Europe Fetal Monitoring Market

Market Size in USD Billion

CAGR :

%

USD

3.55 Billion

USD

6.54 Billion

2025

2033

USD

3.55 Billion

USD

6.54 Billion

2025

2033

| 2026 –2033 | |

| USD 3.55 Billion | |

| USD 6.54 Billion | |

| % | |

|

Europe Fetal Monitoring Market Size

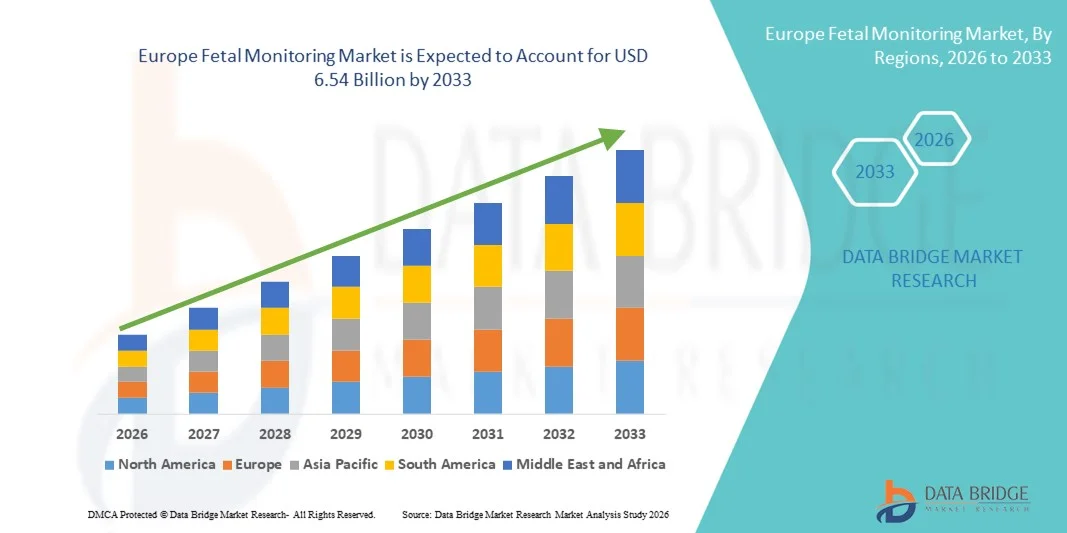

- The Europe fetal monitoring market size was valued at USD 3.55 billion in 2025 and is expected to reach USD 6.54 billion by 2033, at a CAGR of 7.95% during the forecast period

- The market growth is largely fueled by ongoing investments in maternal healthcare infrastructure, rising awareness of prenatal care benefits, and the adoption of advanced fetal monitoring technologies across European healthcare facilities

- Furthermore, stringent healthcare regulations, strong hospital networks in countries such as Germany, the U.K., and France, and a growing emphasis on reducing maternal and neonatal complications are increasing demand for efficient fetal monitoring devices. These converging factors are accelerating the uptake of fetal monitoring solutions, thereby significantly boosting the industry’s growth

Europe Fetal Monitoring Market Analysis

- Fetal monitoring devices, used for assessing fetal health and detecting complications during pregnancy, are becoming increasingly essential in European maternal healthcare due to their ability to provide continuous, real-time monitoring, reduce risks during labor, and support clinical decision-making in hospitals and maternity centers

- The rising demand for fetal monitoring is primarily driven by increased awareness of prenatal care, technological advancements in non-invasive and wireless monitoring devices, and the growing focus on reducing maternal and neonatal complications

- Germany dominated the Europe fetal monitoring market with the largest revenue share of 28.5% in 2025, supported by advanced healthcare infrastructure, high healthcare expenditure, and strong adoption of cutting-edge medical devices, with hospitals and clinics widely using both electronic fetal monitoring and ultrasound solutions

- France is expected to be the fastest-growing country driven by increasing investments in maternal healthcare, rising prenatal awareness among expectant mothers, and the expanding adoption of portable and non-invasive fetal monitoring devices

- Electronic fetal monitoring segment dominated the Europe fetal monitoring market in 2025 with a market share of 42.7%, driven by its widespread use in intrapartum and antepartum monitoring, reliability in detecting fetal heart rate patterns, and integration with hospital information systems for real-time clinical decision support

Report Scope and Europe Fetal Monitoring Market Segmentation

|

Attributes |

Europe Fetal Monitoring Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Europe Fetal Monitoring Market Trends

Integration of Wireless and Portable Monitoring Solutions

- A significant and accelerating trend in the Europe fetal monitoring market is the adoption of wireless and portable monitoring devices, enabling real-time maternal and fetal health tracking both in hospitals and home settings

- For instance, the HeraBEAT wireless fetal monitor allows expectant mothers to transmit fetal heart rate data directly to clinicians via smartphone apps, supporting remote prenatal care

- Portable and wireless fetal monitors facilitate continuous monitoring without restricting maternal mobility, enhancing comfort during labor and prenatal checkups

- The integration of these devices with hospital IT systems enables centralized data collection and analytics, supporting improved clinical decision-making and early complication detection

- This trend towards connected, user-friendly, and mobile fetal monitoring devices is reshaping maternal care expectations, prompting companies such as Monica Healthcare to develop wearable fetal monitors with wireless and cloud-enabled features

- The demand for portable, non-invasive fetal monitoring solutions is growing rapidly across hospitals and clinics, as both healthcare providers and expectant mothers prioritize convenience and real-time health insights

- Increasing integration of fetal monitoring devices with telemedicine platforms allows remote consultations, enhancing prenatal care access in rural and underserved areas

- Adoption of AI-driven analytics in fetal monitoring systems is enabling predictive insights for early detection of complications, further improving maternal and neonatal outcomes

Europe Fetal Monitoring Market Dynamics

Driver

Increasing Focus on Maternal and Neonatal Safety

- The rising awareness of prenatal care and the need to minimize fetal and maternal complications is a significant driver for fetal monitoring adoption

- For instance, in March 2025, GE Healthcare launched the Corometrics wireless fetal monitoring system in France, emphasizing improved maternal safety and early detection of complications

- Fetal monitors provide continuous heart rate tracking, contraction monitoring, and alerts for abnormal readings, offering superior clinical oversight compared to manual checks

- Growing investment in advanced maternal healthcare infrastructure across Germany, France, and the U.K. is driving the deployment of high-end monitoring solutions

- The increasing adoption of digital health platforms and telemedicine integration is further supporting demand, allowing clinicians to monitor fetal health remotely and provide timely interventions

- Government initiatives and healthcare policies promoting maternal and neonatal safety are encouraging hospitals and clinics to upgrade to modern fetal monitoring systems

- Rising patient preference for non-invasive and continuous monitoring solutions is pushing healthcare providers to adopt advanced electronic and telemetry-based fetal monitors

Restraint/Challenge

High Costs and Limited Skilled Workforce

- The relatively high cost of advanced fetal monitoring devices can limit adoption, particularly in smaller clinics or low-budget healthcare facilities

- For instance, the Sonicaid Team 3 fetal monitor is priced higher than basic Doppler devices, which may discourage smaller maternity centers from investing

- In addition, proper use of fetal monitoring systems requires trained healthcare professionals, creating challenges in regions with limited skilled workforce availability

- Inconsistent reimbursement policies for fetal monitoring services in some European countries can also hinder widespread adoption

- Overcoming these challenges requires cost-effective devices, training programs for clinicians, and supportive healthcare policies to encourage adoption in both hospitals and clinics

- Variability in hospital infrastructure and IT readiness can affect integration of advanced fetal monitoring solutions, limiting efficiency gains

- Concerns regarding data privacy and secure handling of patient monitoring information may slow adoption of cloud-enabled and remote fetal monitoring platforms

Europe Fetal Monitoring Market Scope

The market is segmented on the basis of product, method, mobility, application, and end use

- By Product

On the basis of product, the Europe fetal monitoring market is segmented into ultrasound, intrauterine pressure catheter (IUPC), telemetry solutions, electronic fetal monitoring, fetal electrodes, fetal doppler, accessories and consumables, and others. The Electronic Fetal Monitoring (EFM) segment dominated the market with the largest revenue share of 42.7% in 2025, driven by its widespread use in both intrapartum and antepartum monitoring. Hospitals in Germany, France, and the U.K. rely heavily on EFM for continuous fetal heart rate and contraction monitoring, allowing clinicians to detect abnormalities early and intervene promptly. EFM systems also integrate with hospital IT networks for centralized patient data management, supporting better clinical decision-making. The reliability and accuracy of EFM, along with real-time alerts for abnormal readings, make it the preferred choice for high-risk pregnancies. Adoption is further supported by government initiatives promoting maternal and neonatal health and by hospitals upgrading to advanced monitoring systems.

The Telemetry Solutions segment is expected to witness the fastest growth, with a projected CAGR of 8.5% from 2026 to 2033, fueled by the demand for wireless and remote monitoring capabilities. Telemetry solutions allow expectant mothers greater mobility during labor while transmitting continuous fetal data to central monitoring stations. The growing adoption of portable telemetry devices in hospitals and maternity clinics is driven by their ability to improve patient comfort, enable real-time data analytics, and integrate with telemedicine platforms. Rising awareness of maternal health and increasing investments in digital hospital infrastructure are also contributing to the rapid growth of this segment.

- By Method

On the basis of method, the Europe fetal monitoring market is segmented into invasive and non-invasive. The Non-Invasive segment dominated the market in 2025, accounting for 65% of the revenue share, due to its ease of use, patient comfort, and low risk of infection. Non-invasive fetal monitors, including external electronic fetal monitors and Doppler devices, are preferred in most hospitals for routine prenatal and labor monitoring. Clinicians favor non-invasive methods for their ability to provide reliable fetal heart rate and uterine contraction data without requiring surgical procedures. In addition, the non-invasive approach supports maternal mobility and can be used in home-based monitoring scenarios with portable devices. The segment benefits from technological advancements, including wireless monitoring, AI integration for predictive analysis, and telemedicine connectivity.

The Invasive segment is expected to register the fastest growth, with a CAGR of 7.9% from 2026 to 2033, driven by its critical role in high-risk pregnancies where accurate and continuous fetal monitoring is essential. Invasive methods such as the Intrauterine Pressure Catheter (IUPC) and fetal scalp electrodes provide precise measurements of uterine contractions and fetal heart activity, which are particularly important during labor complications. The increasing number of high-risk pregnancies in Europe and the demand for precise intrapartum monitoring are supporting growth in this segment. Hospitals with advanced labor and delivery units are increasingly adopting invasive monitoring systems alongside non-invasive solutions to optimize maternal and neonatal outcomes.

- By Mobility

On the basis of mobility, the market is segmented into portable and non-portable. The Non-Portable segment dominated the Europe fetal monitoring market in 2025, capturing 58% of the market share, primarily due to the wide installation of fixed monitoring systems in hospitals and maternity clinics. Non-portable monitors, including centralized electronic fetal monitoring systems, provide continuous and reliable data for labor wards. These systems are preferred for high-risk cases where uninterrupted monitoring and integration with hospital IT systems are critical. Hospitals in Germany, France, and the U.K. continue to rely on non-portable systems for labor management and neonatal risk mitigation. The segment’s dominance is further supported by clinical trust, regulatory approvals, and long-standing usage in established hospital infrastructures.

The Portable segment is expected to witness the fastest growth, with a CAGR of 8.2% from 2026 to 2033, driven by the rising adoption of wireless and wearable fetal monitors. Portable devices allow for remote monitoring, home-based prenatal care, and enhanced patient comfort during labor. Increasing awareness among expectant mothers, coupled with advancements in battery life, connectivity, and data analytics, is boosting adoption of portable fetal monitoring solutions. Telemedicine integration and demand for mobility-friendly solutions in maternity clinics also contribute to the rapid growth of this segment.

- By Application

On the basis of application, the market is segmented into intrapartum fetal monitoring and antepartum fetal monitoring. The Intrapartum Fetal Monitoring segment dominated the Europe market in 2025 with a share of 55%, driven by the need for real-time monitoring during labor to prevent complications. Hospitals and maternity centers rely on intrapartum monitoring to detect fetal distress, abnormal heart rate patterns, and uterine contraction irregularities. Adoption is supported by government safety guidelines, hospital protocols, and increasing high-risk pregnancies. The availability of integrated electronic monitoring systems enhances clinical efficiency and provides actionable data for timely interventions.

The Antepartum Fetal Monitoring segment is expected to witness the fastest growth, with a CAGR of 9% from 2026 to 2033, fueled by rising awareness of prenatal care and early detection of fetal complications. Non-invasive antepartum monitoring solutions, including Doppler devices and portable electronic fetal monitors, are increasingly being adopted in hospitals and home-care settings. Telemedicine-enabled antepartum monitoring also supports remote care for high-risk pregnancies, enhancing patient comfort and convenience. The segment’s growth is further strengthened by maternal health campaigns and increased hospital investments in prenatal care technologies.

- By End Use

On the basis of end use, the market is segmented into hospitals, clinics, and others. The Hospitals segment dominated the market in 2025, accounting for 70% of the revenue share, due to high adoption of advanced fetal monitoring devices and centralized monitoring systems. Hospitals provide continuous care for high-risk pregnancies, and labor wards rely heavily on electronic fetal monitoring, telemetry solutions, and both invasive and non-invasive devices. Government and private hospital investments in digital health infrastructure further support this segment’s dominance.

The Clinics segment is expected to witness the fastest growth, with a CAGR of 8.7% from 2026 to 2033, driven by the rising adoption of portable and home-use fetal monitoring devices. Prenatal care clinics are increasingly using non-invasive and wireless monitors for routine checkups and remote patient monitoring. The growing focus on maternal wellness, coupled with telemedicine integration, is encouraging clinics to invest in smart fetal monitoring technologies. Clinics benefit from cost-effective solutions and flexibility in monitoring multiple patients efficiently, supporting rapid segment growth.

Europe Fetal Monitoring Market Regional Analysis

- Germany dominated the Europe fetal monitoring market with the largest revenue share of 28.5% in 2025, supported by advanced healthcare infrastructure, high healthcare expenditure, and strong adoption of cutting-edge medical devices, with hospitals and clinics widely using both electronic fetal monitoring and ultrasound solutions

- Healthcare providers in the country highly prioritize accuracy, real-time monitoring, and integration of fetal monitoring systems with hospital IT networks, ensuring improved maternal and neonatal outcomes

- This strong adoption is further supported by government initiatives promoting maternal and neonatal health, the presence of leading medical device companies, and increasing awareness among expectant mothers, establishing Germany as a key hub for fetal monitoring solutions in Europe

The U.K. Fetal Monitoring Market Insight

The U.K. fetal monitoring market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising awareness of prenatal care and maternal health safety. Concerns regarding fetal distress and neonatal complications are encouraging hospitals and clinics to adopt advanced electronic and telemetry-based fetal monitoring devices. The U.K.’s robust healthcare infrastructure, combined with increasing adoption of connected and portable monitoring systems, is expected to continue stimulating market growth. In addition, government initiatives promoting maternal and neonatal health and the widespread integration of fetal monitoring with hospital IT systems are further supporting adoption across both public and private healthcare facilities.

Germany Fetal Monitoring Market Insight

The Germany fetal monitoring market is expected to expand at a considerable CAGR during the forecast period, fueled by the country’s advanced healthcare infrastructure and growing focus on maternal and neonatal safety. Hospitals and maternity clinics in Germany are investing in high-accuracy electronic fetal monitoring systems and telemetry solutions, emphasizing non-invasive and portable devices for maternal comfort. Integration of fetal monitors with hospital IT networks and telemedicine platforms is becoming increasingly prevalent, ensuring timely detection of complications. The German market also places strong emphasis on clinical efficiency, data reliability, and adherence to stringent healthcare standards, which supports adoption of technologically advanced fetal monitoring systems across both hospitals and prenatal care centers.

France Fetal Monitoring Market Insight

The France fetal monitoring market is poised to witness robust growth during the forecast period, driven by government policies supporting maternal health and high awareness of prenatal care. Hospitals and clinics are increasingly adopting electronic fetal monitors, ultrasound devices, and portable telemetry solutions to improve maternal and neonatal outcomes. The French market also benefits from rising demand for non-invasive monitoring and telemedicine-enabled solutions that allow continuous patient oversight and remote consultations. Integration of monitoring systems with hospital IT platforms enhances clinical decision-making and workflow efficiency. Growing investments in digital healthcare infrastructure and modernization of maternity care units are key factors propelling market expansion in France.

Italy Fetal Monitoring Market Insight

The Italy fetal monitoring market is experiencing steady growth, supported by increasing hospital investments in advanced maternal healthcare technologies. Italian hospitals and prenatal clinics are adopting electronic fetal monitoring systems, telemetry solutions, and portable devices to ensure continuous monitoring of fetal health and early detection of complications. Rising awareness of prenatal care benefits among expectant mothers and growing focus on reducing maternal and neonatal risk are driving adoption. Integration with telemedicine and hospital IT systems enhances clinical efficiency and remote patient monitoring capabilities. Government support and initiatives promoting maternal and child health are further encouraging investments in fetal monitoring infrastructure.

Europe Fetal Monitoring Market Share

The Europe Fetal Monitoring industry is primarily led by well-established companies, including:

- GE HealthCare (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Siemens Healthineers AG (Germany)

- Medtronic (Ireland)

- Mindray Bio Medical Electronics Co., Ltd. (China)

- FUJIFILM SonoSite, Inc. (U.S.)

- Natus Medical Incorporated (U.S.)

- CooperSurgical Inc. (U.S.)

- Analogic Corporation (U.S.)

- Edan Instruments, Inc. (China)

- Huntleigh Healthcare Limited (U.K.)

- Neoventa Medical AB (Sweden)

- Spacelabs Healthcare Inc. (U.S.)

- Bionet Co., Ltd. (South Korea)

- Contec Medical Systems Co., Ltd. (China)

- Trivitron Healthcare (India)

- MedGyn Products, Inc. (U.S.)

- OBMedical Company (U.S.)

- Bistos Co., Ltd. (South Korea)

- Progetti Srl (Italy)

What are the Recent Developments in Europe Fetal Monitoring Market?

- In April 2025, the ELAINE project supported by the Bern MedTech Collaboration Call announced advancements in prenatal care technology, focusing on the development of wearable and AI‑enhanced fetal monitoring solutions to improve maternal and fetal health tracking, reduce hospitalizations, and expand remote prenatal monitoring capabilities

- In April 2024, GE Healthcare launched its AI‑driven Voluson Signature 20 and 18 ultrasound systems, which enhance imaging accuracy in women’s health and contribute to improved fetal monitoring diagnostics across European healthcare facilities

- In March 2023, GE Healthcare introduced a new generation of maternal and fetal monitoring systems incorporating AI‑powered analytics, aimed at boosting diagnostic accuracy and workflow efficiency in fetal monitoring practices

- In July 2022, Siemens Healthineers unveiled the Acuson Juniper ultrasound system designed for enhanced prenatal diagnostics and maternal health monitoring, contributing to broader adoption of advanced fetal imaging technologies in European clinical environments

- In January 2022, Nuvo Group partnered with Charité – Universitätsmedizin Berlin to establish a remote fetal surveillance protocol in Europe and study predictive analytics for preeclampsia patients, aimed at enabling expectant mothers to conduct remote fetal and maternal monitoring from home under physician supervision and improving early identification of at‑risk pregnancies through advanced data analytics

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.