulatory compliance, and cost-effective product development is vital for sustained market growth

- Variability in reimbursement policies across European countries for ENT surgical procedures and associated products can limit consistent market uptake, particularly for premium absorbable packs

- Limited awareness among smaller clinics and outpatient centers regarding the benefits of advanced packing solutions may slow adoption, requiring targeted education and marketing by manufacturers

Europe Ear and Nasal Packing Market Scope

The market is segmented on the basis of type, material, distribution channel, and end user.

- By Type

On the basis of type, the Europe ear and nasal packing market is segmented into nasal and ear packs. The nasal packing segment dominated the market with the largest market revenue share of 55.7% in 2025, driven by its widespread use in controlling epistaxis, compatibility with both absorbable and non-absorbable materials, and established effectiveness in surgical and trauma-related ENT procedures. Nasal packs are increasingly preferred by hospitals due to their ability to reduce postoperative bleeding, minimize follow-up procedures, and enhance patient comfort. The segment also benefits from continuous innovation in foam, gel, and bioresorbable materials, making them safer and easier to use. Clinicians often prioritize nasal packing solutions for both emergency care and planned surgeries, contributing to steady revenue growth. Their versatility across adult and pediatric ENT procedures further strengthens their dominant position in the market.

The ear packing segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rising awareness of postoperative care in otologic surgeries and the growing prevalence of ear-related disorders. Ear packs are essential in procedures such as tympanoplasty, mastoidectomy, and trauma management, providing support, hemostasis, and medication delivery. Advances in bioresorbable materials and antimicrobial options are driving adoption, as these products reduce the need for manual removal and lower infection risks. In addition, increasing ENT procedures in outpatient and ambulatory care settings are boosting demand for convenient and patient-friendly ear packing solutions. The growing geriatric population with chronic ear conditions and the rise of pediatric ENT surgeries are also key factors supporting segment growth.

- By Material

On the basis of material, the market is segmented into bio-absorbable and non-absorbable packing materials. The non-absorbable segment dominated the market in 2025, owing to its long-established use, cost-effectiveness, and availability in hospitals and ENT clinics. Non-absorbable packs, such as Merocel® foam or gauze, provide reliable hemostasis and structural support during surgical recovery. Clinicians often prefer them for complex procedures where precise control of bleeding and packing placement is critical. The segment benefits from widespread familiarity among ENT surgeons and robust supply chains across European countries. Non-absorbable materials are also preferred in emergency settings due to their immediate availability and predictable performance.

The bio-absorbable segment is expected to witness the fastest growth rate during the forecast period, driven by increasing preference for patient-friendly and minimally invasive solutions. Bio-absorbable materials dissolve naturally over time, eliminating the need for painful removal procedures and reducing patient discomfort. Advances in drug-eluting bio-absorbable packs delivering antibiotics or hemostatic agents locally are further fueling adoption. Hospitals and outpatient clinics are increasingly using these innovative materials to improve patient satisfaction and recovery outcomes. The growth is further supported by awareness campaigns highlighting the benefits of absorbable packing in pediatric and geriatric ENT care.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender and over-the-counter (OTC). The direct tender segment dominated the market in 2025, driven by large-scale procurement by hospitals, government health programs, and ENT specialty centers. Hospitals prefer direct tender agreements for guaranteed supply, volume discounts, and regulatory compliance with EU medical device standards. This channel ensures timely availability of critical packing products, reduces supply chain interruptions, and allows healthcare providers to negotiate bulk pricing. ENT device manufacturers often establish strong partnerships with hospitals through this channel, further strengthening market dominance.

The OTC segment is anticipated to witness the fastest growth from 2026 to 2033, fueled by increasing patient awareness and rising self-care initiatives for minor nasal bleeding or ear disorders. OTC availability allows patients and smaller clinics to access standard packing products without formal procurement procedures. Growing awareness of first-aid measures for epistaxis and ear conditions, along with online and retail availability of basic packs, is accelerating segment growth. Convenience, affordability, and easy access are key factors driving OTC adoption in both urban and semi-urban European markets.

- By End User

On the basis of end user, the market is segmented into hospitals, clinics, ambulatory centres, and others. The hospital segment dominated the market in 2025, holding the largest revenue share due to the high volume of ENT surgeries, availability of specialized surgeons, and advanced healthcare infrastructure. Hospitals are primary purchasers of both absorbable and non-absorbable packing products and often engage in direct tenders for long-term supply. The dominance is reinforced by the adoption of bioresorbable and antimicrobial packs in major surgical centers, improving patient outcomes and workflow efficiency. Hospitals also drive innovation adoption as they test and validate new packing materials before broader use in smaller healthcare facilities.

The clinics and ambulatory centres segment is expected to witness the fastest growth rate during the forecast period, driven by increasing outpatient ENT procedures, minor surgeries, and follow-up care. Smaller clinics are adopting advanced packing materials to enhance patient comfort, reduce recovery time, and compete with hospital services. The growth is also supported by the rising prevalence of ENT disorders in urban areas and increasing patient preference for convenient, local care options. Enhanced awareness of postoperative care protocols and minimally invasive procedures is further encouraging adoption in clinics and ambulatory centres across Europe.

Europe Ear and Nasal Packing Market Regional Analysis

- Germany dominated the Europe ear and nasal packing market with the largest revenue share of 28.4% in 2025, characterized by advanced healthcare infrastructure, high adoption of innovative ENT devices, and a strong presence of key industry players

- Hospitals and clinics in the region prioritize patient safety, effective hemostasis, and postoperative comfort, making Germany a key revenue-generating market for ENT packing solutions

- This widespread adoption is further supported by well-established healthcare systems, high clinical awareness, and increasing investments in ENT treatment facilities, establishing ear and nasal packing products as essential components of surgical and trauma care

The Germany Ear and Nasal Packing Market Insight

The Germany ear and nasal packing market is expected to expand at a considerable CAGR during the forecast period, fueled by the country’s advanced healthcare system, high volume of ENT surgeries, and strong adoption of innovative absorbable and non-absorbable packs. Hospitals and specialized ENT centers are increasingly using patient-friendly and antimicrobial materials to improve recovery outcomes. Germany’s emphasis on medical technology innovation and surgical efficiency is promoting the uptake of advanced packing solutions. Furthermore, growing clinical awareness and adherence to strict postoperative care protocols are driving demand for nasal and ear packing products. Continuous collaboration between manufacturers and hospitals to develop procedure-specific packing solutions further accelerates market growth.

France Ear and Nasal Packing Market Insight

The France ear and nasal packing market is projected to grow at a noteworthy CAGR during the forecast period, driven by rising ENT surgical procedures, increasing patient awareness, and the adoption of bioresorbable and non-absorbable packing materials in hospitals and clinics. The focus on reducing postoperative complications and enhancing patient comfort is encouraging the use of advanced packing solutions. Government initiatives supporting hospital modernization and improved ENT care infrastructure are further boosting adoption. In addition, outpatient and ambulatory care centers in urban areas are increasingly procuring innovative nasal and ear packs to improve procedural efficiency and patient satisfaction. The rising prevalence of chronic ENT disorders also sustains consistent market demand in France.

U.K. Ear and Nasal Packing Market Insight

The U.K. ear and nasal packing market is expected to grow at a considerable CAGR during the forecast period, fueled by growing ENT surgeries, awareness of postoperative care, and the adoption of innovative absorbable and antimicrobial packing products. Hospitals and clinics are increasingly focusing on patient-friendly solutions to reduce discomfort and accelerate recovery. The U.K.’s well-developed healthcare infrastructure, coupled with clinical expertise and rising patient volumes, supports steady adoption of nasal and ear packing solutions. Rising demand in outpatient and ambulatory centers, along with private ENT practices, further drives market expansion. Collaborative efforts between manufacturers and healthcare providers to improve product efficiency and safety also contribute to growth.

Italy Ear and Nasal Packing Market Insight

The Italy ear and nasal packing market is poised for notable growth during the forecast period, driven by rising awareness of ENT disorders, improving healthcare infrastructure, and increasing surgical procedures in both hospitals and outpatient clinics. The adoption of bioresorbable and non-absorbable packing materials is accelerating due to enhanced patient comfort and reduced need for follow-up interventions. Increasing investments in ENT care modernization and postoperative management protocols are also boosting market demand. Manufacturers are actively promoting procedure-specific packs and antimicrobial options to Italian healthcare providers. In addition, the focus on improving clinical outcomes and minimizing complications in ENT surgeries is expected to sustain market growth across the country.

Europe Ear and Nasal Packing Market Share

The Europe Ear and Nasal Packing industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Stryker (U.S.)

- Smith+Nephew (U.K.)

- Olympus Corporation (Japan)

- Network Medical Products Ltd. (U.S.)

- Lohmann & Rauscher GmbH & Co. KG (Germany)

- Meril Life Sciences Pvt. Ltd. (India)

- Boston Medical Products Inc. (U.S.)

- Fannin Ltd. (Ireland)

- Datt Mediproducts Pvt. Ltd. (India)

- SPIGGLE & THEIS Medizintechnik GmbH (Germany)

- Medasil Surgical Ltd. (U.K.)

- EON Meditech Pvt. Ltd. (India)

- Anand Meditech (India)

- KOKEN CO., LTD. (Japan)

- Boston Scientific Corporation (U.S.)

- B. Braun SE (Germany)

- AptarGroup, Inc. (U.S.)

- NeilMed Pharmaceuticals Inc. (U.S.)

- Summit Medical Group (U.S.)

What are the Recent Developments in Europe Ear and Nasal Packing Market?

- In June 2025, ConMed launched NavPak, a next‑generation bioabsorbable nasal packing device designed to reduce postoperative bleeding and simplify recovery for nasal surgeries, marking a notable product advancement in ENT packing solutions

- In October 2024, Polyganics BV launched the OCEAN Biodegradable nasal dressing across European markets, offering surgeons a bioresorbable packing solution that naturally degrades over time and is compatible with mometasone furoate, helping reduce post‑operative inflammation and bleeding. This innovation supports improved mucosal healing and advances patient‑friendly surgical care within the ENT sector

- In March 2024, Smith & Nephew received regulatory approval for its balloon‑based nasal packing system with integrated pressure monitoring capabilities, showcasing an innovation in nasal packing technology that enables remote pressure monitoring to support ENT postoperative care

- In May 2022, Medtronic completed its acquisition of Intersect ENT, expanding its ENT product portfolio including sinus and postoperative care solutions that complement nasal packing technologies after announcing the deal in August 2021. This acquisition broadens Medtronic’s reach in sinus treatment devices used in both U.S. and European markets

- In August 2021, Medtronic announced it would acquire Intersect ENT for approximately USD 1.1 billion, adding Intersect ENT’s bioabsorbable, drug‑eluting implants for sinus care to its ENT portfolio a move expected to strengthen product offerings that overlap with nasal packing and postoperative ENT treatment solutions globally

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.