Europe Epigenetics Diagnostic Market

Market Size in USD Billion

USD

2.08 Billion

USD

5.43 Billion

2024

2032

USD

2.08 Billion

USD

5.43 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.08 Billion | |

| USD 5.43 Billion | |

| % | |

|

Europe Epigenetics Diagnostic Market Size

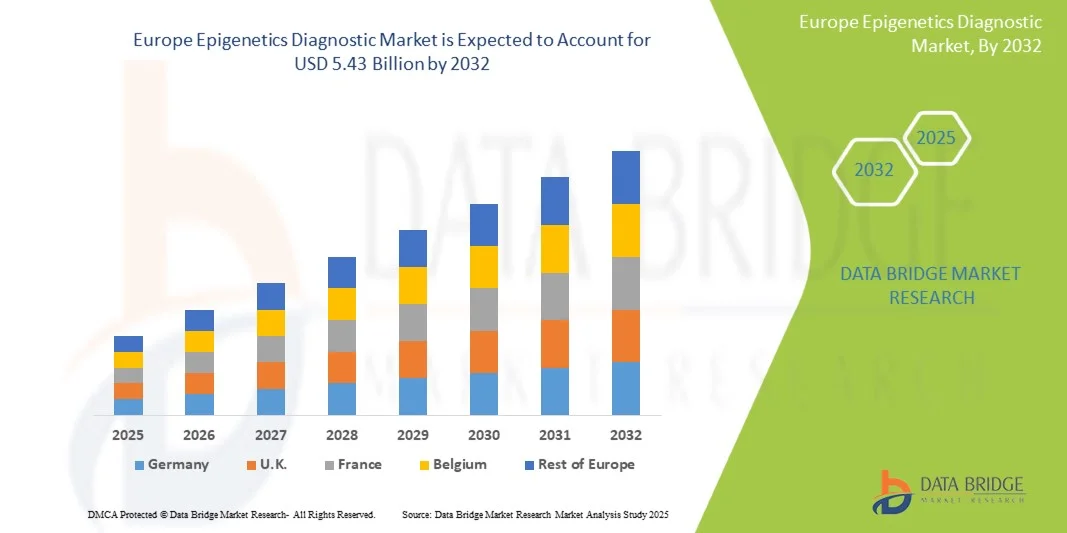

- The Europe epigenetics diagnostic market size was valued at USD 2.08 billion in 2024 and is expected to reach USD 5.43 billion by 2032, at a CAGR of 12.70% during the forecast period

- The market growth is largely fueled by the increasing adoption of advanced molecular biology techniques, high-throughput sequencing, and bioinformatics platforms, which enhance the accuracy, sensitivity, and efficiency of epigenetic diagnostics in both research and clinical applications

- Furthermore, rising demand for early disease detection, personalized medicine, and biomarker-driven diagnostics is driving the adoption of epigenetics diagnostic solutions. These converging factors are accelerating the uptake of epigenetics diagnostic solutions, thereby significantly boosting the industry's growth

Europe Epigenetics Diagnostic Market Analysis

- Epigenetics Diagnostic systems, offering advanced tools for analyzing gene expression and modifications, are increasingly vital components of modern healthcare and research infrastructure in Europe due to their enhanced precision, faster diagnostics, and integration with bioinformatics platforms

- The escalating demand for epigenetics diagnostic solutions is primarily fueled by rising awareness of personalized medicine, increasing incidence of oncology and metabolic diseases, and growing investments in research and development

- Germany dominated the Europe epigenetics diagnostic market in 2024, with contributing the largest revenue share of 36.50% of the European market, driven by advanced healthcare infrastructure, strong R&D investment, and adoption of innovative diagnostic technologies

- France is expected to be the fastest-growing country in Europe epigenetics diagnostic market during the forecast period, fueled by increasing investments in bioinformatics tools, rising awareness of epigenetic therapies, and government initiatives supporting precision medicine

- The oncology segment dominated the Europe epigenetics diagnostic market with 46.3% revenue share in 2024. Rising cancer prevalence, increased early detection initiatives, and adoption of epigenetic biomarkers fuel this dominance

Report Scope and Europe Epigenetics Diagnostic Market Segmentation

|

Attributes |

Europe Epigenetics Diagnostic Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Europe Epigenetics Diagnostic Market Trends

“Intelligent and Hands-Free Epigenetics Diagnostic Systems”

- A significant and accelerating trend in the Europe epigenetics diagnostic market is the deepening integration with artificial intelligence (AI) and popular voice-controlled ecosystems. This fusion of technologies is significantly enhancing user convenience and control over diagnostic and health monitoring systems

- For instance, advanced home-based epigenetics diagnostic kits now allow users to schedule sample collections, access reports, or receive reminders via voice commands. Platforms like BioInsight and EpiGenX integrate seamlessly with major voice assistants, providing users with a convenient hands-free experience for managing their personal health data

- AI integration in epigenetics diagnostics enables features such as monitoring gene expression patterns, analyzing longitudinal lifestyle and health data, and providing predictive insights for personalized interventions. Some platforms leverage AI to detect unusual trends in biomarkers and alert users for timely action, thereby improving overall health management

- Voice control capabilities offer the ease of hands-free operation, enabling users to interact with diagnostic platforms remotely using simple verbal commands. This functionality enhances accessibility, particularly for individuals with mobility limitations or busy schedules, allowing them to maintain proactive health monitoring

- The seamless integration of epigenetics diagnostic platforms with digital assistants and broader health ecosystems facilitates centralized control over multiple monitoring and analytical tools. Users can manage sample data, track trends, and receive actionable insights from a single interface, creating a unified and automated personal health management experience

- • This trend towards intelligent, intuitive, and interconnected diagnostic systems is fundamentally reshaping consumer expectations in preventive healthcare. Companies such as BioInsight and EpiGenX are developing AI-enabled platforms with features such as automated risk assessment, personalized guidance, and voice command functionality across major digital assistants

- The demand for epigenetics diagnostic solutions that combine AI and voice control integration is growing rapidly across both individual consumers and clinical healthcare providers, as convenience, personalization, and comprehensive health insights become key priorities

Europe Epigenetics Diagnostic Market Dynamics

Driver

“Growing Need Due to Rising Health Awareness and Personalized Medicine Adoption”

- The increasing prevalence of health awareness among consumers, combined with the growing adoption of personalized medicine approaches, is a significant driver for the heightened demand for epigenetics diagnostics. Consumers are increasingly seeking insights into their genetic predispositions, disease risks, and lifestyle-related health factors to enable proactive management

- For instance, in April 2024, BioTech Health announced the launch of a new home-based epigenetics diagnostic kit capable of providing insights into gene expression patterns, lifestyle risk factors, and personalized health recommendations. Such innovations by key market players are expected to drive Epigenetics Diagnostic market growth during the forecast period

- As individuals become more proactive about their health, epigenetics diagnostics offer advanced insights into potential disease risks, treatment responses, and personalized wellness strategies, providing a more comprehensive alternative to traditional diagnostic methods

- Furthermore, the integration of diagnostic platforms with AI and mobile health applications allows users to interpret complex genetic data more effectively, enabling better-informed decisions for preventive care and lifestyle interventions

- The convenience of home-based sample collection, personalized reporting, and actionable health insights are key factors propelling the adoption of epigenetics diagnostics in both consumer and clinical settings. The growing trend toward self-managed health monitoring and the availability of user-friendly diagnostic kits further contribute to market expansion

Restraint/Challenge

“Concerns Regarding Data Privacy and High Initial Costs”

- Concerns surrounding the privacy and security of personal and genetic data pose a significant challenge for the broader adoption of epigenetics diagnostics. These platforms often rely on cloud storage, AI-driven analytics, and network connectivity, which could be vulnerable to data breaches or unauthorized access, creating hesitation among potential users

- High-profile reports regarding vulnerabilities in digital health systems have made some consumers cautious about adopting home-based or connected diagnostic solutions, despite their clinical or preventive benefits

- Addressing these privacy concerns through robust encryption protocols, secure authentication measures, and compliance with data protection regulations such as GDPR is critical to building consumer trust. Companies such as BioInsight and EpiGenX emphasize advanced data security features in their marketing to reassure users

- In addition, the relatively high initial cost of advanced epigenetics diagnostic kits compared to conventional testing methods can be a barrier for adoption, particularly in price-sensitive regions or among budget-conscious consumers. While basic testing kits are becoming more affordable, premium solutions that integrate AI analytics, personalized reporting, and digital assistant compatibility often carry higher price point

- Although prices are gradually decreasing, the perceived premium for advanced diagnostic technology can still limit adoption, particularly among individuals who do not immediately recognize the value of comprehensive genetic insights

- Overcoming these challenges through improved data security, user education on privacy and benefits, and the development of more cost-effective epigenetics diagnostic solutions will be crucial for sustained market growth

Europe Epigenetics Diagnostic Market Scope

The market is segmented on the basis of product, technology, type of therapy, application, end user, and distribution channel.

• By Product

On the basis of product, the epigenetics diagnostic market is segmented into reagents, kits, instruments & consumables, and bioinformatics tools & enzymes. The reagents segment dominated the largest market revenue share of 42.8% in 2024. This is driven by their essential role in sample preparation, detection, and analysis across epigenetic studies. Reagents are highly reliable, compatible with multiple assay platforms, and provide reproducible results, making them indispensable in both research and clinical diagnostics. The growing adoption of precision medicine and biomarker-based diagnostics further propels demand. Academic research and pharmaceutical companies rely heavily on high-quality reagents to achieve consistent outcomes. Moreover, specialized reagents for DNA methylation, histone modifications, and RNA analysis strengthen their market position. The segment benefits from continuous innovation in reagent formulation and improved shelf life. Rising investment in epigenetic research globally supports market growth. Reagents also facilitate automation in high-throughput laboratories.

The instruments & consumables segment is anticipated to witness the fastest CAGR of 20.3% from 2025 to 2032. This growth is fueled by increasing demand for high-throughput, automated, and precise epigenetic diagnostic platforms. Instruments such as next-generation sequencers and real-time PCR machines enhance assay accuracy and reproducibility. The segment benefits from trends toward miniaturized and portable devices suitable for decentralized labs. Consumables like tips, plates, and tubes are critical for assay reliability and efficiency. Rising adoption in hospitals, research institutes, and biotech companies drives volume demand. Advanced automation reduces human error and processing time. Increasing investments in personalized medicine and targeted therapies further boost adoption. New instrument launches with integrated software solutions attract end users seeking streamlined workflows. Emerging applications in oncology, cardiovascular, and metabolic research propel growth further.

• By Technology

On the basis of technology, the epigenetics diagnostic market is segmented into DNA methylation, histone methylation, chromatin structures, histone acetylation, and large non-coding RNA & microRNA modification. The DNA methylation segment dominated with a revenue share of 44.5% in 2024, as it is a key biomarker in cancer, cardiovascular, and metabolic diseases. Its widespread adoption stems from cost-effective, reproducible assays and validated clinical utility. DNA methylation is crucial for early disease detection and prognosis, supporting clinical decision-making. Both research labs and diagnostic companies extensively use DNA methylation profiling. Its applications in precision medicine and epigenetic therapy monitoring enhance demand. Established assay kits and platforms provide reliability and ease of use. Regulatory approvals for diagnostic tests based on DNA methylation biomarkers further strengthen market position. The segment’s growth is backed by increasing public and private funding in epigenetics research.

The histone methylation segment is expected to witness the fastest CAGR of 19.6% from 2025 to 2032. The growth is driven by its role in understanding disease progression and identifying therapeutic targets. Histone methylation profiling is increasingly adopted in oncology and inflammatory disease research. Advanced detection techniques, including ChIP-seq, enhance sensitivity and precision. Demand is rising in both academic and pharmaceutical sectors. New assay kits and instruments targeting histone modifications are being launched. Research in chromatin remodeling and epigenetic therapy development fuels adoption. High throughput and automated platforms improve scalability and efficiency. Global initiatives for epigenetic research support expansion. Integration with computational biology and bioinformatics strengthens analytical capabilities. Histone methylation is becoming essential in personalized medicine applications.

• By Type of Therapy

On the basis of type of therapy, the epigenetics diagnostic market is segmented into histone deacetylase (HDAC) inhibitors, DNA methyltransferase (DNMT) inhibitors, and others. The HDAC inhibitors segment dominated the market with a 40.2% revenue share in 2024. They are widely used in cancer treatment and clinical research due to their ability to modulate gene expression epigenetically. HDAC inhibitors have well-established clinical pipelines, making them highly adopted in hospitals and pharmaceutical studies. Their therapeutic relevance in hematologic and solid tumors drives demand. The segment benefits from ongoing R&D in combination therapies. Regulatory approvals for multiple HDAC inhibitors provide market credibility. Academic research exploring HDAC pathways sustains consistent use. Pharma companies invest in HDAC inhibitor-based drug discovery. HDAC inhibitors are applied in inflammatory and metabolic disease research. Established manufacturing processes and reproducibility of compounds strengthen adoption. Clinical trial activity globally supports steady market growth. Continuous innovation in HDAC formulations ensures segment dominance.

The DNMT inhibitors segment is projected to register the fastest CAGR of 18.9% from 2025 to 2032. Growth is driven by increased research in epigenetic therapy and personalized medicine. DNMT inhibitors target DNA methylation patterns linked to cancer and other chronic diseases. Rising clinical trials exploring DNMT inhibitors expand adoption. Academic and pharmaceutical labs increasingly implement DNMT inhibitor studies. Combination therapy research enhances their application scope. Emerging markets are investing in DNMT inhibitor accessibility. Technological advances in formulation and delivery improve efficacy. Awareness of epigenetic targets in cardiovascular and metabolic diseases further boosts growth. Continuous pipeline expansion by pharma companies supports market momentum. DNMT inhibitors are increasingly incorporated into precision medicine initiatives. Adoption is further reinforced by growing government and private funding.

• By Application

On the basis of application, the epigenetics diagnostic market is segmented into oncology, cardiovascular diseases, metabolic diseases, immunology, inflammatory diseases, infectious diseases, and others. The oncology segment dominated the market with 46.3% revenue share in 2024. Rising cancer prevalence, increased early detection initiatives, and adoption of epigenetic biomarkers fuel this dominance. Oncology applications rely heavily on DNA methylation, histone modifications, and non-coding RNA profiling. Clinical utility in prognosis, therapy selection, and treatment monitoring drives demand. Both hospitals and research institutes extensively adopt oncology-focused epigenetic diagnostics. Commercial companies develop oncology-specific kits and instruments. Funding for cancer research supports continual growth. Integration with high-throughput platforms allows efficient screening of large patient cohorts. Advanced bioinformatics tools enhance actionable insights. Government initiatives promoting cancer screening further boost adoption. Collaborations between diagnostic firms and oncology centers strengthen market presence.

The cardiovascular diseases segment is expected to witness the fastest CAGR of 19.2% from 2025 to 2032. Growth is fueled by emerging research linking epigenetic mechanisms to heart disease. Adoption of epigenetic diagnostic tools for early detection and risk stratification is increasing. Hospitals and research labs are investing in biomarker profiling. DNA methylation and histone modification assays are applied in cardiovascular research. Technological advancements in detection platforms enhance accuracy and throughput. Increasing prevalence of cardiovascular disorders worldwide drives market potential. Academic studies and pharmaceutical R&D contribute to rising adoption. Integration with personalized medicine programs accelerates growth. Investment in diagnostic infrastructure supports accessibility. Awareness campaigns and clinical guidelines incorporating epigenetics further propel demand.

• By End User

On the basis of end user, the epigenetics diagnostic market is segmented into academic and research institutes, pharmaceutical and biotechnology companies, contract research organizations (CROs), and others. The academic and research institutes segment accounted for the largest market revenue share of 43.7% in 2024. Institutions conduct extensive epigenetics research, focusing on biomarker discovery, disease mechanisms, and therapeutic development. Availability of research grants and funding strengthens adoption. High investment in molecular biology infrastructure supports sophisticated assays. Collaboration with pharmaceutical companies ensures access to reagents, kits, and instruments. Research output drives innovation in epigenetic diagnostics. Integration with bioinformatics platforms improves analysis and reproducibility. Training of skilled personnel ensures optimal utilization of tools. Global research initiatives in oncology, cardiovascular, and metabolic diseases support segment dominance. Peer-reviewed publications and patent activities sustain long-term demand. Continuous expansion of research programs fuels reagent and instrument consumption.

The pharmaceutical and biotechnology companies segment is expected to witness the fastest CAGR of 18.5% from 2025 to 2032. Companies focus on drug discovery, epigenetic therapy development, and clinical trials. Rising investment in precision medicine accelerates adoption. CRO partnerships enhance scalability and expertise. Demand for high-quality reagents, instruments, and bioinformatics tools is increasing. Advanced technologies enable better compound screening and efficacy evaluation. Pharma R&D pipelines in oncology and metabolic disorders drive market growth. Emerging applications in immunology and infectious diseases support expansion. Strategic collaborations with academic institutes facilitate knowledge transfer. Regulatory approvals of novel diagnostics bolster adoption. Global competition encourages continuous innovation.

• By Distribution Channel

On the basis of distribution channel, the epigenetics diagnostic market is segmented into direct tender and retail sales. The direct tender segment dominated the market in 2024, accounting for the largest revenue share of approximately 48.5%. This dominance is primarily due to the preference of hospitals, academic institutions, and large research organizations to procure high-value diagnostic instruments and reagents directly from manufacturers or authorized distributors. Direct tender ensures reliability, bulk purchasing benefits, and better after-sales support, which is crucial for sophisticated epigenetic diagnostic tools. Large-scale end users often prefer this channel as it allows them to negotiate customized contracts, receive technical training, and ensure uninterrupted supply for critical research and clinical applications. Moreover, direct tender offers the advantage of access to premium products, advanced technologies, and comprehensive maintenance services, which are essential for precise diagnostics. The segment benefits from long-term agreements with leading manufacturers, ensuring consistent product quality and regulatory compliance. In addition, direct tender facilitates better integration of instruments, reagents, and bioinformatics tools, which is crucial for streamlined workflows in research and clinical laboratories. The high-value nature of products, including instruments, kits, and bioinformatics software, makes direct tender the preferred channel among institutional buyers. Furthermore, manufacturers often provide tailored solutions and post-installation technical support through this channel, enhancing customer loyalty and repeat purchases.

The retail sales segment is expected to witness the fastest CAGR of 18.3% from 2025 to 2032. This growth is driven by the increasing accessibility of epigenetic diagnostic kits, reagents, and consumables for smaller laboratories, specialty clinics, and individual researchers. Retail channels offer convenience and faster procurement cycles, enabling smaller end users to adopt cutting-edge technologies without engaging in complex tender processes. The expansion of e-commerce platforms and online marketplaces has further accelerated the adoption of retail sales, allowing researchers and clinical labs to purchase instruments, consumables, and bioinformatics tools directly with minimal lead time. In addition, the growing trend of personalized medicine and demand for at-home or decentralized testing kits contribute to the rising adoption of retail sales channels. Retail channels also facilitate broader market penetration in semi-urban and regional markets, where direct tender may be less accessible. Manufacturers are increasingly offering bundled solutions and promotional packages through retail, enhancing affordability and adoption. Moreover, retail sales channels help in creating brand visibility, expanding reach to new end users, and enabling faster feedback collection for product improvement.

Europe Epigenetics Diagnostic Market Regional Analysis

- Germany dominated the Europe epigenetics diagnostic market in 2024, with contributing the largest revenue share of 36.50% of the European market, driven by advanced healthcare infrastructure, strong R&D investment, and adoption of innovative diagnostic technologies

- France is expected to be the fastest-growing country in Europe epigenetics diagnostic market during the forecast period, fueled by increasing investments in bioinformatics tools, rising awareness of epigenetic therapies, and government initiatives supporting precision medicine

- Europe is witnessing significant growth across oncology, cardiovascular, metabolic, and immunology applications, with diagnostics being increasingly integrated into clinical workflows and research programs

Germany Epigenetics Diagnostic Market Insight

The Germany epigenetics diagnostic market is expected to expand at a considerable rate with contributing the largest revenue share of 36.50% of the European market in 2024, fueled by strong emphasis on research and innovation, rising demand for precision diagnostics, and the integration of advanced bioinformatics tools in clinical and research settings. Germany’s well-developed healthcare infrastructure, focus on sustainability, and high R&D expenditure promote the adoption of epigenetics diagnostics in hospitals, specialty clinics, and research institutions. The increasing prevalence of oncology and metabolic disorders is also driving the demand for advanced diagnostic solutions.

France Epigenetics Diagnostic Market Insight

The France epigenetics diagnostic market is projected to grow at a significant CAGR during the forecast period, driven by government support for precision medicine, increasing research activities in genomics and epigenetics, and rising adoption of advanced diagnostic technologies in clinical practice. Growing awareness of personalized treatment approaches and the prevalence of chronic and infectious diseases are further encouraging the adoption of epigenetics diagnostic tools. Strong collaboration between research institutes, pharmaceutical companies, and healthcare providers is expected to continue fueling market growth in France.

Europe Epigenetics Diagnostic Market Share

The epigenetics diagnostic industry is primarily led by well-established companies, including:

- PerkinElmer (U.S.)

- Diagenode (Belgium)

- F. Hoffman-La Roche Ltd (Switzerland)

- EpiCypher (U.S.)

- Promega Corporation (U.S.)

- QIAGEN (Germany)

- PacBio (U.S.)

- Epigenomics AG (Germany)

- Reaction Biology (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- Agilent Technologies, Inc. (U.S.)

- Merck KGaA (Germany)

- Illumina, Inc. (U.S.)

- ACTIVEMOTIF (U.S.)

- Thermo Fisher Scientific, Inc. (U.S.)

- EpiGentek Group Inc. (U.S.)

- Enzo Life Sciences, Inc. (U.S.)

- Epizyme, Inc. (U.S.)

Latest Developments in Europe Epigenetics Diagnostic Market

- In July 2024, the European Commission announced the launch of the Horizon Europe program's new funding call, focusing on "Innovative Epigenetic Diagnostics for Precision Medicine." This initiative aims to support collaborative research projects across EU member states, facilitating the development of advanced epigenetic diagnostic tools to enhance early disease detection and personalized treatment strategies. The program underscores Europe's commitment to advancing healthcare through innovative technologies

- In March 2025, the UK Department of Health and Social Care published a strategic report titled "Advancing Epigenetic Diagnostics in the NHS." The report outlines plans to integrate epigenetic testing into routine clinical practice, particularly for oncology and cardiovascular diseases, aiming to improve diagnostic accuracy and patient outcomes. This initiative reflects the UK's dedication to incorporating cutting-edge diagnostic technologies into its national healthcare system

- In June 2025, the French National Institute of Health and Medical Research (INSERM) announced a collaborative project with several biotech companies to develop a novel epigenetic biomarker panel for early detection of neurodegenerative diseases. The project, funded by the French government, aims to bring innovative diagnostic solutions to clinical settings, enhancing the ability to diagnose conditions like Alzheimer's disease at earlier, more treatable stages

- In August 2025, Germany's Federal Ministry of Education and Research (BMBF) launched a national initiative to establish "Epigenomics Centers of Excellence." These centers are tasked with advancing research in epigenetics and translating findings into clinical applications, including the development of diagnostic tests for various diseases. The initiative highlights Germany's leadership in fostering innovation and research in the field of epigenetics

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.