Europe Lung Cancer Therapeutics Market

Market Size in USD Billion

USD

2.33 Billion

USD

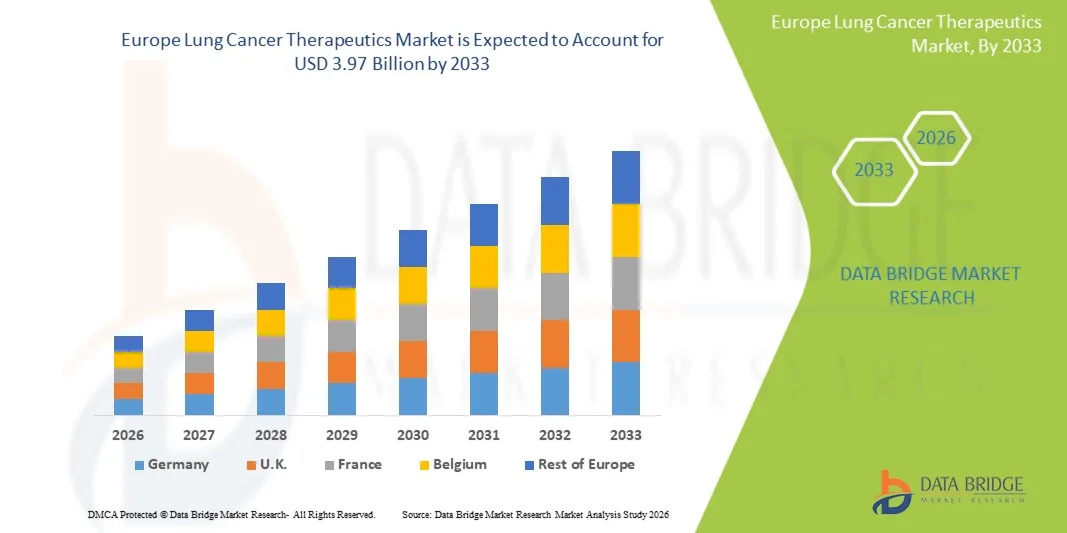

3.97 Billion

2025

2033

USD

2.33 Billion

USD

3.97 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.33 Billion | |

| USD 3.97 Billion | |

| % | |

|

Europe Lung Cancer Therapeutics Market Size

- The Europe Lung Cancer Therapeutics Market size was valued at USD 2.33 billion in 2025 and is expected to reach USD 3.97 billion by 2033, at a CAGR of 6.90% during the forecast period

- The market growth is largely fueled by the increasing prevalence of lung cancer worldwide, coupled with advancements in diagnostic technologies and targeted treatment options. Rising awareness of early detection, coupled with the integration of precision medicine and biomarker-based therapies, is driving the adoption of innovative lung cancer therapeutics across both developed and emerging regions. Moreover, growing investments in oncology research and expanding healthcare infrastructure are further supporting the market’s expansion

- Furthermore, the rising demand for personalized treatment solutions, along with continuous advancements in immunotherapy and targeted drug development, is establishing lung cancer therapeutics as a critical segment within the oncology industry. These converging factors—supported by favorable regulatory approvals, increased R&D funding, and strategic collaborations among pharmaceutical companies—are accelerating the uptake of advanced lung cancer therapies, thereby significantly boosting the industry’s overall growth

Europe Lung Cancer Therapeutics Market Analysis

- Lung cancer therapeutics, encompassing targeted therapies, immunotherapies, and chemotherapy agents, have become vital components of modern oncology treatment due to their improved efficacy, precision, and survival outcomes. The integration of molecular diagnostics and biomarker testing has revolutionized treatment selection, enabling personalized approaches that enhance patient response and reduce side effects

- The escalating demand for advanced lung cancer treatments is primarily fueled by the increasing global incidence of lung cancer, rising awareness regarding early diagnosis, and growing investments in oncology research. In addition, favorable reimbursement frameworks and the approval of novel drugs by regulatory authorities are supporting widespread adoption across healthcare systems worldwide

- The U.K. dominated the Europe Lung Cancer Therapeutics Market with the largest revenue share of 23.9% in 2025, supported by its robust healthcare infrastructure, rapid adoption of targeted and immune-based therapies, and favorable government initiatives toward early cancer detection

- Germany is expected to be the fastest-growing market for lung cancer therapeutics during the forecast period, with an anticipated CAGR of 16.7% from 2026 to 2033. Growth is primarily attributed to the increasing prevalence of lung cancer cases, rapid expansion of oncology centers, and government-backed initiatives promoting cancer awareness and screening programs

- The Small Molecules segment dominated with a revenue share of 61.4% in 2025. Small molecules’ leadership is due to their established role in targeted therapies, oral dosing convenience, and broad clinical experience across many lung cancer subtypes

Report Scope and Europe Lung Cancer Therapeutics Market Segmentation

|

Attributes |

Europe Lung Cancer Therapeutics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Europe Lung Cancer Therapeutics Market Trends

“Enhanced Convenience Through AI and Precision Medicine Integration”

- A significant and accelerating trend in the Europe Lung Cancer Therapeutics Market is the deepening integration of artificial intelligence (AI) and precision medicine platforms, revolutionizing the diagnosis, treatment personalization, and overall management of lung cancer. This convergence of technologies is significantly improving patient outcomes, treatment accuracy, and clinical decision-making processes

- For instance, AI-driven imaging tools are increasingly being utilized to detect lung tumors at earlier stages by analyzing CT scans with greater accuracy and speed than traditional radiological methods. Similarly, precision oncology platforms such as Tempus and Foundation Medicine enable the identification of specific genetic mutations, allowing clinicians to select the most effective targeted therapies for individual patients

- The use of AI in lung cancer therapeutics extends to predicting treatment response, optimizing drug combinations, and detecting potential resistance mutations before clinical symptoms emerge. For example, AI algorithms integrated into oncology research platforms can process vast genomic datasets to recommend adaptive treatment strategies and enhance patient monitoring. Furthermore, digital health tools and voice-assisted platforms are streamlining communication between patients and healthcare providers, ensuring consistent treatment adherence and timely symptom reporting

- The seamless integration of AI with hospital information systems, electronic health records, and clinical trial databases is facilitating more efficient data sharing and accelerating the pace of research and clinical development. Through unified data platforms, oncologists can now access real-time insights on patient progress, enabling faster and more informed treatment adjustments

- This trend toward more intelligent, data-driven, and interconnected therapeutic solutions is fundamentally reshaping expectations in cancer care. Consequently, leading biopharmaceutical companies such as Roche, AstraZeneca, and Merck & Co. are investing heavily in AI-enabled drug discovery, real-world data analytics, and adaptive clinical trials to enhance therapeutic efficacy and improve survival outcomes for lung cancer patients

- The demand for personalized, AI-assisted lung cancer treatment approaches is expanding rapidly across both developed and emerging markets as healthcare systems increasingly prioritize precision, cost-efficiency, and improved patient experiences

Europe Lung Cancer Therapeutics Market Dynamics

Driver

“Growing Need for Targeted and Immuno-Oncology Therapies”

- The rising global incidence of lung cancer and the shift toward precision medicine approaches are key drivers fueling the growth of the Europe Lung Cancer Therapeutics Market. Targeted therapies and immuno-oncology drugs have transformed treatment paradigms, offering improved survival rates and fewer side effects compared to traditional chemotherapy

- For instance, in April 2025, AstraZeneca announced the advancement of its next-generation EGFR inhibitor in Phase III clinical trials, aimed at addressing resistance mutations in non-small cell lung cancer (NSCLC) patients. Such strategic developments by major players are expected to significantly propel market growth during the forecast period

- As the understanding of tumor biology and genomic profiling deepens, clinicians are increasingly adopting biomarker-based treatment selection, which improves therapeutic precision and patient response rates. Furthermore, ongoing innovations in PD-1/PD-L1 inhibitors and combination immunotherapies continue to expand the range of options available for previously untreatable cases of lung cancer

- The rising demand for early diagnostic tools, liquid biopsy technologies, and companion diagnostics further enhances treatment efficiency, while the expansion of reimbursement coverage for targeted and immunotherapy drugs is making these treatments more accessible. The global healthcare community’s growing focus on personalized treatment regimens is therefore a major force driving the evolution of the Europe Lung Cancer Therapeutics Market

Restraint/Challenge

“High Treatment Costs and Limited Accessibility in Developing Regions”

- Despite significant therapeutic advancements, the high cost of lung cancer treatment remains a major barrier to widespread adoption, particularly in low- and middle-income countries. Targeted therapies and immuno-oncology drugs often come with premium pricing due to their complex manufacturing and research requirements, making affordability a key concern for patients and healthcare providers

- For instance, reports from oncology associations indicate that many patients in developing regions still rely on conventional chemotherapy due to the limited availability and high price of advanced biologics and targeted drugs. In addition, disparities in healthcare infrastructure and diagnostic capabilities further restrict the timely detection and treatment of lung cancer

- Addressing these challenges through cost-effective biosimilar launches, expanded patient assistance programs, and broader reimbursement initiatives is essential for improving accessibility. Companies such as Bristol Myers Squibb and Roche are investing in programs to enhance affordability and reach underserved populations, while governments and NGOs are emphasizing early screening and awareness campaigns

- Furthermore, the complexity of regulatory approvals and the lengthy clinical trial process can delay the introduction of innovative therapies in emerging markets. Overcoming these hurdles through policy reforms, collaborative research initiatives, and enhanced healthcare funding will be vital for ensuring equitable access to advanced lung cancer therapeutics worldwide

- While prices are gradually stabilizing and biosimilars are entering the market, the cost burden still poses a restraint for widespread adoption. Increasing global collaboration among pharmaceutical companies, policymakers, and healthcare organizations will be key to ensuring sustainable growth and broader accessibility in the Europe Lung Cancer Therapeutics Market

Europe Lung Cancer Therapeutics Market Scope

The market is segmented on the basis of cancer type, molecule type, drug class, treatment type, therapy type, end user, and distribution channel.

• By Cancer Type

On the basis of cancer type, the Europe Lung Cancer Therapeutics Market is segmented into Non-Small Cell Lung Cancer (NSCLC), Metastatic Lung Cancer, Pulmonary Neuroendocrine Tumors, Mediastinal Tumors, Mesothelioma, and Chest Wall Tumors. The Non-Small Cell Lung Cancer (NSCLC) segment dominated the market with the largest revenue share of 58.6% in 2025. NSCLC’s dominance stems from its very high global prevalence and the large, well-defined pool of patients who benefit from targeted and immune-based therapies. Breakthroughs in molecular diagnostics have enabled widespread identification of actionable mutations in NSCLC, which in turn drives prescription of precision drugs. Approved targeted agents for EGFR, ALK, ROS1 and KRAS mutations have significantly improved progression-free and overall survival in this cohort. The strong pipeline of next-generation targeted agents and combination regimens continues to expand therapeutic choices for NSCLC. Major pharma investments and numerous ongoing global clinical trials further consolidate NSCLC’s market leadership. Reimbursement coverage in developed markets and improving access in emerging markets sustain high uptake. Physician familiarity with NSCLC treatment algorithms and established diagnostic pathways also expedite therapy adoption. Patient advocacy and screening programs have increased early diagnosis rates in some regions, supporting volume demand for NSCLC treatments. Health systems prioritize NSCLC due to its clinical burden, which attracts greater R&D and commercial focus. Overall, clinical evidence, market investment, diagnostics, and a large patient base combine to keep NSCLC as the dominant cancer-type segment.

The Metastatic Lung Cancer segment is projected to witness the fastest CAGR of 13.7% from 2026 to 2033. Growth is driven by the rising number of patients diagnosed at advanced stages and by better systemic therapies that meaningfully extend survival in metastatic settings. Advances in immunotherapy and targeted combinations that address resistance mechanisms are creating new treatment options for metastatic disease. Expanded access to genomic profiling allows oncologists to tailor treatments even in late-stage disease, improving outcomes and uptake. Palliative and supportive care improvements increase the number of patients eligible for systemic interventions. Regulatory approvals for late-line therapies and broader reimbursement for novel agents also enhance market expansion. The unmet need in metastatic disease attracts significant clinical trial activity and investment, accelerating the introduction of innovative agents. In addition, real-world evidence demonstrating improved quality of life with newer regimens supports wider adoption in metastatic care, further boosting CAGR.

• By Molecule Type

On the basis of molecule type, the Europe Lung Cancer Therapeutics Market is segmented into Small Molecules and Biologics. The Small Molecules segment dominated with a revenue share of 61.4% in 2025. Small molecules’ leadership is due to their established role in targeted therapies, oral dosing convenience, and broad clinical experience across many lung cancer subtypes. Well-known tyrosine kinase inhibitors (TKIs) such as osimertinib, gefitinib and erlotinib are staples in NSCLC regimens and have large patient populations. Small molecules are often less costly to manufacture and distribute than complex biologics, increasing access in many regions. Their pharmacokinetic profiles and ability to penetrate solid tumors make them clinically attractive for intracellular targets. The availability of generics for some agents further supports volume uptake in emerging markets. Ongoing development of next-generation small molecule inhibitors addressing resistance mutations sustains continual adoption. Physicians are comfortable prescribing small molecules due to long-term safety and effectiveness data. Health systems favor these therapies in many guideline-directed settings, reinforcing market share. Commercial strategies by manufacturers, including lifecycle management and label expansions, also protract small molecule dominance.

The Biologics segment is expected to expand at the fastest CAGR of 14.2% from 2026 to 2033. This rapid growth is led by immune checkpoint inhibitors, monoclonal antibodies, antibody-drug conjugates (ADCs), and other complex biologics that have demonstrated durable responses in many lung cancer patients. Increased investment in biologic R&D and an expanding approvals pipeline are driving adoption. Biologics often deliver profound survival benefits and new mechanisms of action, making them high-value therapies in oncology portfolios. The growing development of biosimilars is improving affordability and access, supporting faster uptake. Moreover, combining biologics with other modalities is unlocking novel regimens that further boost demand. Reimbursement support for high-impact biologics in major markets accelerates penetration. Clinician preference for immunotherapy as a standard of care in many settings continues to propel biologics’ growth trajectory.

• By Drug Class

On the basis of drug class, the Europe Lung Cancer Therapeutics Market is segmented into Alkylating Agents, Antimetabolites, EGFR Inhibitors, Mitotic Inhibitors, Multikinase Inhibitors, and Others. The EGFR Inhibitors segment held the dominant revenue share of 37.9% in 2025. EGFR inhibitors are dominant because EGFR mutations are among the most actionable and widely tested abnormalities in NSCLC, and approved EGFR agents have well-established survival benefits. Drugs such as osimertinib and gefitinib are commonly used in first-line and subsequent lines where mutations are present, creating substantial treated populations. The segment benefits from routine EGFR mutation screening, which channels patients into targeted therapies. Next-generation EGFR inhibitors that overcome resistance mutations have reinforced clinical utility and market share. Clinical guidelines strongly endorse EGFR testing and targeted treatment, which supports adoption across treatment centers. Favorable safety profiles vs. cytotoxic chemotherapy also promote clinician preference. Pharmaceutical companies continue to invest in improving EGFR inhibitor profiles and in developing combination regimens, maintaining their market leadership. Robust real-world effectiveness data further underpin payer support and physician adoption. Global regulatory approvals across regions increase accessibility and bolster revenue contributions from this drug class.

The Multikinase Inhibitors segment is predicted to register the fastest CAGR of 13.4% from 2026 to 2033. Multikinase inhibitors are gaining momentum because they can simultaneously target multiple oncogenic and angiogenesis pathways, which is valuable in resistant and heterogeneous tumors. These agents are increasingly tested in combination with immunotherapies and other targeted drugs to overcome single-target resistance. Advances in molecular profiling help identify patients most likely to benefit from multikinase approaches, improving clinical outcomes and uptake. Continued pipeline activity and new approvals for multitarget compounds are expanding clinical indications. The advantage of multi-pathway inhibition in refractory or metastatic cases makes these drugs attractive for complex treatment algorithms. Academic and industry combination trials further validate efficacy and increase adoption. Improved formulations and dosing strategies aimed at minimizing toxicity are enhancing tolerability and market appeal.

• By Treatment Type

On the basis of treatment type, the Europe Lung Cancer Therapeutics Market is segmented into Chemotherapy, Radiation Therapy, Targeted Therapy, Immunotherapy, and Others. The Targeted Therapy segment dominated with a 42.1% share in 2025, reflecting the shift toward precision oncology and treatment guided by molecular biomarkers. Targeted agents deliver superior progression-free survival for patients with specific mutations and are increasingly used in early and advanced settings. The proliferation of companion diagnostics and wider availability of genomic testing has reinforced targeted therapy uptake. Pharmaceutical pipelines focused on novel targets (ALK, ROS1, BRAF, MET, RET) continuously expand the repertoire of precision options. Targeted treatments are often better tolerated than conventional chemotherapy, improving quality of life and adherence. Health systems are investing in diagnostic infrastructure to support targeted approaches, which further drives market share. Reimbursement policies in many developed markets favor evidence-backed targeted regimens, enhancing access. Clinical guidelines now incorporate molecular testing and targeted therapy pathways, standardizing care and reinforcing dominance. Ongoing label expansions and combination studies maintain momentum for targeted modalities.

The Immunotherapy segment is forecasted to show the fastest CAGR of 15.3% from 2026 to 2033. Immunotherapy’s rapid growth follows landmark successes with checkpoint inhibitors that produce durable responses in subsets of patients. Continued breakthroughs in novel immune targets, bispecific antibodies and cell therapies broaden clinical applicability. Combination strategies pairing immunotherapy with targeted agents or chemotherapy are producing improved response rates. Expanding biomarker research (beyond PD-L1) is refining patient selection and boosting responder rates. Regulatory approvals and guideline incorporations for immunotherapies in first- and later-line settings continue to multiply. Investment in manufacturing capacity and improved cost-effectiveness through biosimilars and value-based reimbursement models supports wider uptake. Real-world effectiveness and long-term survival data drive clinician confidence and accelerate adoption globally.

• By Therapy Type

On the basis of therapy type, the Europe Lung Cancer Therapeutics Market is segmented into Single Drug Therapy and Combination Therapy. The Combination Therapy segment dominated with a share of 55.8% in 2025, reflecting the clinical reality that combining modalities (chemotherapy + targeted agents, or immunotherapy + targeted) often yields superior tumor control. Combination regimens have become standard in many first-line settings due to demonstrated survival advantages in randomized trials. The segment’s dominance is supported by robust clinical evidence, guideline endorsements, and broad physician acceptance. Pharmaceutical partnerships and co-development agreements have expanded combination portfolios and accelerated regulatory filings. Combination approaches help mitigate resistance mechanisms and provide multi-pronged tumor suppression. Health systems increasingly reimburse evidence-based combination regimens in high-impact indications, facilitating uptake. Adoption of combination therapy in advanced and metastatic settings is particularly high, translating to substantial market revenues. Patient outcomes improvements and expanded indications for combined modalities sustain their leading role across treatment lines.

The Single Drug Therapy segment is anticipated to record the fastest CAGR of 11.9% from 2026 to 2033. Growth in monotherapy is driven by the approval of highly specific single-agent drugs with favorable efficacy and tolerability for defined patient subgroups. Monotherapies are attractive in maintenance settings, elderly patients, or where combination toxicity is a concern. The lower complexity of administration and reduced monitoring requirements make single-agent use appealing in resource-constrained contexts. Continued discovery of novel targets enabling effective monotherapy options fuels adoption. Economic considerations and simplified reimbursement pathways also support monotherapy growth, especially where cost-effectiveness has been demonstrated. Real-world evidence that certain single agents provide durable control in selected patients further cements their use.

• By End User

On the basis of end user, the Europe Lung Cancer Therapeutics Market is segmented into Hospitals, Homecare, Specialty Clinics, and Others. The Hospitals segment dominated with the largest share of 64.3% in 2025, because hospitals provide comprehensive oncology services including diagnostics, infusion centers, radiation suites, and multidisciplinary teams required for complex lung cancer care. Hospitals also host most clinical trials and have the infrastructure for safe administration of cytotoxic and biologic therapies. Government and private payor reimbursements often flow through hospital settings, supporting higher treatment volumes and centralized procurement. The integrated care pathways in hospitals facilitate rapid diagnosis, staging, and initiation of therapy, contributing to high patient throughput. Advanced hospitals attract referrals for complex cases, further strengthening utilization of high-value lung cancer therapeutics. Training programs and specialist concentration within hospitals sustain expertise and adoption of new regimens. Expansion of oncology departments and investments in cancer centers globally continue to underpin hospital dominance. Hospitals are also focal points for biomarker testing and multidisciplinary tumor boards, which drive targeted therapy uptake.

The Specialty Clinics segment is expected to experience the fastest CAGR of 12.8% from 2026 to 2033. Specialty oncology clinics are expanding due to demand for outpatient, patient-centric care that offers faster access and personalized management. These clinics often focus on infusion services and targeted therapy delivery with streamlined appointment systems. Cost efficiencies and convenience for patients, particularly in non-acute settings, make specialty clinics attractive. Partnerships with pharma for sponsored programs and local payer contracting enhance service offerings. The shift toward outpatient administration of many modern therapies supports specialty clinic growth. Expanding networks of such clinics in urban and suburban areas increase accessibility and patient choice, accelerating adoption rates.

• By Distribution Channel

On the basis of distribution channel, the Europe Lung Cancer Therapeutics Market is segmented into Hospital Pharmacy, Retail Pharmacy, Online, and Others. The Hospital Pharmacy segment held the largest share of 53.6% in 2025, because hospital pharmacies manage procurement, cold-chain storage, and dispensing of complex oncology drugs requiring clinical oversight and immediate availability for inpatient and infusion use. Centralized hospital pharmacy systems also coordinate medication safety, dosing, and clinical pharmacy services that improve therapeutic outcomes. Bulk purchasing agreements and tendering by hospitals ensure stable supply and often favorable pricing for high-cost therapies. Hospital pharmacies’ integration with electronic medical records facilitates prescribing, administration, and monitoring workflows for cancer therapeutics. This channel’s control over in-house oncology inventory is essential for timely care delivery and clinical trial support. The strategic role of hospital pharmacies in cancer centers makes them the dominant distribution channel.

The Online Pharmacy segment is anticipated to grow at the fastest CAGR of 14.9% from 2026 to 2033. Growth drivers include increasing telemedicine adoption, expansion of e-prescription frameworks, patient preference for home delivery of chronic oral oncology agents, and improvements in regulatory support for online drug sales. Online channels reduce geographic access barriers and provide competitive pricing and subscription delivery models that appeal to patients managing long-term therapies. Integration with teleconsultation and home nursing services further enhances convenience and adherence. Expansion of secure, compliant online pharmacy platforms and partnerships with clinics and hospitals are accelerating channel adoption globally.

Europe Lung Cancer Therapeutics Market Regional Analysis

- The Europe Lung Cancer Therapeutics Market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by the rising incidence of lung cancer and the increasing adoption of advanced targeted and immunotherapy treatments

- The region’s strong focus on precision medicine, supported by government healthcare initiatives and growing investments in oncology research, is significantly contributing to market expansion. Furthermore, the availability of well-established healthcare infrastructure and the rapid integration of AI-assisted diagnostic systems are enhancing early detection and treatment efficiency

- European nations are also witnessing increased collaborations between pharmaceutical companies and research institutions to accelerate drug discovery and clinical trials. The growing geriatric population and rising environmental risk factors, such as pollution and smoking prevalence, are further propelling the market across major economies including Germany, France, Italy, and the U.K.

U.K. Europe Lung Cancer Therapeutics Market Insight

The U.K. Europe Lung Cancer Therapeutics Market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the increasing demand for personalized medicine and innovative treatment modalities. The country’s National Health Service (NHS) continues to promote early screening programs and molecular testing to identify genetic mutations, enabling the use of targeted therapies and immuno-oncology drugs for improved patient outcomes. The strong presence of global pharmaceutical leaders and continuous regulatory support for novel oncology treatments are boosting clinical advancements in the region. Furthermore, rising public awareness campaigns about early diagnosis and the availability of reimbursement for advanced therapies are accelerating adoption rates. The U.K.’s growing focus on digital health integration and the use of real-world evidence in treatment decisions are expected to sustain its market momentum.

Germany Europe Lung Cancer Therapeutics Market Insight

The Germany Europe Lung Cancer Therapeutics Market is expected to expand at a considerable CAGR during the forecast period, fueled by the nation’s advanced healthcare infrastructure, rising research collaborations, and high adoption of next-generation cancer therapies. Germany is at the forefront of precision oncology in Europe, with a strong emphasis on molecular diagnostics, biomarker testing, and targeted therapy combinations. Increasing government and private sector investments in oncology R&D, along with the expansion of clinical trial networks, are fostering innovation in lung cancer treatment. Moreover, the growing use of immunotherapies, particularly PD-1 and PD-L1 inhibitors, is significantly improving survival outcomes among patients. The country’s focus on sustainable healthcare delivery and technological advancement continues to reinforce its leadership position in the European Europe Lung Cancer Therapeutics Market.

Europe Lung Cancer Therapeutics Market Share

The Lung Cancer Therapeutics industry is primarily led by well-established companies, including:

- AstraZeneca (U.K.)

- Bristol Myers Squibb (U.S.)

- Merck & Co., Inc. (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- Lilly (U.S.)

- Amgen Inc. (U.S.)

- Takeda Pharmaceutical Company Limited (Japan)

- Sanofi S.A. (France)

- Boehringer Ingelheim International GmbH (Germany)

- Johnson & Johnson (U.S.)

- AbbVie Inc. (U.S.)

- GlaxoSmithKline plc (U.K.)

- Daiichi Sankyo Company, Limited (Japan)

- Astellas Pharma Inc. (Japan)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- Blueprint Medicines Corporation (U.S.)

- BeiGene Ltd. (China)

- Innovent Biologics, Inc. (China)

Latest Developments in Europe Lung Cancer Therapeutics Market

- In December 2021, the European Medicines Agency (EMA) granted conditional marketing authorisation for Rybrevant (amivantamab) for the treatment of advanced non-small cell lung cancer (NSCLC) with EGFR exon 20 insertion mutations. This approval marked a major advancement in targeted therapy options available to patients across Europe

- In November 2022, several new lung cancer therapies, including next-generation immunotherapies and targeted drugs, received indication extensions from the EMA, broadening access to precision medicines for European patients and reinforcing the region’s leadership in early adoption of innovative cancer treatments

- In March 2024, AstraZeneca announced positive results from its FLAURA2 trial, demonstrating that TAGRISSO (osimertinib) in combination with chemotherapy significantly improved progression-free survival in patients with EGFR-mutated advanced NSCLC. These findings strengthened the company’s regulatory position for expanded use across Europe

- In April 2024, the EMA’s Committee for Medicinal Products for Human Use (CHMP) issued a positive opinion recommending an indication extension for Rybrevant® (amivantamab), reflecting growing confidence in bispecific antibody therapies for EGFR-mutated NSCLC across European markets

- In December 2024, the European Commission approved the combination of RYBREVANT (amivantamab) with LAZCLUZE (lazertinib) as a first-line treatment for adults with EGFR-mutated advanced NSCLC. This marked a major milestone in Europe’s transition toward combination targeted therapies

- In December 2024, AstraZeneca secured regulatory approval in the European Union for TAGRISSO (osimertinib) as the first EGFR inhibitor authorised for the treatment of locally advanced, unresectable lung cancer, expanding its clinical utility beyond metastatic disease and setting a new regional treatment benchmark

- In January 2025, Henlius Biotech received European Commission approval for Serplulimab, an anti-PD-1 immunotherapy, in combination with carboplatin and etoposide for the first-line treatment of extensive-stage small-cell lung cancer (ES-SCLC). This launch added a novel immunotherapy option for European clinicians treating SCLC patients

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.