Europe Electroencephalography Devices Market

Market Size in USD million

USD

424.05 million

USD

631.31 million

2024

2032

USD

424.05 million

USD

631.31 million

2024

2032

| 2025 - 2032 | |

| USD 424.05 million | |

| USD 631.31 million | |

| % | |

|

Europe Electroencephalography Devices Market Size

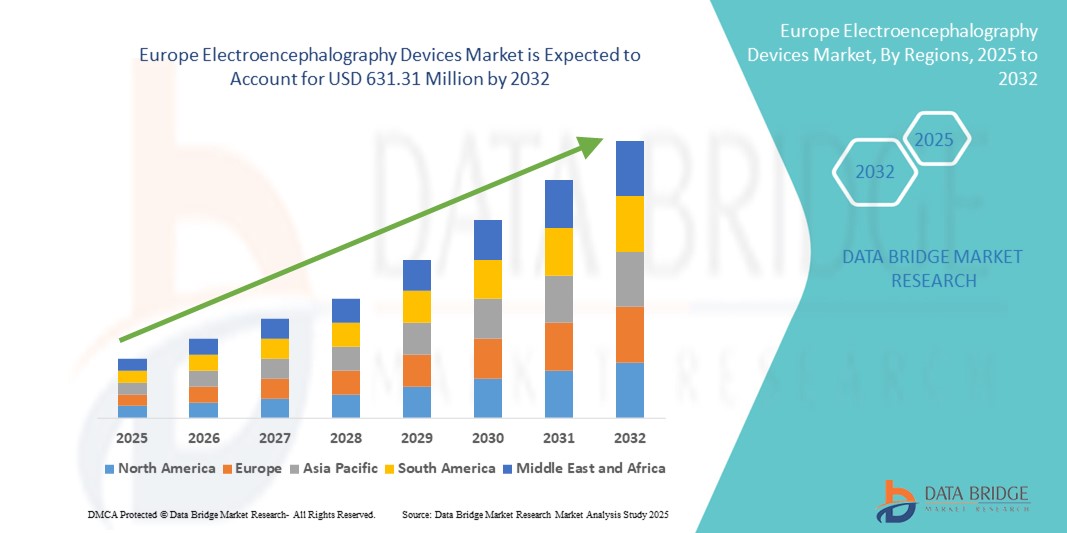

- The Europe electroencephalography devices market size was valued at USD 424.05 million in 2024 and is expected to reach USD 631.31 million by 2032, at a CAGR of 5.10% during the forecast period

- The market growth is largely fueled by the rising prevalence of neurological disorders, including epilepsy, Alzheimer's, and Parkinson's disease, coupled with increasing adoption of advanced EEG technologies such as portable and wearable devices across hospitals and research centers

- Furthermore, growing investments in healthcare infrastructure, research funding for neurodiagnostic tools, and rising demand for non-invasive, user-friendly, and real-time brain monitoring solutions are establishing EEG devices as essential tools in both clinical and consumer applications. These factors are accelerating the adoption of EEG devices, thereby significantly boosting the industry's growth

Europe Electroencephalography Devices Market Analysis

- EEG devices, offering non-invasive monitoring of brain electrical activity, are increasingly vital components of modern neurology, clinical diagnostics, and research applications across hospitals, clinics, and neurotechnology labs due to their enhanced accuracy, real-time monitoring capabilities, and integration with advanced neuroimaging systems

- The escalating demand for EEG devices is primarily fueled by the rising prevalence of neurological disorders such as epilepsy, Alzheimer's, and Parkinson's disease, growing awareness of brain health, and a preference for non-invasive, portable, and wearable monitoring solutions

- Germany dominated the electroencephalography devices market with the largest revenue share of 39.2% in 2024, characterized by advanced healthcare infrastructure, high adoption of neurodiagnostic technologies, and a strong presence of key industry players. EEG device installations are increasing substantially in hospitals and research institutions, driven by innovations in wearable and wireless EEG systems

- France is expected to be the fastest-growing country in the electroencephalography devices market during the forecast period due to rising healthcare investments, increasing prevalence of neurological disorders, and expanding neurodiagnostic facilities

- Portable EEG devices dominated the electroencephalography devices market with a market share of 61% in 2024, driven by their mobility and suitability for use in multiple clinical and research settings

Report Scope and Europe Electroencephalography Devices Market Segmentation

|

Attributes |

Europe Electroencephalography Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Europe Electroencephalography Devices Market Trends

Advancements in Wearable and AI-Enabled EEG Solutions

- A significant and accelerating trend in the European EEG devices market is the integration of artificial intelligence (AI) and the development of wearable EEG solutions. These innovations are enhancing real-time brain monitoring, predictive diagnostics, and user convenience in both clinical and research settings

- For instance, companies such as Neuroelectrics and g.tec medical engineering have introduced wearable EEG headsets capable of continuous monitoring, data transmission to cloud-based platforms, and integration with AI algorithms to analyze brain signals for neurological assessments

- AI integration enables features such as automated detection of abnormal brain activity, predictive modeling for seizure events, and personalized neurofeedback for patients. Similarly, wearable devices allow non-invasive, long-term monitoring outside clinical environments, improving patient comfort and compliance

- The combination of AI analytics with wearable EEG technology allows healthcare providers to access and interpret complex neural data efficiently. Through centralized software platforms, clinicians can track brain activity trends, monitor treatment responses, and adjust therapies in real-time

- This trend towards more intelligent, intuitive, and patient-friendly EEG devices is reshaping expectations for neurodiagnostic tools. Consequently, companies such as NeuroSky are developing AI-enabled portable and wearable EEG devices with features such as continuous monitoring, cloud-based analytics, and predictive alerts for neurological events

- The demand for wearable and AI-powered EEG solutions is growing rapidly across hospitals, research institutions, and consumer neurotechnology applications, as stakeholders increasingly prioritize convenience, real-time insights, and comprehensive brain monitoring capabilities

Europe Electroencephalography Devices Market Dynamics

Driver

Rising Prevalence of Neurological Disorders and Growing Adoption of Advanced Neurodiagnostic Tools

- The increasing prevalence of epilepsy, Alzheimer’s, Parkinson’s, and other neurological disorders, coupled with rising awareness of brain health, is a major driver for the heightened demand for EEG devices

- For instance, in 2024, Neuroelectrics launched advanced portable EEG systems integrated with AI algorithms to assist in epilepsy monitoring, showcasing how innovations by key companies are driving market expansion

- EEG devices offer advanced features such as real-time monitoring, automated abnormality detection, and integration with cloud platforms, providing significant advantages over traditional diagnostic methods

- Furthermore, the growing adoption of telemedicine and remote patient monitoring is making EEG devices an integral component of modern healthcare, enabling continuous monitoring and early detection of neurological issues

- The ability to perform non-invasive, portable, and wearable EEG assessments allows for convenient, patient-friendly diagnostics, further boosting adoption in clinical and research settings

Restraint/Challenge

High Cost of Advanced Systems and Regulatory Compliance Hurdles

- The high cost of advanced EEG devices, particularly wearable and AI-integrated models, poses a challenge to widespread adoption in price-sensitive healthcare markets. Premium features such as cloud analytics, AI predictive tools, and wireless connectivity often come with higher investment requirements

- In addition, compliance with medical device regulations and data privacy laws across European countries adds complexity to market entry and product deployment. Manufacturers must ensure devices meet stringent CE marking standards and GDPR compliance when handling patient data

- For instance, in 2023, a mid-sized clinic in Italy delayed adopting a new AI-enabled EEG system due to concerns over GDPR compliance and the high upfront costs of the technology, illustrating how regulatory and financial barriers can slow market penetration

- Addressing these challenges through cost-effective device designs, streamlined regulatory approvals, and robust cybersecurity protocols will be crucial for expanding market penetration. Companies such as g.tec and NeuroSky emphasize secure data encryption, regulatory adherence, and software validation to build clinician and patient trust

- While prices are gradually decreasing for portable EEG systems, the perceived premium of advanced AI-enabled wearable devices can still limit adoption, particularly in smaller clinics or research labs

- Overcoming these barriers through innovation, education on clinical benefits, and improved affordability will be vital for sustained growth in the European EEG devices market

Europe Electroencephalography Devices Market Scope

The market is segmented on the basis of product type, type, usability, procedure, function, signal frequency, filtering settings, age group, application, end user, and distribution channel.

- By Product Type

On the basis of product type, the electroencephalography devices market is segmented into devices, accessories, and consumables. The devices segment dominated the market with the largest revenue share of 61.3% in 2024, primarily due to increasing investments in neurodiagnostic equipment by hospitals, neurology centers, and research institutions. The demand for devices is also fueled by the shift toward AI-enabled, portable, and wearable EEG systems, which provide real-time brain monitoring, predictive analytics, and enhanced diagnostic accuracy.

Accessories, including EEG caps, electrodes, and lead wires, are witnessing steady growth during forecast period, due to recurring usage in clinical and research procedures, while consumables such as gels, adhesives, and cleaning solutions support consistent device performance and hygiene. These components are critical for maintaining device functionality, ensuring signal quality, and supporting repeated diagnostic procedures.

- By Type

On the basis of type, the electroencephalography devices market is segmented into portable, standalone, and wearable EEG devices. The portable segment dominated with a market share of 61% in 2024, driven by its convenience, mobility, and flexibility to be used in multiple clinical and research environments. Portable EEG systems allow clinicians to conduct rapid assessments in hospitals, outpatient centers, and even patient homes, enhancing accessibility and patient compliance. These devices allow clinicians to perform tests at the patient’s convenience while maintaining diagnostic accuracy.

Wearable EEG devices are expected to witness the fastest growth during the forecast period due to rising consumer neurotechnology applications, long-term monitoring needs, and integration with mobile and cloud platforms for continuous data collection. Standalone EEG systems continue to be widely used in traditional hospital and research setups where fixed installations are preferred for comprehensive neurological testing. Wearable EEGs are increasingly used in cognitive studies, sleep monitoring, neurofeedback therapies, and real-time brain-computer interface (BCI) applications.

- By Usability

On the basis of usability, the electroencephalography devices market is segmented into disposable, semidisposable, and reusable EEG devices. Reusable devices held the largest market share in 2024 due to their long-term cost-effectiveness and ability to serve multiple patients across hospitals and diagnostic centers. Semidisposable devices are gaining traction in specific procedures where partial reusability is required, such as specialized research applications or short-term clinical monitoring. They are a preferred choice for large hospitals and neurology centers with high patient throughput.

Disposable devices are increasingly adopted during forecast period, in hygiene-sensitive procedures, particularly in pediatric and geriatric care, minimizing cross-contamination risks while ensuring accuracy in measurements. These devices provide reliable measurements while ensuring patient safety. Semidisposable devices are increasingly utilized for procedures requiring partial reusability, such as short-term clinical monitoring and experimental research applications

- By Procedure

On the basis of procedure, the electroencephalography devices market is segmented into routine EEG, sleep-deprived EEG, ambulatory EEG, and others. Routine EEG dominates the market due to its widespread application in initial diagnosis, neurological assessments, and monitoring of common disorders such as epilepsy. Ambulatory EEG is witnessing rapid growth, driven by the demand for home-based monitoring, long-term data collection, and patient convenience. Clinicians rely on routine EEG for baseline brain activity measurements and early detection of abnormalities.

Sleep-deprived EEG procedures are steadily increasing during forecast period, especially in epilepsy diagnostics, where deprivation protocols help in capturing abnormal brain activity that may not appear during routine sessions. Increasing in epilepsy diagnostics to capture abnormalities that may not appear in routine sessions. It helps clinicians identify seizure-prone patterns and better design treatment plans.

- By Function

On the basis of function, the electroencephalography devices market is segmented into standard EEG, ambulatory EEG, and video EEG. Standard EEG devices held the largest share in 2024 due to their established use in hospitals and clinics for routine diagnostics. Video EEG is experiencing significant growth owing to its application in seizure monitoring, complex neurological assessments, and integration with AI-based analytics for automated interpretation. Their widespread adoption is reinforced by robust accuracy, ease of operation, and compatibility with hospital IT systems.

Ambulatory EEG continues to gain traction during forecast period, as hospitals, clinics, and research centers increasingly adopt mobile solutions that allow extended monitoring of patients outside traditional clinical environments. Ambulatory systems enable continuous patient tracking over hours or days, providing critical insights into episodic neurological events. The portability and integration with cloud platforms make these devices attractive for home monitoring, remote research studies, and tele-neurology applications.

- By Signal Frequency

On the basis of signal frequency, the electroencephalography devices market is segmented into delta (3 Hz or below), theta (3.5–7.5 Hz), alpha (7.5–13 Hz), and beta (14 Hz or greater). Alpha frequency EEG recordings dominated the market in 2024 due to their importance in monitoring relaxed wakefulness and routine clinical assessments. widely used to monitor relaxed wakefulness and routine clinical assessments. Alpha rhythms are critical in diagnosing cognitive and neurological disorders, and their consistency makes them a standard reference in EEG procedures.

Beta and theta frequencies are growing steadily during forecast period, in research applications, neurofeedback therapies, and advanced diagnostics, enabling better interpretation of cognitive states, sleep patterns, and neurological disorders. Gaining importance in research and advanced diagnostics, particularly for cognitive studies, attention monitoring, and mental workload analysis. Beta rhythms also aid in sleep and neurofeedback therapies. Used increasingly in pediatric neurology, sleep studies, and meditation research. Its slow-wave patterns are useful in developmental disorder assessments, neurorehabilitation, and epilepsy evaluation.

- By Filtering Settings

On the basis of filtering settings, the electroencephalography devices market is segmented into low frequency filter (1 Hz), high frequency filter (50–70 Hz), notch filter, and bandpass filter. Low frequency filter settings dominated in 2024 because of their standard use in clinical EEG diagnostics. Dominates due to standard use in clinical EEG diagnostics, helping remove slow baseline drifts and ensuring stable recordings. It is commonly applied in routine hospital EEGs and research environments.

Bandpass filters are gaining adoption during forecast period, in advanced portable and wearable EEG systems, particularly in AI-enabled devices that require real-time signal processing and noise reduction for accurate brain activity analysis. High frequency and notch filters are increasingly used in research and specialized clinical setups to eliminate interference and improve data precision. Bandpass filtering enhances diagnostic precision, reduces artifacts, and facilitates advanced applications like brain-computer interface integration.

- By Age Group

On the basis of age group, the electroencephalography devices market is segmented into pediatric, adult, and geriatric. Adult patients dominate the EEG devices market due to higher prevalence of neurological disorders and routine monitoring requirements. Dominates due to higher prevalence of neurological disorders such as epilepsy, stroke, and migraines. Adults also undergo frequent cognitive and neurological assessments, driving consistent demand for accurate EEG monitoring in hospitals, clinics, and research institutions.

Pediatric EEG is growing steadily during forecast period, due to support epilepsy diagnostics, developmental disorder assessments, and early detection of neurological conditions in children. Geriatric EEG adoption is increasing due to the rising incidence of Alzheimer’s, Parkinson’s, and other age-related neurological conditions, with wearable and portable solutions offering convenient monitoring in long-term care and home settings. Portable and wearable devices enable child-friendly monitoring, minimizing stress and improving compliance during testing.

- By Application

On the basis of application, the electroencephalography devices market is segmented into disease diagnosis, sleep monitoring, anesthesia monitoring, trauma and surgery, and others. Disease diagnosis dominates the market with the largest share in 2024, driven by rising prevalence of neurological disorders and increased demand for accurate and non-invasive diagnostic solutions. EEG devices are essential for epilepsy evaluation, cognitive disorder assessment, and neurodegenerative disease monitoring.

Sleep monitoring and anesthesia monitoring are witnessing notable growth during forecast period, in hospital and clinical settings due to integration with portable and wearable EEG devices that allow continuous monitoring and improved patient safety during procedures. Trauma and surgical monitoring applications are emerging, particularly in neurosurgery and intensive care, where real-time brain activity tracking is critical. Hospitals, research labs, and home users increasingly rely on EEGs to study sleep patterns, disorders, and therapeutic outcomes.

- By End User

On the basis of end user, the electroencephalography devices market is segmented into hospitals, neurology centers, ambulatory surgical centers, diagnostic centers, academic and research organizations, and others. Hospitals dominated with the largest revenue share in 2024, owing to comprehensive diagnostic facilities, high adoption of advanced EEG devices, and the need to serve large patient volumes. Hospitals utilize EEG for routine assessments, ICU monitoring, and specialized neurology services.

Academic and research organizations are growing rapidly during forecast period, due to increasing investments in neurotechnology research, clinical trials, and experimental applications. Neurology centers and diagnostic centers are expanding EEG adoption for specialized monitoring and routine clinical assessments. Witnessing rapid growth due to investments in neurotechnology research, clinical trials, and experimental studies. Research institutions use EEG extensively for cognitive, behavioral, and brain-computer interface studies.

- By Distribution Channel

On the basis of distribution channel, the electroencephalography devices market is segmented into direct tender and retail sales. Direct tender held the largest share in 2024 due to bulk procurement by hospitals, government healthcare facilities, and large diagnostic chains. Dominates due to bulk procurement by hospitals, government healthcare facilities, and large diagnostic chains. Direct tenders ensure standardized procurement, competitive pricing, and consistent device maintenance services.

Retail sales are growing steadily during forecast period, especially for portable and wearable EEG devices aimed at consumer neurotechnology, home-based monitoring, and smaller clinics, offering convenience, rapid deployment, and accessibility for end users outside traditional hospital settings. Growing steadily for portable and wearable EEG devices aimed at home-based monitoring, smaller clinics, and consumer neurotechnology. Retail availability allows rapid deployment, greater accessibility, and individualized patient or research use without institutional constraints.

Europe Electroencephalography Devices Market Regional Analysis

- Germany dominated the electroencephalography devices market with the largest revenue share of 39.2% in 2024, characterized by advanced healthcare infrastructure, high adoption of neurodiagnostic technologies, and a strong presence of key industry players. EEG device installations are increasing substantially in hospitals and research institutions, driven by innovations in wearable and wireless EEG systems

- Consumers and healthcare providers in the region highly value the accuracy, real-time monitoring capabilities, and integration of EEG devices with cloud-based and AI-enabled platforms, facilitating efficient diagnosis and patient management. Continuous innovation in device technology, including wearable and portable solutions, supports the widespread adoption across hospitals, academic institutions, and specialized neurology centers

- This leading position is further reinforced by strong regulatory support, substantial R&D expenditure, and the presence of prominent EEG device manufacturers, establishing Germany as a key hub for EEG device adoption and technological advancement in Europe

The Germany EEG Devices Market Insight

The Germany electroencephalography devices market dominated the Europe market with the largest revenue share of 39.2% in 2024, driven by a well-established healthcare infrastructure, high adoption of advanced neurodiagnostic tools, and significant investments in R&D and clinical applications. Hospitals, neurology centers, and research institutions in Germany actively deploy portable, wearable, and AI-enabled EEG devices for routine diagnostics, epilepsy monitoring, and neurorehabilitation. Integration of EEG systems with hospital IT platforms and telemedicine services enhances remote monitoring and efficient patient management.

U.K. EEG Devices Market Insight

The U.K. electroencephalography devices market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the increasing adoption of portable and wearable EEG devices for home-based monitoring and telehealth applications. Rising incidence of epilepsy, sleep disorders, and neurodegenerative conditions encourages healthcare providers to integrate standard, ambulatory, and video EEG systems. Strong healthcare infrastructure and awareness about brain health further boost market demand.

France EEG Devices Market Insight

The France electroencephalography devices market is witnessing steady growth due to increasing prevalence of neurological disorders and expansion of specialized neurology centers. Adoption of portable and wearable EEG systems for research and home monitoring is rising, supported by investments in academic institutions and clinical trials. Favorable regulatory and reimbursement frameworks also encourage market expansion.

Italy EEG Devices Market Insight

The Italy electroencephalography devices market is gaining momentum owing to growing demand for advanced neurodiagnostic tools in hospitals, diagnostic centers, and research organizations. AI-enabled portable and wearable EEG devices are increasingly used for disease diagnosis, epilepsy monitoring, and clinical research. Rising awareness of neurological health and telemedicine adoption are expected to drive further growth.

Spain EEG Devices Market Insight

The Spain electroencephalography devices market is poised to grow steadily during the forecast period, driven by the adoption of portable and wearable EEG devices for clinical, research, and home monitoring applications. Government initiatives promoting digital healthcare, rising neurological disorder prevalence, and investments in advanced diagnostic infrastructure support market expansion.

Europe Electroencephalography Devices Market Share

The Europe Electroencephalography Devices industry is primarily led by well-established companies, including:

- Natus Medical Incorporated (U.S.)

- Nihon Kohden Corporation (Japan)

- Compumedics Limited (Australia)

- Neurosoft (Russia)

- Cadwell Industries Inc. (U.S.)

- Micromed Group (Italy)

- Brain Products GmbH (Germany)

- g.tec medical engineering GmbH (Austria)

- NeuroSky Inc. (U.S.)

- Bitbrain Technologies (Spain)

- EMOTIV Inc. (Australia)

- Biosemi B.V. (Netherlands)

- Advanced Brain Monitoring Inc. (U.S.)

- Wearable Sensing (U.S.)

- Masimo Corporation (U.S.)

- Mindray Medical International Limited (China)

- Medtronic (Ireland)

- Integra LifeSciences (U.S.)

- Deymed Diagnostic (Czech Republic)

What are the Recent Developments in Europe Electroencephalography Devices Market?

- In May 2025, Natus announced the launch of BrainWatch, a point-of-care EEG system that can be set up in less than five minutes. Leveraging the NeuroWorks platform, BrainWatch facilitates quick intervention in acute care environments and streamlines treatment decisions with remote neurologist collaboration

- In April 2024, Soterix Medical introduced the MxN-GO EEG system, featuring a lightweight, wire-free design with 33 stimulation channels and 32 recording channels. This system is designed for rapid setup and ease of use, providing precision in neuromodulation applications

- In November 2023, BioSerenity, a leader in EEG technology, announced that its portable EEG device, Neuronaute Plus, received FDA clearance. This device offers simplified EEG recordings, enhancing accessibility for both clinical and home settings. The approval marks a significant step in expanding the availability of advanced EEG monitoring tools

- In March 2022, Bittium presented its next-generation continuous EEG (cEEG) monitoring solution, Bittium BrainStatus with Cerenion C-Trend, at the 65th Congress of the German Society for Clinical Neurophysiology and Functional Imaging (DGKN). This wireless EEG measuring system and analysis tool has medical device approval for the European Union, enhancing monitoring capabilities in acute and intensive care settings

- In January 2022, iMEDISYNC unveiled iSyncWave at CES Las Vegas, the world's first integrated wireless brain EEG device combining EEG brain mapping and LED therapy. This innovative device features high-quality dry EEG sensors that autofit to various sizes and shapes, offering a new approach to brain health monitoring

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.