Europe Infertility Testing Market

Market Size in USD Billion

USD

1.63 Billion

USD

3.29 Billion

2025

2033

USD

1.63 Billion

USD

3.29 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.63 Billion | |

| USD 3.29 Billion | |

| % | |

|

Europe Infertility Testing Market Size

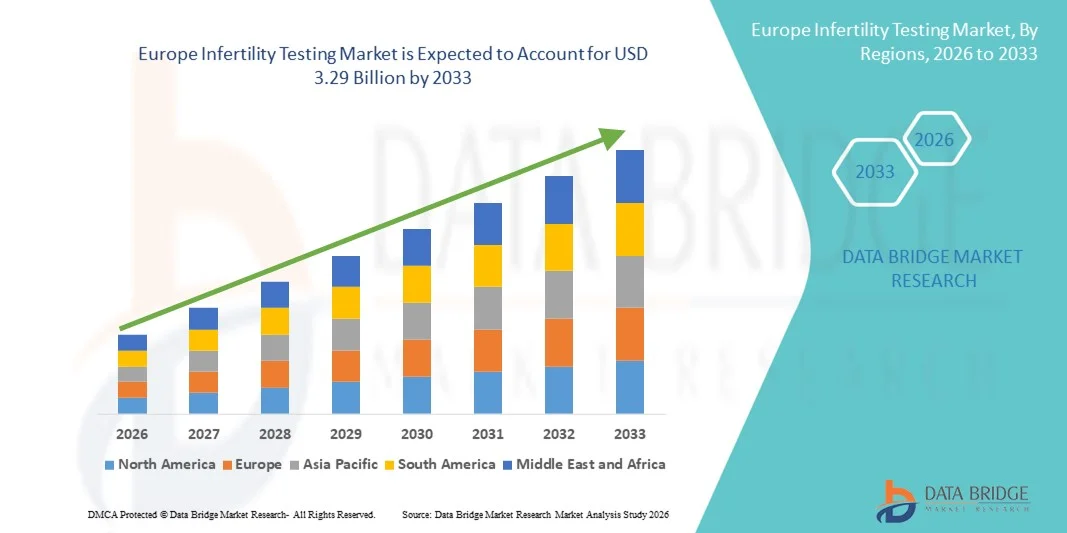

- The Europe infertility testing market size was valued at USD 1.63 billion in 2025 and is expected to reach USD 3.29 billion by 2033, at a CAGR of 9.2% during the forecast period

- The market growth is largely fueled by rising awareness of fertility health, increasing prevalence of infertility, and robust healthcare infrastructure across major European countries, which are driving the adoption of advanced infertility and fertility testing solutions

- Furthermore, growing consumer preference for early detection of fertility issues, continued technological advancements in diagnostic tools, and expanding distribution channels are boosting demand. These converging factors are strengthening the role of infertility testing as an essential component of reproductive health care, thereby significantly accelerating market expansion in Europe

Europe Infertility Testing Market Analysis

- Infertility testing, encompassing diagnostic solutions for both male and female reproductive health, is becoming increasingly essential in Europe due to rising infertility prevalence, growing awareness of reproductive health, and the adoption of advanced testing technologies in clinical and home settings

- The escalating demand for infertility testing is primarily driven by technological advancements in test kits, increasing focus on early detection of fertility issues, and a rising preference among couples for convenient, accurate, and non-invasive diagnostic solutions

- The United Kingdom dominated the Europe infertility testing market in 2025 with the largest revenue share of 22.5%, supported by well-established healthcare infrastructure, high consumer awareness, and widespread adoption of fertility diagnostics in private and public clinics

- Poland is expected to be the fastest-growing country in Europe infertility testing market during the forecast period fueled by improving healthcare access, rising awareness of reproductive health, and expanding availability of infertility testing solutions through hospitals, pharmacies, and online platforms

- Female infertility testing segment dominated the Europe infertility testing market in 2025 with a share of 58.9%, driven by strong demand for hormone-based ovulation and reproductive health test kits

Report Scope and Europe Infertility Testing Market Segmentation

|

Attributes |

Europe Infertility Testing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Europe Infertility Testing Market Trends

Advancements in AI and Hormone-Based Diagnostic Solutions

- A significant and accelerating trend in the Europe infertility testing market is the increasing incorporation of artificial intelligence (AI) and advanced hormone-based diagnostic tools such as FSH, LH, and HCG test kits, which are enhancing accuracy, convenience, and predictive capabilities for fertility monitoring

- For instance, AI-enabled ovulation prediction systems and integrated mobile apps allow users to track menstrual cycles, hormone fluctuations, and fertility windows with personalized recommendations, improving planning and diagnostic precision

- AI integration in infertility testing enables features such as predicting optimal conception periods, analyzing hormonal patterns over time, and sending intelligent alerts if irregularities are detected, while hormone-based blood and urine test kits offer non-invasive and reliable results for both clinical and home use

- The seamless integration of infertility testing with digital health platforms and fertility management apps facilitates centralized monitoring of reproductive health, enabling users and clinicians to manage test results, consultations, and treatment plans from a single interface

- This trend toward more intelligent, data-driven, and interconnected fertility solutions is fundamentally reshaping user expectations for reproductive health diagnostics, prompting companies such as Modern Fertility and Ava Health to develop AI-supported, hormone-based testing services with app-based insights

- The demand for infertility testing solutions that combine AI analytics, hormone monitoring, and user-friendly digital interfaces is growing rapidly across Europe, as couples increasingly prioritize early detection, personalized recommendations, and convenience in fertility planning

- Collaboration with telehealth providers and fertility clinics is increasing, enabling seamless integration of at-home testing with professional consultations, treatment planning, and follow-up care, enhancing patient engagement and market adoption

Europe Infertility Testing Market Dynamics

Driver

Growing Demand Due to Rising Infertility Awareness and Digital Health Adoption

- The increasing prevalence of infertility cases among couples and rising awareness of reproductive health, coupled with the accelerating adoption of digital health and diagnostic technologies, is a significant driver for the heightened demand for infertility testing

- For instance, in March 2025, Modern Fertility launched an AI-powered at-home hormone test kit integrated with a mobile app, enabling comprehensive fertility tracking and personalized insights for users, which is expected to drive market growth

- As consumers become more conscious of reproductive health and seek early detection solutions, infertility tests offer advanced features such as hormone monitoring, cycle prediction, and personalized health recommendations, providing a compelling alternative to traditional clinical testing alone

- Furthermore, the growing popularity of telemedicine and online fertility platforms, coupled with convenient at-home testing options, is making infertility tests an integral part of digital reproductive health management across clinics and households

- The convenience of at-home testing, mobile app integration, AI analytics, and access to prescription or OTC kits are key factors propelling the adoption of infertility testing in both clinical and home settings, while user-friendly test designs further contribute to market expansion

- Increasing investment by healthcare providers and private fertility clinics in advanced diagnostic tools is boosting market growth, as clinics seek to offer more comprehensive and data-driven fertility solutions to patients

- Government initiatives and public health campaigns promoting awareness about infertility and reproductive health screening are supporting wider adoption, particularly among couples planning pregnancies and in high-risk age groups

Restraint/Challenge

Regulatory Compliance and Accuracy Concerns

- Concerns surrounding regulatory compliance, clinical validation, and accuracy of home-based infertility test kits pose a significant challenge to broader market penetration, particularly for AI-supported digital solutions

- For instance, discrepancies in hormone readings or cycle predictions from unvalidated kits have made some consumers hesitant to adopt at-home testing solutions, preferring clinician-supervised diagnostics instead

- Addressing these regulatory and accuracy concerns through standardized clinical validations, robust testing protocols, and transparent reporting is crucial for building consumer trust, while companies such as Ava Health and Modern Fertility emphasize their validated methodologies and accuracy assurances in marketing materials

- In addition, the relatively higher cost of clinically validated AI-assisted infertility kits compared to traditional lab tests can be a barrier for price-sensitive consumers, even though basic test kits have become more affordable

- Overcoming these challenges through stricter regulatory adherence, consumer education on test reliability, and the development of cost-effective, validated kits will be vital for sustained growth of the Europe infertility testing market

- Limited awareness and knowledge gaps among consumers regarding proper usage, interpretation, and follow-up of at-home test results can hinder adoption and reduce the perceived value of infertility testing services

- Competition from traditional laboratory-based fertility diagnostics and unregulated online kits offering lower prices but questionable accuracy presents a challenge to market growth, requiring companies to differentiate through quality, clinical validation, and integrated digital solutions

Europe Infertility Testing Market Scope

The market is segmented on the basis of type, test kits, prescription mode, distribution channel, and end use.

- By Type

On the basis of type, the Europe infertility testing market is segmented into female infertility testing and male infertility testing. The female infertility testing segment dominated the market with the largest revenue share of 58.9% in 2025, driven by higher adoption of hormone-based ovulation and reproductive health tests. Women often prioritize these tests due to the ability to monitor ovulation, hormone levels, and menstrual cycles at home or in clinics. The market also sees strong demand for female infertility tests because of their integration with digital health apps and AI-based prediction tools, which enhance usability and accuracy. In addition, clinics and fertility centers in countries such as the UK, Germany, and France widely utilize female infertility tests for diagnosis, monitoring, and personalized treatment planning. The growing awareness of female reproductive health and accessibility of both prescription and OTC options further contribute to the dominance of this segment.

The male infertility testing segment is anticipated to witness the fastest growth rate of 12.5% CAGR from 2026 to 2033, fueled by increasing screening for sperm count, motility, and reproductive health. Male testing adoption is rising due to greater awareness of male-factor infertility and non-invasive at-home semen analysis kits. Advances in AI-assisted sperm quality analysis and easy-to-use test kits have simplified monitoring and diagnosis. Fertility clinics and research institutes are increasingly recommending male infertility testing alongside female tests for comprehensive evaluation. Digital health integration, smartphone-based reporting, and personalized insights are also driving adoption among tech-savvy users. Rising awareness campaigns and government support for reproductive health screening further accelerate growth in this segment.

- By Test Kits

On the basis of test kits, the market is segmented into FSH urine test kits, LH urine test kits, HCG hormone blood test kits, and others. The FSH urine test kits segment dominated the market with a share of 30% in 2025, due to its reliability in detecting hormonal imbalances and predicting ovulation cycles. Women frequently prefer FSH tests for early fertility monitoring and personalized family planning. Fertility clinics widely adopt FSH kits for diagnostic and treatment monitoring purposes. The ease of use, integration with mobile health platforms, and high accuracy rates contribute to strong market demand. Rising awareness of early fertility detection and availability in both prescription and OTC formats further strengthen dominance. The established clinical protocols and compatibility with fertility management apps also encourage repeat usage.

The LH urine test kits segment is expected to witness the fastest CAGR of 14.3% from 2026 to 2033, driven by their increasing adoption in at-home ovulation prediction. LH kits offer simplicity, rapid results, and integration with smartphone apps to provide personalized fertility insights. The segment benefits from growing awareness of ovulation tracking, convenience, and accuracy for conception planning. Fertility centers and online pharmacies are expanding distribution of LH kits, increasing accessibility for home users. Partnerships with telehealth providers and fertility apps enhance user engagement and predictive capabilities. Rising demand for cost-effective, reliable, and non-invasive kits further accelerates market growth.

- By Prescription Mode

On the basis of prescription mode, the market is segmented into prescription-based and over-the-counter (OTC) based tests. The prescription-based segment dominated with a market share of 65% in 2025, due to the preference for clinically validated, accurate diagnostics administered under medical supervision. Clinics and hospitals recommend prescription tests for precise hormonal evaluation and treatment planning. Patients value the reliability, follow-up consultation, and integration with fertility treatment programs. Availability of these tests in hospital labs and specialized fertility centers strengthens dominance. Prescription tests are also preferred for regulatory compliance and insurance coverage. Increasing infertility cases among women and men drive repeat testing and sustained market demand.

The OTC-based segment is projected to witness the fastest growth with a CAGR of 13.8% from 2026 to 2033, driven by rising at-home testing adoption. Users increasingly prefer convenience, privacy, and early monitoring without visiting clinics. Online pharmacies and retail channels make OTC kits widely accessible across Europe. Integration with mobile apps, AI insights, and user-friendly instructions enhances usability. Rising awareness campaigns, digital health literacy, and growing trust in validated OTC kits further accelerate adoption. Partnerships with telemedicine providers also contribute to rapid growth in this segment.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospitals, pharmacies, online pharmacies, and drug stores. The hospitals segment dominated the market in 2025 with a share of 48%, due to the extensive use of infertility testing in clinical diagnostics and treatment planning. Fertility clinics, hospitals, and specialized diagnostic centers rely on hospitals for access to validated test kits and professional supervision. Hospitals provide integrated services with AI-supported monitoring, consultations, and follow-ups. Established healthcare infrastructure in countries such as the UK, Germany, and France strengthens this segment. Availability of both male and female testing kits in hospitals ensures comprehensive fertility evaluation. Growing demand for accurate, supervised testing drives repeat usage and sustained market revenue.

The online pharmacies segment is expected to witness the fastest CAGR of 15.5% from 2026 to 2033, fueled by increasing digital adoption and preference for convenient, at-home access to test kits. Users benefit from discreet delivery, app integration, and telehealth support. Online pharmacies expand reach to remote and underserved areas. Partnerships with fertility apps and subscription services enhance engagement and retention. Convenience, accessibility, and growing trust in validated online kits further boost this segment. The increasing penetration of e-commerce platforms and digital health awareness in Europe also accelerates growth.

- By End Use

On the basis of end use, the market is segmented into fertility centers, hospitals and clinics, research institutes, and cryobanks. The fertility centers segment dominated the market in 2025 with a share of 52%, due to the high adoption of comprehensive testing solutions for couples seeking assisted reproductive technologies (ART) and IVF treatments. Fertility centers provide integrated services including AI-assisted analysis, counseling, and follow-up care. Clinics leverage both male and female tests to offer personalized treatment plans. Growing patient awareness of fertility preservation and early diagnosis drives market demand. Established centers in the UK, Germany, and France further strengthen this segment. Fertility centers also benefit from partnerships with test kit manufacturers and telehealth services.

The research institutes segment is expected to witness the fastest CAGR of 14.9% from 2026 to 2033, driven by increasing R&D activities in reproductive health, hormone-based diagnostics, and AI-assisted fertility monitoring. Institutes conduct clinical trials, validate test kits, and innovate predictive algorithms. Collaborations with hospitals, fertility centers, and technology providers accelerate adoption. The growing focus on improving fertility outcomes and advancing reproductive technologies fuels market growth. Government and private funding for infertility research further support expansion. Adoption of advanced lab-based and at-home research-oriented kits also contributes to growth.

Europe Infertility Testing Market Regional Analysis

- The United Kingdom dominated the Europe infertility testing market in 2025 with the largest revenue share of 22.5%, supported by well-established healthcare infrastructure, high consumer awareness, and widespread adoption of fertility diagnostics in private and public clinics

- Consumers in the region highly value accuracy, early detection, and convenience offered by infertility testing solutions, including hormone-based FSH, LH, and HCG kits, which can be used at home or in clinical settings for comprehensive reproductive health monitoring

- This widespread adoption is further supported by strong healthcare networks, government initiatives promoting fertility awareness, and a growing preference for digital health tools and AI-assisted diagnostic solutions, establishing infertility testing as a preferred choice for couples seeking fertility evaluation and planning

The U.K. Infertility Testing Market Insight

The U.K. infertility testing market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the escalating focus on fertility awareness and the desire for early detection and personalized reproductive health solutions. In addition, increasing infertility cases and consumer preference for convenient at-home and prescription-based tests are encouraging both individuals and clinics to adopt infertility testing. The U.K.’s advanced healthcare infrastructure, robust fertility clinics, and strong online pharmacy network are expected to continue supporting market expansion.

Germany Infertility Testing Market Insight

The Germany infertility testing market is expected to expand at a considerable CAGR during the forecast period, fueled by growing awareness of reproductive health, the adoption of technologically advanced diagnostic kits, and a focus on precision fertility monitoring. Germany’s well-developed healthcare infrastructure, high disposable income, and emphasis on innovation promote the adoption of both clinical and at-home infertility tests. Fertility centers and hospitals increasingly integrate AI-assisted and hormone-based test kits for comprehensive fertility evaluation, aligning with local expectations for reliability and accuracy.

France Infertility Testing Market Insight

The France infertility testing market is gaining momentum due to the country’s advanced healthcare system, rising infertility prevalence, and increasing acceptance of at-home and clinic-based fertility testing. French consumers highly value early detection and personalized reproductive insights, driving adoption of hormone-based and AI-assisted test kits. Integration with telehealth platforms and fertility management apps is expanding access and convenience. The government’s reproductive health initiatives and growing fertility clinic network further support market growth.

Poland Infertility Testing Market Insight

The Poland infertility testing market is expected to witness the fastest CAGR during the forecast period, fueled by increasing awareness of reproductive health, improving healthcare access, and rising adoption of hormone-based and digital fertility diagnostic tools. Both home-use and clinical testing solutions are becoming popular due to ease of use, accuracy, and integration with fertility apps. Expansion of online pharmacies, telemedicine services, and fertility clinics enhances accessibility. Rising demand for affordable yet reliable testing kits further drives rapid market growth.

Europe Infertility Testing Market Share

The Europe Infertility Testing industry is primarily led by well-established companies, including:

- EKF Diagnostics Holdings plc (U.K.)

- Vitrolife Group (Sweden)

- Diasorin S.p.A. (Italy)

- SYNLAB International GmbH (Germany)

- Igenomix (Spain)

- Profertility Ltd. (U.K.)

- Hertility Health Ltd. (U.K.)

- IVI Fertility (Spain)

- FutureLife Group (Czech Republic)

- Enhanced Fertility (U.K.)

- GoFertile (Europe)

- Institut Marquès (Spain)

- Bourn Hall Clinic (U.K.)

- iVF Riga Fertility Clinic (Latvia)

- Embryolab (Greece)

- Medical Electronic Systems (Europe)

- Swiss Precision Diagnostics GmbH (Switzerland)

- International Biosciences (U.K.)

- Proov Test (Europe)

- GoFertile (Europe)

What are the Recent Developments in Europe Infertility Testing Market?

- In December 2025, Enhanced Fertility, a UK‑Portugal startup, announced its AI‑powered digital platform that dramatically reduces infertility diagnosis time from years to under 30 days. The platform combines at‑home testing, clinic diagnostics, and personalized treatment planning, expanding across the EU

- In November 2025, the World Health Organization (WHO) issued its first global guideline on infertility prevention, diagnosis, and treatment, urging countries including EU member states to integrate evidence‑based fertility care into health systems to improve access and affordability. This landmark guideline covers clinical pathways for diagnosing male and female infertility, prevention strategies, and the need for psychosocial support

- In November 2025, Overture Life received CE Mark approval to commercialize its automated IVF and fertility automation platform DaVitri in Europe, marking the first regulatory clearance in the EU and U.K. for a device that automates the vitrification (freezing) of unfertilized eggs and supports reproductive treatments.

- In March 2025, Modern Fertility launched an at‑home hormonal fertility test kit for men, broadening the traditionally female‑focused infertility diagnostic landscape and reflecting growing awareness of male‑factor infertility across European markets

- In October 2023, Enhanced Fertility officially launched its at‑home fertility test kits in Europe after obtaining a CE mark, enabling fertility clinics across the region to request tests for international patients. The launch was commemorated with a professional webinar demonstrating the tests to healthcare providers

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.